Aum has two components on book and off book, in book 100 percent is on balance sheet and off book about 20 percent. So roa is calculated on 100 percent in book + 20 percent off book aum… that is my understanding…. Sad to them trimming their 2025 guidances… even after having so much capital… they aim increase their roe to 18 percent this year so i think now profitability is top priority

At 12000 cr aum 6000 would be on book and 6000 off book total bs would be 6000+1500=7500 cr. So profit should be 3 percent of 7500 = 225 cr /4 =about 65 cr in q4 next year and assuming 18000 cr in 2026 it would be 9000’+3000 = 12000 and considering roa equal to 4 it would be 120 cr in q4 fy 26 but that is lot of assumptions:)… good thing is book value after fund raise would be 210 rs and getting a 2.5 multiple would increase price to around 500 this year and if rate cut happen price may move further

2 Likes

Huge Capital raising @264 is certainly big considering the fact that stock was 260 level on 30th APRIL. From the list submitted, allottees are many. Then why the stock is not galloping ? Why retail investors are not flocking to this sound business model but are running after dud companies with astronomical PE ratios? What happened to common sense? None the less I have started acquiring in small amounts.

Only caveat is that 25% is payable on allotment of warrants. And on CCD there is no clarification regarding payment on allotment.

2 Likes

One reason for lack of buying frenzy in Ugro capital could be that this stock does not figure in the broker funding list due to which punters, day traders etc are unable to play in this counter.

Only when the liquidity goes up along with market cap, ugro will become eligible for broker funding.

Another important thing is that the mngt has said that they have raised capital now to take care of any adverse market conditions later on. So that takes care of any election related surprise in June 2024 or a black swan event like Capital gains tax shocker in the coming budget or recesssion in US…etc. With additional capital locked in and branch expansion in place and interest rates expected to come down and ratings upgrade…its time for Ugro mngt and employees to run hard …run fast and deliver the promised 4% ROA & 18% ROE.

This makes Ugrocap a safe investment stock for next 2 years with a potential price target of around 1000

incidentally the long term chart pattern is more bullish. If there is a close above 350 by end of June quarter, then ugro becomes an excellent momentum stock too…it then makes a transition from being potentially bullish to being actually bullish.

Those who wish to buy more of ugro may wait for a weekly close above 290…till then its better to wait on sidelines.

9 Likes

ROA is calculated as Avg of assets/Net Profit.

Avg assets = (Last year assets on BS+ This years assets on BS)/2

You can use the numbers from the presentation, Avg assets around 5100 cr and PAT 119 cr, that will give ROA of 2.3%

2 Likes

This is the info I have:

- CCD - 12% coupon to be paid at end of 18 months (Possible that Big investors may have negotiated different rates)

- Conversion Date - 30th Sep (18 months from 1st Apr)

- Conversion Price - CMP (*Conversion Price will be as per SEBI ICDR Regulations)

- Warrants - 25% upfront

I of course don’t know what the market is thinking but the book value per share growth rate is quite ordinary for this stock. This is due to constant and large share dilution that is happening.

In my understanding this is what matters in the financials.

Book value would increase stupendously by equity infusion… the dilution would if done today would result in 45 percent extra share and equity would double ….yes after that book value would hardly increase with profit 14 cr share and 140 cr profit would increase 10 rs but equity infusion would substantially increase book value

As per quarterly earning presentation the book value per share at the end of:

Q2 FY24: 150.2

Q3 FY24: 153.8

Q4 FY24: 157

So, no compression of the book value.

1 Like

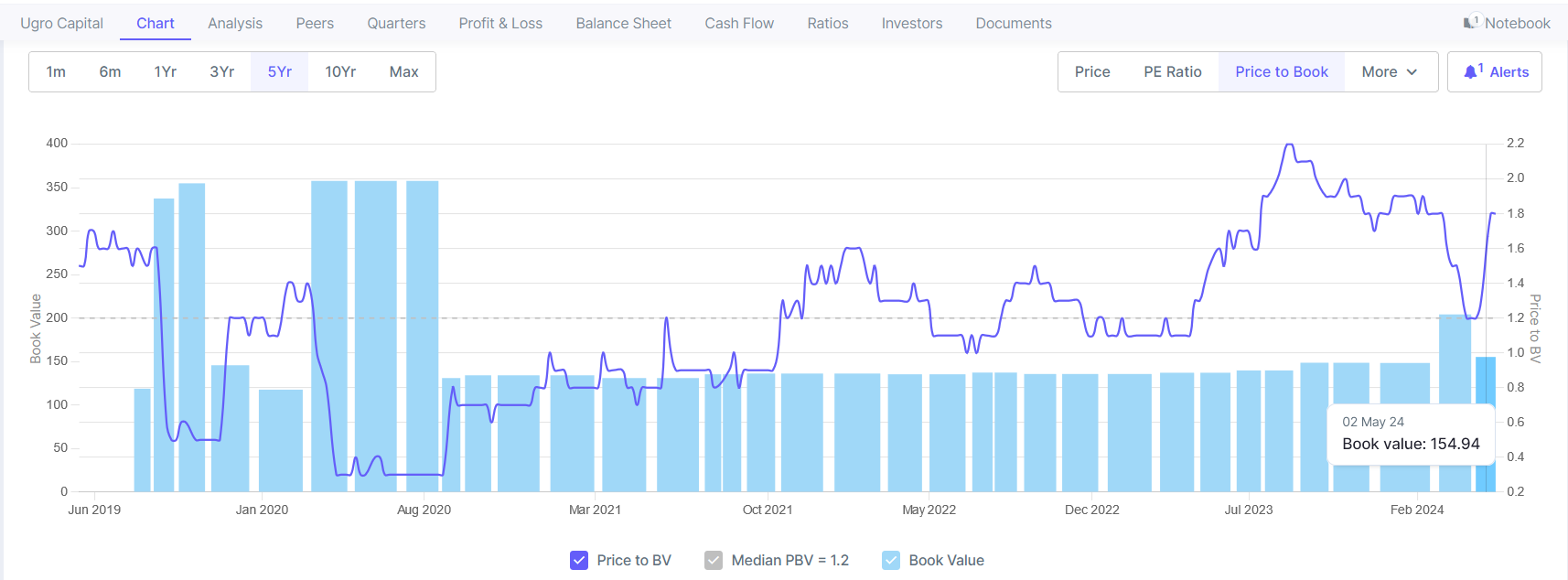

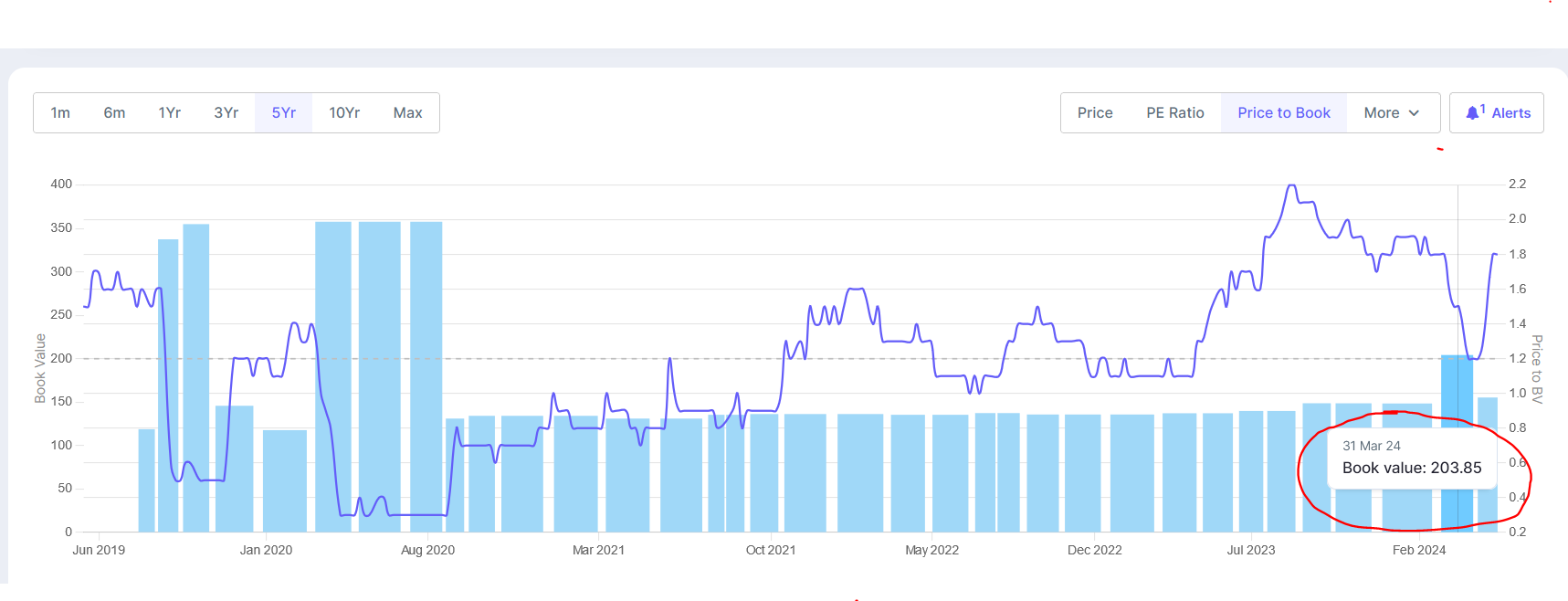

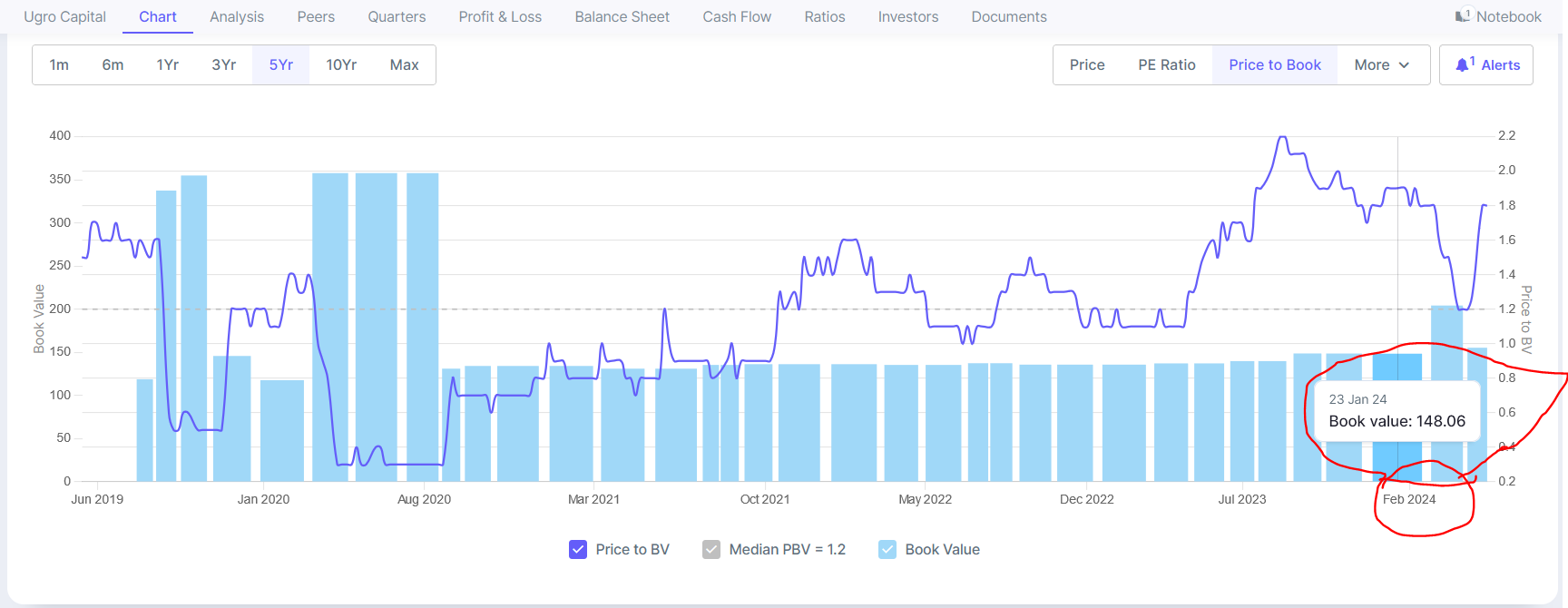

Thanks a lot. Don’t know how screener take this data ! See they take strange date to mention the book value.

23 Jan 24 → 148.06

31 Mar 24 ->203.85

02 May 24 ->154.94

Do you know why?

And from where I can get correct book value data other than investor presentation for any NBFC?

I was struggling to calculate the CAR (capital adequacy ration) of Ugro capital. Could someone please help me calculate this?

Due to their on and off-balance sheet lending model, i do not know how to find the risk weightage asset. Thanks!

I would say the book value of all the NBFC is quite accurate at screener, wrt. Ugro capital, it maybe some on off error by the screener.

1 Like

Hi Gaurav

Thanks for sharing this information … I did not fully understand the implication of this maybe as a beginner investor… can you please share in slight detail why has book value increased and what implications it might have on potential valuation / share price of the company ?

Book value has increased yet till money comes in… let take case of equity infusion of 1332 cr . Total capital would be 1400+1300 equal to 2700 cr and assuming ugro earns 300 cr pat in next 2 year . With no dividends total capital would be 3000 cr and with 15 cr share book value would be 200 per share. Now it is upto what multiple mkt give assuming 2.5 it would be 500 rs and if it get 4 like sbfc it would be 800 after 8 quarter

3 Likes

I am following Ugro Capital very closely, but the share price is not moving at all, looks like someone is artificially controlling the price movement.

- Company raised 1332cr which is approx. 55% of their market cap and 90% of their current net-worth, part of the very high growth company and sector, at the peak of rate cycle, pristine management, what else does the market need to re-rate the company?

- SBFC or Five start business have as big the AUM as Ugro, still Ugro is at mere 2.6kcr Mcap. Could someone help me what is going on, is it at the cusp of breakout or more pain is ahead?

- Why is stopping small cap mutual fund taking position in this company, when they are receiving thousands of crore INR every month in SIP form?

4 Likes

- The money they’ve raised was by issuing new shares/ warrants. So , include those shares while calculating the marketcap.

- The business models are different. Not a fair comparison

- Mutual Funds may have better investment opportunities. They may buy HDFC Bank, or Axis at 2.5-3 P/B, instead of Ugro at 1.5-1.8x P/B

2 Likes

- Even you add up all the shares and warrant, the Mcap would be around 3900cr but the CCDs and Warrants are convertible after 18months. By that time the company will have used the money to lend more and get more profit. If you add the capital raise of 1332cr and current networth of 1440.

The total net worth = 2772cr

Total share = 9.3 + 5= 14.4cr

BV= 193 INR

CMP/BV= 1.39

Now, are any of the mutual funds getting such a pristine quality NBFC at such as cheap valuation? I doubt.

SBFC, Fivestar and Ugro are all MSME lender, i guess we can compare them. Also, their target customers in many ways are also similar.

6 Likes

The public holding exceeds the promoter holding. This could potentially impact the share prices.

It’s a professionally managed company and the major stake is with FIIs just like HDFC bank and for that matter just like any other bank.

promoter stake is irrelevant on financial institutions as they have to raise capital a lot in the initial days, which leads to the stake dilution of promoters.

Example: Aavas Financiers, SBFC, etc.

Indeed there are a few NBFC i.e, likes of Bajaj Finance, Kotak who had the backing of the giant parents and are managed to have promoters. However, they are rare companies.

1 Like