Ugro capital is scaling down on supply chain financing…as explained in the last concall…

Those vendors supplying to AAA rated companies and those dealers buying from AAA rated companies are getting loans from banks @7.5%…whereas ugro capital cost of capital ia 10.5%…so to get higher yield, they were forced to go to BBB rated dealers and vendors …which leads to spike in NPAs…so they decided to scale back on this financing

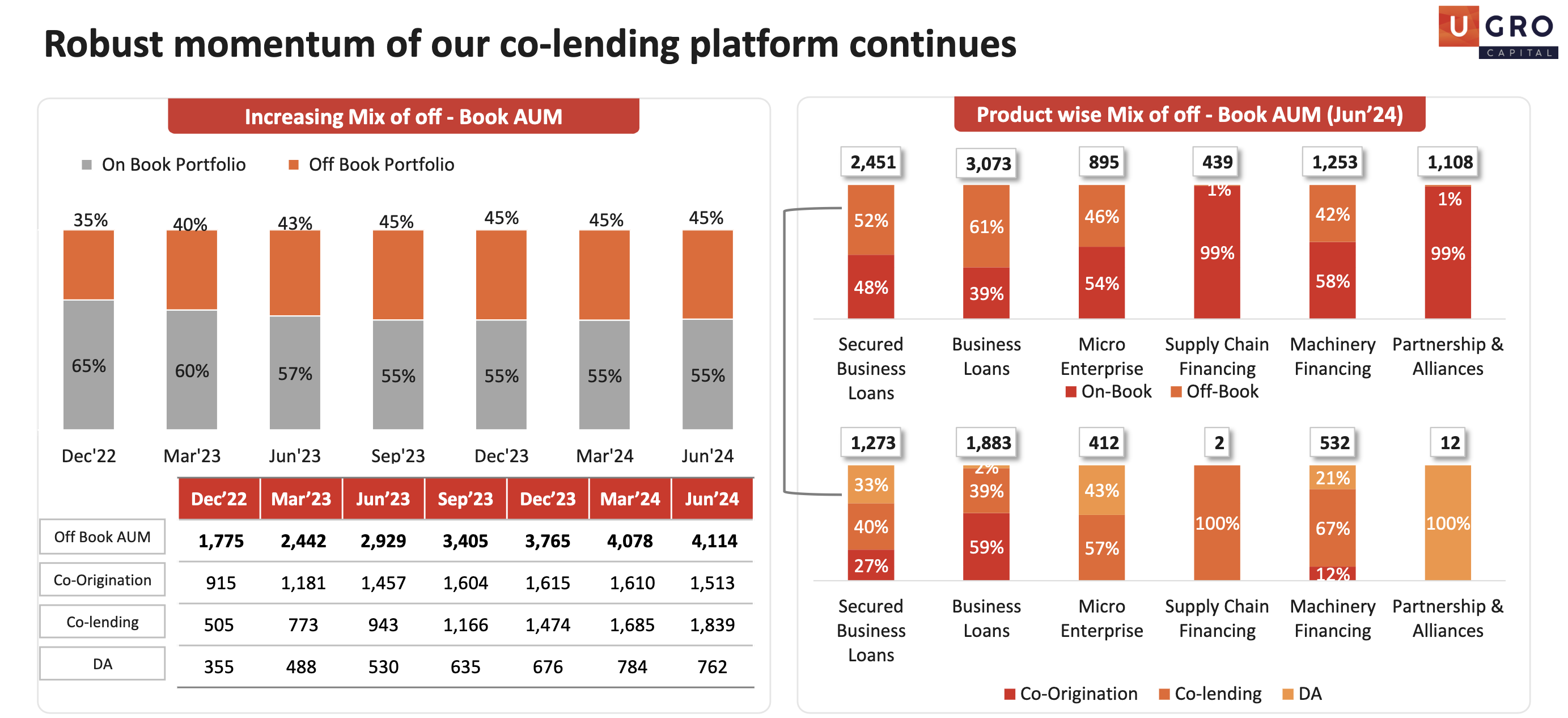

Excluding supply chain financing…AUM has gone up from 6192 crores to 8765 crores QnQ…

Now instead of financing top of the supply chain…dealer and vendor…they are moving to the bottom of the supply chain…the retailers…where yields are higher…there is no competition from banks…and more amenable to their Grow platform / data analytics / cash flow analysis.

Mngt needs to clarify only one thing…do they still stand by their target of 18000-20000 crores AUM by end of Fy2026?

How much of a factor does election has played in the overall degrowth in net loan origination since this time the elections were also prolonged almost 1.5 months and businesses tend to avoid taking big loans ahead of uncertain policy outcomes? Maybe comparing it with Q updates of peers in MSME lending would give a clear picture.

Mr. Shachindra Nath, Founder and Managing Director of UGRO Capital said, “At UGRO Capital, we have

set ambitious goals for FY25, and we are poised to innovate and expand our footprint in MSME lending.

Our recent rating upgrade underscores our relentless dedication to supporting the growth aspirations of

MSMEs and reflects the strength of our business fundamentals. Since inception, we have been and

continue to be dedicated to facilitating their success because we truly believe that ‘MSME Accha Hai’. As

the company marches forward on its path of sustainable growth, it offers a compelling opportunity for

investors seeking long-term value and returns.”

Key performance highlights for Q1’FY25

AUM of INR 9,218 Cr (up 36% YoY and 2% QoQ)

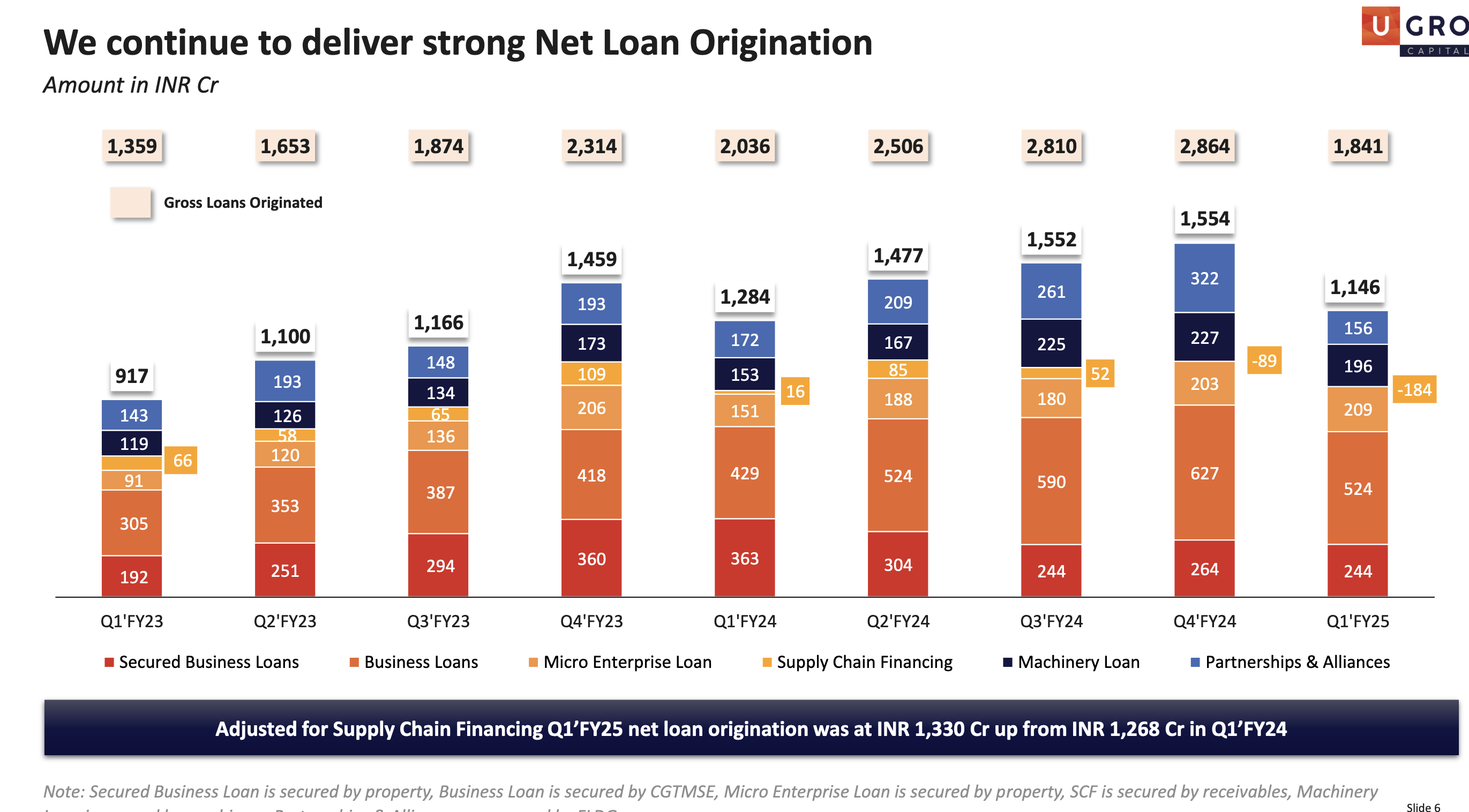

Net disbursement (adjusted for SCF) stood at INR 1,330 Cr compared to INR 1,268 Cr in Q1’FY24

Total Income stood at INR 301.6 Cr for Q1’FY25 (up 38% YoY)

Net Total Income stood at INR 165.4 Cr for Q1’FY25 (up 32% YoY)

PBT increased to INR 42.8 Cr in Q1’FY25 (up 20% YoY) as against INR 35.6 Cr in Q1’FY24

PAT increased to INR 30.4 Cr in Q1’FY25 (up 20% YoY)

GNPA / NNPA as on Jun’24 stood at 2.0% /1.2% (as a % of Total AUM)

164 branches (as on Jun’24)

Ratings upgrade: Upgraded to IND A+/Stable for long-term and IND A1+ for short-term by India Ratings

and Research

Capital adequacy at 27.9% (as on Jun’24) on account of equity fund raise.

NPM seems to have contracted from 11.56 to 10.07 QoQ. Neutral to slightly negative result. Seems the stock will continue hibernating. This is one of my top two holdings. Overall same story most NBFC this quarter. Opportunity cost is the problem.

Good things is that asset quality has increased which is a big deal. Margin’s will expand in future due to credit rating upgrade. Now all depends on how they can bring back the loan book growth.

Ugro is expanding it’s micro enterprise branches by 100 branches this and 150 next year. So by the end of fy25 they should have 250 and by fy26 400 running micro enterprise branches.

This should drive the loan growth and ROA. So, the loan growth shouldn’t be a concern.

Interesting fact:

Credit rating of SBFC from India Ratings is AA- and now Ugro got upgraded to A+. With one more upgrade Ugro will have credit rating same as SBFC, i.e, AA-.

The cost of borrowing for SBFC is 9.23% and for Ugro it is 10.7%. If Ugro performs well, there is a high chance of rating upgrade, same happened with SBFC in 2023.

Rating upgrade is instrumental for any lending business, with every rating upgrade the CoB will decrease and the spread will increase, and hence the profitability will go multi-fold.

They are continuously increasing their co-lending book, got increased by 9% qoq. This is aligned with the long term objective of the management.

They are focusing on Secured and unsecured business loans for co-lending and using their balance sheet to ramp-up Micro enterprise loans. This way they will earn a good fees from banks for co-lending and high spreads from Micro enterprise loans. Good proposition for Ugro.

Question(refer the screenshot below):

What is co-origination, is it same as co-lending and why it got decreased?

Why over all net loan origination is muted in the quarter for all the buckets(only micro enterprise loan-book increased minimally), need some clarity here?

Co-origination and co-lending generally refer to similar processes where two financial institutions (typically a bank and an NBFC) collaborate to issue loans. In this setup, both banks (lenders) and NBFCs (originators) share the risk in a predetermined ratio (typically 80:20). [Specifically, 80% of the loan is with the lender, and a minimum of 20% is with the originator (https://www.go-yubi.com/blog/what-is-co-origination-and-how-does-the-co-origination-model-work/)

The primary goal of co-origination is to provide more funds to priority sectors, such as micro-finance and MSME lending.

It allows NBFCs to overcome funding challenges, expand their assets under management, and focus on client servicing, while banks benefit from diversifying their loan portfolio and meeting priority sector lending requirements.

The net loan origination appears muted across all buckets except for the micro enterprise loan-book. Here could be some potential reasons:

Market Conditions: Economic factors may impact borrower creditworthiness and demand for loans.

Lender Strategies: Banks and NBFCs may strategically focus on specific segments, affecting overall origination.

Tighter Lending Standards: Lenders might apply stricter criteria due to risk considerations.

Liquidity Constraints: The NBFC sector faced liquidity challenges, impacting origination

Interest Rates: Changes in interest rates can impact loan demand, with higher rates typically leading to reduced borrowing. But considering the recent FOMC meeting it looks like there are good chances of a rate cut by the US Fed in the month of September which might take care of this problem eventually.

Inspite of tall claims by CEO and management, share price is coming down . This is due to regular and continuous increase in equity. Whatever little progress is there in profitability, earnings are getting diluted by bigger share capital. Without details road map on equity dilution, share price will continue to decline or, in best case scenario, consolidate.

Equity dilution is very normal for a high growth small financial companies. Without a significant equity raise they cannot raise debt and hence cannot lend.

Equity can only be raised by equity dilution. When Ugro reaches a sustainable 17-18% ROE, the need of equity raise will decreases drastically. Ugro foresee to reach that ROE level in the next 2-3 yrs.

As an example Bajaj finance raised equity via dilution continuously between 2012 to 2019, and later the speed got decreased drastically.

However, I do agree with you that the dilution really hurt the EPS growth. The problem is we are in the high interest rate environment wherein NBFC sector is not at all performing, this is visible in the share price of most of the NBFCs. As a result, more dilution is need to raise the equity. Having said that, with good financial performance the market will realize the potential of this company and reward by appreciating the stock price, as a result the next equity raise (after 10quarters) will be at the higher stock price and will leads to less dilution.

When all the managements’ materialize and operating leverage kicks in the PAT will increase drastically and will negate the ill effect on EPS growth. For example the PAT increased by 200% from fy23 to fy24, whereas the EPS grew by 128% in the same period.

Summary: Raising capital via equity dilution is the nature of the business and not capital mismanagement or anything else. Management is using capital very efficiently and this is clear from their strategies, rest their future results need to be checked diligently.