Triveni Turbines might just have passed an inflection point.

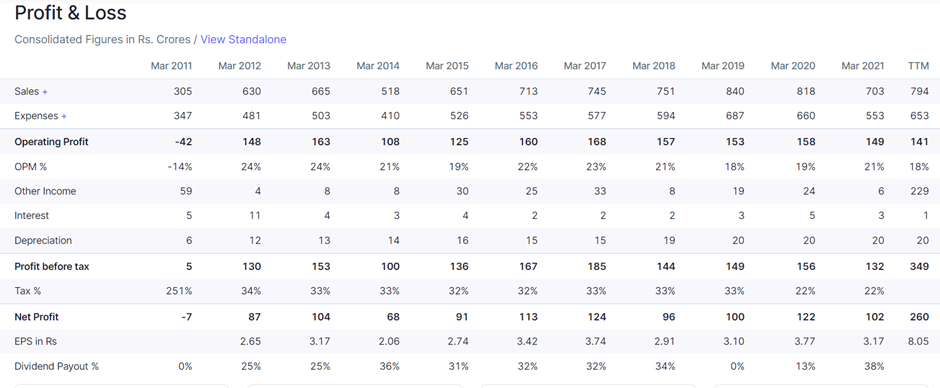

To be sure, the numbers for the past 10 years have been nothing home to write about. Sales grew from Rs.300 crore to Rs.800 crore in 10 years, while profit growth has been tepid too.

But things might just be changing.

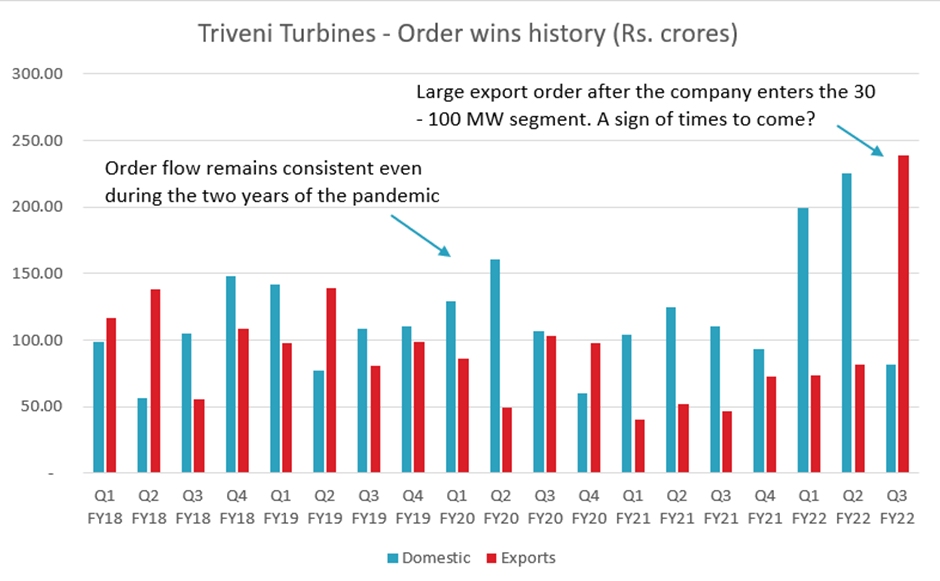

The dispute with GE has been resolved on what looks like favorable terms for Triveni (click here). The stake held by GE & Baker Hughes has been bought back by Triveni for just Rs. 8 crores, making the 50:50 JV a 100% WOS. In addition, the company has received Rs.208 crores as settlement compensation. Triveni Turbines is now free to go to the market on its own and target the lucrative 30 – 100 MW segment. This increases the TAM for the company substantially. Icing on the cake is that in the very first quarter after this, company announced they have received 3 large orders from the export market in the 30 -100 MW.

Already, the business has a natural tailwind from the ESG waive sweeping the world. Besides thermal, steam turbines are used in all sorts of renewable energy plants such as those from biomass pellets, sugarcane bagasse, liquid biofuels like ethanol, gaseous fuels like biogas and landfill gas, solid waste processing plants and so on (but not solar). Steam turbines are also used in Waste Heat Recovery Systems (WHRS) used commonly in high energy consuming industries such as Steel, Cement, Petroleum etc.

But besides this, there are many other things I liked about Triveni Turbines.

The company has an asset light business model, despite being in the capital goods / infrastructure sector. The Gross Block which stands at Rs.352 crores stood at Rs.164 crore a decade ago, indicating minimal investment in fixed assets. Essentially, the company focuses on manufacture of a few critical IP-sensitive components and subcontracts the rest. And then, testing and final assembly is performed in-house to ensure quality of the final product.

The company works on negative working capital, as it gets advances from customers for the projects it executes. The Balance Sheet is debt free, has more than Rs.700 crore in surplus cash. It did a buyback in 2019. Margins in this business are high, as the product is tailored to customer requirements. No competitor can mass-produce a turbine on an assembly line and flood the market. In the domestic market, Triveni has a dominant market share of more than 50%.

Cash Flow from Operations have been consistently ahead of PAT for the last 3 years, understating the reported profitability of the company. P/E therefore looks elevated but actual valuation is lower. Going ahead, as the order book grows and bigger order come in (30 – 100 MW) cash flows should improve even further.

Around 25 – 30 % of the revenues come from the sale of spares, servicing and Operation & Maintenance activities. These are less volatile and more recurring in nature, they also carry higher margins. As the installed base of Triveni’s turbines grow, these revenues can only go up. They provide a recurring annuity type of cash flows for the company at very high margins.

The order flow remained consistent even during the two years of the pandemic with minimal declines. Meanwhile, the recent bump up in export orders may be a sign of times to come.

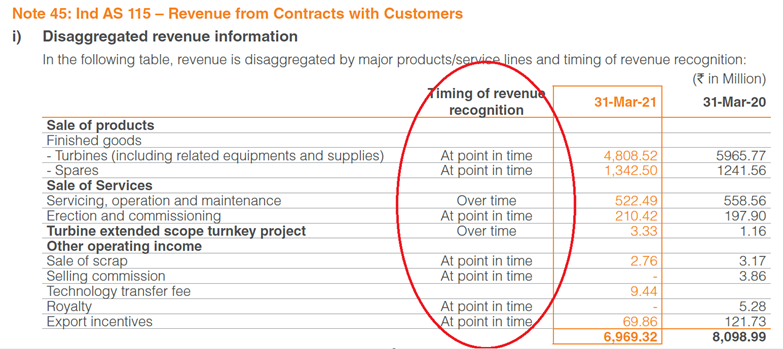

Interestingly, even the accounting policy seems conservative. Revenue recognition is NOT on a percentage completion method for majority of revenue. Revenue recognition happens when the control of goods is passed on to the customer. This is better than the Percentage Completion method, used commonly in capital goods / infra industries.

As can be seen above, less than 1/10th of the revenues came from the Percentage Completion Method. The corresponding figure for Siemens was 38% and Thermax was 59% for the financial year 2021.

Overall, there are many things going for Triveni Turbines. With the capex cycle beginning to take off, JV dispute out of the way and export markets warming up, the future may be very different from the past.

Counter points and anti-thesis is invited.

(Disc: Invested)