They do secure lending to SMEs at ~14%. Which is actually aligned with market range. My family being once part of the informal lending system can say that these kind of yields are actually inline.

Even today, good businesses do not mind taking credit at 12-15% range in cash (& goes unaccounted from formal P&L reporting). Now for credit taken from likes of Ugro, the interest expenses becomes part of formal P&L and hence net-net beneficial for the debtor (vis-a-vis informal loan).

Usually in any sector, whenever informal and formal competes, formal business suffers because of compliance, tax costs etc. Herein, UGRO is competing head-on with informal lenders & this makes it a unique proposition for them (they just need to keep their asset quality, credit cost in control).

While a lot of technology & personnel cost is front loaded for Ugro, they seem to be still struggling with the key capability of collections. Ultimately lending is an easy business, it is the collection muscle that will separate a leader from the rest.

Ugro Capital’s management, expressing confidence in asset quality, positions the company for potential rerating and significant wealth creation.

The assertion aligns with the current growth trajectory, indicating a positive outlook for the company’s financial health. Should the management successfully execute their strategy and maintain robust asset quality, this accomplishment could pave the way for enhanced investor confidence, potentially resulting in a rerating of Ugro Capital’s valuation. Such a rerating has the potential to generate substantial wealth for investors who align with the company’s growth narrative.

However, it is essential for investors to closely monitor the company’s performance and market dynamics for a comprehensive understanding of the evolving scenario.

Ugro capital has touched 200 DMA today. Correction was with low volume so indicating not much worry on technical front.

But recently company has started updating events and disclosure via whatsapp. I would take it as a red flag as when a company over emphasised its achievement to retail shareholders, “dal me kuch to kala hai…”

I want to know boarders view on that. Are there any other companies doing so? Is it a normal trend?

I don’t see it as a red flag either. On the contrary, I like the fact that they are being pro-active in keeping us in the loop by providing all the key updates and happenings. If I look at the last few messages i received, they talk about 1. Launch of MSME Sampark - which has details of how the MSME ecosystem is evolving 2. Impact analysis of the interim budget 3. Confirmation about raising 250 crores through NCDs 4. Earnings report 5. Press release of Q3 FY24

Maybe what we can watch out for is, see if they will continue to send all information, even bad news, with the same enthusiasm and transparency. If they do, this is a good move.

I don’t think any of them is accurate. I searched for a few names and couldn’t find any of them related to the company.

Neelesh Choukesy - PPFAS (I have invested in this for quite some. Never heard of a person called Neelesh)

Anil Talreja - Edelweiss (No such person existed or resigned)

Jaideep Goswami - AU Small Finance Bank (Same here).

Thanks community for sharing so many important insights about Ugro. I am quite convinced of the future prospects of the company and have started building position steadily.

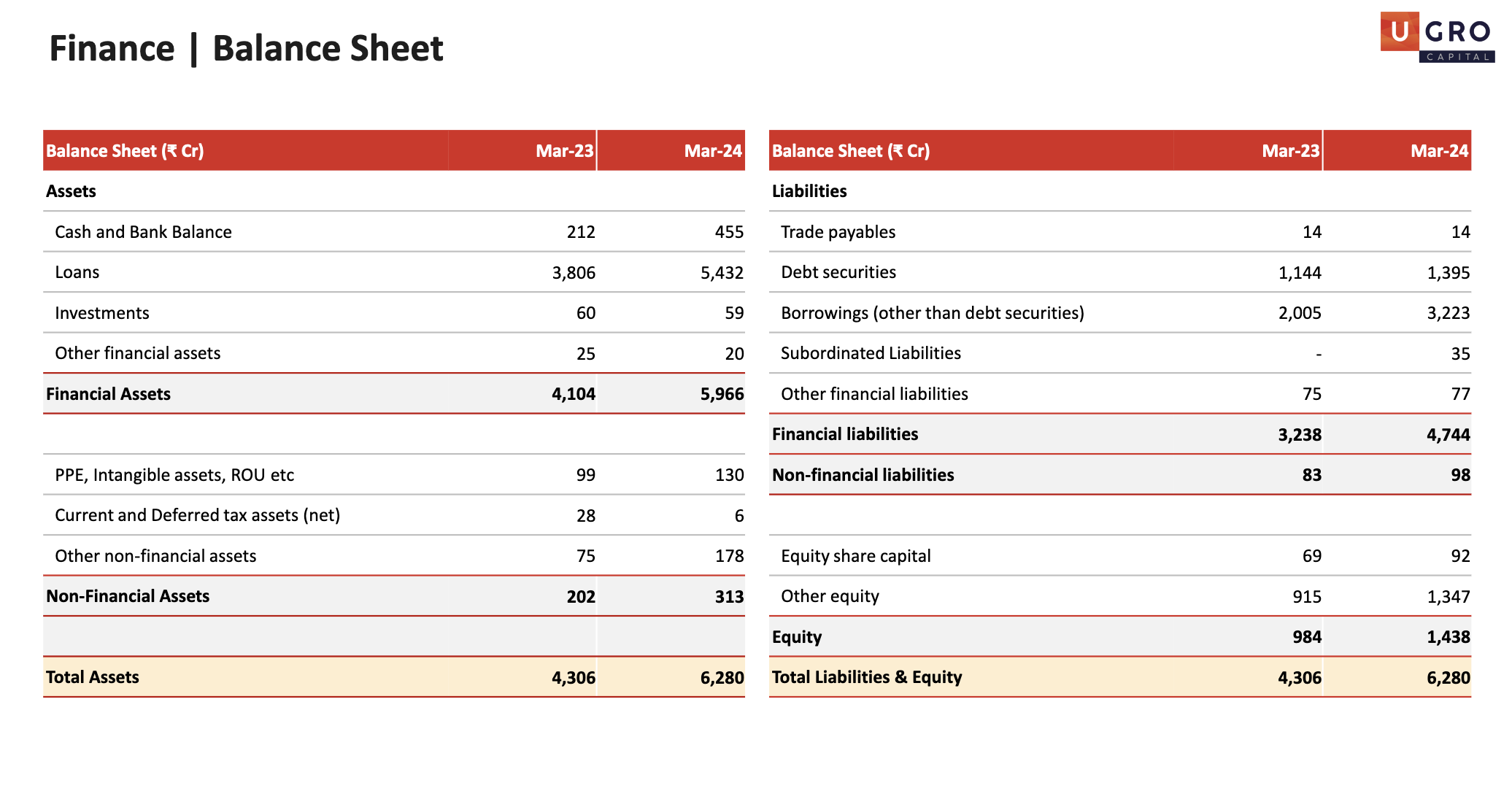

The net worth of the company is 1400cr and the current Market cap is 2000cr. This comes around 1.4 times. For a company like Ugro, which is growing at this phenomenal rate and maintaining above average profitability looks unjustified to me.

Do you think this is a time to invest heavily with a long term investment horizon?

It’s a financial institution, unlike other companies, they do not throw lots of cash flows. Banks are built to sell cash. For reference check the snap shared by Mohit in the post above, even Bajaj, shriram, HDFC bank, etc. have negative cash-flow.

FCF is not a relevant metric for valuing a financial institution. Because FCF calculations exclude the major source of earnings for an FI, interest income.

Here is a doc which will be of help to understand FI valuation

Even if Ugro wouldn’t have been an FI, most likely its FCF would have been negative as it is currently in Capex/rapid expansionary mode which requires lots of front loaded investments.

Very good result for the whole year, however some concern on the credit cost/asset quality for Q4.

I am personally astonished to see that Ugro was able to raise 1332 Cr from the large renowned family offices, that too at very good market price. 1332 cr of capital infusion is suffice for pushing the AUM over and above 22K in the next 2-3years.

Current book value is 157INR. At the CMP of 284INR the P/BV is just 1.8. There is a strong possibility of re-rating to 2.5 to 3x P/BV, considering the asset quality remains stable.

Could anyone of you help me to understand how the ROA of Ugro is being calculated for F24.

ROA: 2.3%

AUM: 9047Cr

On book and off-book mix for loan is 55:45

Management said that they calculate the ROA on balance sheet and not on AUM. Please explain me the calculation. Thanks!