They only have institutional support , last share holding pattern have 40000 retail investors, mutual fund cant buy them as they have written rules for company usually 15 percent roe … And this have gone up 60 percent this calender year ans is within 5 percent of ath… What more one want, this is a long term story as generally all fin institute are… Rapid rise and fall are seen in generally commodity or manufacturing shares

I found this interesting. I was wondering if this company could become a technology company selling this underwriting software to all NBFCs where everyone wants to be SME lender.

Reason I mention is that I don’t like lending businesses. Nature of business is such that there are very few lending businesses which make money consistently over a long period. Whereas a lot of software/specialized services make consistent return. I would have loved this to be a non-lending but tech services business.

8 Likes

Reading their ar theh have again sought permission for a 500 cr equity infusion, now that means at today rate it would be a 25 percent dilution , they should have asked permission in next year agm… Why in such a hurry to pass this resolution when they themselves stated that they dont need fund this financial year… Makes no sense

1 Like

Last QIP - 11/4/2023. Amt - Rs 341 Crs

Proposed QIP as per 2023 AR - 1/8/24 (within 12 months of approval in AGM) - Upto Rs 500 Crs. The amount could be even lesser in case capital markets are favorable the stock price.

Time period between the two - 5 quarters / 15 months

Some snippets from Q4FY23 Concall:

Kishore Lodha (CFO): –We ended the year with a capital adequacy of 20.23%. And then over and above in April and May, we have raised INR 340 crores. If I take that back into March 31, roughly, we are around 30% of capital adequacy, which will be sufficient to cater all the needs for this entire year (only 1 year), and we don’t see capital adequacy going below the current level for the full year in this equity base.

We have a text question from Pramod Jain from Purshottam Investofin Limited. When you

intend to raise next capital as you’re moving up the ladder in the world of financing, where you

will face interest war? Since you are still A rated, so your cost of funds will be much higher than

your peers. How will you be able to meet the competition?

Kishore Lodha: So next round of capital that we have said in our commentary earlier that for this full year, we are not looking at raising any equity. Probably in the mid of next year, we will look at another round of equity for the growth capital (Aug’24).

In your 30/6 post you hve mentioned that they have to dilute in 5/6 quarters which from the above dates and management commentary seems fair. Your thoughts ?

4 Likes

Q1FY24 Business updates

3 Likes

They need growth capital which is a fact , but why to take approval in this agm, they could have postponed it to next agm or called an egm in next two/three quarter . This just show desperation to raise capital, which would never be rewarded by market. Let your retained earning accumulate . Price wont move if you keep showing your despiration to dilute existing equity furthur

1 Like

While equity dilution by itself isn’t bad for existing shareholders in banks and NBFCs, it is definitely better if the dilution is done at a higher valuation. So hoping that their ROA and ROE improve as per guidance and there is some sort of rerating before the next round of dilution, irrespective of when that is.

2 Likes

Beg to differ with the view of Gaurav. The company has repeatedly clarified their business model and need for fund raising. I don’t think there is any desperation to obtain approval from AGM. Because we know that market is fickle. They can plan their fund raising better and can seek good valuation if time is in their hand. Their growth is linked to funds. So only watchable is business growth and EBITA. So far, their track record has been good regarding QIP pricing. Yes, for investors it is a long process and if you believe then stay invested in.

2 Likes

It is 25 percent of my portfolio, my point is not they didnot need money, my only point is desperation they show… If i were anh investor knowing soneone desperarly needs money , why not wait and dicatate price on my terms instead of their… Market are a poker game and you are showing your hand

1 Like

Hi. I am an ex banker and have good exposure to Financial stocks. I think diversification is the key. Ugro forms part of my portfolio also but less than 5%. Today there are well established banking models like Equitas,IDFC, Federal. Although sizing is important but Risk diversification is more important. All the best.

Many companies do take approval in AGMs for fund raise even if they may not have immediate requirements so as to avoid the hassle of conducting EGM later on.

Not having 5 percent in one company means a portfolio of 20 company, this for me to track is impossible , l also believe that money can only be made in few stocks and would buy the best story which i believe is there… Diversification is sonetine dis worsififstion in peter lynch term… I am not against ugro issuing share but issuing by showing desperation and diluting equity…what have been the return of original 4 investors in 5 yeara… Pathetic … This year qip was not even at 10 percent cagr premium to original share allotment (152)… Any pe or any investor would be happy … I dont think so …

3 Likes

Seen that way, then it should not just be seen as prioritizing Shareholder wealth but as also their own interest. They do need funding for the next phase of expansion which is through equity dilution. Considering their last effort for raising fund through equity dilution happened at not much of gain for their majority Share Holders, they would love to see the share price rising so as to ease their way to raise funds for Company’s Operational expansion.

Ugro recently released their Annual Report. A few observations from the report.

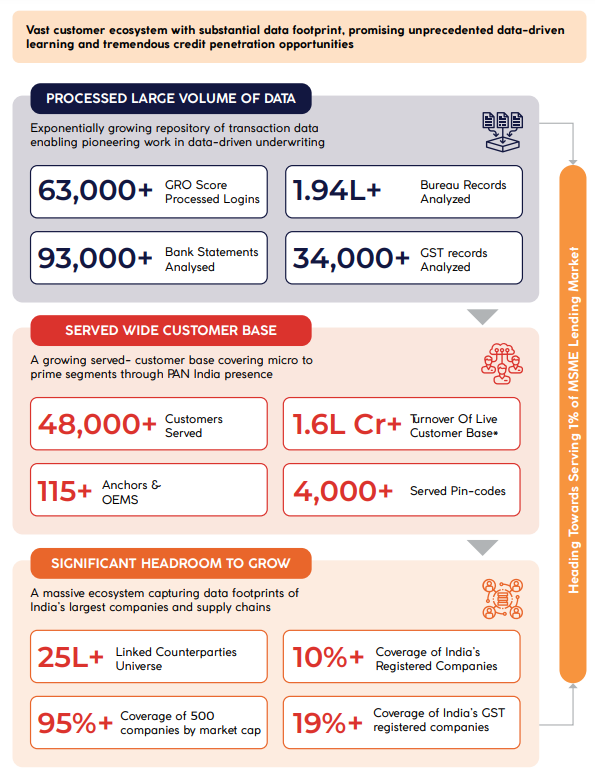

They’ve processed 34k GST records, 93k bank statements and 1.94L+ bureau records. These are still small numbers in the context of the overall MSME universe in India. As the amount of data crunched increases, the hope is their credit underwriting models become more robust.

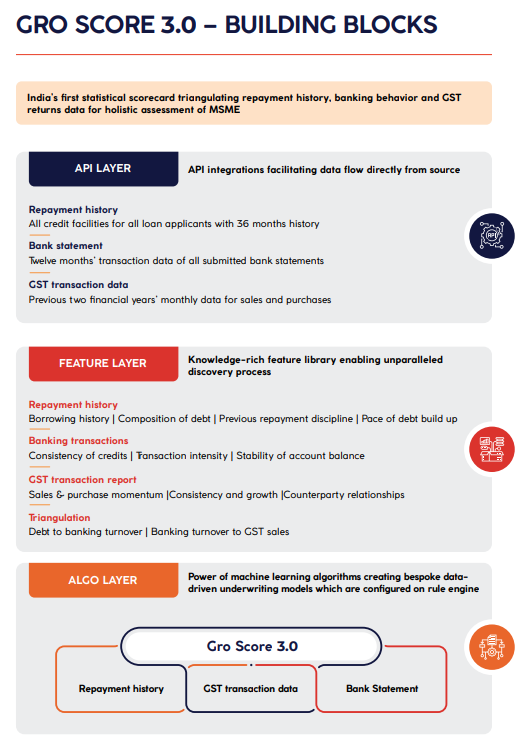

Some insights into the data and feature layers of their Gro Score 3.0 Algorithm. Data science domain experts on this forum may like to take a look at this snapshot and the one above and provide their comments if any.

Below are some aspects that need management questioning IMO.

As per the graphic, 59% of machinery finance is to the Hospitality sector. What kind of machines might hotels be buying?

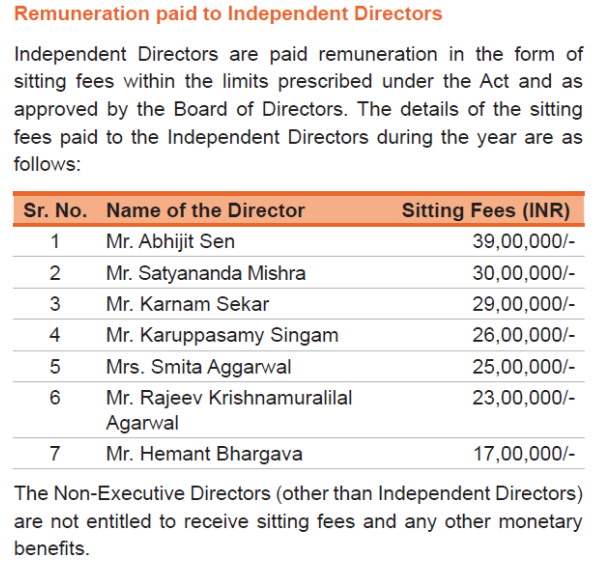

Sitting fees paid to the independent directors are very high compared to what is normally paid by other companies. The company has always maintained it wants to be a Board driven organization. Are these fees being paid to attract reputable independent directors who would otherwise not be interested in advising a small company like Ugro? Similar sums were paid last year as well.

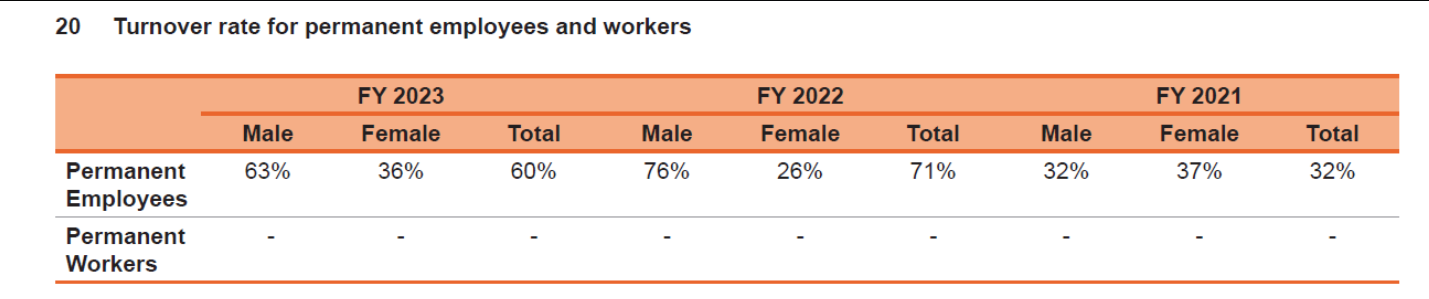

The employee turnover rate for FY23 was 60%, down from 71% in FY22. In FY21 the number was 30%. I assume most of this is front end sales force turnover. Does anybody know comparable turnover data for other relatively newly established NBFCs? We can benchmark this number.

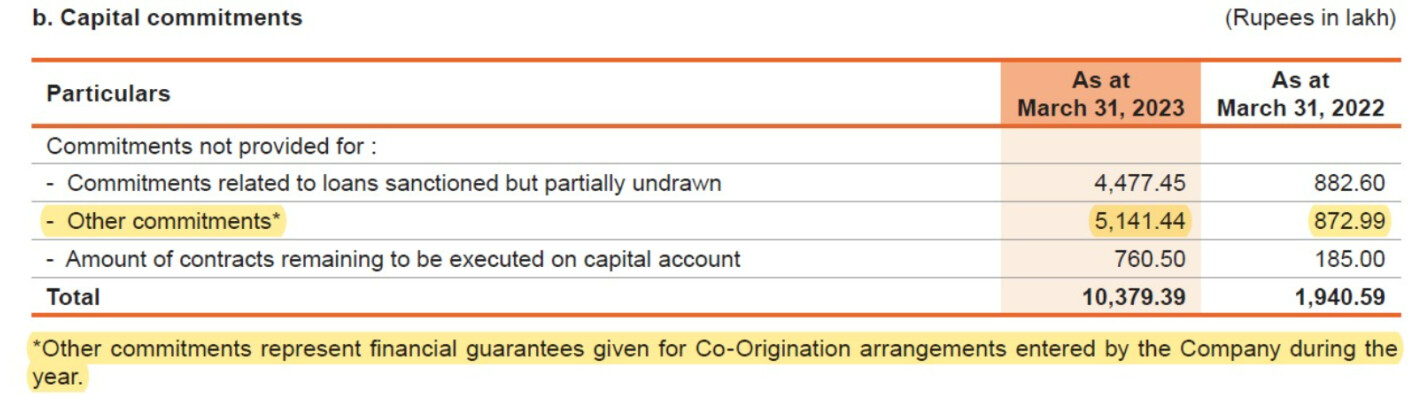

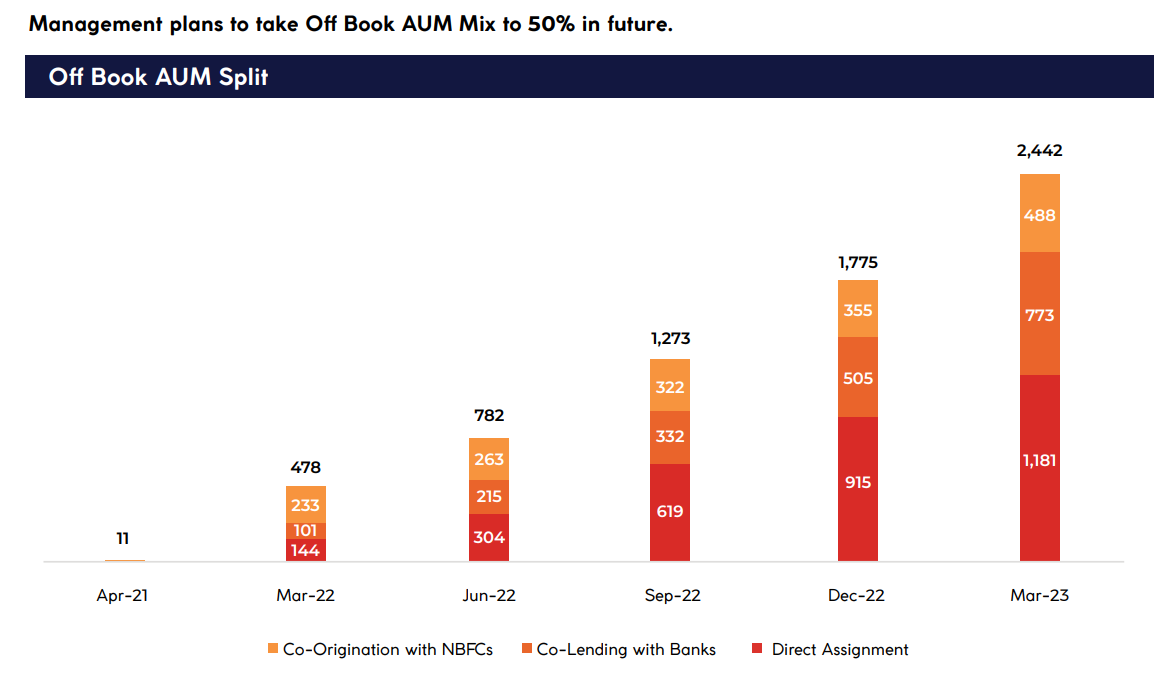

They have ~51Cr worth of contingent liabilities earmarked as financial guarantees given for co-origination arrangements. This means this 51Cr is FLDG guarantee provided by Ugro to its co-lending partners for its co-origination book (Co-lending doesn’t need any FLDG, co-origination does). They have a co-origination book worth 488Cr as of FY23, so the FLDG guarantee stands at ~10% of the co-originated amount. That’s a higher % than earlier understood (Earlier understanding was that this would not be more than 3-4% of co-originated amounts)

New CFO (Kishore Lodha) seems to be on 3x+ salary of the earlier CFO (Amit Gupta). MD’s salary has also increased by 58% YoY.

Disc: Invested and biased.

10 Likes

This an industry wide phenomena. High but hear that at large pvt banks also this is 30-40%.

Regarding fldg if you want to build 8000 off balance sheet loan book you may have to early satisfied bank, for which I think they have committed this amount showing their own skin in the game . This may encourage bank to co lend more and finally this would go back to standard 5 percent over time. This is what I think which can be 100 percent off :). Good question to ask in Agm/con call

2 Likes

Q1FY24 Nos

ddb799c0-f54b-4e04-b66f-a23c7410f186.pdf (2.1 MB)

c1f0fa2f-94b3-4941-8b0d-33c1329d68aa.pdf (783.1 KB)

1 Like

There seems to have been a slight increase in Gross and Net NPAs during this quarter. Is that cause for concern?

2 Likes

20 bps as concern is like asking a student why he got 98.9 percent and not 99 percent. They have said their model allow for 3% npa .

SBFC ipo is coming with worse return ratio and is valued at 2.6 bv , if it open at any premium (gmp is 40) p/bv would be near 4…In that case ugro would catch up or may be it would at 360/380 by august end… Lets hope for best openeing for SBFC ![]()

8 Likes

AGM recording link for those interested - https://www.youtube.com/watch?v=r2PcJt0-BM0&t=6683s

2 Likes