Do you know if there is a difference between pa pm vs pa (latest fund raise?)

The term p.a.p.m. stands for per annum, payable monthly.

This means that the interest is payable monthly as opposed to paying yearly or at the end of the tenure.

Quick question regarding the fund raise done earlier last year. Per my understanding, there were CCDs issued which will convert at 264, which will be accretive to any shareholders buying near current prices.

My concern was with the warrants issued. Based on filings, 25% of the amount was paid upfront, with the balance to be paid on conversion at a valuation of 264/sh. Due to recent drawdowns, it would be cheaper for warrant holders to purchase at CMP ~180, instead of converting warrants by paying 198/sh.

Is there a possibility where UGRO is unable to complete the fund raise if market price remains at these levels for the next few months. Realistically, this should not be the case as most of the raise was from bigger players, and there would not be enough liquidity in open market for such a large purchase, but just curious to see if a possibility exists.

On that front, I believe this is a big challenege to UGRO in the coming years. Unlike other companies, UGRO is at a juncture where it needs the share price to go up to go up to keep growing and market is not giving Ugro any credit at all at this point (perhaps once ROA / ROE improvement is actually seen). The only other option I see would be to significantly increase off-book % if leverage needs to be maintained near the 4x range.

Current valuations are extremely tantalizing though. Very hard to see downside from here, barring a significant deterioiration in asset quality.

Disc : Invested, considering to add more

1 Like

When the warrants were issued, 25% of the amount was paid upfront. In case, if one of the warrant holders didn’t pay the remaining amount, his money would be confiscated and he will get nothing. This is legal and as per the general contractual terms, the company can do this.

1 Like

When is the expiry date of the warrants? May not be the worst outcome for minority shareholders if the 25% gets foreited - money in and no dilution.

At the latest by August all the warrants should be converted into equity shares.

Note: when you raise money from large respected family offices, the risk of them not honoring the commitment is minuscule.

Share price is moving with very low volume that shows just the apprehension and speculation and the moment any of the large investors jump in to buy, the share price will skyrocket.

2 Likes

Wouldn’t it make more sense for the warrant subscribers to forgo the 25% paid and instead buy from the secondary market if they still want to play the Ugro story? Stock is down ~25% from issue price. Some could even skip considering it as loss and look for better investment avenues considering broader market trend.

While it maybe good for existing shareholders as won’t lead to equity dilution there will still be the issue of raising equity for growth.

Infact somebody asked a related question in the earnings call that if Ugro is targeting to grow at 30% annually and their ROE is much lower they will need to continually raise equity and at current market prices it will lead to significant dilution.

CEO acknowledged the challenge and said he is hoping market will reward their perfomance and hopefully can raise at higher levels but that’s a big ‘if’

3 Likes

Well, I can really understand your perspective, but this is a wishful thinking. Maybe a small set of investors who have subscribed to some warrants will let go of their small investments. However, institutional investors, who have actually invested a large amount of money, wouldn’t do this as this will ruin their reputation in the market. It doesn’t work like this.

On the other hand, Ugro raised around INR 1280 crore by issuing 5 crore shares; no investor can buy these many shares from the open market because there is no liquidity. If investors were to buy 5cr shares from the open market, the price would skyrocket.

Generally, all the institutional investors invest for the long term because in the long term the price will just go up, and obviously, no one could buy shares in a large quantity from the market. It’s actually impossible unless the company is a large cap, for example, HDFC Bank.

9 Likes

Large ownership of public / retail-investors in Ugro is a drawback here. And this group panic selling is the only reason I can think of for hitting new lows everyday.

11.83% of the company is owned by individuals that have invested <2 lacs, and they are selling since the last 1.5 quarters. Current skepticism around small caps has further accelerated this selling.

If you have noticed, the selling is happening with significantly low volume viz-a-viz the peers or other small-cap financial like MFIs.

Well considering, the only financial company in the small to midcap universe that hasn’t shown an elevated provisioning or credit cost. On the contrary, their credit cost has decreased by 170 bps; their current valuation is nothing but shows a general panic during which investors tend to paint all the companies with the same brush as they do during a bull cycle.

Some other observations:

I have checked their LinkedIn page, and it’s outright clear that they are expanding big time with continuous hiring and opening new branches. In the very short term it’s CAPEX heavy, but considering the new branches are breaking even in a mere 8 months, and from the 9th month they are ROA accretive, this expansion should result in excellent operating leverage. In this market, finding a company with such caliber, governance, and solid business is very difficult, if not impossible.

A few reasons for depressed matrices and the share price:

We investors are mostly impatient and constantly look for quick gains. When so many shares went from nothing to being multibaggers (most of them now down by at-least 50% from the top), who wants to invest in a slow-moving business even if the future is promising?

Ugro deliberately chose to adopt a business model where the company is like an index of 4 distinct NBFCs catering to 4 distinct products, namely, Prime Secure, business loans, machinery financing, and micro-enterprises. Actually, in India, as I said, we have 4 different types of NBFCs that offer these products. For example, SBFC and Five Start offer micro-enterprise loans, Bajaj Finance and traditional banks do prime secure, many unlisted NBFCs do machinery financing, and so on and so forth.

There are some phenomenal advantages of this business model, like:

- You just can’t create an institution by catering to a single category. A very lame example: if a retail store is just selling trousers, which may be one of the most comfortable and profitable, you cannot scale beyond a point. On the contrary, if you use your store franchise to sell and cross-sell many precisely chosen products, your chance of creating an institution is very realistic.

- Since, in this approach, the ROA is depressed for the initial years as the loan book is constituted of low, medium, and high-yielding products. As the company scales, it gets rating upgrades, which results in a decrease in the cost of borrowing, and this ensures that even the lowest-yielding products are also super profitable.

- This split of 70% secured, 30% unsecured, and an index of 4 different yielding products ensures that the credit cost is always within the limit. Remember, the more greedy a lender you are, the more risky your book becomes. MFIs are the testament to this.

Discl: Invested and biased

13 Likes

Agree,

As they are targeting 35% portfolio of micro enterprises, if they can maintain asset quality, numbers look promising.

Calculation Based on 35% High-Yield Micro Loans using Chatgpt

1. Base Financials from Q3 FY25

- AUM: ₹11,067 Cr

- Net Interest Income (NII): ₹218 Cr

- PAT: ₹38 Cr

- Annualized PAT (FY25 Projection): ₹38 Cr × 4 = ₹152 Cr

- PAT Margin Calculation:

[

PAT \text{ Margin} = \frac{152}{218 \times 4} = 17.4%

]

2. Future FY26 Projections

- Projected AUM: ₹17,300 Cr

- Micro Loan Contribution (35% of AUM): ₹6,050 Cr

- Remaining Loan Contribution (65% of AUM): ₹11,250 Cr

Blended Yield Calculation

- Current Loan Yield: 14%

- High-Yield Micro Loan Yield (Based on Five Star Finance): 24%

- Blended Yield Post Expansion:

[

(35% \times 24%) + (65% \times 14%) = 8.4% + 9.1% = 17.5%

]

Net Interest Margin (NIM) Impact

- Current NIM (Q3 FY25): 7%

- Future NIM (Proportional to Yield Increase):

[

7% \times \frac{17.5}{14} = 8.75%

]

Projected Net Interest Income (NII)

[

NII = 17,300 \times 8.75% = 1,513.8 \text{ Cr}

]

Projected PAT Margin (Proportional to NIM Expansion)

[

17.4% \times \frac{8.75}{7} = 21.8%

]

Projected Profit (PAT) Calculation

[

PAT = 1,513.8 \times 21.8% = 330 \text{ Cr}

]

3. Final Comparison: FY25 vs FY26

| Metric | FY25 (Projected from Q3) | FY26 (With 35% Micro Loans) | % Growth |

|---|---|---|---|

| AUM (₹ Cr) | 11,067 | 17,300 | +56% |

| Yield on Advances (%) | 14% | 17.5% | +25% |

| NIM (%) | 7.0% | 8.75% | +25% |

| PAT Margin (%) | 17.4% | 21.8% | +25% |

| Profit (₹ Cr) | 152 | 330 | +117% |

4. Key Takeaways

![]() Profit Expected to More Than Double (₹152 Cr → ₹330 Cr)

Profit Expected to More Than Double (₹152 Cr → ₹330 Cr)

![]() Blended Yield Expansion to 17.5% Will Drive Higher Profitability

Blended Yield Expansion to 17.5% Will Drive Higher Profitability

![]() PAT Margin Expansion to 21.8% Due to Shift to Higher-Yield Micro Loans

PAT Margin Expansion to 21.8% Due to Shift to Higher-Yield Micro Loans

![]() ROE Expected to Improve from 10% to ~14-15%

ROE Expected to Improve from 10% to ~14-15%

With this transition, UGRO Capital could significantly boost its profitability and valuation, assuming credit quality remains intact.

5 Likes

@Akash_Padhiyar

Did you also check for the potential ROA value at the end of fy26, if yes could you share?

Also, what prompt did you use, want to cross check?

1 Like

Projected ROA for FY26

- Projected AUM (FY26): ₹17,300 Cr

- Projected PAT (FY26, from previous analysis): ₹330 Cr

- ROA Calculation for FY26:

ROA=33017,300×100=1.91% and around 1.7% if we consider branch expansion cost with same asset quality.

| Metric | FY25 (Base from Q3 Data) | FY26 (Post Branch Expansion) | % Growth |

|---|---|---|---|

| AUM (₹ Cr) | 11,067 | 17,300 | +56% |

| Net Interest Income (₹ Cr) | 218 | 1,384 | +535% |

| PAT (₹ Cr) | 152 | 300 | +97% |

| ROA (%) | 1.37% | 1.73% | +26% |

As pwe management they are targeting RoA around 4% with above changes in loan portfolio. If that would be the case then huge upside possible.

Disc: No holding

ROA of 4% is very much ambitious target, but 2% ROA seems achievable.

![]() At 2% ROA, a P/B of 1.5 could take UGRO to ₹360 in FY26.

At 2% ROA, a P/B of 1.5 could take UGRO to ₹360 in FY26.

![]() At 3% ROA, a P/B of 2-3 could lead to ₹578-867 in FY27.

At 3% ROA, a P/B of 2-3 could lead to ₹578-867 in FY27.

![]() ROE could rise from 8.15% (FY25) to 15.5% (FY26) and 18%+ (FY27).

ROE could rise from 8.15% (FY25) to 15.5% (FY26) and 18%+ (FY27).

Risk Factor: Asset Quality

All assumptions depend on asset quality. Rising NPAs or provisioning needs could lower profitability and impact re-rating potential. Execution discipline in underwriting and risk management is crucial for sustained growth.

“I think you are calculating ROA based on the gross AUM. This is incorrect in the case of Ugro, as only a portion of this AUM is on-balance sheet, while the rest is off-balance sheet due to the co-lending arrangement.

My back-of-the-envelope calculation based on the AUM levels you quoted:

• AUM FY25 : ₹12,500 crore (on-balance sheet: ₹8,000 crore )

• AUM FY26 : ₹17,300 crore (on-balance sheet: ₹10,380 crore )

• Profit FY26: ₹330 crore

Breakdown of the ₹8,000 crore on-balance sheet:

• ₹6,875 crore (55% of AUM)

• ₹1,125 crore (20% of the co-lending volume*)

In co-lending, Ugro finances 20%, while the co-lending partner finances 80%.

For FY26, the on-balance sheet calculation assumes co-lending will account for 50% of the total AUM.

• Average on-balance sheet loans in FY26 : ₹9,190 crore

• ROA Calculation: ₹330 crore / ₹9,190 crore = 3.6% (very likely)

Looks like ChatGPT cannot replace a human just yet—pun intended! ![]()

13 Likes

Would the PAT be the same even for the off balance sheet AUM?

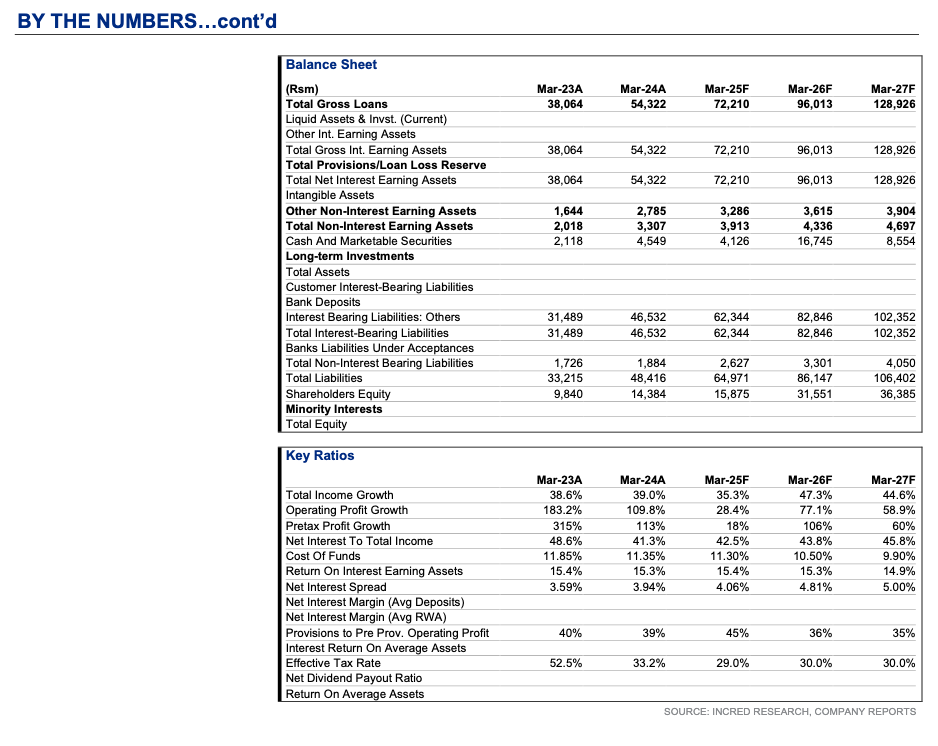

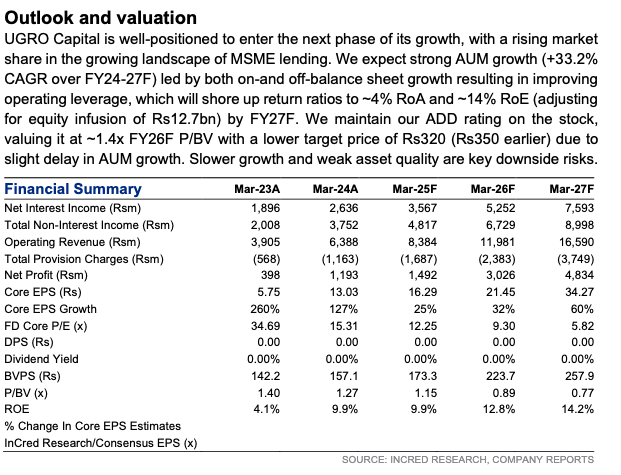

Sharing the analyst coverage report form Incred Equities:

Some key insights:

ROA for fy25= 2.0, fy26= 3.1 and for fy27= 3.8.

PAT for fy25= 149cr, fy26= 303cr and for fy27= 483cr.

incred 3Q FY25_UGRO_28Jan25.pdf (379.1 KB)

Disc: Biased and invested

6 Likes

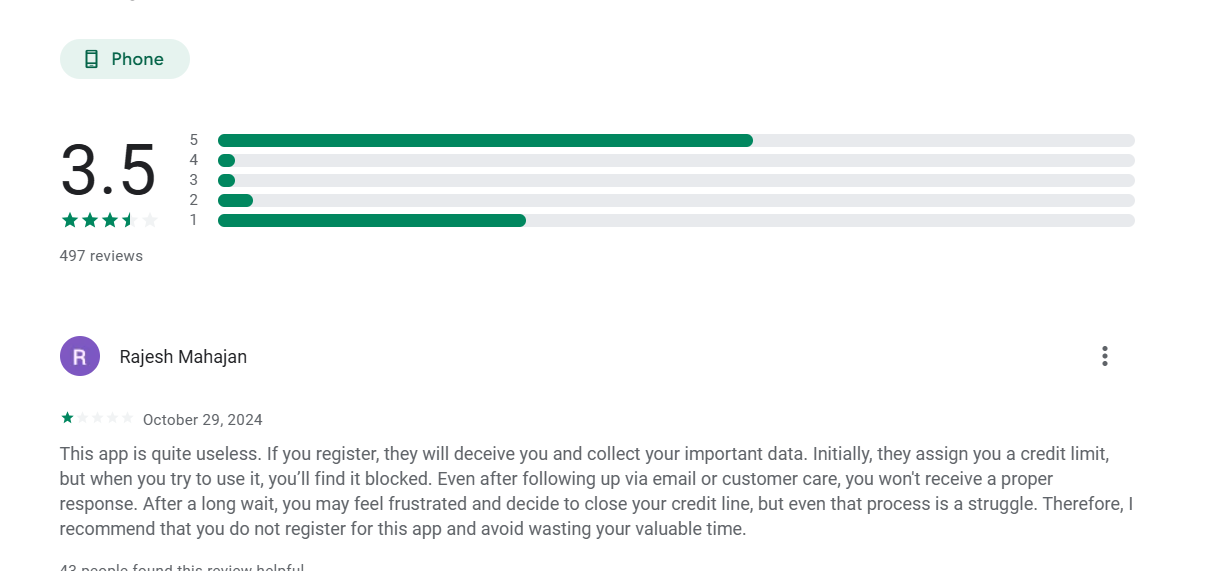

I have gone through some of the reviews on its app from play store, there seems to be some serious issues customer facing. Anyone used thier products through app ?

- Disc - Not invested yet