Thanks everyone for the reply.

@rks00 No, I am not taking about management guidance. I purely talk about the illustration

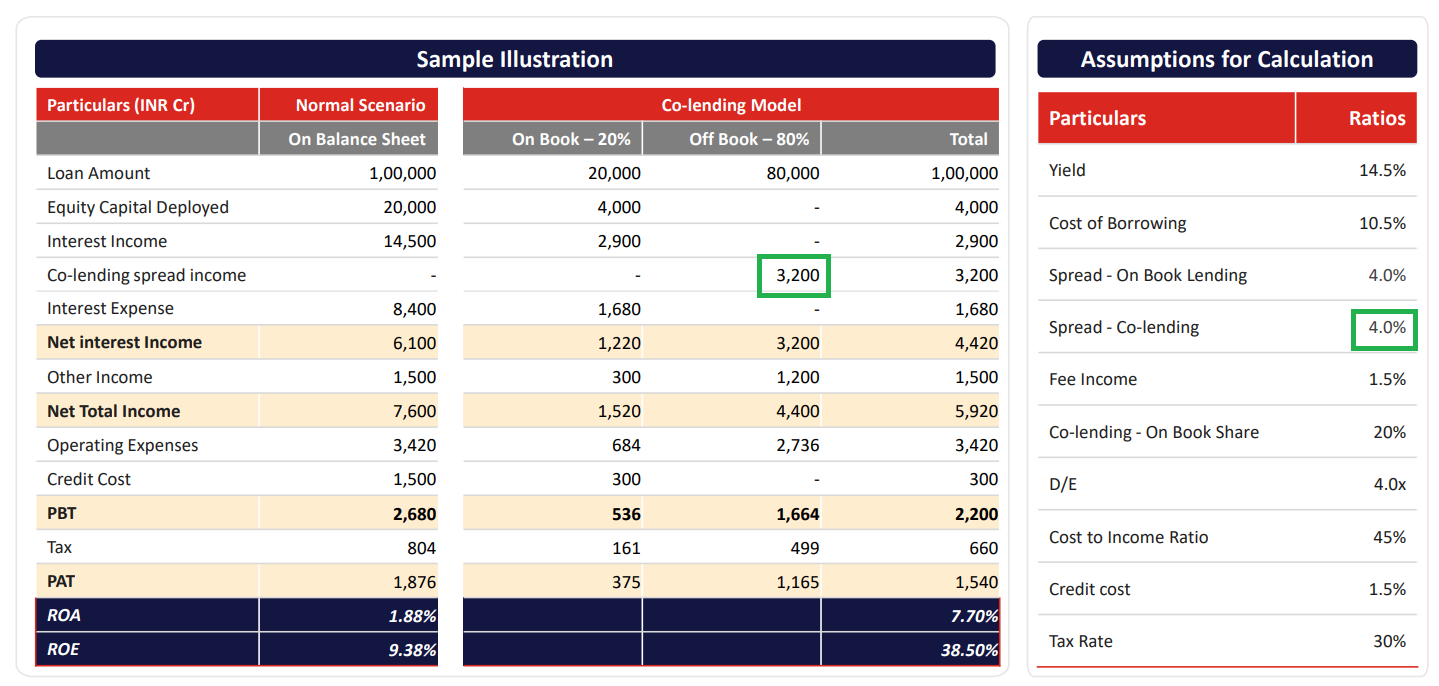

I did not say math is wrong. The point I raised initially is why they are including 3200 cr. spread of the bank’s portion as their income. How you can claim the interest portion of someone else’s money

To elaborate more on this, I was going over the RBI guidelines for the co-lending.

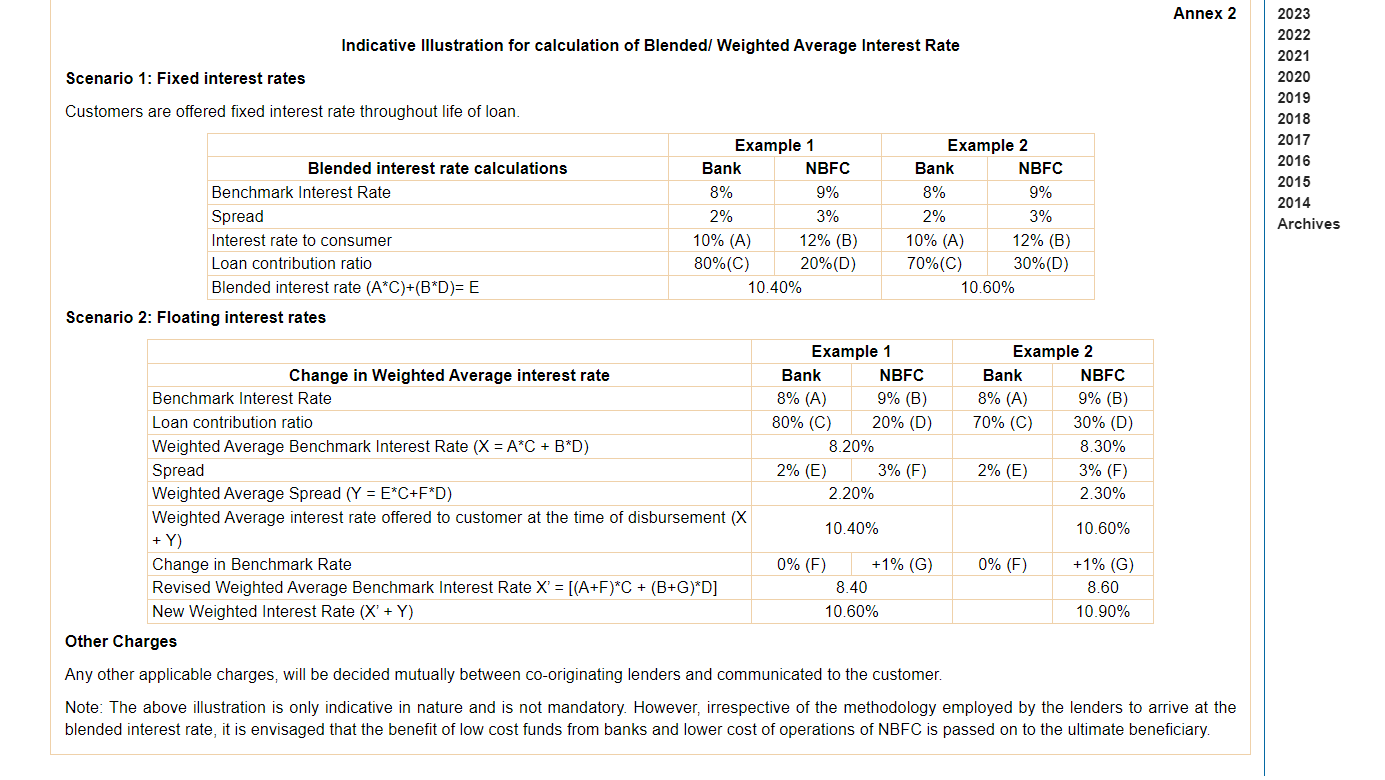

If you see the attached pic which I took from the RBI website and also what I heard in Indiabulls concall, co-lending interest rate is the blended rate of both bank and NBFC. The main motive of this approach is to lower the cost of credit. But as per the illustration stated by UGRO, in both cases(Co-lending and regular mode of lending) they are charging 14.5%. The ultimate borrower does not have any benefit from this.

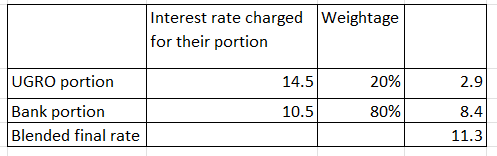

if I go by the logic which RBI mentioned, interest rate of co-lended loan should be 11.3%

I understand companies has some leeway to change the structure of this transaction, but if you read the last two lines of the attached pic, it is clearly mentioned that the benefit of low cost funds of banks should be passed on to the ultimate borrower. As per the illustration, this is not happening and borrower is charged at same rate.

And if you think from other perspective, Co-lending is much like two parties(nbfc and bank) is coming together to lend money to borrower. How one party(NBFC) claims the interest component on the other party’s proportion of the loan(Bank). In securitization this is possible, since loans are securitized at a lower rate and the excess spread can be considered for loss provision and any excess will be passed back to originator. In co-lending, NBFC has nothing do with the 80% of banks contribution, no risk sharing, no loss enhancement. In indiabulls, management mentioned same, two parties have their own interest rate and borrower is charged with blended rate and NBFC get 100% processing fee charged to borrower and they also charge bank some percentage every year as a servicing fee.

I understand the benefits, parties involved and roles in co-lending. But I in here I am trying to understand only the technicality on how this is structured

Disclosure: Neither owning nor tracking. Neither bullish or bearish. Just found this illustration in presentation, so trying to understand the co-lending, as my other portfolio companies do some co-lending