510cr infusion lead to the dilution by around 2cr shares. Total outstanding shares then would be around 11.32cr.

Total net worth as reported by Ugro in q32025 earning presentation is 1998cr.

BVPS= 2000/11.32 = 177INR

at CMP i.e, 160 the P/B =0.9

510cr infusion lead to the dilution by around 2cr shares. Total outstanding shares then would be around 11.32cr.

Total net worth as reported by Ugro in q32025 earning presentation is 1998cr.

BVPS= 2000/11.32 = 177INR

at CMP i.e, 160 the P/B =0.9

Hi @dpk1994

I noticed you have been closely tracking this one. I am also unable to understand if its only the market sentiment which is driving the valuations so low or there’s more behind it.

In the recent credit report I found:

"UGRO began operations in 2018 and it has built an AUM of INR101.6 billion since then. While UGRO’s portfolio has been witnessing strong growth, the franchise size remains at a medium level. Also, the seasoning in the portfolio is low, as nearly 61% of AUM was generated in the 12 months ended September 2024.

The gross stage 3 for UGRO stood at 2.1% in 2QFY25 (FY24: 2.0%; FY23: 1.6%)%), with credit costs of 2.9% (on on-book AUM). However, on a one-year lagged basis, the gross NPA remained elevated at 5.1% in 2QFY25. Also, the gross stage 3 provisions coverage was 47% in 2QFY25 (FY24:48%; FY23: 49%), with total provisions at 1.0% of the AUM."

As more of the book matures we could see the GNPAs trending upward. And if it hits the 5% mark that does sound troubling. Do you see this as an important factor which is deriving the valuations where they are today?

There are several moving wheels deciding the valuation, like:

I would personally not read to much into this:

It’s a general risk highlighted by the credit agency. they are comparing the yoy growth in NPA. When we already know that we are not in the best credit cycle, such variations are acceptable. 70-80% of their book is secured so, I wouldn’t lose my sleep over it.

Major risk for me is the consistent unavailability of low cost liquidity which will prevent the decline in cost of borrowing. Situation should improve going forward especially when/if RBI cuts interest rate again in April. However, at that time you may not get this market price.

Disc: invested and biased

Just trying to understand the weakness reported. Paraphrasing it below:

UGRO is a relatively new company (started in 2018), and most of its loans (61%) were issued in the last year. This means there’s limited data to assess how well these loans will perform over time. While current bad loans (2.1%) seem low, older data shows a higher delinquency rate (5.2%), hinting that more loans could turn risky as they age. Additionally, the company’s reserves to cover potential loan losses (47%) may not be sufficient if defaults rise.

Now, from the latest earnings call, we have the management talking about CGTMSE policy and how 75% of the unsecured loan amount is kind of backed by the government. (note that for CGTMSE, claims still take ~1 year to process, straining short-term liquidity).

Given these, I wonder what a worst case scenario would look like for UGRO. If you have calculated it, it would be quite useful.

My rough attempt below using OpenAI:

| Metric | Base Case | Worst-Case Scenario | Difference |

|---|---|---|---|

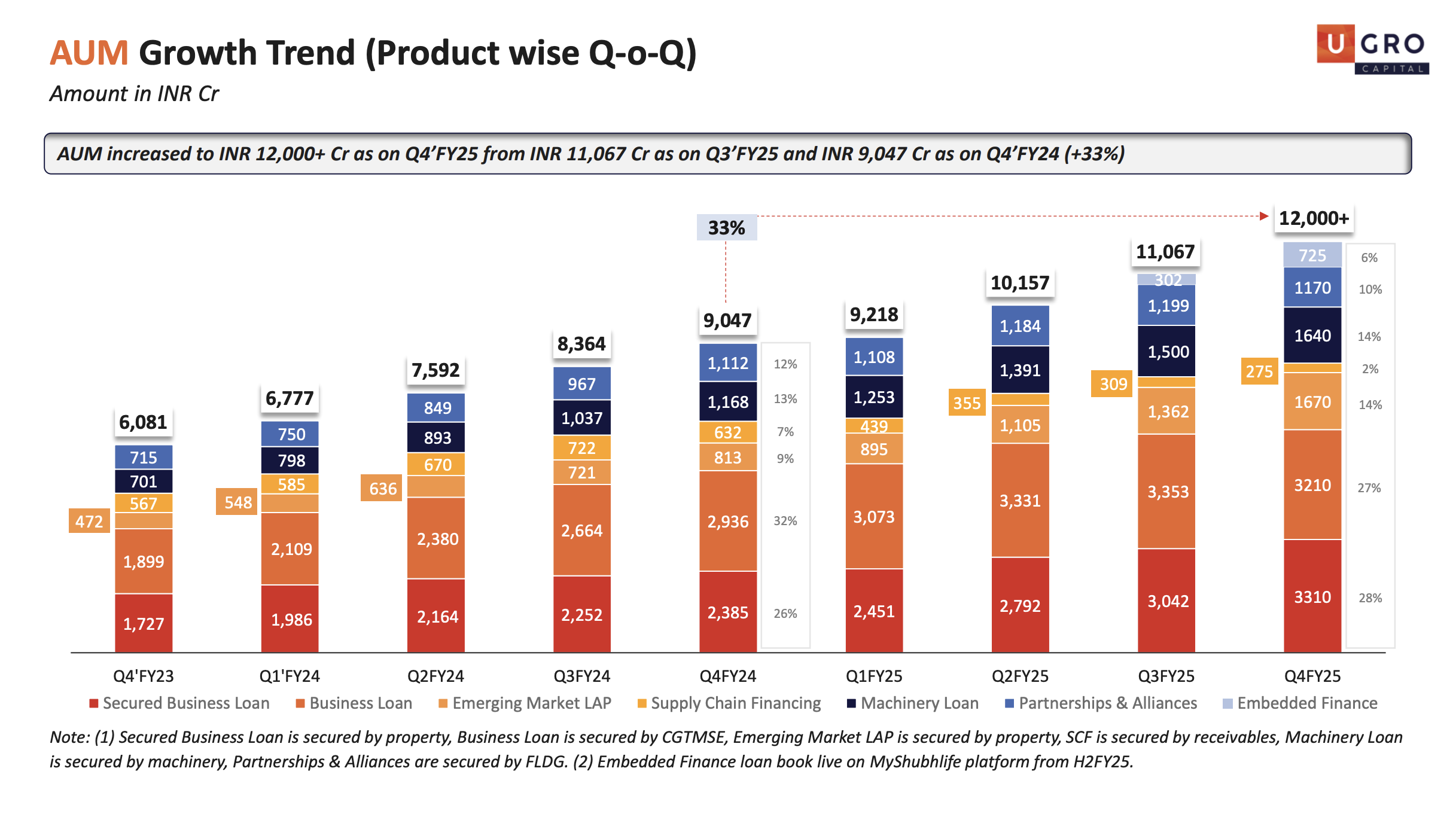

| Total AUM (Cr) | 11,067 | 11,067 | – |

| Secured Loans (Cr) | 7,747 | 7,747 | – |

| Unsecured Loans (Cr) | 3,320 | 3,320 | – |

| Effective Unsecured (Cr) | ~1,993 (after CGTMSE) | ~1,993 (after CGTMSE) | – |

| Current Gross NPAs (Cr) | ~232 (2.1% of AUM) | ~372 (≈3.36% of AUM) | +140 Cr |

| Current Net NPAs (Cr) | ~166 (1.5% of AUM) | ~300 (≈2.7% of AUM) | +134 Cr (approx.) |

| Additional Provisioning | – | ≈140 Cr | +140 Cr |

This would wipe out the company’s net profit. But still, wont be a big loss.

Disc: Invested

Good analysis. Just one check, have you also considered disproportionately higher npas in supply chain financing which they have discontinued now or do you see only marginal impact of that on your workings?

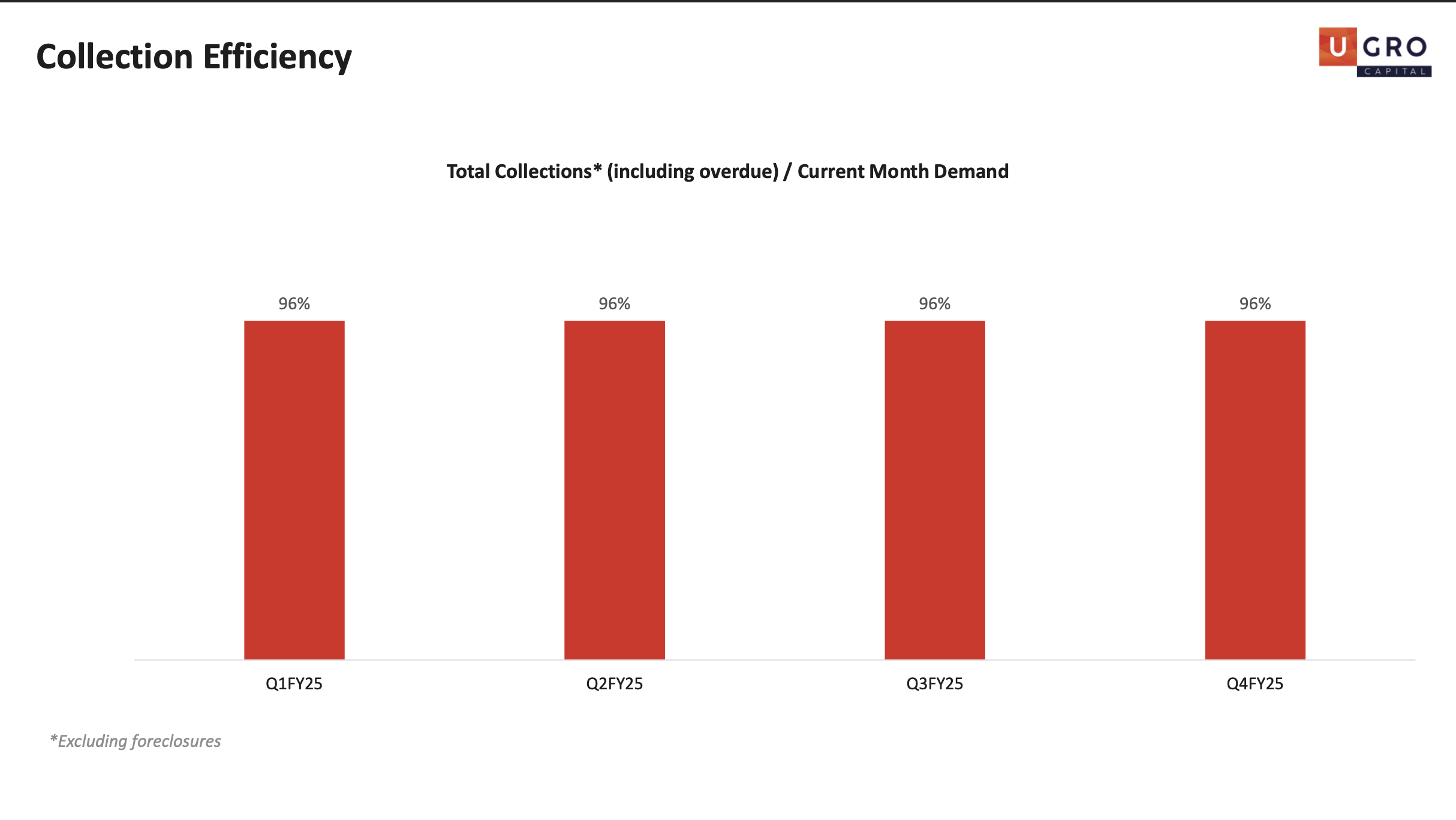

Collection efficiency is intact in this uncertain time. Moderate (not bad) growth in advances.

Some notable Green shoots:

Overall, very balanced growth nothing that I should be concerned about or otherwise.

I’m puzzled that Promoter didn’t add to his stake during the fall. If the prospects are so bright why does the promoter have such low stake?

They have already susbscribed to warrants by august they would be converted

Good to see clear communication

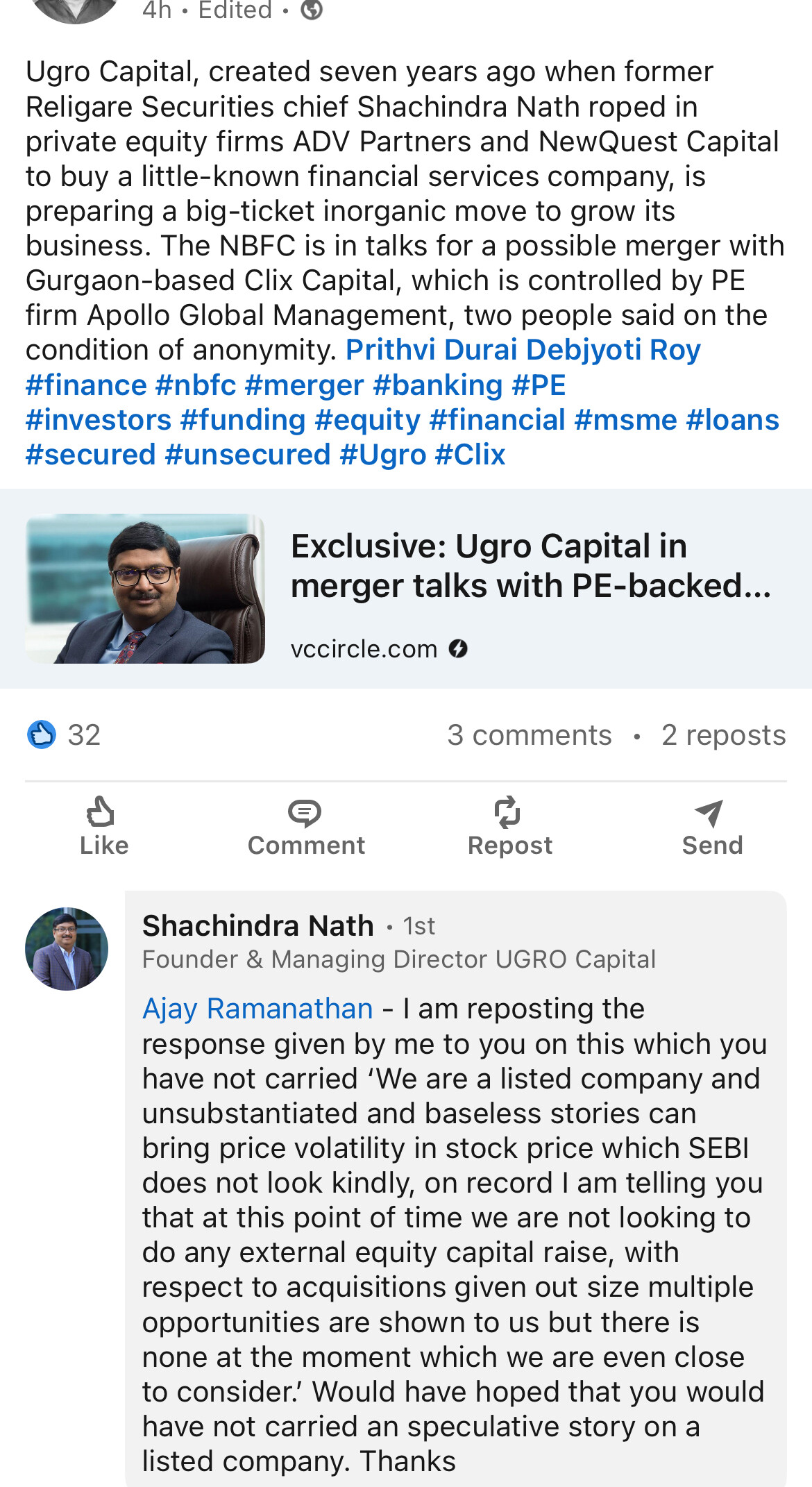

Something seems to be cooking under the hood!

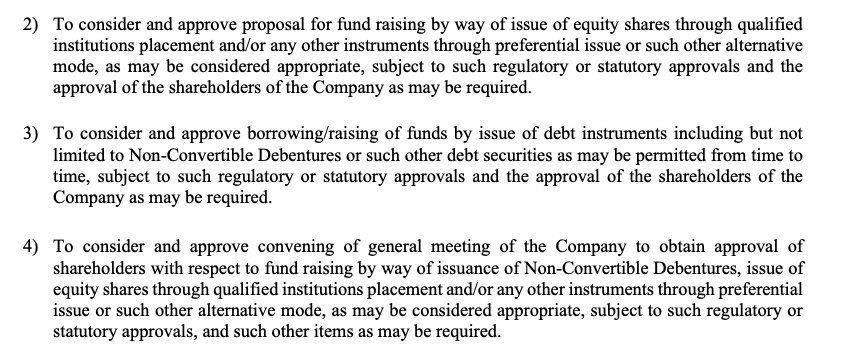

Company changed the agenda of the upcoming board meeting to include the discussion about raising of equity capital via preferential issue of shares. My guess is that they are going to acquire either Clix capital or some other company otherwise why would they need to allocate share. They are not getting merged in some other company but going to acquire one.

The combine entity could have AUM in the excess of 19000/- cr, ROA- 2% approx, Book value=4000cr.

As I said some guess work based on my google research, lets’ see what happens.

Disc- Invested and Biased

Again dilute at a price less than 264 , the last they had raised at… what kind of management is this if they raise preferential share

I agree, but if it were to happen, you should see the relative valuation at dilution.

As of now the small NBFCs are trading at very low valuation. Ugro is trading at near P/BV of 1, so is true for the company they want to acquire. If Ugro were to pay the same or less valuation at which it is currently trading, the acquisition wouldn’t be bad at all IMHO. On the top the acquisition would further strengthen the Net worth of the company, could lead to a rating upgrade and better CoB. There are so many synergies involved. The only caveat is the implication on the governance structure, if it doesn’t handled smartly could lead to many senior management departure.

This would be detrimental to holder of ccd and warrant holders who still has to get ccp and warrant converted.. still they have to pay around current price and qip being done at current price ..only way to be fair would be to issue at 264

If company waits for a fair price to come, the deal may not be there anymore.

I understand your point, it’s just the way company or capitalist world operates.

Noteworthy: The management team, including some of the board members have also invested in the previous round. Also, there are two PE players who have invested in the company in 2018-19 at around 118-130 per share and still waiting for their money to get doubled.

Is share holder return even a point i am failing to understand..or they just keep talking big … all these pe fund has to return money to their holder

![]() I share your disappointment.

I share your disappointment.

Just a few data points:

Of-course there are examples like ICICI bank, Cholamandalam that are the absolute outliers but in the broader financial space there hasn’t been any return generated in the last 5years. Thanks to Covid, over-leveraging of customers, phenomenol interest rates and so on so forth.

I assume that these early investor PE funds have to now return the money to their investors, hence they may push for such acquisitions. In general, i think the company has a huge potential but it is just that we were in a bad interest cycle.

A quote that I read in one of the books: You have to take a risk, trust the luck factor, and also exercise some skills for choosing the right stocks. They have to work in nexus to earn you good returns. In the case of Ugro, i thought I was super smart to identify such an amazing high growth company at a relative early stage, with a pristine governance but it looks the luck factor was missing and is missing…hahahaha

Let’s see what happens, I still trust the company management, that they will not take any foolish decisions. They have been successfully able to keep the boat afloat in this time of un-certainity, I would hope they are not doing a bad job behind the curtain. It is just the time and the circumstances which has to be cursed.

My 2 cents on this:

This could be (a) genuine acquisition, but given the movement in share price away from the earlier qip it could also be (b) a simple misgoverned qip - the previous qip warrant holders might want another round at lower prices as they have the board seats and votes to get it approved.

If it is (b) it will be quite disappointing as the PE investors would have misused their board seats and votes.

Even if (a) also does the same thing, atleast its masked as an EPS accruing balance sheet inflator.

Its a shame because a goldilocks period has begun for this subsector and UGRO :

Obviously theres a risk of US recession, but apart from that things look as good as they get