Till now the persistent selling by DBZ Cyprus was considered as an overhang. They sold out completely on 3rd May. But now I see that another shareholder Chhattisgarh Investments Limited which was recently allocated shares as part of the recent QIP, sold a big chunk on 4th May. This is strange. Maybe I am missing something (e.g. corresponding buy transaction by the same/related entity), anyone has any information which can possibly explain this?

11 Likes

Great set of numbers :

2 Likes

Ugro Capital Business Update Q4FY23:

Business Highlights:

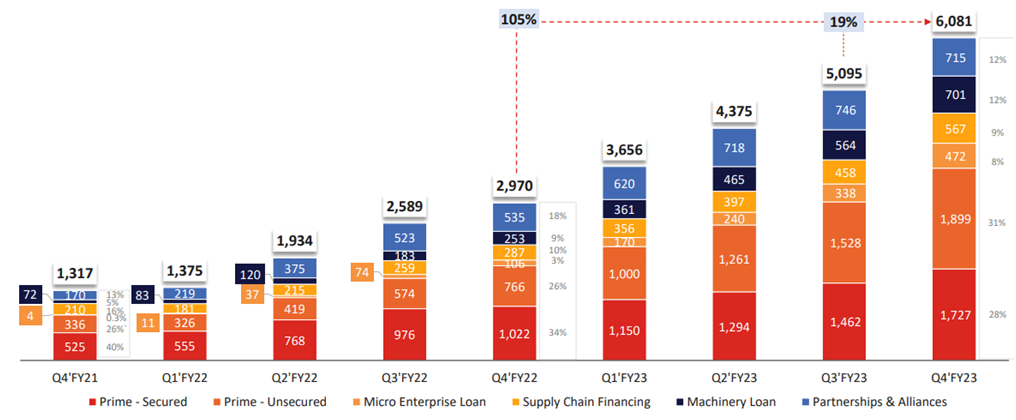

- UGRO Capital’s AUM reached INR 6,081 Cr, a 105% increase from the previous year.

- Collaborated with ten co-lending partners, over 65 lenders, 35 fin-techs, and 1,200 GRO partners.

- Provided data-backed customised finance solutions to over 46,000 MSMEs in India.

Future Growth and Opportunities:

- Intends to gain a 1% market share with 1 million small businesses as customers in the next three years.

- Recently launched the GRO X App, a digital solution for small businesses, offering collateral-free instant credit and financial management capabilities.

- The equity capital raise will strengthen UGRO’s capital position and balance sheet.

Financial Highlights

- UGRO Capital has shown impressive growth in its assets under management (AUM) with a significant increase of 105% YoY and 19% QoQ. This indicates a strong expansion of the company’s lending activities. The substantial growth in gross loans originated both annually and in Q4’FY23 further emphasises the company’s expansion efforts.

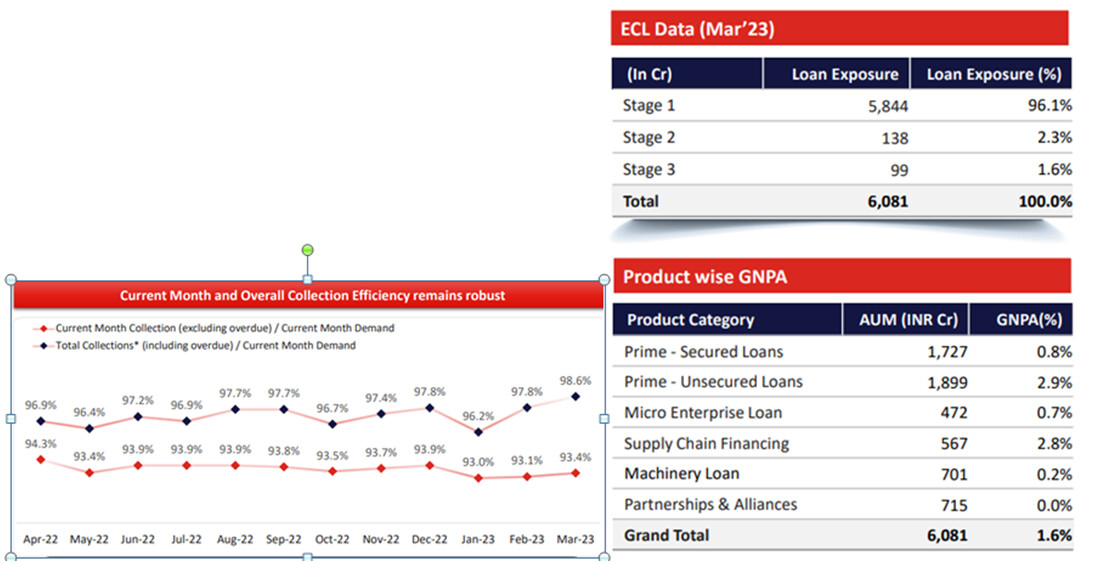

- UGRO Capital has maintained a relatively low level of gross non-performing assets (GNPA) and net non-performing assets (NNPA) with a ratio of 1.6% and 0.9%, respectively. This suggests effective risk management and a healthy loan portfolio.

- The company has witnessed a substantial increase in total income, with Q4’FY23 and FY23 showing impressive growth of 92% YoY, 15% QoQ, 119% YoY, and 123% YoY, respectively. This growth demonstrates the company’s ability to generate higher revenue from its lending activities.

- UGRO Capital has reported improved profitability, as indicated by the significant increase in net total income, reaching INR 126.8 Cr for Q4’FY23 (up 101% YoY and 17% QoQ) and INR 390.5 Cr for FY23 (up 123% YoY). The growth in pre-tax profit (PBT) further highlights the company’s enhanced profitability.

- UGRO Capital has maintained a diverse pool of lenders, with the lender count reaching 66 as of Mar’23. This indicates a robust liability position and access to funding sources. Additionally, the healthy capital position with a capital adequacy ratio (CRAR) of 20.23% provides a strong cushion for future lending activities.

- The company’s debt to equity ratio of 3.2x suggests a moderate level of leverage. It is important to monitor this ratio to ensure a sustainable capital structure and manage any associated risks.

Overall, UGRO Capital has demonstrated strong growth, improved profitability, and maintained a healthy portfolio quality. The company’s focus on expanding its lending activities and managing risks will be crucial for sustained success. Additionally, the diversified lender base and healthy capital position provide a favorable outlook for future growth and liquidity.

13 Likes

Update: I asked the question to the Management on why CIL sold its share so soon after QIP. Mr. Nath replied along the lines - ‘maybe because the share price rose too fast’ (not verbatim). I was disappointed with the response, I expected a more nuanced response. A QIP investor doesn’t invest hoping for a 10-15% bump in stock price they (generally) do it for the long term because they believe in the long-term growth story. Possible that Mr. Nath deemed the question (why a particular shareholder sold) unfit to be asked to the Management hence the curt response.

Thankfully someone asked a follow-up question stating the above and also added that the sell transaction by CIL seems to be a negotiated trade with a big investor. He asked if the Management is aware of who the new investor is. This time round Mr. Nath spent more time answering - (i) CIL has been a long-term investor, even prior to QIP (ii) yes the trade was a negotiated trade (iii) during the QIP the interest from investors was far more than the QIP amount on offer ( what I understood was - seems some interested investor(s) who didn’t get an allocation in QIP, entered into a negotiated deal with CIL).

Disc: Invested and notwithstanding the above, nothing I heard on the call made me doubt my bullish take on Ugro’s future prospects. Management seems genuine and works hard to create a strong institution. They also have substantial skin in the game via ESOPs.

18 Likes

Ugro capital Q4 FY23 earning call summary

In addition to inputs from @Akashdeep & @njain1983 , these are some of the points I noted from Ugro earning call.

- AUM growth continues to be high - 600 cr dispersal in March alone, only 30% acceptance rate. FY24 target of 6400 cr disposal.

- Opex spending to be slow down in coming quaters, target double digit RoE for FY24 and High teens RoE for FY25.

- post covid portfolio (With Gro 2.0) perform much better than restructured portfolio during covid.

- Supply chain financing is strtegically important on 2 reasons

- Enables short term lending, helps with ALM

- Open door for cross selling of many other products

- Co-lending with 2-3 private sector banks will happen next year.

I agree with @njain1983 regarding management integrity of Ugro Capital, looks like trustworthy and shareholder friendly management. But guidance’s are aggressive and biggest challenge will be to maintain asset quality.

8 Likes

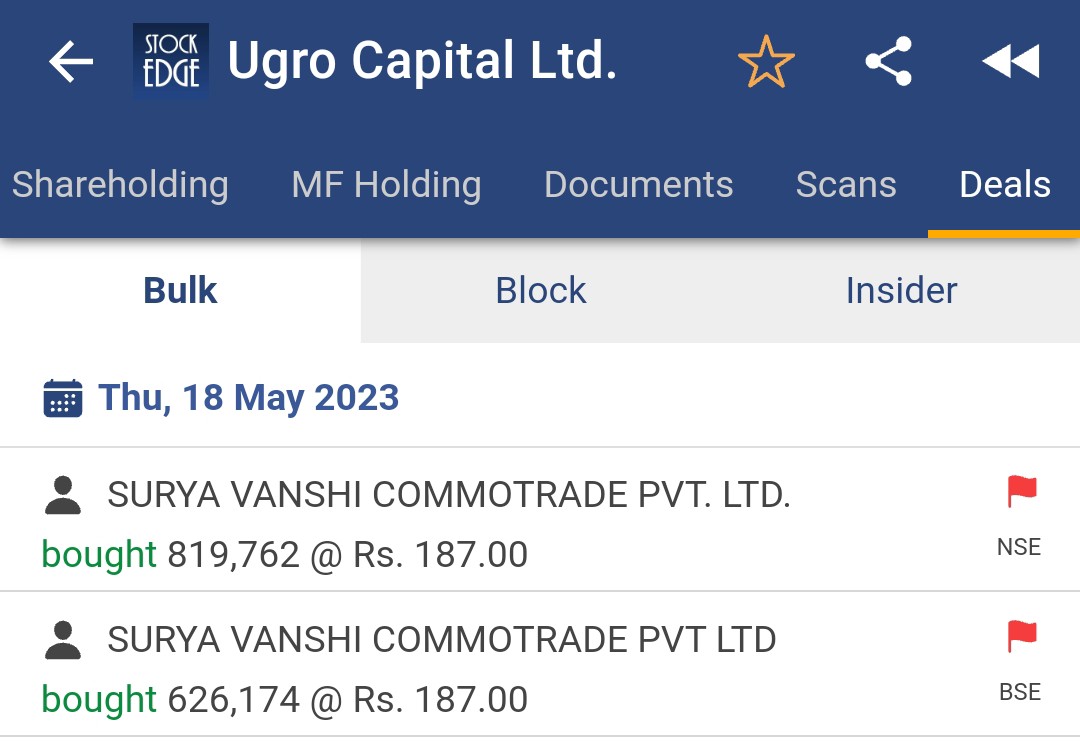

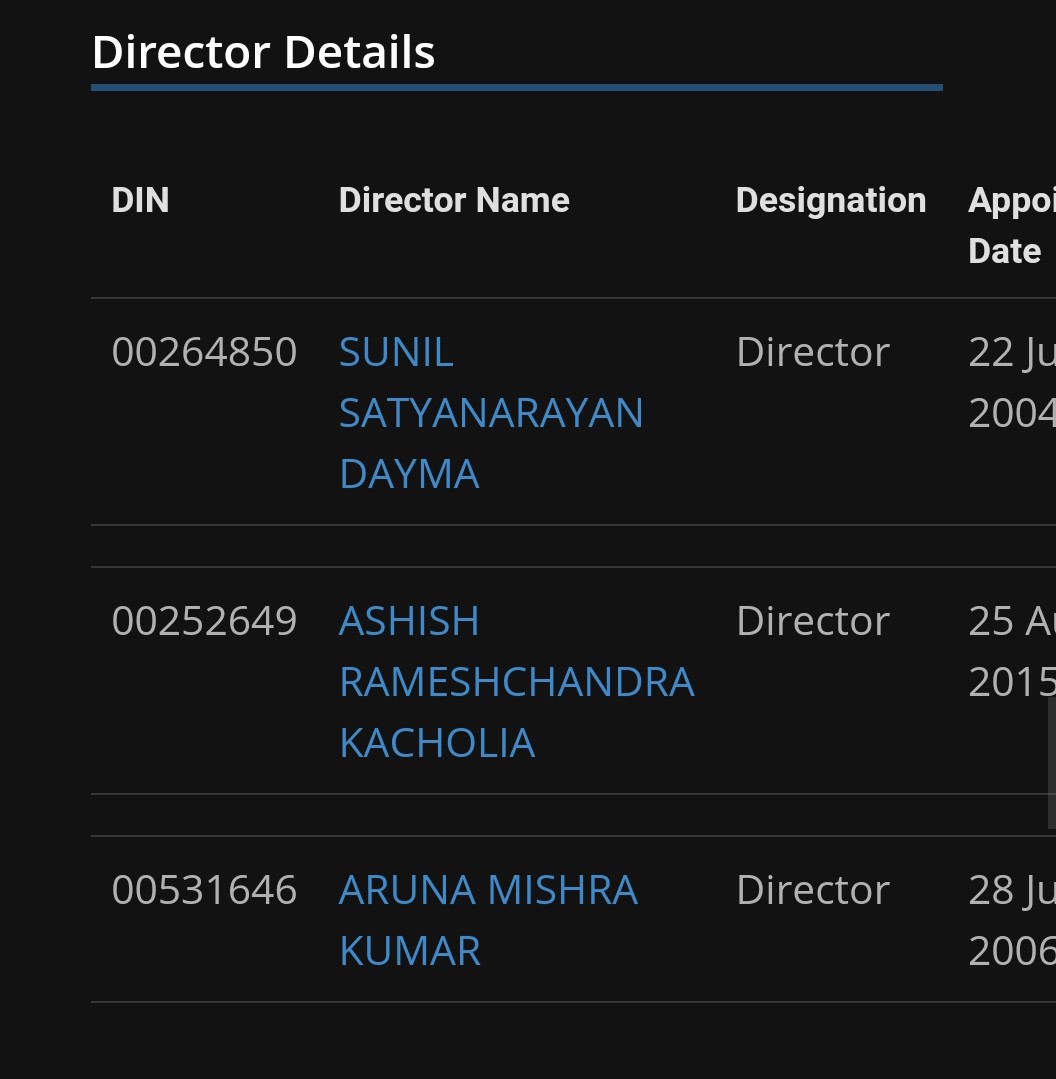

Ashish Kacholia has taken a stake in Ugro.

Ashish Kacholia is a director in this company

Source - SURYAVANSHI COMMOTRADE PVT LTD - Company, directors and contact details | Zauba Corp

I know it’s not relevant to the fundamentals of the company but still worth noting.

9 Likes

Great discussion on this thread everyone ![]()

![]() @Admantium Malkd Nirvana etc. really helped me appreciate the uniqueness of the business.

@Admantium Malkd Nirvana etc. really helped me appreciate the uniqueness of the business.

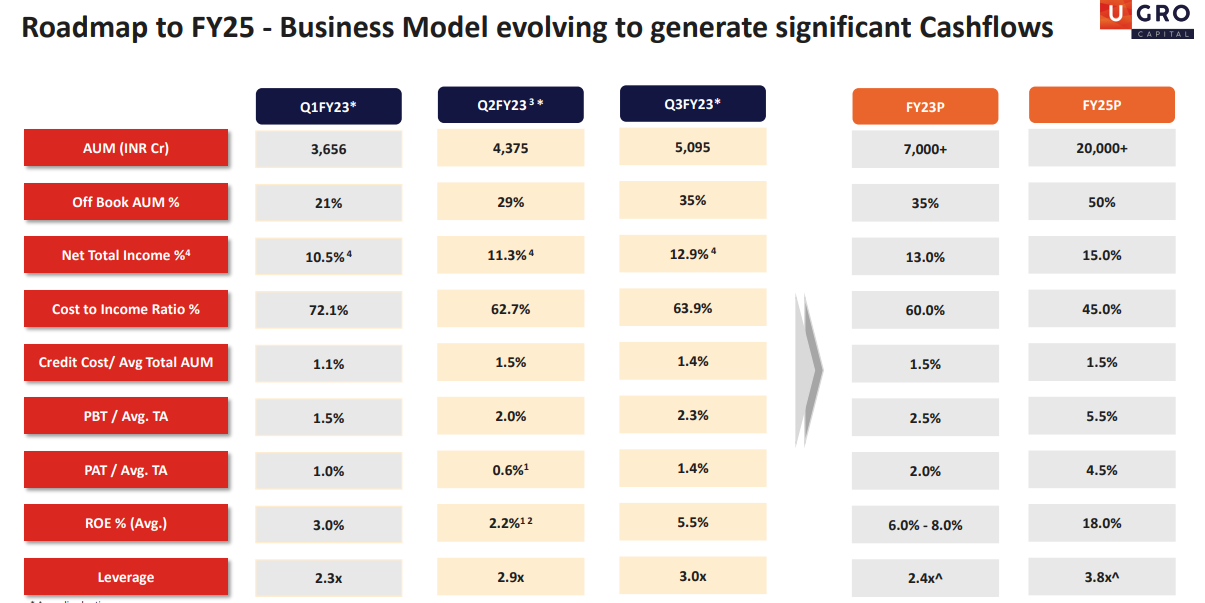

I wanted to dig deeper into the 2025 Guidance to better understand what it means.

First the 2025/2026 guidance -

AUM 20,000 Cr

RoA - 4%

Leverage 3.8x

RoE - 16% - 18%

What this means - Some back of the envelope calculations

2025 PAT = 800 Crores. [ 4% of 20,000]

For context - FY23 PAT = 60 crore. Even after adding back the deferred tax reversals.

2025 Book Value = 5,000 Crore (Approx) [20,000/3.8]

Current Book Value - 984 cr. + approx 350 cr additional capital recently raised. Lets say 1,400 cr.

Lets assume they raise another 1,000 crore in additional capital between now and 25/26. That’s 2400 cr, leaving another 2600 cr to be added by retained earnings (Addition to reserves) to reach the 5,000 crore figure. Divide 2,600 by 2 or 3 whatever, thats an addition of more than 800 cr to reserves every year till 2025/2026 (That’s more than the 2026 PAT guidance or half their current market cap every year ![]() ) That’s a very tall ask!

) That’s a very tall ask!

I know @nirvana_laha and a few others were worried about book value growth going forward as it hasn’t grown in the past because of Esop’s etc. Nirvana - Do you happen to have any projections of Book growth till FY26?

Given the above - What do you all think of the 2025 guidance? Achievable?

A more than 10x increase in PAT !!! And a steep growth in reserves ?

Is my math right? If so, I would love to get the management’s opinion on the same in the next call ![]()

Disc: Invested

3 Likes

According to the projections, AUM mix is 50% on-book portfolio and 50% off-book (made possible due to co-lending)

So in reality it’s AUM of 10,000 crs they have to fund at a target leverage of 3.8 i.e. 2,631 crs equity and rest of the AUM being funded by co-lending partner banks.

Given current book value of ~1,400 crs and future fund raise of say 600 crs and 600 crs retained earnings over the next 2-3 years they can reach equity of 2,600 crs

These are just projections and errors of ±15% is possible given the growth being talked about here.

8 Likes

What this means - Some back of the envelope calculations

2025 PAT = 800 Crores. [ 4% of 20,000]

For context - FY23 PAT = 60 crore. Even after adding back the deferred tax reversals.

Of the 20k Cr AUM in FY25, 50% will be off-book. So on book AUM is going to be likely closer to 10k Cr and balance sheet assets basis historical trends is likely to be 11.5-12kCr (On book AUM/Assets has trended at 86-88% in the last two years). Equity needed will be much lower - this is the beauty of an at-scale co-lending model.

Having said that I think Management will slow down on the 20k Cr guidance for FY25 and focus more on steering the ship with good cost metrics and underwriting quality and my projection is they will end up with 17-18k Cr AUM by 2025. I think most of the 2025 metrics are achievable, the most challenging one IMO will be their cost to income ratio of 45%. I will be very pleasantly surprised if they do hit that C-I target in FY25.

As far as further equity dilution is concerned, the CFO was on record this year saying there is unlikely to be any dilution in FY24. I expect another round of equity infusion of 500-600Cr in FY25, probably in Q1. The dilution at that point is likely to be much less than now because the price will hopefully be much higher.

To my mind, if Ugro can show that their underwriting is robust as their book matures or the cycle starts turning, sky is the limit.

Disclaimer: Invested and biased. Projections may be wrong, please do your own DD. Financial businesses carry inherent leverage risks plus new financial companies only prove themselves after seeing a full underwriting cycle.

17 Likes

Thanks for that. Makes more sense now, so they meant a total on B/S Asset book of 12,000 cr (10,000 + 20% of off balance sheet) split 50:50. ![]()

So working that math again based on the slide you added -

PAT of approx. 540 Cr by 2025 (4.5% of 12,000) current pat 60 cr. Little under a 10x.

Book Value of approx 3,100 cr. 1,400 current + 600 future raise per your expectation.

They would still need about a 1,100 cr of reserve addition in 2 years. Maybe a little difficult to acheive.

In any case, if they come even 70% close to reaching these numbers it will be nothing short of amazing given that they’re currently trading at 0.5 guided 2025 book value & 3x 2025 earnings.

I agree with you on the asset quality! If they can keep their credit costs under control, this could be one heck of a company ![]()

1 Like

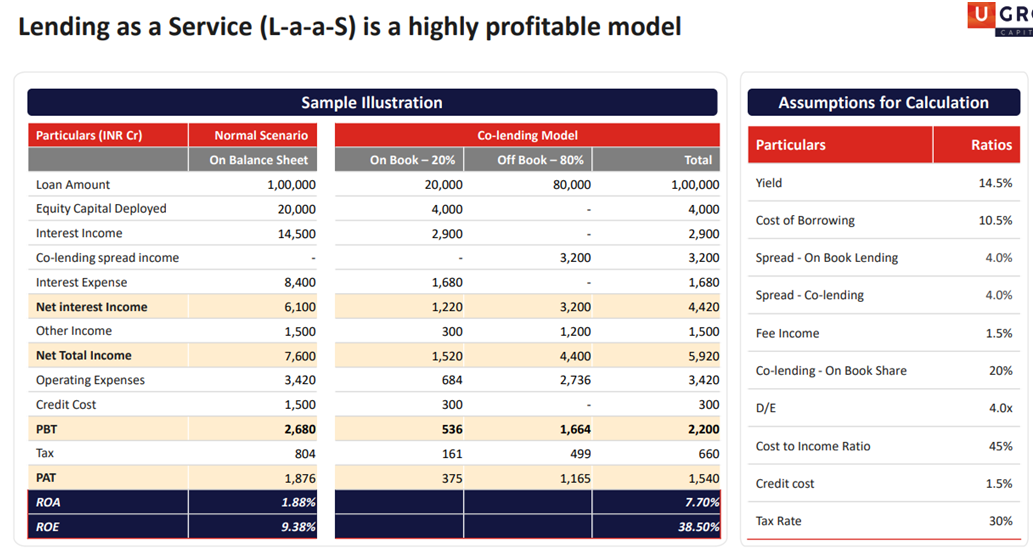

Ugro has established a co lending business model. The off balance sheet book (mainly with PSBs) earns spread without credit risk (except FLDG with NBFCs) and pushes the ROE magnificently.

There are two data points I want to discuss.

Gross NPA is 1.6%

Q4 AUM: 6081cr

Q3 AUM: 5095cr

Disbursement made in Q4 cannot be NPA (requires at least 90 days due). So, for me GNPA is at least 1.9% (still good number).

For a very fast growing company AUM is increasing rapidly and GNPA may look optically low. The day AUM starts slowing down, real GNPA number will be reflected.

With a very little history, it’s very difficult to judge the underwriting quality.

Collection efficiency:

Their net collection efficiency (excluding overdue) is 93.4% for March.

It means 6.2% book fall into SMA bucket. This is disturbing for me.

But their gross collection efficiency (including overdue) is 98.6% for March. This number on a growing book is extremely good probably because of their in house collection team & litigation team.

The NPA is low because of their ability to recover.

6.6% account does not pay EMI. Out of which 2.7% pay within 60 days.

2.3% pays within 60-90 days.

Finally GNPA is 1.6%.

I am positively surprised by their recovery capability & equally worried whether they will be able to do the same in a downcycle.

8 Likes

A well written article on the various kinds of risks a msmse entails.

best

divyansh

3 Likes

Another issue which haunts the MSME more than others is their inability to manage working capital and its financing for various reasons.

sharing a paragraph which i was reading for more details

“” * A similar issue is the use of working capital. Despite the increase in turnover, MSMEs still end up defaulting on their payment obligation. Why so? In the pursuit of growing their business, they often end up diverting the working capital to buy fixed assets without tying up long term funds. They fail to understand the importance of liquidity and this also hurts their credit rating. MSMEs, therefore, must be given some “Basic Financial Education” to make them understand the nuance of the finances.

- At the same time, RBI’s Asset Classification norms are applicable mutatis-mutandis across all segments i.e Large Corporates, Mid-Corporates, and MSMEs. However, it is unfair to expect the same kind of financial discipline from SMEs vis-a-vis Large/ Medium Corporates. It is a well-known fact that SMEs largely depend on their larger counterparts for sales of goods and timely realisations of their dues. Therefore, they generally end up providing credit period against their sales to these entities in the range of 60 to 120 days. On the other hand, they do not easily get the raw material on credit. Overall, the cash cycle for the MSMEs works out to be anything between 3 and 6 months. Therefore, they find it extremely difficult to manage their working capital requirement and thus end up delaying payment towards their commitments. “”"

its from open source and the writer is G.K Kansal

Head- Credit & Risks, Power2SME

Ugro has also been mentioning about rise in npa is there working capital loans if i am not wrong. if other can throw light on how this might affect the business in long term.

best

divyansh

3 Likes

2 Likes

This investment is from a couple of months back I suppose.

2 Likes

The forward looking statements from the 17 minute mark onwards are pretty promising.

1 Like

Please delete the response if it is irrelevant.

How would look into such interviews marketed by the company itself? This is not a concall or a private analyst interview or Investor Presentation but more so like an advertisement for retail shareholders because I don’t think any of the users of Ugro’s services will be watching this interview on ET NOW.

Does it impact the stock price with more retail investors entering? Will you interpret as Management trying to advertise to retailers?

Or am I overthinking?

5 Likes

It is clearly a promotional segment, so I would take it as such. Mr. Nath has never shied away from talking about Ugro being undervalued. I am not a fan of managements talking about price but for a fast growing company like Ugro which is guzzling capital, price is a very important determinant of performance. Higher the price, lower the dilution and better the terms of growth for shareholders. So I can sympathize with his yearning for higher multiples. Equally, I would understand people being skeptical about a management that focuses on stock price, I have been the same with other company managements, often. Even so, there was no “overt selling” of Ugro the stock as far as I could see.

Keeping aside the promotional nature of the segment, a few key snippets from the business POV that I took away:

-

His constant re-iteration that the the themes of - 1. MSME sector (with around 20-25Cr voters) 2. Cash flow based underwriting and 3. Co-lending as a model are all going to find favour with Government and RBI regulations because they are collectively in the interests of higher credit penetration and growth for the country

-

He gave some indications about expected disbursal rates in FY24, FY25 and FY26 (I don’t think these can be treated as guidance at all, but might help us in understanding Ugro’s internal directional thoughts). Basis that it would seem to be that FY exit AUMs for Ugro could look something like this:

FY24: 10k Cr

FY25: 17k Cr

FY26: 26k Cr

I have a suspicion that they may be able to grow faster in FY24 and FY25, maybe 11k Cr and 18k Cr of AUM respectively. If co-lending continues to work well, then there is a chance that co-lending as a % of AUM may even exceed 50% (Already at 40%). That would further strengthen ROEs.

This is clearly a business which has figured out the growth side of the equation via

- large capital at its disposal (large equity base, access to PSB funds via co-lending and fast software based underwriting ) and

- A large runway (huge under-penetration in MSME lending)

What it needs to establish is the quality and robustness of its underwriting across a cycle. If it is able to establish that, then this business has the potential to become one of the most exciting lending businesses in India. We should all be watching their NPA nos. and collection data very closely.

A couple of data points I’d like the company to start disclosing from next Q:

- ALM details

- GroX traction: Quarterly disbursement and customer counts (GroX is another very exciting and high potential product which moves the needle on the ground for MSMEs)

Disc: Invested and biased. Lending businesses are leveraged and thus quite risky. Please do your due diligence and maybe even err on the side of caution while evaluating lending businesses.

31 Likes

They have to dilute equity in next 5/6 quaters and if they have to pick 600 cr for d/e ratio they aspire , they would ideally like mcap to be north of 6000/7000 cr, so that dilution is less tham 10 percent… They Have no choice but to work on capital market for this… They have to increase price 3/4 times in next 4/5 quarters

6 Likes

I think the real issue here is why aren’t institutions coming in and buying this story in a big way?

Retail money won’t take them far.

Maybe this is the year for them to prove and then they’d look to fund raise from better and more credible institutional investors.