great update by the company

after a slow q1, things have picked up this q2.

Disc- Invested

3 Likes

I’ve recently been studying this stock after I saw Arihant Capital aggressively push it, and am still fairly new - broadly what I understand as the right to win is that it’s an innovative tech solution backed by on-ground hands-on sales/support staff. I had some queries -

-

One thing the management seems to boast of is that their default ratios (both actual and assumed) are far lower than the market. This begs the question - how does a lending company grow aggressively without sliding down the credit curve?

-

There has been some talk of NPAs but I can’t readily find data on this, for e.g. in their last update. Is it normal for a lending company to not disclose this upfront?

3 Likes

How can we acess arihant report.

1 Like

UGRO CAPITAL AND UNITED STATES INTERNATIONAL DEVELOPMENT FINANCE CORPORATION (DFC) PARTNER TO INCREASE FINANCE INCLUSION IN INDIA

2 Likes

Recently they have posted very good quarterly update, and before massive 1280cr capital raise and now 330cr fund-raise.

Many good news, but somehow the stock is not moving at all.

2 Likes

Yes. Even I am surprised. Collection ratio and NPAs are the only missing pieces.

1 Like

Results are mixed. Seems pain ahead. Only AUM has increased all other metrics are down. ROA has decreased. NPAs increasing, also interest margin has increased. Why has rating upgrade not helped. Supply chain financing has GNPAs of 10% up from 7% last quarter. Stock will become cheaper based on Price to book but immediate future doesn’t look very rosy.

3 Likes

Disagree largely.

NPA increase is marginal, not much to read into at this stage. RoA drop also marginal, and largely because the A in RoA has grown sharply with AUM, but the R in RoA will take time to come through as these assets mature.

Rating upgrade will take some time to play into the cost of funds. Also once interest rates start decreasing, which is not too far away, I expect NIMs to expand in the short term.

Only unknown is RBI’s disposition to and any modifications of colending norms.

Disclosure: Invested from 170s. No transactions in last 30 days. May add sone if it corrects mlre with the broader market.

8 Likes

10% GNPA in SCF looks elevated due to the fact that management has completely halted the disbursement of loans in this vertical.

One observation: If you completely remove the 355cr outstanding book of SCF the GNPA on rest of the AUM is only 1.8%.

Disbursement of 615cr as co-lending is huge (highest in it’s peer, like SBFC and Five star), this shows the banks trust Ugro’s underwriting methodology. Massive debt raised at the time, when bank lending to NBFC is not prevalent, is worth mentioning.

I feel the business momentum is good and the management has finally found their Mojo (micro enterprise lending), and share should also do good in the quarters to come.

Invested and biased

7 Likes

2 Likes

The way economy is crumbling down, I don’t think RBI will wait longer to cut interest rates. However, there won’t be any big rate cut, if the inflation is not easing out.

2 Likes

No chance of rate cut soon.

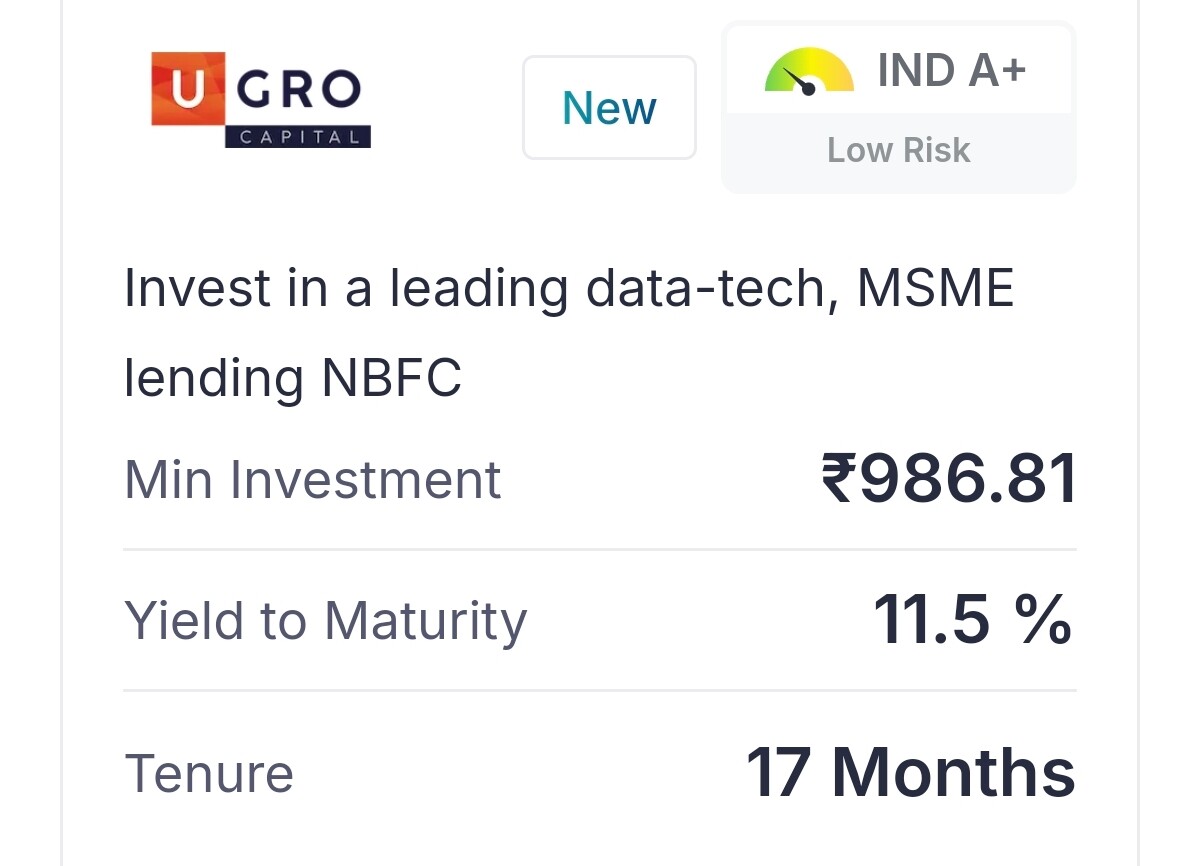

From a shareholder’s perspective, the significant increase in yield to 11.5% for this investment in U Gro Capital could indicate rising borrowing costs for the company. While this higher rate may help attract more retail investors in the short term, it raises questions about U Gro’s financial strategy and cost structure.

For shareholders, such high yields could mean either a squeeze on profit margins or a potential increase in the risk profile of the company’s lending book, especially if they pass on these costs to MSME borrowers who may already be under financial pressure. In the long term, sustained high yields might impact profitability, dividend payouts, or even share value if U Gro faces challenges in maintaining healthy growth without compromising asset quality.

Could anyone explain the reasons behind such a steep increase? It would be helpful to understand if this is specific to U Gro or an industry-wide phenomenon for MSME lenders. Knowing this could provide insights into the future trajectory and risks associated with investments in this sector.

4 Likes

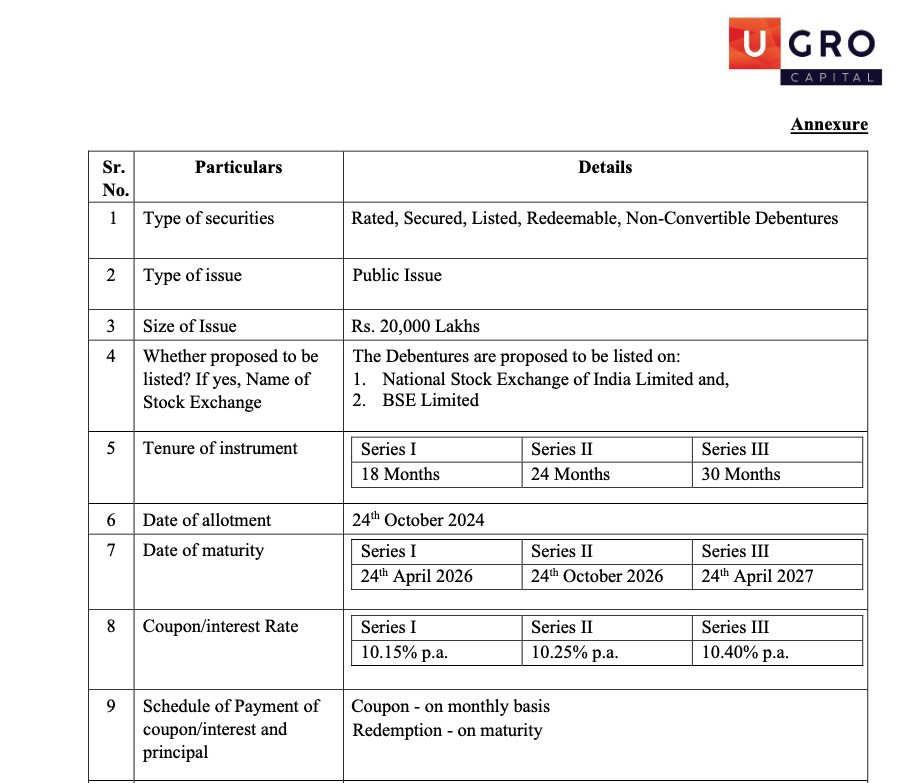

@Akash_Padhiyar I think you miss-understood the concept of yield to maturity. It is not same as Annual Coupon Rate or annual yield.

The annual coupon rate here is approx. 10.5%. On the contrary, the cost of borrowing here is lower than their current aggregate CoB which is 10.7% (as per Q2 earnings).

Community please feel free to correct me, if you disagree!

1 Like

Thank you for clarifying the distinction between Yield to Maturity (YTM) and the annual coupon rate. You may be right regarding the current coupon rate being below the aggregate cost of borrowing at 10.7%.

However, I noticed that previous bonds were trading at less than 11% YTM, whereas these new bonds are now offering an 11.5% YTM. Doesn’t this indicate an increase in the cost of borrowing compared to past issuances? This higher YTM could reflect a shift in market conditions or perhaps a change in U Gro’s funding strategy.

YTM is a complicated calculation and fluctuate overtime. It’s calculated after discounting the future coupon payment. Kinda DCF method.

I would just focus on annual coupon rate. Post rating upgrade, it’s evident that their incremental CoB has been reduced. Since, only new funds are being borrowed at the lower rate and the older borrowing was at higher rate, it will still take some to see the material change on the aggregate CoB.

Attaching screenshot of the recent fund raised via allocating 200cr worth of NCDs in October 2024. Check for yourself the Coupon rate, which is materially lower than the aggregate CoB.

3 Likes

Comparing the YTM of a new issue to the YTM of an old issue trading on an exchange can lead to incorrect conclusions. After issuance, once bonds are listed for trading, their market price often differs from their face value, even if it was issued at par. The bond’s current price inversely affects its YTM.

In UC’s scenario, the older bonds offered higher coupon rates than the new ones, making them more appealing in the secondary market. This demand drove up prices, which in turn lowered the YTM.

When bonds are issued at face value, the coupon rate is the primary focus. However, if they are issued at a discount, both the discount and the coupon rate must be considered.

As equity investors, we should compare the coupon rates/YTM at the new bonds’ issuance with those of the older bonds at their issuance, rather than the old bonds’ current YTM.

2 Likes

6 Likes

With the recent actions of RBI where they have asked NBFCs to stop business because of charging high rate of interest (among few other reasons) … Isn’t charging such high rate of 20%+ from micro enterprises may also land up NBFCs like UGRO in the same situation.

And in case they will charge less, and cost of fund at such 10% level … ROA will get hit, and accordingly the ROE.

URGO being next Five-Star … seems similar to the story of IDFC First being next HDFC Bank.

3 Likes