Guidance for FY26:

-

AUM Growth: Projected at approximately ~30% year-over-year. This significant expansion is indicative of robust demand for Ugro Capital’s services and a strong market position in MSME financing. The growth underscores the company’s capability to scale operations efficiently.

-

ROE: Expected to soar above 18% from the current ~8%. This leap suggests enhanced profitability and operational efficiency, potentially attracting more investors looking for high return on equity.

-

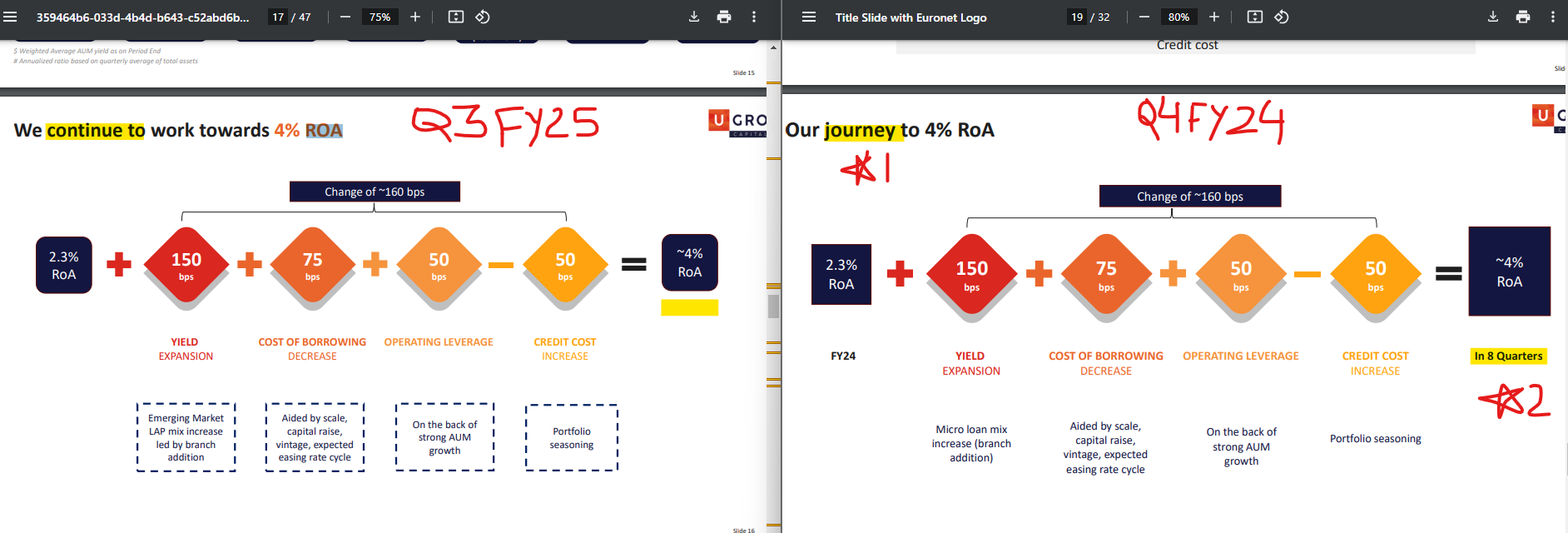

ROA: Anticipated to reach ~4% from the current ~2%. This improvement in return on assets signals better asset management and profitability per unit of asset, making Ugro Capital an attractive investment in terms of asset utilization.

) -

Leverage: The leverage ratio is expected to increase to 4x-5x from ~3.5x, indicating Ugro’s strategic move to leverage more debt to fuel growth while maintaining a healthy balance sheet. This could lead to higher returns if managed well.

-

Credit Cost: Projected to be between 0.8-1%, demonstrating effective risk management and potentially lower provisions for bad loans, which enhances the bottom line.

Hypothesis on Valuation Rerating:

If Ugro Capital achieves its FY26 guidance, particularly the ROA at 4%, there’s a strong case for a rerating in its stock valuation. Here’s how:

-

Price to Book (P/B) Ratio: Currently, Ugro Capital’s P/B ratio might not reflect its potential due to the lower ROE and ROA. However, with the ROA projected to double, this could lead to a significant rerating. If the market starts pricing Ugro Capital at a P/B ratio of 4, akin to high-growth financial institutions, it would reflect:

-

A recognition of its asset quality and profitability.

-

Confidence in management’s ability to execute their growth and efficiency strategy.

-

An acknowledgment of the company’s niche in the high-demand MSME sector, which is less volatile than consumer lending.

-

-

Market Sentiment: The substantial growth in AUM and profitability metrics could change market perception from seeing Ugro as a mere MSME lender to a growth-oriented financial institution. This shift could attract both value and growth investors, pushing up demand for the stock.

-

Comparison with Peers: If Ugro’s metrics outperform those of its peers, particularly in ROE and ROA, it might command a premium valuation. A P/B ratio of 4 would not be out of place if its financial health and growth trajectory outstrip industry standards.

-

Risk Management: Low credit costs suggest a robust risk management framework, which could further justify a higher valuation as it implies a lower risk profile.

-

Potential Catalysts:

-

Expansion into new sectors or regions could further bolster growth prospects.

-

Strategic alliances or acquisitions like the one with MyShubhLife could open new revenue channels and improve market penetration.

-

In conclusion, if Ugro Capital meets or exceeds its FY26 guidance, the market’s perception could shift, leading to a revaluation of the company’s stock. A P/B ratio of 4, while optimistic, would align Ugro Capital with leaders in the NBFC space that demonstrate similar or superior financial performance metrics. This scenario would not only reflect its current state but also its potential for future growth and profitability.