Thanks for sharing the interview. There is a lot to learn if we take this with the earnings call that happened a few days ago. As I’m relying on memory, please double check all statements with the transcript when released.

What was the impact of the second wave?

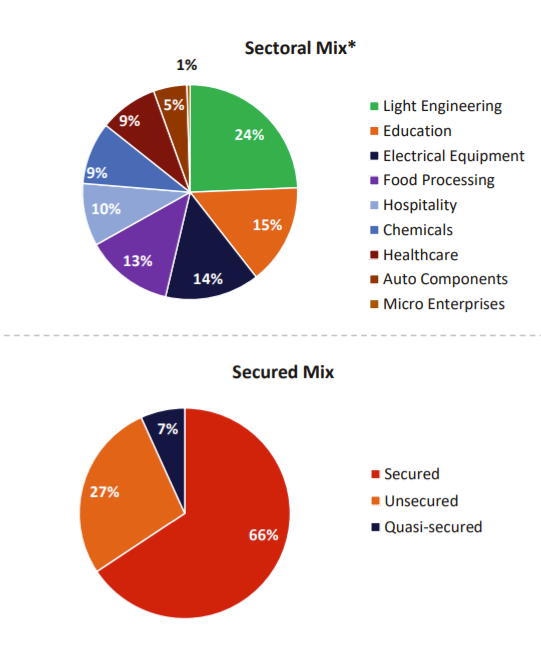

Mr. Pandey tells us that out of the 8 sectors that they’ve chosen, education and hospitality were impacted the most due to the pandemic. This translates to 25% of their loan book, but is more nuanced since different channels (Tier I vs Tier IV towns) saw different impacts from the pandemic.

On the concall, they told us that bounce rates were up in late April and May, there was a drop in collection efficiency, and they are expecting a pick up from July onwards. This is in line with what other NBFCs have been saying, and Mr. Pandey expects education to pick up once schools open, as expansion plans have been deferred for a long time.

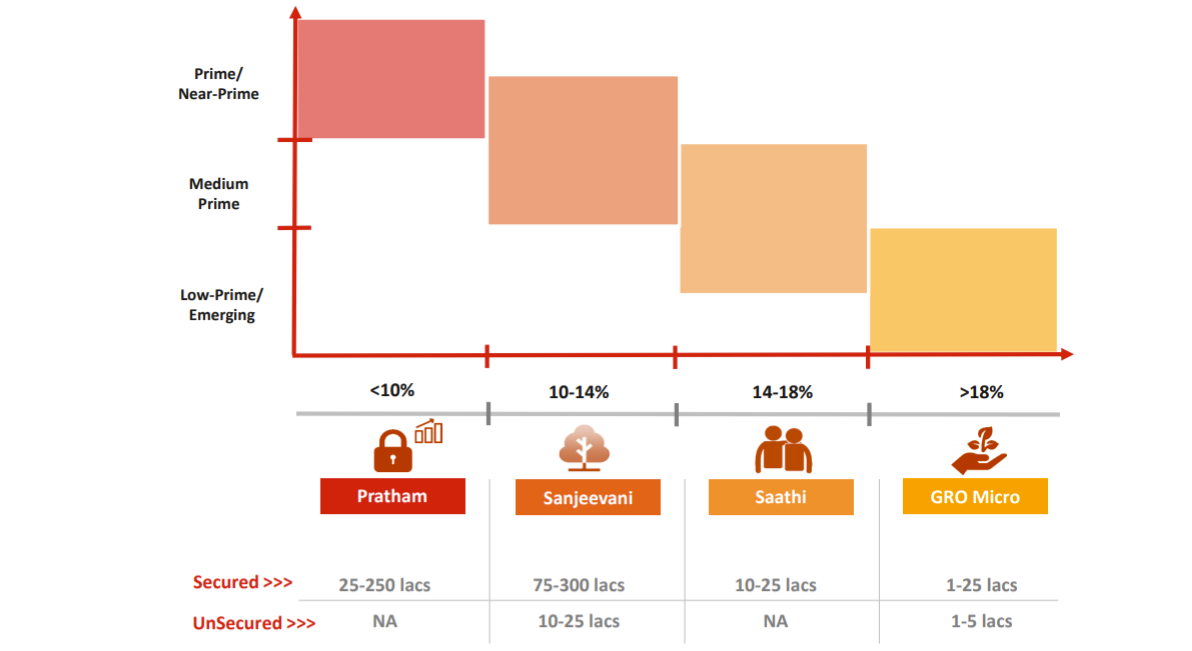

As far as the Sanjeevani loans go, it shouldn’t worry us as much as if they said they’re suddenly handing out the high yield GRO Micro loans.

On the concall, Mr. Nath explained his take on why small finance banks like Equitas and Ujjivan ran into problems with unsecured loans, and how they’re making sure to keep a check on this through position sizing.

What are they planning going ahead?

On the concall, they explained that they want to be patient with their new offerings that are coming into play (co lending with ICICI/SBI) and don’t want to make the mistake of being aggresive before we know a definite answer on the possibility of a future third wave.

A question often discussed in this thread is whether they really have a technology moat. The takeaway I got from both the concall and this interview with Mr. Pandey is that we should look at them as having a people / management moat. On the concall, they mentioned not wanting to replace a CEO going forward, but they want to bring in sectoral specialists that truly understand the nuances of the areas where they work. The interview echoed this because Mr. Pandey came across as someone aware of how the various sectors catered to by NBFCs have been hit in general, not just the 8 Ugro focuses on. He speaks about how financial institutions are rigid with their models and miss the nuances within the subsectors(healthcare was the example in the interview). He also explained how they’re evolving their process of underwriting(parts of hospitality won’t exist), and working to really understand the forward cash flows of the SMEs they lend to, rather than simply looking at previous revenue and payment/default history.

Given that we’re now in for two back to back Ugro meetings, with the Q1FY22 earnings call on the 11th of August, and the AGM on the 1st of September, Mr. Nath’s going to have to work very hard to spin two more 30 minute speeches out of the investor presentation. ![]()

Personally, I like that they’ve given targets for FY25:

- AUM of 25,000 Cr.

- Disbursals of 11,900 Cr.

- 16.3% interest yield.

- 9.5% borrowing costs.

- 8.5% NIMs.

- 4.2% RoA.

- 18.8% RoE.

- 3.8x Debt / Equity

I’ve written before in the thread that they have very real default conditions on the NCDs they’ve given out, so those triggers serve as proper monitorables going forward.

Disclosure: Invested and biased.