very good points raised @njain1983

As the management says, UC is the listed startup and unlike other NBFCs it’s valuation wasn’t pumped up by the PE players as generally happens during IPOs. Since last year, management is going live on all the possible media outlets to promote his companies, as until last year nobody in the industry knew about it. Sometime, it looks bit over to me, but i guess it’s a new trend. Most of the small size companies are continuously going for interviews for building up the investor sentiment.

Interest rate (IR) is insanely high right now, even considering Indian standard. Pr-pandemic IR was 5.15% and it was slowly coming down. Between 2014 to 2017, IR declined by 2% (from 8 to 6%).

IR was declining some 75bps per year (approx). Had there been no Pandemic, IR would have been significantly reduced by now. Unlike China or other big western economies which are export based, India is a consumption based economy. Broad scale consumption can only thrive in moderate IR environment. Current lackluster consumption can be attributable to high IRs.

High IRs could be one reason of higher delinquencies in the finance sector, irrespective of vintage of the organization everyone reported higher credit cost, elevated NPAs and reduced lending in the Q1 FY2025. UC is no exception. I was bit unhappy about the result of UC but after reading into the results of its peers (or adjancies), i am fine with the performance. On the portfolio level UC has reported satisfactory asset quality.

Like any-other NBFC, UC is also affected by bank to NBFC lending norms. There co-lending model comes into highlight here, as they do not need to lend on their balance sheet and still get good fee income. So funding per-se shouldn’t be a major problem for Ugro, with easing rate cycle, situation should improve. AUM around 13.5k by fy2025 and 19k by fy26 is doable. I am much more interested in seeing ROA>4%, ROE>16%, AUM alone is not of much value. FIIs, DI looks for asset quality over just AUM.

I also hope someday RBI realizes the need of dedicated MSME categorization in NBFCs. Like MFI there should also be a separate category. This is inevitable if MSME sector really has to grow. It’s better to be with the best class NBFC rather than waiting for the clarity, won’t get value later. UC may not be the best class NBFC, but certainly a very good one.

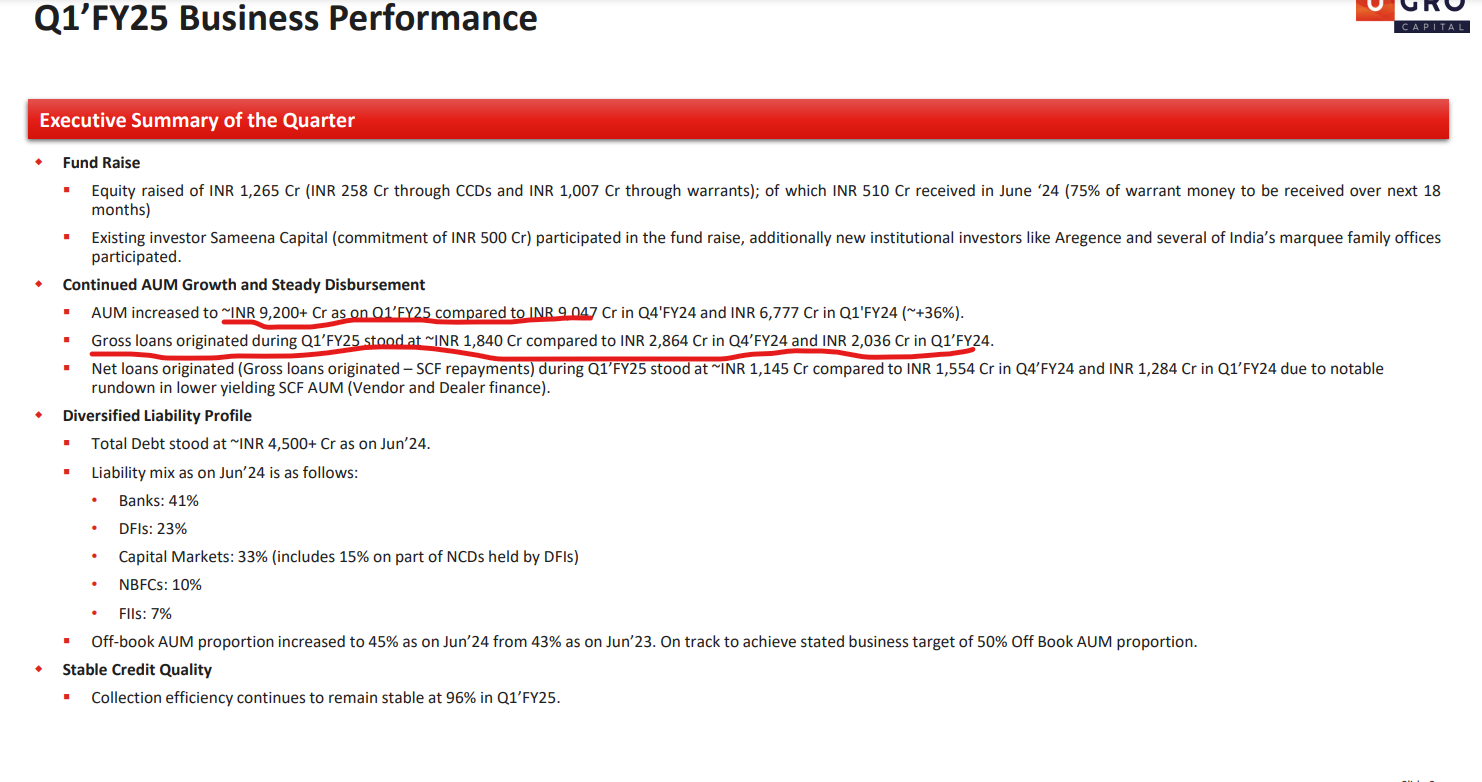

UC raised 1280cr from large family offices, PE and individual investors, on the top got rating upgrade. Financial market is certainly understanding the opportunity here. Price movement is very well based on the sentiment in the current market rather than on fundamental. UC intends to grow its AUM and PAT at >30% (>40% for the next 2 years) siting on a huge operating leverage and available at just 1.3x 1 year fwd P/BV. This investment offers huge risk to reward ratio to me.

Disc: Among top 2 biggest holdings

PS: I have similar opinion for Muthoot micro finance