I’m going to attempt to answer a few FAQs here so everyone can get their answers regards all of the questions on here and we can get back to analysing the business:

Why are the net interest margins so low?

Ugro capital began disbursals in Jan 2019. As of now they have a majority of secured loans at 12 to 13 percent interest which take up nearly 70 percent of the portfolio. Unsecured loans take up the balance 30 and and their plan is to increase this allocation over the next few years once they have a vintage secure book. They also have zero new to credit customers since they are playing it safe with credit history customers. Their micro lending branches will open in 2 quarters and they are targetting approx 30 percent of new customers when they do begin. The margins here will be obviously higher too.

Their cost of income is currently around 10.12 percent which has dropped from 12 percent in just a year. This won’t decrease drastically anytime soon but should remain stable. They are targetting 9.5 percent in 5 years. Overall as costs decrease and their book gets more unsecured and new to credit customers the NIMs will icrease… Their target is 8.5 percent in 5 years.

What about gnpas?

Last year gnpas were under 0.1 percent but that is obviously not sustainable since they just began operations. Gnpas are currently 2.3 percent. This is obviously due to covid however one must remember that this is with a majority secured book and no new to credit customers. In latest Concall management confirmed that due to vintage book they would have had gnpas anyway but covid increased it. This is within their comfort zone though. Going forward as they target riskier segments(unsecured, micro, new to credit) Post covid the gnpas will increase anyway. So expect gnpas in this region for the next few years. When targetting high yields this is just the norm. If gnpas cross 5 percent and nnpas cross 3 percent is when panic needs to come in. As long as its within range however I wouldn’t be too worried. Currently 3.9 percent of their books are restructured and they expect a max of 20 percent more over covid 2.0. However, these are customers they are sure will pay but have short term issues. If they found someone with a really bad issue they did not offer restructuring and classified as npa. They have given sufficient provisions and are well capitalised so there is 0 existential threat here. So over the next few years NIMs will increase and expect gnpas of 2.5 or so percent. Again, if these suddenly balloon past 5 percent it would show somethings gone really wrong with their underwriting process. Uptil 4 to 4.5 percent max I’d be comfortable. Anymore and I’d be a bit worried.

What’s this sector based targeting?

The sectors and process is mentioned above. However I’d like to add that these sectors are very broad. For eg if a caterer supplies food exclusively to a school the caterer falls under the education sector since majority income is from there. This was an actual example taken from mr nath. Also when they move to micro lending ie under 25 lakhs they won’t be too fussed about sectors since they don’t see a difference between a pharmacy or kirana shop at that size(source latest Concall). So they have core sectors that they target and have created underwriting models for each of those with the help of crisil but they also have underwriting models outside of these sectors for micro and the models can pick up someone like the caterer above.

Do they handle digital lending?

Yes they will start that this fiscal year. But don’t panic. They aren’t doing a lenden club. They are targetting new customers not via Google etc but with tie ups with sectors and databases and then offering those loans to potential customers when they already pass their filters. They are limiting this to max 10 to 15 percent of their book. So don’t expect too much here and don’t get too worried either. We ll know more later this year when we see it in practice.

They also are bullish on colending via their platform too. They’ve already partnered with some big names and with recent rbi directives for colending they are expecting this to be a good source in the future.

Are they a fintech?

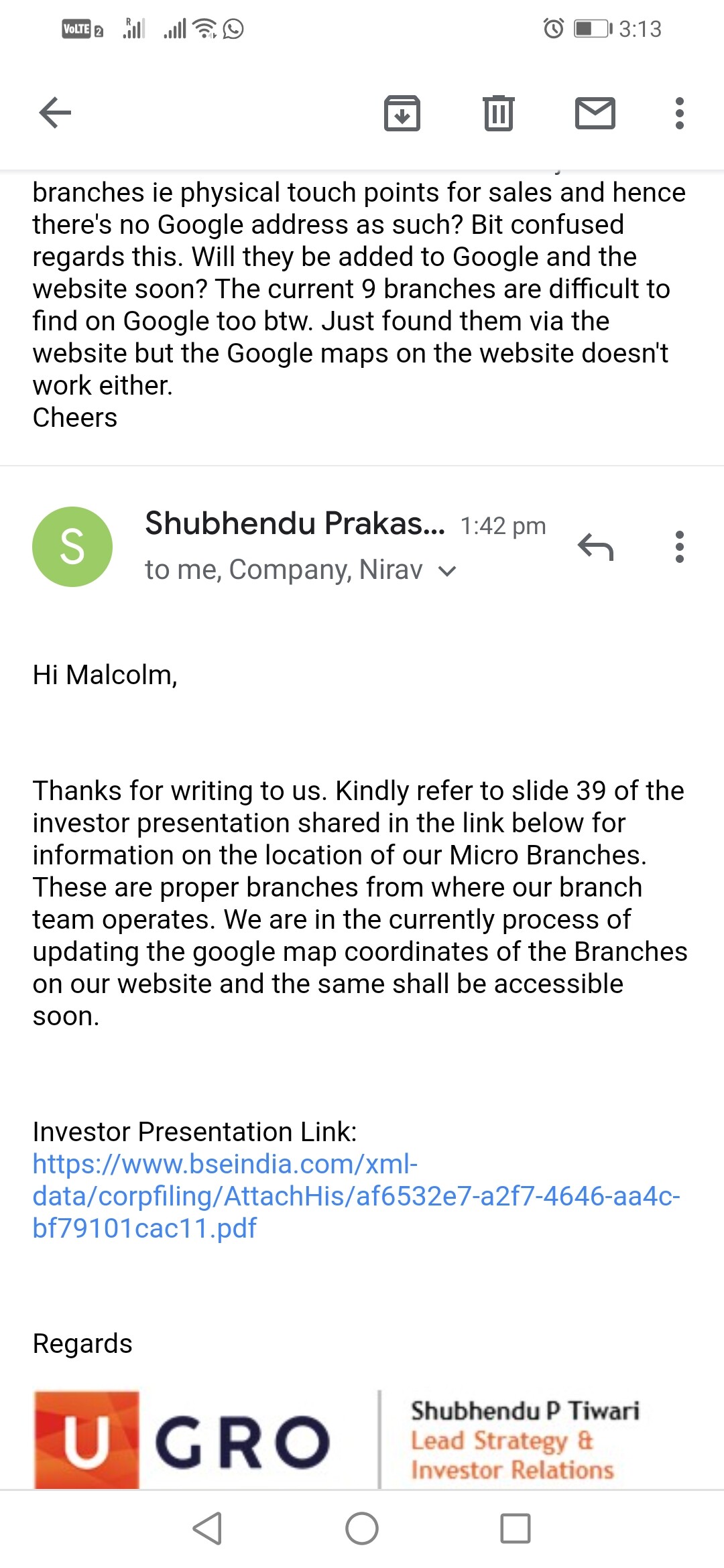

No and yes. You could consider tech side to be their digital lending platform which will contribute about 10 percent and their colending platform. They are just a normal Nbfc otherwise however they have embraced the use of technology. They have branches and gro partners that they disburse loans from and use their scorecard based sector models to help them figure out if their customer is credit worthy which takes them just 1 hour to get an inprincipal approval. Its then a human hand that gets involved just like any other Nbfc but due to the quick 1 hour approval by their scorecard(I’ve attached a screenshot from their corporate presentation which shows how they do it) they can spend more time on good leads rather than bad.

At the end of the day they use tech to improve efficiency just like anyone else. They have final approval and collection agents just like an other Nbfc so don’t expect gnpas to blow up as much as one would expect with a fintech… This is nt exactly one. BTW they’ve applied for a patent for their underwriting process and have won an award for it but at the end of the day humans look at the output and spend about 2 days deciding if the loan should be approved or not so imo overall whether you want to name them a fintech or a very digitally enabled Nbfc is just a label.

Are they a risky bet?

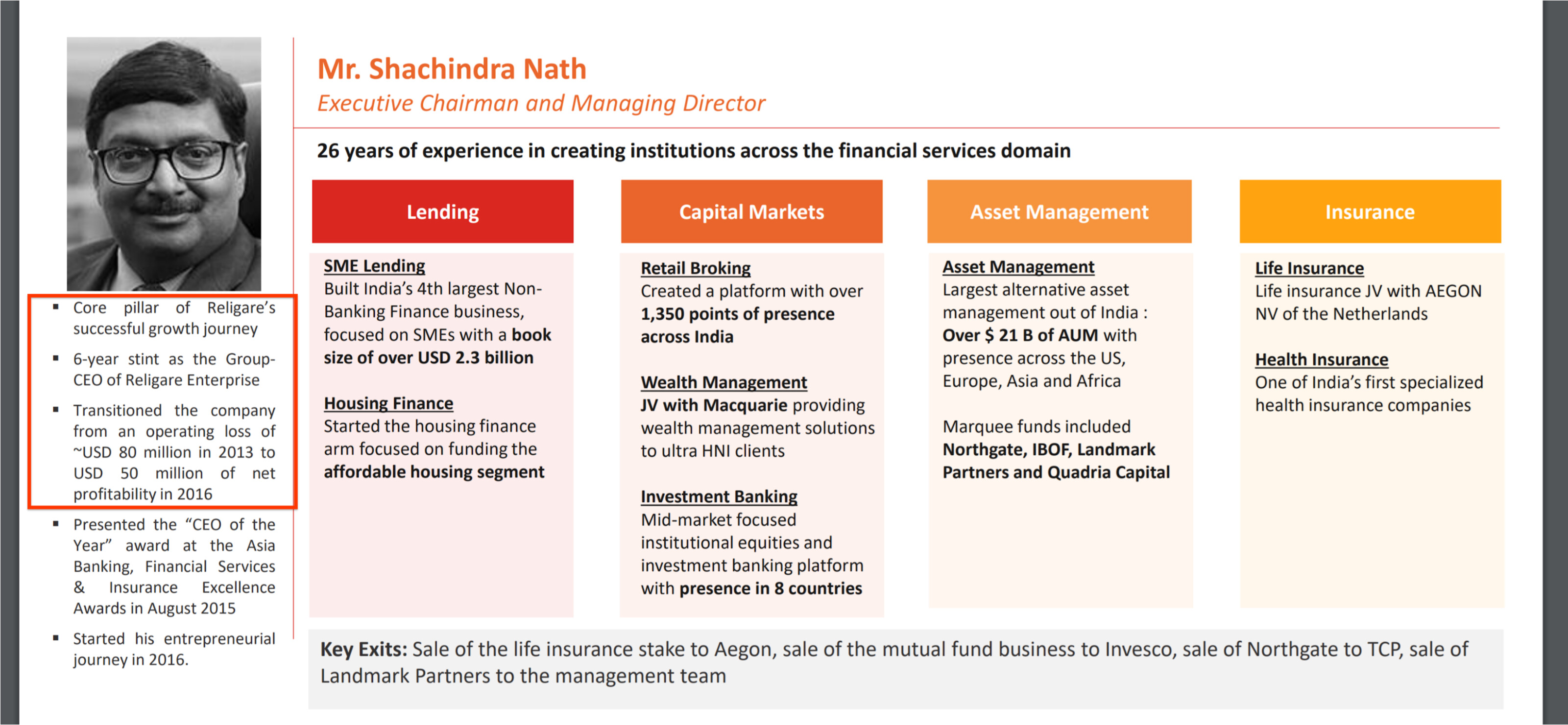

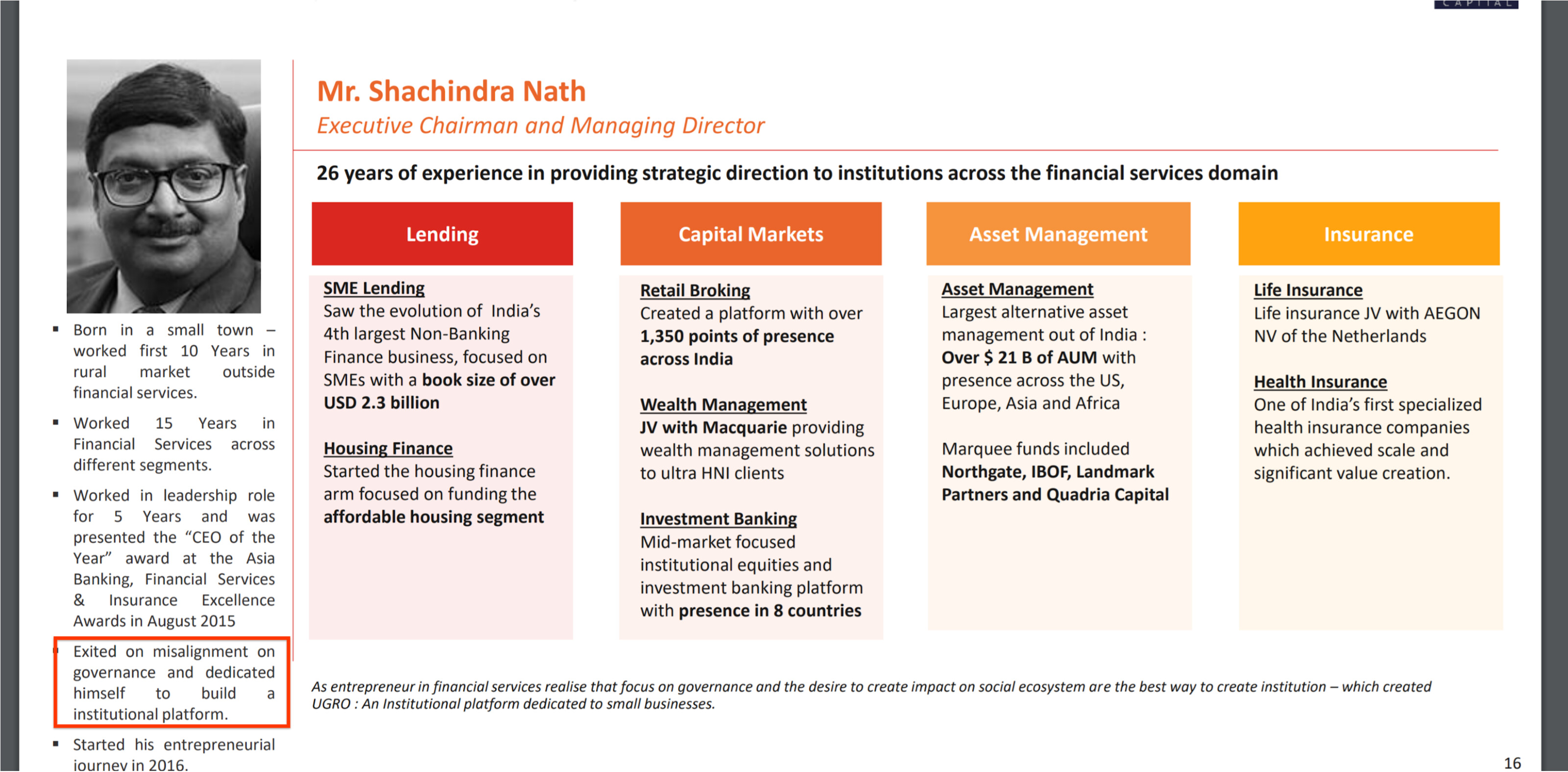

The corporate governance issues above regards Mr nath and religare are something you need to know about and need to decide for yourself regards that.

They are leveraged at just 0.59 times and are well capitalised and plan to increase leverage slowly so that isn’t a worry at all.

They are in a comfortable position to grow so that won’t be a issue either and giving money away is never a problem so they’ll continue disbursing loans too.

The risk is will they get the money back? You need to accept that NIMs are low now so you need to track that they increase over the next few years and that their gnpas remain on track.

Also, the liquidity is super low(at least upto this past week) and you need to see if you are comfortable with the way the company is structured such that the promoter percent is just 2.88 percent.

They also just do about 3 to 4 crores per quarter so far in normal tax conditions.

Their costs are huge currently because a lot has been upfront ie staff and branches etc. One needs to track that the costs come down to a more manageable figure(currently 7 to 8 percent… Ideally 1 to 2 percent) as their leverage and profits increase.

So while the potential is huge(their targets are in the investor presentation) the risks are now laid out for everyone to decide if its worth it or not.

Personally, Even though I’m invested and I’ve gathered most of the information available in the public domain im still not sure if the risk/reward is favourable even now.

Anyway, I hope this answers most questions that have been unanswered in this thread. My sources were the Concalls, video interviews and the corporate presentations. Cheers

Disc: Invested. Not a buy or sell reco. Not a sebi advisor.