there is nothing new under the sun, lending is process from ancient time… The only good thing they do is to keep liabilty/ assest in check and grow their aum, profit would automativly come…what has idfc done to triple its value compare to other bank in last 15 month… nothing special… ugro is not in business to devlop new vaccine, create new ai, but the bussiness which has created wealth all over the would has been mostly lending the money, feeding the people and catering to basinc requirement. Real investment is boring

Disc: invested

7 Likes

Update for the quarter -

4 Likes

I had a conversation with the head of co-lending at a large PSU bank. They have interacted with Ugro daily for the last two years.

Key pointers from the discussion:

On Co-Lending

-

Co lending uptake from PSU banks has been slow due to skepticism about the MSME segment in the wake of covid. Finally after the second wave resolved, co lending has picked up to an industry size of around 25,000 Cr. today. The formal landscape is around 400,000 Cr. and can be easily reached in 10-15 years.

-

There is a split between private and public sector banks on co-lending. Public sector banks want to partner with large NBFCs and are keen to have a social impact: formalisation of credit, bring more people within the purview of a bank, without compromising on asset quality. Private banks in comparison want to partner with small niche NBFCs, where they see co lending as a way to create a product, and lend to a segment they haven’t already tapped (example: Trucap and HDFC).

-

Banks have daily reviews of portfolio quality on co lending, and set collection efficiency targets for NBFCs, and have close discussions on all aspects of the book frequently. If something isn’t right, they slow down. Conversely, if things work, they will scale relationships.

On Ugro and the Competitive Landscape

-

Tech integration is extremely important in co-lending. RBI regulations require co-lending to be done on the same day as disbursals. This cannot be done by manual entries at scale. Ugro very early understood this and were ready with an API stack, middleware and a digital platform. They were an early mover/leader in the space, and this alone is not an advantage today, as everyone else has had to invest and build to get to the same stage.

-

Bank and NBFC have to simultaneously underwrite the loan. NBFCs have proprietary scorecard models, and do not disclose the workings to banks. Ugro’s approval ratings were very low in the early stages of the relationship. Today, the approval ratings under co-lending are up 8x from the early days. Rejections are due to a difference in interpretation of policy, and 70% of loans sent from Ugro’s side are accepted by the bank, and is a great number in the bank’s eyes.

-

There are several things Ugro does right in the bank’s eyes.

a. Relationship was slow in the early days until bank got comfort in Ugro’s collection mechanism and quality of the book that was passed on. Did secured lending initially, but now have started to do unsecured.

b. Middle management is very good, no one has left in the last couple of years. This keeps the bank happy, as there is continuity in working relationships. They have brought on more quality people, and have become more stringent with regulations and underwriting.

c. A loan that is sourced doesn’t differentiate which bank it goes to. Ugro is very good with knowing what exactly the bank wants, and sending them the correct loans for their requirements.

d. There is no USP today on a product / segment. The market is very large and can accomodate lots of players. Working culture is more important to the bank than a lot of things investors look for like USP. There is no complaint with Ugro at the moment, no challenges and Ugro is upfront in their discussions with the bank. They constantly ask what kinds of expectations and ratios the bank wants in their secured/unsecured book. Softer USPs are the ability to bring the right pockets of people into formal credit.

e. Religare was a non issue. Regulators have no complaints, company has managed to raise a lot of capital from a good investor base. Management is known in the industry and is capable.

f. Another highlight is the digital collections system, where collections are based on NACH/e-NACH, and documents are digitally signed without physical copies. Cash collection has a lot of compliance risk. Peers like Paisalo have fallen behind in this respect.

g. Co-lending discussions start with an expected credit cost of the product, and then targets are calculated in reverse. As an example (not actual figures), if you are pricing in 5-7% stage 2 NPAs, then collection efficiency targets are around 93-94% initially. These are then recalculated on the product and life cycle.

IIFL and SBFC were also discussed as really good names in the industry. SBFC was called an excellent company. Capri Global has poached good people from IIFL and has built a book quickly.

Lastly, by regulation, direct assignment can be classified as co-lending. A lot of PSU banks talk of scaling the co lending book, but it’s DA that gets scaled, not true co-lending. It’s important to focus on this distinction amongst stakeholders in the future.

Disclosure: invested and biased. These conversations rarely are made public, and I’d like to give back to the community.

65 Likes

@Chins Thank you for the scuttlebutt update.

I have had cursory look at Ugro Capital and have not been comfortable with overall setup. I have not done deep dive work. It would be good if you can help with following basic questions.

- How does the profitability gets shared in the co-lending model between bank and NBFC? Who dominates the underwriting decision and consequently who has to provide for slippages?

It would be good if you can explain above points with current balance sheep of Ugro as an example.

The reason for asking this is simple. Banks struggle to make 1.5-2% RoA as it is on a consolidated diversified book. Corporate lending and housing loans are low RoA segments. So to boost RoA, banks have to go after credit cards, gold loans, MSME, consumer appliances financing, personal loans etc. These segments provide 3-4% RoA and at an overall level bank makes 1.5 to 2% RoA.

In this case, it looks like Ugro has ambition to make 4% RoA and bank wants to make 3% RoA. That is 7% RoA - which is really high !!!

To achieve this kind of RoA, you have to go after risky segments - unsecured lending, micro enterprise loans etc. You also have to go to kind of customers who are willing to take yield on advances of 20%+.

I am also seeing that collection efficiencies are in the range of 95% which means that credit costs are 4-5% range - which means yield have to be even higher.

With this kind of setup (poor segments, poor customers), why should one get excited about co-lending?

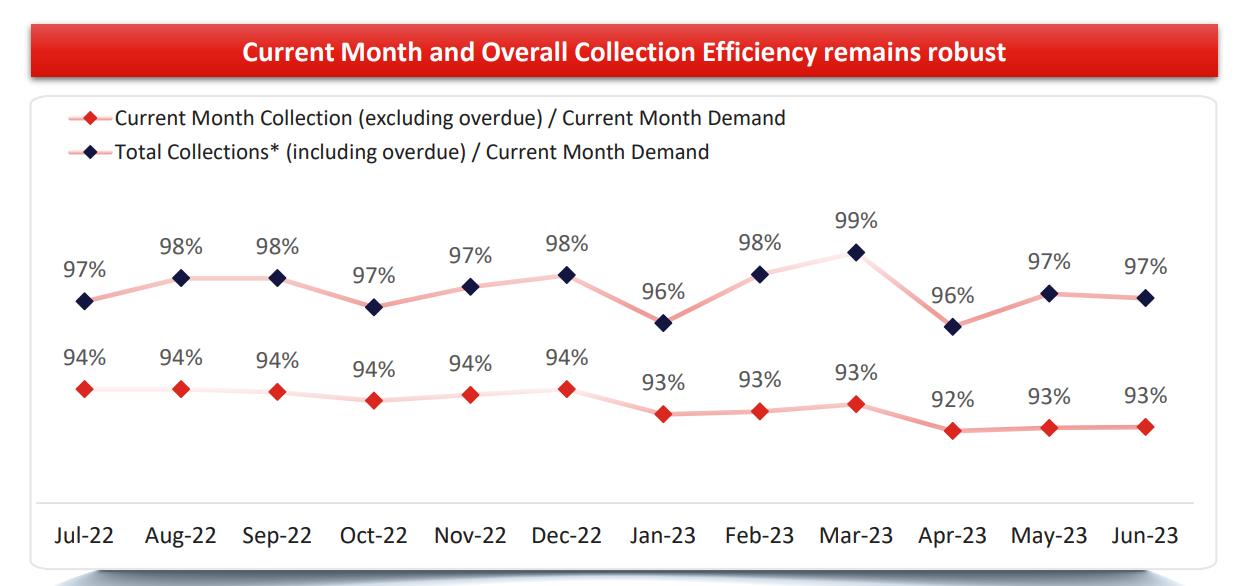

- Following chart is quite worrying for me. When a finance company is growing at fast pace, assumption is that new loans will not become NPA. Which means that collection efficiency numbers should look very good. In this case, I am seeing collection efficiency numbers of 93% even with the fast growth. Which means one of two things - either new loans are also slipping or old loans are slipping at a very high rate (10-15% of the book type).

Please help to reconcile this low collection efficiency numbers.

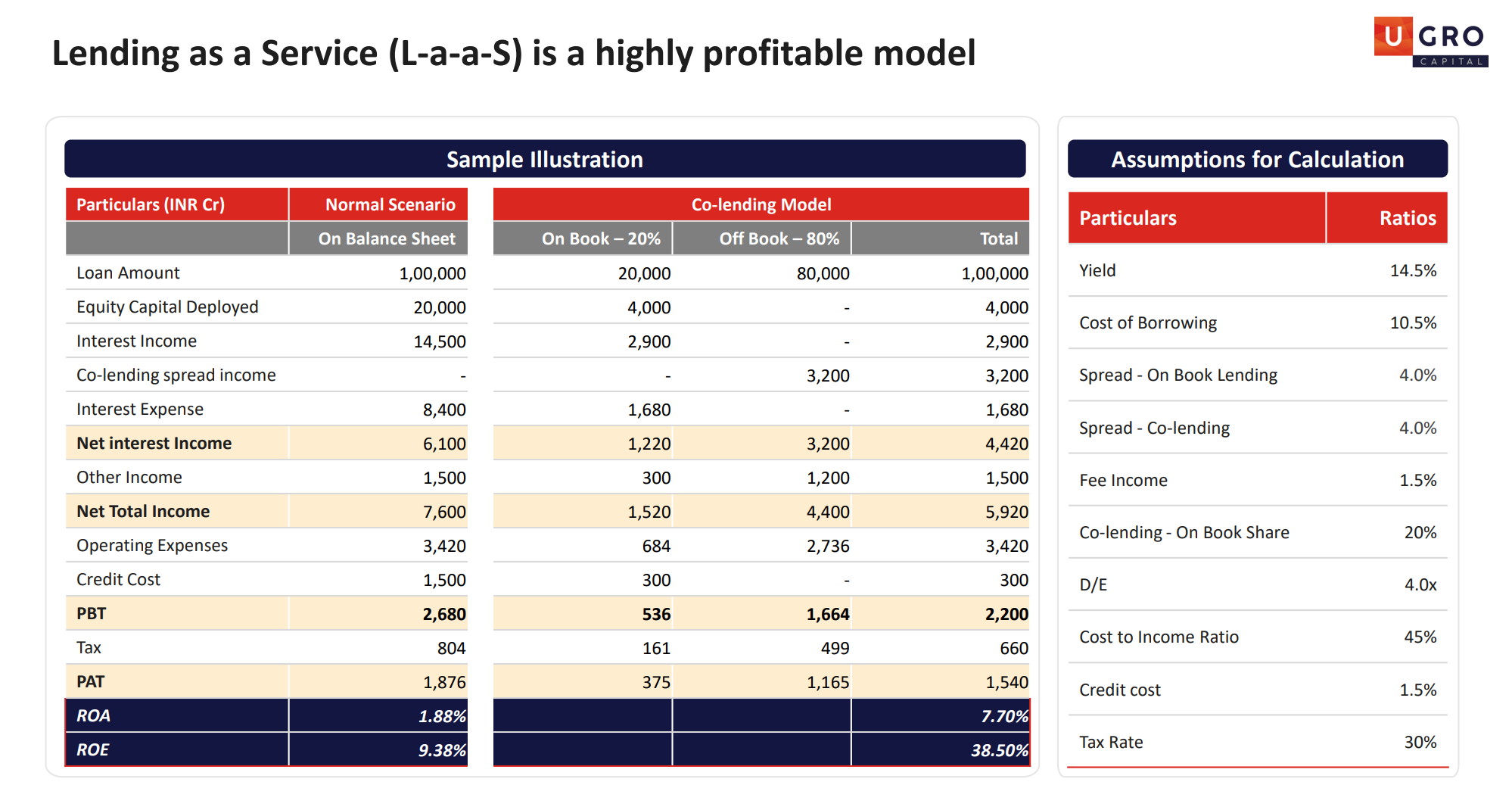

- I also do not get this slide below.

In on-balance sheet model, one is making PAT of 1876 rupees on Asset of 1,00,000 Rs. RoA - 1.8%.

In hybrid balance sheet model, one is making PAT of 1540 rupees on Asset of 20,000 Rs. RoA - 7.7%.

Who are these banks who are willing to take 80% of loan on its book, bear the 80% credit cost and only take miniscule profitability - at NII and PAT level.

Bank’s share of NII = 6100 - 4420 = 1680

Bank’s share of Credit cost = 1500 - 300 = 1200

Bank’s share of PAT = 1876 - 1540 = 336.

i.e. PAT of 336 rupees on asset of 80,000 i.e. RoA of 0.42% !!

It looks like a super raw deal for the bank and very hard to believe.

Bank is taking all the risk on its balance sheet and giving away all the profitability to what is essentially a sourcing agent.

I would expect that bank would have more power on negotiation table.

Disc - No investment whatsoever.

21 Likes

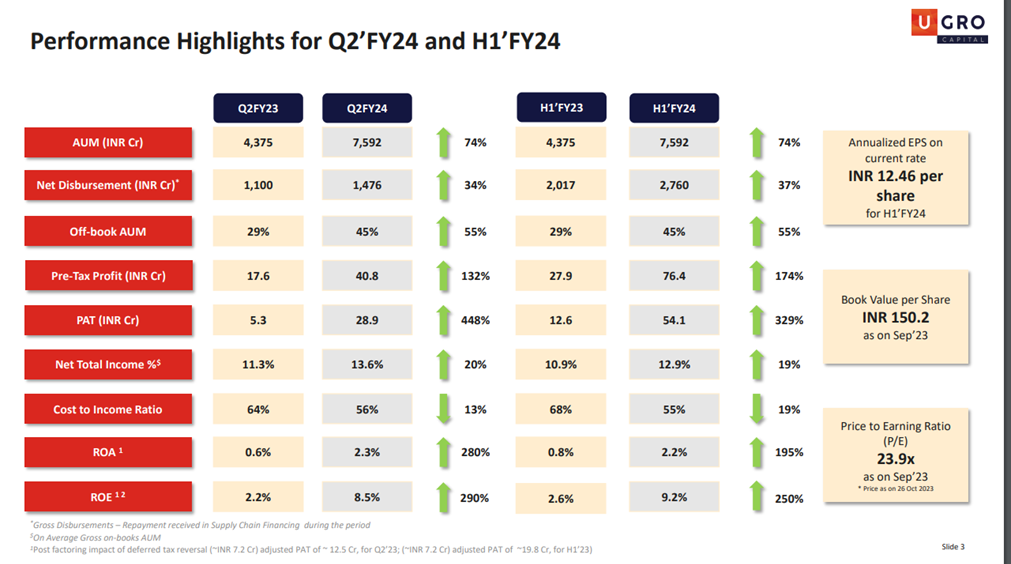

Great set of numbers by UGRO - Better than my most optimistic expectation.

Need to monitor how asset quality evolves as the book seasons.

9 Likes

But their GNPA has increased during the same period, when most of the Banks and NBFC have seen reduction in GNPA. Can someone help me understand this?

2 Likes

Ugro is lending at high interest rates to risky segments and unsecured as well. Their asset quality will never be comparable with large pvt banks.

2 Likes

I couldn’t ask some follow up questions in yesterday’s concall as they had run out of time. Mr. Nath had asked me to write to IR or take it offline.

I have sent the following list of follow up and additional questions: (My comments for VP in brackets)

-

I think RBI has capped FLDG at 5% for each FinTech. Your presentation still states 5 – 15% FLDG cover. So how much does this impact your growth and existing partnerships which are >5%, have they been changed to 5% FLDG?

-

How do you ensure FLDG is 5% at the FinTech level and not for each partnership that the FinTech has?

-

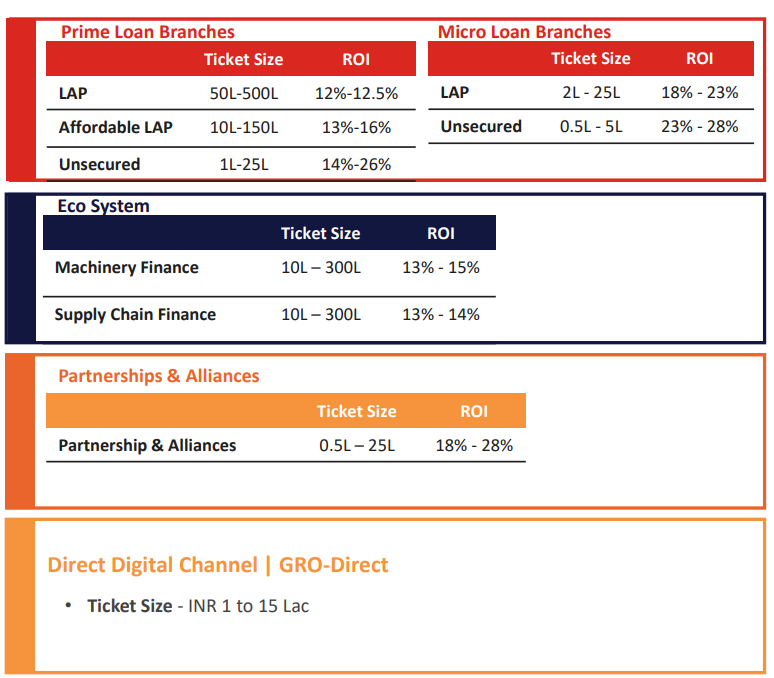

We seem to be the preferred player for secured MSME co-lending among PSU Banks. When do you think PSU Banks will open the flood gates for unsecured lending? Is any other NBFC doing co-lending for unsecured loans for PSU Banks?

-

Is 100% of our collection digital? Or do we still have some cash transactions? When will we become 100% digital in terms of collections?

-

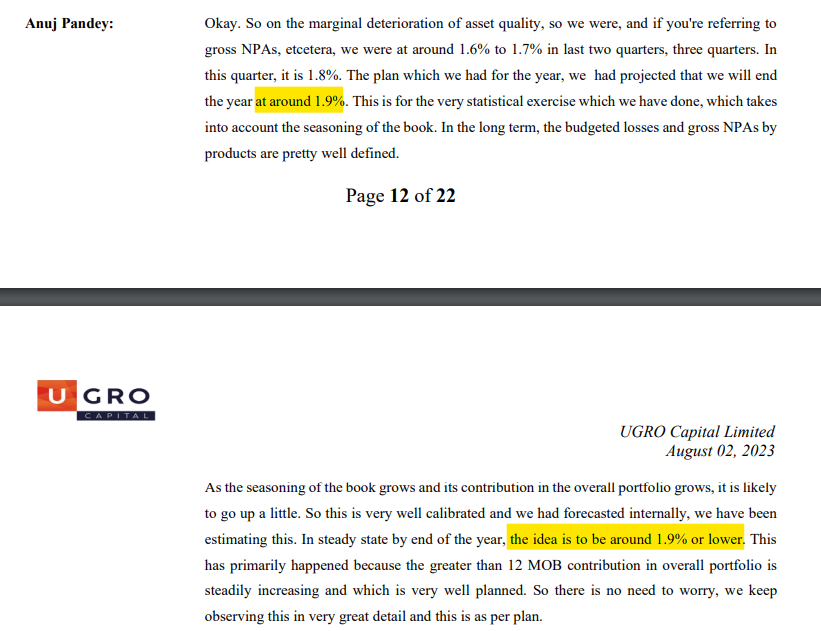

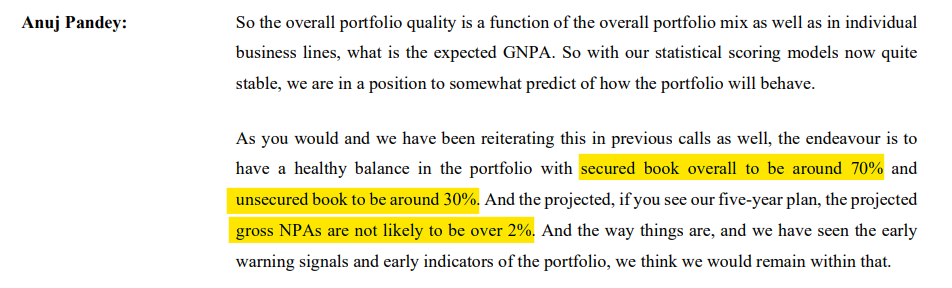

You said the GNPA in prime unsecured to stabilise at 4.0%. Previously you had stated 3.0% - 3.5%. What is the normalised GNPA in this segment?

(The GNPA goal post for unsecured seems to be trending higher with every quarter. Looks like the Mgmt themselves aren’t sure?)

- Say, Unsecured is 30% of mix with GNPA of 4%, and Secured is 70% with GNPA of 1%, is the overall GNPA of ~2% (1.2% + 0.9%) a decent assumption?

(But currently, the secured itself is trending higher than 1% and increasing. So, 0.31.2% + 0.71.5% = 2.25% is where GNPAs will settle at?)

-

How much of micro enterprise is unsecured? Do you want to start giving the breakup of the micro enterprise as well similar to Prime?

-

In Supply Chain Finance, what is the proportion of loans to Anchor Customers vs total supply chain finance AUM?

-

Asset quality deterioration in supply chain finance is basically default by large anchor customers but scale is achievable ONLY by onboarding more anchor customers with risks cascading. How do we see the risks in this business going forward? Do we have anchor level caps? Or anything else?

-

You said in call that you want to keep the Supply Chain book granular and hence dropped ticket size from 1 Cr to 50 Lakhs. But if I check Q4 FY22 ppt, the ticket size is only 42 Lakhs. Q4 FY23 PPT, the ticket size is 95 Lakhs, Q1 FY24, the ticket size is 103 Lakhs, Q2 FY24 it is 49 Lakhs. Why this volatility? Even the tenure dropped from 0.5 years to 0.25 years. What is the existing book ticket size and what is the ticket size going to be for new loans? Looks like we are learning lending on the job which is not the right way. Either that, or we wanted higher growth and hence we started disbursing higher ticket size. We should be learning from other lenders and their past track record. Say someone like CUB.

(Was Mgmt chasing growth at the cost of risk and now course correcting? In one slide in H1 FY23, they have even mentioned 5 Crs for LAP and 3 Crs for Supply Chain. Now they have removed these slides.)

-

How does our ticket size compare with SG Finserv? What do we do differently than SG Finserv, CSL Finance and other MSME or supply chain lenders?

-

How many anchors do we have currently? How many are we planning to add in H2 FY24 and FY25?

-

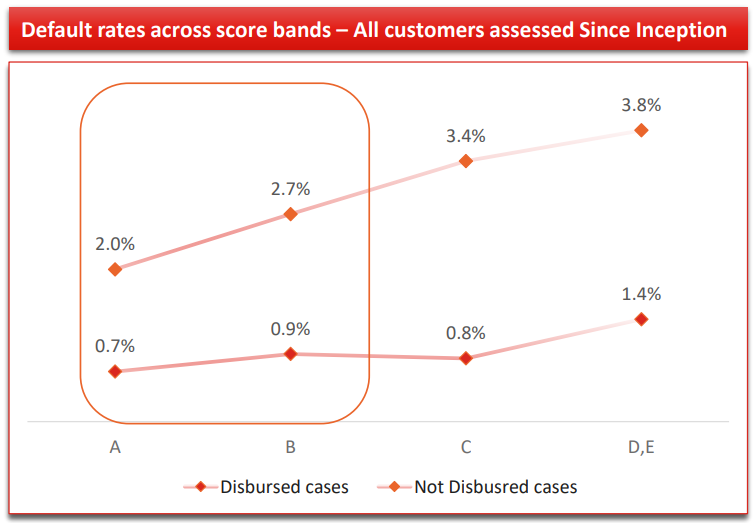

A dumb question. In Q4 FY23 PPT, Slide 10 where you talk about Default rates across score bands – the disbursed default rate of D & E is higher than not-disbursed A and B. So why even disburse to D and E? You can disburse to only A, B and C?

And in 6 months, Q2 FY24 PPT, Slide 11, now the disbursed default rates for D and E are much lower than not-disbursed B and C. What changed in 6 months since this data is “all customers since inception”? Does it mean significant deterioration of not-disbursed customers and that the UGro score is working to tee?

More importantly, why has C’s disbursed default rate declined from 1.2% to 0.8% and D&E from 1.7% to 1.4%? Is this being skewed by new customers who don’t have any default at least for first 3 months?

Please give cohort level data.

Q4 FY23:

Q2 FY24:

-

What are the approval rates in each of your products and score bands?

-

D and E score, which loan product is the major contributor? Unsecured or Secured?

16 Likes

Mgmt reply:

Some questions cannot be answered since this is confidential information and not in public domain.

Digital Lending Guidelines restricting 5% FLDG is for digital lending, for other partnerships the FLDG is restricted to 20%.

We have started doing Business Loans (Unsecured) with few of the PSU Banks, now we have CGTMSE cover for Co Lending as well.

We do not have any cash collection.

Normalized Life Time Credit Cost is around 1.25% Annualized. For more than 21 MOB we are seeing the credit cost to remain below our targeted range.

“Unsecured is 30% with GNPA of 4%, and Secured is 70% with GNPA of 1%, is the overall GNPA of 2% a decent assumption?” - Yes that is what we have designed our asset engine for.

We have a very small portion of unsecured loans in Micro segment.

Almost 95% of our business is to anchor customer in supply chain finance.

We finance the retailers associated with the Anchors so the risk on anchor is very limited, still we have program level limits on anchors.

Ticket Size - We are graduating from higher ticket vendor / Distributor financing to Dealer and Retailer Financing, whenever we onboard a new program the first level of financing happens with Distributor which is normally little higher ticket size and then they on board their retailer which granulises our portfolio.

SG Finserv, CSL - We are highly digital retailer finance which is driven by out GRO Score platform, as far as we understand these companies are still focused on their captive network and mostly vendor financing.

Number of anchors - We do not provide this data being its tracked by competition.

“In Q4 FY23 PPT, Slide 10 where you talk about Default rates across score bands – the disbursed default rate of D & E is higher than not-disbursed A and B. So why even disburse to D and E? You can disburse to only A, B and C?”

Some time in D & E Band the score deterioration is due to wrong reporting where as the data is verified and curated thus making customer eligible and also it is a function of price + collateral as well.

“And in 6 months, Q2 FY24 PPT, Slide 11, now the disbursed default rates for D and E are much lower than not-disbursed B and C. What changed in 6 months since this data is ‘all customers since inception’? Does it mean significant deterioration of not-disbursed customers and that the UGro score is working to tee?”

This means that our hybrid model of Score + Credit Underwriting is working better.

24 Likes

Hey Sanjay, so whats your take on the aswers that you received from the management?

1 Like

How much the new guidelines from RBI about unsecured and not a priority sector will affect UGRO? Any views or thought from experts?

Unsecured book is 31% of total loan book right now.

4 Likes

I don’t believe increase in risk based weights would have any direct impact on UGRO, as they operate in business lending (that too in priority sector) whereas the increased weight is specific to consumer credit business.

There could be second order effect but those would be hard to gauge depending on who their customers are and if they face any slowdown in growth due to new rules. UGRO seems to have a well diversified portfolio across sectors, so I am thinking once the dust settles down and people are able to understand that the change impact NBFCs with lending in consumer credit and not all NBFCs (like UGRO) the stock could recover from the recent lows post the news.

Disclosure: Invested and not registered. Please do your own due diligence as well.

7 Likes

I share the same view as Pratik. I wish Mr. Nath when he appeared on ET NOW should have categorically stated that Ugro Cap isn’t impacted by this RBI decision or if its impacted then by how much, rather he just explained what and why RBI did. Right now market is treating Ugro as if its impacted. Anyways, for long term investors such occurrences only give opportunities to top-up if one is not fully invested.

Link of the interview: https://x.com/CapitalUGRO/status/1725495254546338183?s=20

4 Likes

Timely clarification ![]()

Ugro nbfc clarification.pdf (549.9 KB)

Ugro nbfc clarification release.pdf (556.6 KB)

6 Likes

Wish granted in a recent interview on the same platform

6 Likes

As per this interview, it seems no impact on Ugro capital. Not sure if that is the case

I disagree with no impact, but very minimal impact. RBI’s regulation applies to all retail loans except housing loans, vehicle loans, educational loans, loans against gold and microfinance/SHG loans. The increase in risk-weighted assets will lead to a decrease in the capital adequacy ratios however it is not expected to materially impact the overall capitalization.

In Ugro’s case, we need to see what consolidated AUM comprises of. How much percentage will fall in to RBI’s regulation is the key.

2 Likes

Strange management has’nt shared this update of colloboration with master card through disclosure

1 Like

One of the better interviews of Sachindra Nath.

6 Likes