1. History of the Company

Triveni Turbine Limited (TTL) traces its corporate lineage back to Triveni Engineering & Industries Limited (TEIL). TTL was originally incorporated as ‘Triveni Sri Limited’ on June 27, 1995. The company’s transformation from a traditional turbine supplier into a comprehensive industrial heat and power solutions provider began earnestly in 1979. A significant milestone occurred in 2010 when the steam turbine business was completely demerged from TEIL into a separate entity, officially listed as Triveni Turbine Limited.

Over the decades, TTL has grown into a globally trusted energy innovator. In 2008, the company formed a joint venture with General Electric (GE), known as GE Triveni Limited (now Triveni Energy Solutions Limited, a wholly-owned subsidiary), allowing it to manufacture and market steam turbines in the >30 MW to 100 MW range. In September 2022, TEIL fully divested its remaining 21.85% equity stake in TTL, establishing the company’s complete independence with a diverse shareholder base of institutional and retail investors.

In recent years, the company expanded its global footprint rapidly:

-

2014: Established its UK subsidiary, Triveni Turbines Europe Pvt. Ltd. (TTE).

-

2022: Acquired a 70% equity stake in TSE Engineering Pty. Limited (TSE) in South Africa, which was later converted into full 100% control, creating a strategic hub for the SADC region.

-

FY 2025: Incorporated Triveni Turbines Americas Inc., setting up a local office and repair facility in Houston, Texas, USA to tap into the lucrative American refurbishment and API (American Petroleum Institute) turbine markets.

https://youtu.be/TSFYSXD8FD8

2. Manufacturing Facilities

Triveni Turbine boasts a robust, asset-light, and highly efficient manufacturing ecosystem. Its manufacturing prowess is concentrated in two state-of-the-art facilities in Bengaluru, Karnataka, India:

-

Peenya Facility: Established in 1973-74, this is the company’s historical manufacturing hub equipped with cutting-edge machinery.

-

Sompura Facility: Commissioned as the second state-of-the-art facility, it underwent a major capacity expansion in 2022-23 with additional assembly, testing, and heavy material handling capabilities.

Both the Peenya and Sompura facilities are designed as green factories. They are certified as Indian Green Building Council (IGBC) Platinum-rated buildings, featuring Zero Liquid Discharge (ZLD) systems, over 50% green space coverage, and a 1,300 kW rooftop solar plant that meets the majority of their energy requirements.

Internationally, TTL operates dedicated turbine assembly and repair facilities in Johannesburg (South Africa) and Houston (Texas, USA) to provide localized aftermarket support and rapid response to global clients.

3. Business Segments, Products, and Revenue Contribution

Triveni Turbine Limited operates primarily in a single broad business segment—power generating equipment and solutions—but strategically divides its operations into two highly distinct revenue streams: the Product segment and the Aftermarket segment.

A. Product Segment

The Product segment is the foundation of TTL’s business, focusing on the design, engineering, and manufacturing of industrial steam turbines up to 100 MW. This segment has evolved from traditional industrial heat and power to highly complex, advanced turbomachinery.

Key Product Lines:

-

Condensing & Backpressure Steam Turbines (up to 100 MW): These are the workhorse turbines used across over 20 industries (including sugar, cement, steel, and textiles). They come in various configurations, including straight, bleed, uncontrolled/controlled extraction, and injection turbines.

-

API-Compliant Turbines: A major breakthrough area for TTL, these turbines are built to meet rigorous American Petroleum Institute standards—API 611 (General Purpose) and API 612 (Special Purpose). They are critical for drive and power generation applications in petroleum refineries, petrochemical plants, and fertilizer units.

-

Thermal Renewable Turbines: TTL has strategically pivoted toward sustainability, manufacturing turbines for Biomass, Waste-to-Energy (WtE), Waste Heat Recovery (WHR), and Geothermal applications. This shift is highly lucrative, as thermal renewable fuels now account for roughly 73% of the global sub-100 MW steam turbine market.

-

Next-Generation Energy Transition Products*: To future-proof the business, TTL is developing CO2-based energy storage systems (including a landmark 160 MWh project for NTPC), supercritical/subcritical CO2 turbines, gas expanders, and CO2-based heat pumps and chillers.

Product Revenue Contribution (Q3 FY26):

-

The Product segment saw robust demand, recording a turnover of ₹486.0 crores during Q3 FY26.

-

This represented a massive 49% year-on-year (YoY) increase compared to ₹326.3 crores in Q3 FY25, driving the bulk of the company’s top-line growth.

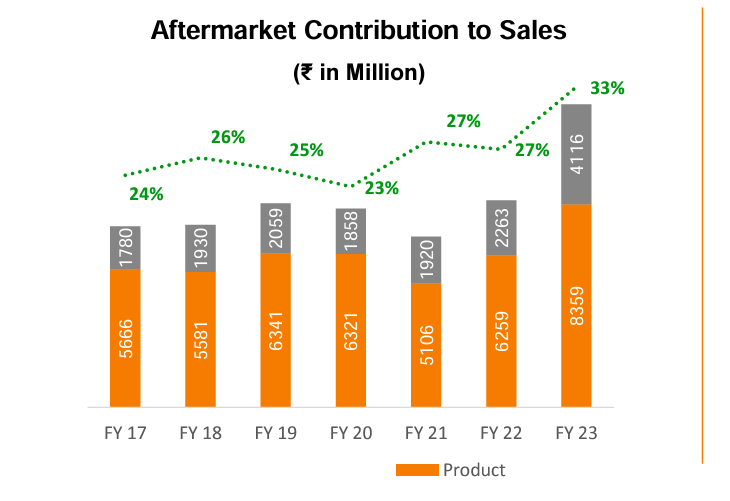

B. Aftermarket Segment (Triveni REFURB)

The Aftermarket segment provides higher margins, predictable cash flows, and acts as a buffer against capital goods cyclicality. TTL’s aftermarket capabilities extend far beyond its own manufactured turbines.

https://youtu.be/yHPBW50ek4g

Key Service Lines:

-

Spares & Services: TTL provides lifecycle support, annual maintenance contracts (AMCs), health checks, remote monitoring, and genuine spare parts for its own global installed base of over 6,000 turbines.

-

Triveni REFURB (Any Make, Any Age): This division focuses on the refurbishment, reverse engineering, and efficiency upgrading of rotating equipment manufactured by other OEMs. TTL services utility steam turbines up to 950 MW, gas turbines, turbopumps, compressors, blowers, and even nuclear turbines (>600 MW).

Aftermarket Revenue Contribution (Q3 FY26):

-

Aftermarket turnover stood at ₹138.0 crores in Q3 FY26.

-

This represented a 22% YoY decline from ₹177.1 crores in Q3 FY25. Management noted that this drop was largely due to the deferment of delivery for a large refurbishment order to coming quarters, rather than a structural loss in demand.

-

Consequently, the Aftermarket segment’s contribution to total turnover dropped to 22% in Q3 FY26, down significantly from 35% in Q3 FY25. Because this segment commands higher margins, the drop in its revenue share caused a mild contraction in the company’s overall EBITDA margins (from 26.1% to 24.6%) during the quarter.

C. Geographical Revenue Contribution

TTL’s strategic focus on internationalization is heavily reflected in its revenue mix:

-

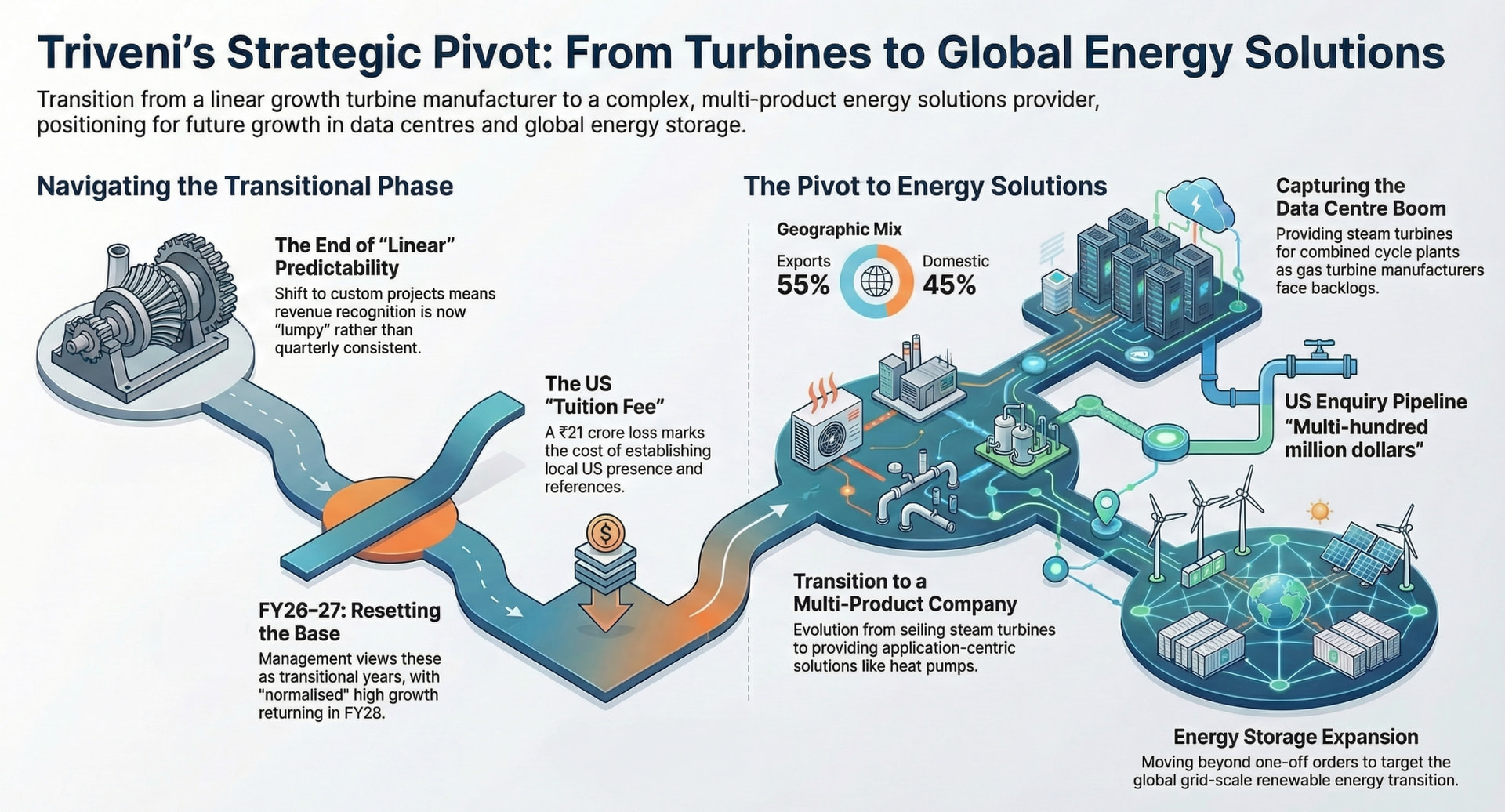

Exports: Export sales were the primary engine of growth in Q3 FY26, surging by 54% YoY to ₹384.5 crores (up from ₹249.0 crores in Q3 FY25). As a result, exports contributed 62% of total sales in Q3 FY26, a sharp increase from 49% in the previous year.

-

Domestic: Domestic sales experienced a mild contraction, declining by 6% YoY to ₹239.5 crores.

4. Promoters & Management Background and Shareholding:

The Sawhney family is the primary promoter group of Triveni Turbine Limited, holding approximately 56% of the company’s equity.

-

Mr. Dhruv M. Sawhney (Chairman & Managing Director): A seasoned industrialist and veteran business leader, he is the Chairman of the broader Triveni Group. While not a pure-play “technocrat” (an engineer by strict definition), he has immense domain experience spanning over four decades in the capital goods and sugar manufacturing industries.

-

Mr. Nikhil Sawhney (Vice Chairman & Managing Director): He has a background in investment banking and consumer goods in the UK and USA prior to joining the family business in 1999. Under his leadership, TTL has aggressively expanded into international markets and R&D-driven product innovations.

-

Technological Backbone: While the top promoters have business, finance, and industrial management backgrounds, the company’s operational backbone is fiercely technocratic. TTL employs over 1,000 people, with a massive focus on R&D. Over 15% of its workforce is dedicated purely to R&D and engineering.

Remuneration, Pledging & Holdings:

-

There is no significant promoter pledging reported.

-

The promoters hold a tight grip on operations, ensuring continuity. Historically, analysts have noted that promoter remuneration across the group has occasionally been on the higher side of industry norms (e.g., 8-10% of net profits), but this is generally approved by shareholders without contest given the exceptional wealth creation and operational outperformance.

Non-promoter shareholding is characterized by strong institutional backing, which accounts for the vast majority of the free float. With the promoter group (the Sawhney family) holding a steady 55.84%, and out of the remaining 44.16%, FIIs and DIIs control nearly 37% of the total outstanding equity

Shareholding Trends (as of December 2025)

There has been a distinct rotational trend in the institutional holding structure over the past year. FIIs have gradually pared down their stakes, dropping from roughly 28.34% in December 2024 to 22.38% by the end of December 2025. Conversely, DIIs have actively absorbed this supply, increasing their total position from 10.92% to 14.60% over the same period. Retail and non-institutional public shareholders account for a relatively small fraction of the float, sitting at approximately 7.18%.

Notable Foreign Institutional Investors (FIIs / FPIs)

· Nalanda India : One of the most notable and consistent long-term investors in Triveni Turbine, currently holding approx. 8% stake.

· First Sentier Investors (Stewart Investors Indian Subcontinent All Cap Fund): Holds approximately 1.49% of the equity.

· Government of Singapore: A prominent sovereign wealth fund holding a 1.10% stake in the company.

Notable Domestic Institutional Investors (DIIs / Mutual Funds)

· SBI Small Cap Fund: A major domestic shareholder, maintaining a 3.13% stake.

· ICICI Prudential Energy Opportunities Fund: Holds 2.78%, aligning logically with the company’s strategic pivot toward energy storage and thermal renewables.

· Nippon India Multi Cap Fund: Holds a 1.34% position.

· Edelweiss Small Cap Fund: Holds 1.03% of the company’s shares.

5. ESOP / ESPS and Effect on Profitability

Triveni Turbine Limited (TTL) aggressively utilizes Employee Stock Option Plans (ESOPs) as a strategic lever to retain elite engineering talent, align key management interests with long-term shareholder value creation, and minimize the attrition of specialized intellectual capital essential for its R&D division.

The ESOP 2023 Plan and Equity Dilution:

The company is currently administering the “Triveni Turbine Limited - Employee Stock Unit Plan 2023”. As per the latest exchange filings, employees are actively exercising their vested options, leading to periodic, small-batch equity allotments.

· Recent Allotments: On February 17, 2026, the company allotted 1,572 equity shares to eligible employees at a nominal exercise price of Re. 1 per share. This follows a steady cadence of recent vesting, including the allotment of 4,187 shares in January 2026 and 6,000 shares in November 2025.

· Dilution Impact: Consequent to the February 2026 allotment, the total issued and paid-up share capital of the company expanded marginally to ₹31.78 crores (comprising 31,78,92,029 equity shares of Re. 1 each). Because these allotments are executed in small, staggered tranches, the actual equity dilution for existing public shareholders is mathematically negligible, while the operational retention benefits remain substantial.

Effect on Profitability:

· Non-Cash ESOP Amortization: The ESOPs granted under the 2023 Plan are accounted for at fair value. The difference between the market price and the Re. 1 exercise price is treated as an employee compensation expense and amortized over the vesting period. While this acts as a non-cash expense that mildly depresses reported operating margins (EBITDA), it does not impact the company’s robust free cash flow generation.

7. Quality of Earnings, Margins, and Return Ratios

Triveni Turbine Limited (TTL) operates with a financial profile characteristic of a highly efficient, asset-light capital goods manufacturer. Its financial metrics reflect immense pricing power, low capital intensity, and superior operational execution.

A. Quality of Earnings: Core vs. Non-Core

The “Quality of Earnings” refers to how much of a company’s profit is derived from its recurring, core operations rather than one-off events, accounting adjustments, or passive “other income.” For TTL, the quality of earnings is exceptionally high.

-

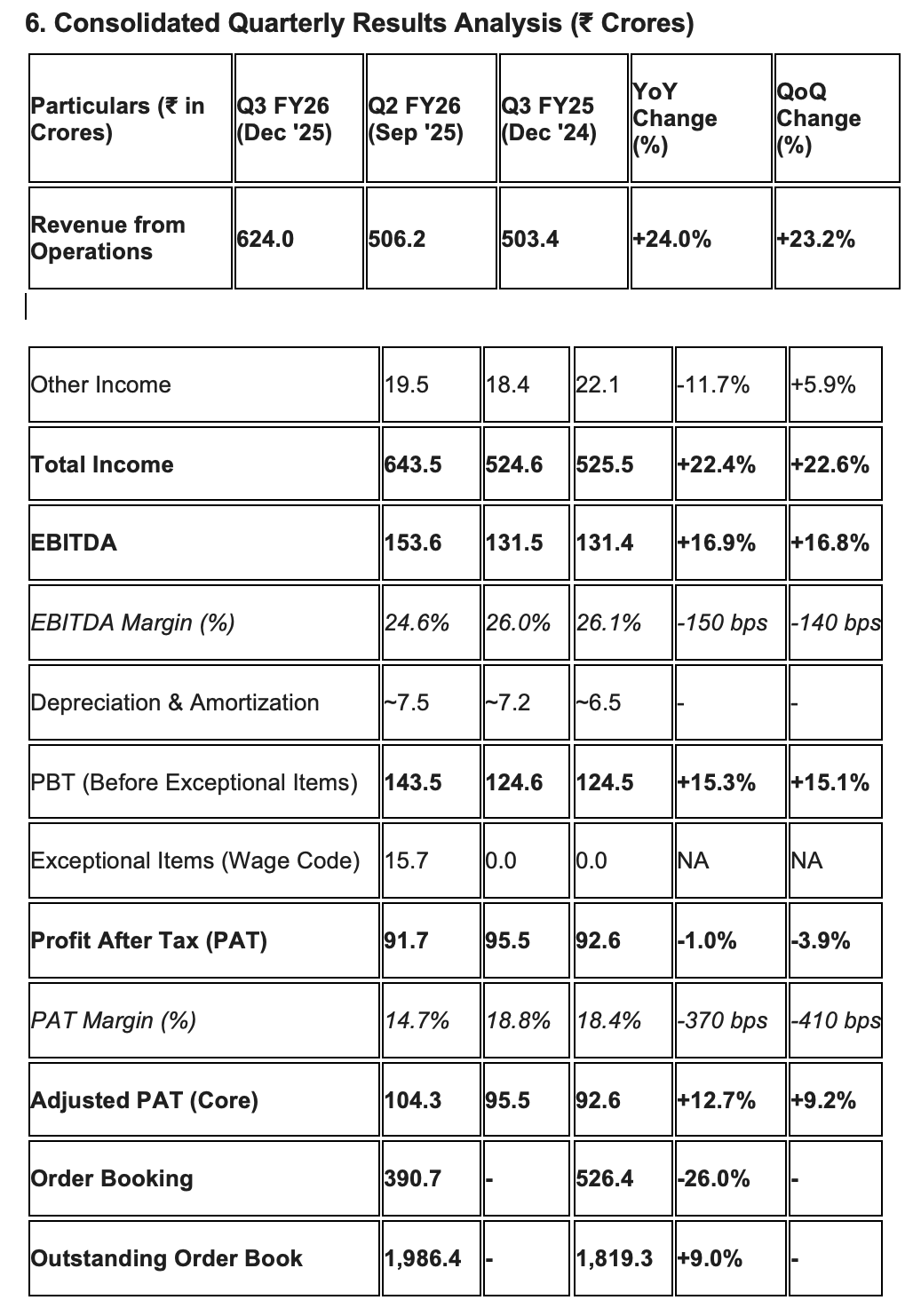

Core Revenue Dominance: In Q3 FY26, the company posted its highest-ever quarterly revenue of ₹624.0 crores, a 24.0% YoY increase. This growth was purely organic and driven by core operations—specifically a massive 54% YoY surge in export sales.

-

Stable Other Income: “Other Income” (which typically includes interest on cash balances or forex gains) stood at just ₹19.5 crores in Q3 FY26, down slightly from ₹22.1 crores in Q3 FY25. This shows that top-line and bottom-line growth is not being artificially inflated by treasury operations.

-

Operating Margins (EBITDA) Decoding: The company reported an EBITDA of ₹153.6 crores in Q3 FY26 (up 16.9% YoY). However, the EBITDA margin contracted mildly by 150 basis points from 26.1% to 24.6%.

- Explanation: This contraction is not due to structural pricing pressure or inflation. It is entirely a product of the “revenue mix.” The highly lucrative Aftermarket segment (which commands superior margins) saw its contribution to total sales drop to 22% in Q3 FY26, compared to 35% in Q3 FY25, mainly due to the deferment of a large refurbishment delivery to coming quarters.

-

Exceptional Items Impacting PAT: The reported Profit After Tax (PAT) for Q3 FY26 was ₹91.7 crores (down 1% YoY). However, the core earnings quality remains intact. This optical stagnation was caused by a sudden, non-recurring exceptional charge of ₹15.7 crores to account for employee benefit obligations under the government’s new wage code. Excluding this, the adjusted core PAT was ₹104.3 crores, a healthy 12.7% YoY growth.

B. Depreciation and Interest: The Asset-Light Advantage

TTL’s cost structure reveals the immense advantages of its business model:

-

Depreciation: In Q3 FY26, depreciation and amortization expenses stood at a mere ₹7.0 crores (and ₹19.0 crores for 9M FY26). For a company generating over ₹620 crores in quarterly revenue, a ₹7 crore depreciation charge is negligible.

- Explanation: TTL operates an “asset-light” manufacturing model. Instead of massive heavy-metal foundries, it focuses on high-value precision engineering, final assembly, and R&D. This ensures that fixed costs remain low, translating into high operating leverage where incremental revenue flows directly to the bottom line.

-

Interest / Finance Costs: Finance costs for Q3 FY26 were practically non-existent at just ₹0.6 crores (₹6 million).

- Explanation: The company is effectively debt-free. It funds its operations internally and via customer advances, completely shielding its earnings from the current high-interest-rate macroeconomic environment.

C. Decoding Capital Allocation and Return Ratios

Triveni Turbine exhibits some of the best return ratios in the global industrial and capital goods sectors.

-

Return on Capital Employed (ROCE) and Return on Equity (ROE): * Historically, TTL’s ROCE and ROE have tracked exceptionally high, with ROCE standing at 40% and ROE at 32% as of recent annual metrics (FY25). Analysts and market data indicate these ratios continue to track well above 30% into FY26.

- Explanation for High Ratios: These phenomenal metrics are driven by a combination of high profit margins (~24.6% EBITDA) and an incredibly high Asset Turnover Ratio. In recent periods, TTL’s asset turnover has improved significantly to around 5.86x. Furthermore, because the company collects hefty customer advances before building the turbines, its working capital is often negative. When a company operates with negative working capital, the “capital employed” denominator shrinks artificially, catapulting the ROCE to stellar levels.

-

Capital Allocation Strategy:

With immense cash generation and no debt to service, TTL’s management faces a “problem of plenty.” As of recent quarters, the company’s cash and investments position stood robustly over ₹1,000 crores. The management allocates this capital across three primary avenues:

-

-

R&D and Future Optionality: Instead of reckless capacity expansion, TTL allocates capital to high-yield R&D. This includes the development of API-compliant turbines, CO2-based heat pumps, and supercritical energy storage systems (like the NTPC pilot). This ensures future-proofing against the global energy transition.

-

Strategic Global Footprint: Capital is deployed to get closer to the customer. For example, incurring planned upfront losses (e.g., ~₹21 crore loss in 9M FY26) to establish the Triveni Turbines Americas Inc. facility in the USA, and capitalizing the South African subsidiary (TSE Engineering) to capture localized refurbishment markets.

-

Generous Shareholder Rewards: Because the business requires very little capital to grow (low maintenance capex), the bulk of free cash flow is returned to shareholders. For FY26, the Board has already declared an aggressive interim dividend of 225% (₹2.25 per share).

8. Working Capital, Inventory, and Cash Flows Analysis

TTL operates an incredibly efficient, engineered-to-order financial model that relies heavily on customer advances rather than external debt. This allows the company to fund its growth internally while maintaining a highly liquid balance sheet.

A. The Negative Working Capital Cycle

TTL is one of the rare capital goods manufacturers that operates with a negative working capital cycle.

-

Over the last five years, the company has transformed its working capital position from a positive ₹66.0 crores in FY20 to a highly efficient negative ₹75.6 crores at the close of FY25.

-

Explanation: Because steam turbines are highly customized, engineered-to-order products, TTL mandates significant upfront advances from customers upon signing the contract. These customer advances (recorded as “revenue received in advance”), combined with standard trade payables (which stood at ₹341.6 crores at the end of FY25), effectively fund the company’s entire raw material procurement and manufacturing process.

B. Receivables and Debtor Days

While the company’s overall collections remain highly secure, there has been a strategic shift in the receivables cycle.

-

Debtors Turnover Ratio: The debtors turnover ratio moderated from 10.76x in FY24 (approx. 34 days) to 7.41x in FY25 (approx. 49 days). Correspondingly, absolute trade receivables rose from ₹125.0 crores in FY24 to ₹354.3 crores in FY25.

-

Explanation for the Shift: This optical increase in receivable days is a direct consequence of the company’s aggressive expansion into international markets. Export orders inherently involve longer transit times and different milestone billing structures compared to domestic orders. The management explicitly clarified that over ₹100 crores of these outstanding dues are fully secured by Letters of Credit (LCs) and bank guarantees. Therefore, the increase in receivable days poses virtually zero credit or default risk to the company.

C. Superior Inventory Management

Despite a massive surge in the company’s order book (which crossed ₹1,986.4 crores in Q3 FY26), TTL has maintained spectacular control over its inventory.

-

Inventory Turnover: The inventory turnover ratio improved substantially from 4.83x in FY24 to 5.96x in FY25.

-

Absolute Inventory Reduction: Counterintuitively, the total inventory on the books actually decreased from ₹226.2 crores in FY24 to ₹194.8 crores in FY25.

-

Explanation: This was achieved through superior supply chain planning, value engineering, and broadening the global supplier base. Furthermore, an improvement in average product delivery lead times by 20% in FY25 meant that raw materials were converted to finished goods and dispatched to customers much faster, preventing capital from being tied up in factory floors.

D. Q4 vs. Q2/Q3 Dynamics (Seasonality and Deferments)

In the industrial capital goods sector, cash flows and working capital requirements fluctuate significantly throughout the financial year based on dispatch schedules.

-

The Q1-Q3 Build-Up: During the first three quarters (Q1 through Q3), inventory levels—specifically Work-in-Progress (WIP)—typically swell. This happens as the company procures raw materials (castings, forgings) and begins the lengthy multi-month assembly of turbines.

-

The Q3 FY26 Impact: In the most recent Q3 FY26 results, the Aftermarket segment’s turnover declined by 22% YoY (to ₹138.0 crores). Management explicitly noted that this drop was largely due to the “deferment of delivery of a large refurbishment order to coming quarters”.

-

Explanation: When clients defer deliveries (often due to site unreadiness), TTL is forced to hold the completed or semi-completed turbine on its own books as inventory. This temporarily traps cash in the working capital cycle during Q2/Q3.

-

The Q4 Unlocking: Q4 is historically the strongest quarter for the capital goods industry. Deferred orders from Q3 and major year-end dispatches are billed and shipped in Q4. This triggers final milestone payments from customers, rapidly depleting the WIP inventory built up over Q2/Q3 and resulting in a massive cash inflow that artificially depresses the year-end working capital numbers to the aforementioned negative levels.

E. Cash Flows and Liquidity Profile

TTL’s operational efficiency translates into phenomenal cash generation.

-

Free Cash Flow (FCF): In FY25, the company generated robust Free Cash Flows of ₹384.4 crores, a massive jump from ₹165.0 crores in FY24.

-

Cash Reserves: As a result of this cash compounding, total investments and cash equivalents swelled to ₹987.3 crores by the end of FY25.

-

Explanation: This enormous liquidity moat provides TTL with significant optionality. It allows the company to self-fund its global expansion (such as the recent incorporation and capitalisation of its Houston, USA facility), invest aggressively in next-generation R&D (like CO2 supercritical turbines), and consistently reward shareholders with hefty dividend payouts.

9. Capex, Timelines, Growth Prospects & Optionality

Triveni Turbine Limited (TTL) is aggressively transitioning from a conventional steam turbine manufacturer into a comprehensive energy transition and turbomachinery solutions provider. Its capital expenditure is strategically directed toward specialized R&D infrastructure rather than purely expanding basic manufacturing floorspace.

Capex and Timelines:

· R&D and Testing Infrastructure (Peenya & IISc):

Commissioned Heat Pump Facility: The company successfully met its timeline and commissioned India’s first commercial, high-temperature CO2 heat pump and chiller test facility at its Peenya plant in Q1 FY26. This facility has already validated TTL’s new heat pump technology (delivering heat up to 122°C with a COP of 6), translating into the company’s first commercial orders for the product.

o Triveni Turbines Centre of Excellence: In November 2025, TTL took a major step in expanding its R&D infrastructure by inaugurating the Triveni Turbines Centre of Excellence at the Indian Institute of Science (IISc), Bengaluru. This state-of-the-art facility is dedicated strictly to advancing energy transition technologies, materials innovation, and sustainable turbomachinery. Concurrently, the ‘Dhruv Manmohan Sawhney Turbomachinery Chair’ was established to fund applied research in thermal energy and next-generation CO2 systems.

o 15 MW Load Test Centre: The company continues its investment in a new Load Test Centre capable of handling up to 15 MW to accelerate the performance validation programs for its increasingly complex turbine configurations.

· Manufacturing Capacity Expansion (Sompura Facility):

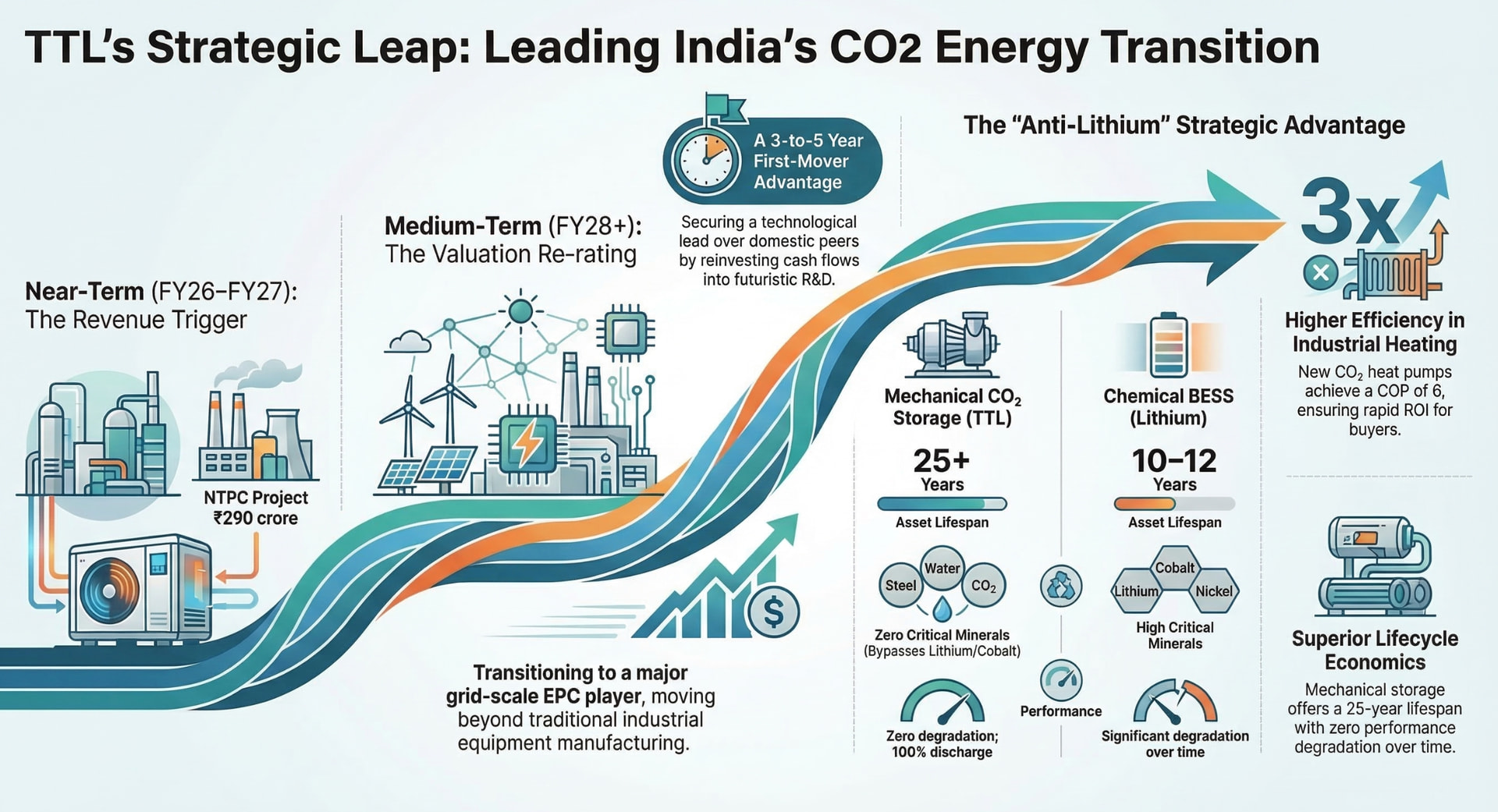

o Driven by an order book that surged past ₹22.2 billion earlier this financial year, management has initiated a significant capacity expansion at its secondary manufacturing hub in Sompura. This capex involves adding further heavy-lifting capabilities and installing a massive new test bed specifically for testing large-scale turbines and rotating equipment. This expansion is scheduled to be capitalized by the end of the current financial year (March 2026) and is expected to be fully operational by June/July 2026.

· Global Footprint Expansion (Americas & South Africa): Capital continues to be deployed to scale Triveni Turbines Americas Inc. in Houston, Texas. While this localized rotating machinery repair facility is currently in its cash-burn phase (reporting an operating loss in the 9M FY26 period).

o Furthermore, in late 2025, TTL deployed capital to acquire the remaining 30% stake in TSE Engineering Pty. Ltd. (South Africa) for roughly ZAR 10.97 million (₹5.6 crores), consolidating full operational control over its strategic aftermarket hub for the African continent.

Growth Prospects & Optionality:

-

API Turbines (Oil & Gas): TTL has successfully penetrated the highly regulated API-611 and API-612 turbine segments. The company has secured vendor approvals from major global refineries and is seeing robust order inflow for both drive and power generation turbines across the Middle East, Southeast Asia, the Americas, and Europe.

-

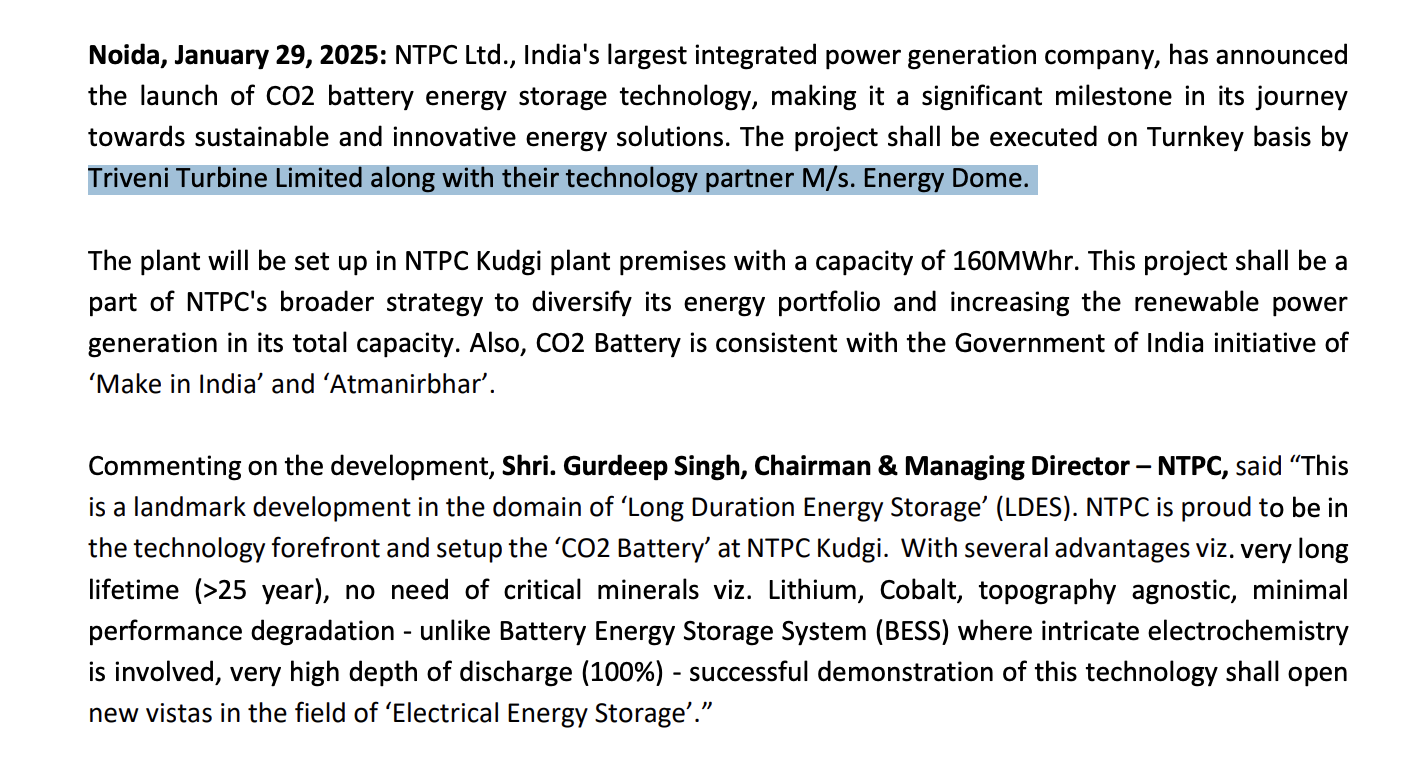

Massive Optionality in CO2-Based Energy Storage: In FY25, TTL secured a landmark ₹290 crore (₹2.9 billion) turnkey contract from NTPC to build a 160 MWh CO2-based long-duration energy storage system (LDESS) at the Kudgi Supercritical Thermal Power Plant. This mechanical storage system utilizes industrial-grade components (turbines, compressors), operates completely independently of critical minerals like lithium or cobalt, and boasts a lifespan of over 20 years. A successful proof-of-concept here unlocks exponential optionality, positioning TTL to capture a significant share of the multi-billion-dollar global grid-scale energy storage market.

-

Gas Expanders and Heat Pumps: The company is developing next-generation gas expanders that utilize alternative working mediums such as CO2, air, and hydrocarbons to recover waste heat. This opens up new, lucrative avenues in low-grade heat recovery for energy-intensive sectors like steel, cement, and chemicals.

10.Acquisitions (Synergies, and Drawbacks)

TTL’s inorganic and subsidiary-led growth strategy focuses on penetrating lucrative international aftermarket and refurbishment segments by establishing localized ecosystems.

TSE Engineering (Pty) Ltd, South Africa:

-

Acquisition & Synergies: Originally acquired as a 70% stake in March 2022, TTL has now assumed full 100% control of TSE Engineering. This acquisition provided immediate, localized access to the Southern African Development Community (SADC) region. The primary synergy realized was the ability to secure and execute major utility-scale refurbishment contracts. For instance, TTL successfully overhauled and maintained large utility steam turbines in the SADC region, directly alleviating severe load-shedding and reducing power outages.

-

Drawbacks: The aftermarket business can be a victim of its own success. Because TTL’s overhauls significantly improved grid stability and reduced regional power outages, the immediate demand for emergency, outage-related services temporarily declined, causing the regional aftermarket order book to grow at a muted 1% year-on-year.

Triveni Turbines Americas Inc., USA:

-

Acquisition & Synergies: Incorporated in February 2024 as a wholly-owned subsidiary, TTL set up this entity and its Houston-based facility to directly penetrate the Americas. The synergy lies in targeting the world’s largest installed base of aging rotating equipment. By operating as a high-end Independent Service Provider (ISP) on the ground, TTL can offer rapid response times for refurbishing third-party machinery, while simultaneously building the customer trust required to cross-sell its own new API and industrial turbines.

-

Drawbacks: Establishing a greenfield presence in a high-cost geography requires absorbing substantial initial capital drag. The U.S. subsidiary closed its first year (FY25) with a net loss of ₹23 crores. This was an anticipated drawback due to the heavy upfront investments required for plant, machinery, specialized manpower, and establishment costs before revenues could adequately scale.

11. Red Flags, RPT, Contingent Liabilities, or Litigations

-

Contingent Liabilities/Litigations: The company has a clean track record with no major ongoing litigations threatening business continuity. Auditor reports are unmodified.

-

Related Party Transactions (RPT): RPTs are strictly conducted at arm’s length. Since the demerger and TEIL’s exit, inter-company overlap has minimized.

-

Red Flags: 1. Wage Code Hit: The sudden ₹15.7 crore exceptional charge for the wage code in Q3 FY26 highlights how regulatory shifts in employee benefits can unexpectedly impact the bottom line.

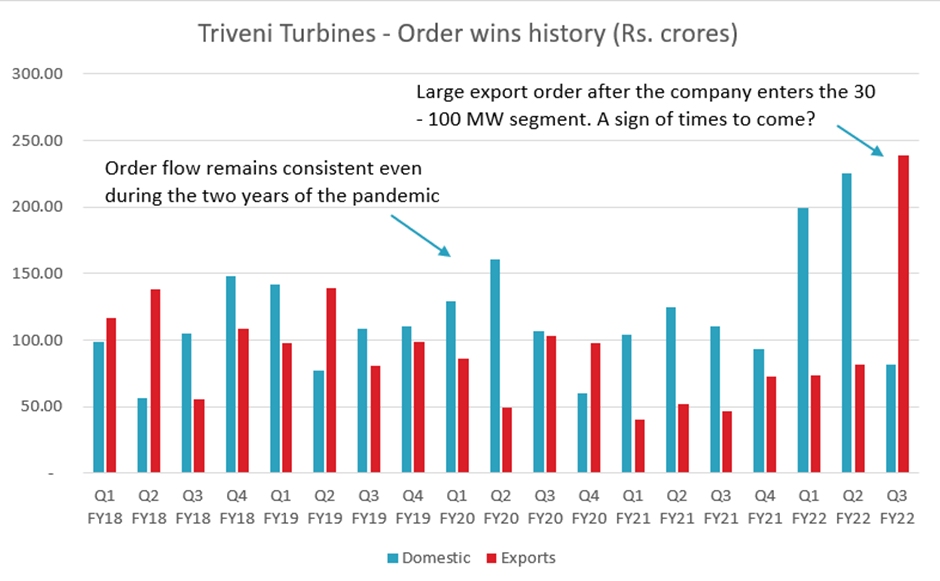

2. Order Book Cyclicality: Q3 FY26 saw a sharp 40% YoY drop in export order booking (₹208.4 crores), attributed to global trade uncertainties and delayed contract closures. While management remains confident about the pipeline, extended decision-making cycles by clients are a warning sign.

12. Competition: China, Local, and International

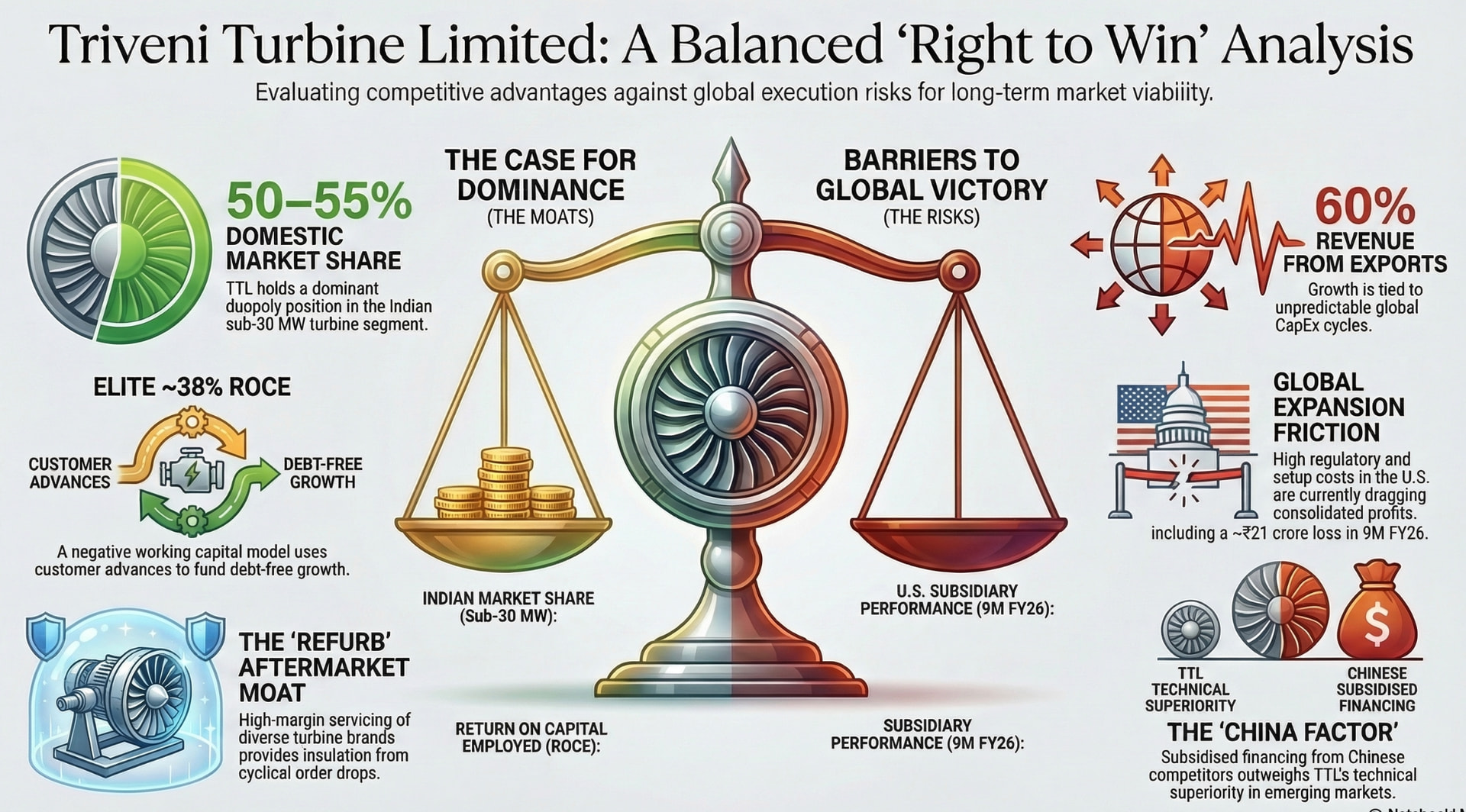

The global industrial steam turbine market (up to 100 MW) is a highly consolidated space because these machines are complex, highly customized engineered products rather than mass-produced commodities. Triveni Turbine Limited (TTL) has systematically carved out a dominant global position by focusing intensely on this niche.

A. Domestic Market Competition: The Duopoly

In the Indian market, especially in the 0–30 MW range, the competitive landscape is effectively a duopoly between Triveni Turbine and Siemens Energy India.

-

TTL’s Dominance: TTL holds a commanding ~50% to 55% market share in the domestic 0–30 MW segment. Siemens controls the bulk of the remainder (around 30% to 40%).

-

The Strategic Edge: While Siemens has a massive global footprint and strong technological capabilities, it historically focused on larger utility-scale turbines and shifted down to smaller turbines later. TTL’s pure-play focus on the sub-100 MW segment allows it to be far more price-competitive and nimble in India. Apart from these two, Japanese player Shin Nippon occasionally captures market share, but domestic customers heavily favour the localized service networks of TTL and Siemens. In the 30–100 MW range, TTL competes with BHEL, though BHEL’s primary focus remains on massive 500 MW+ utility projects

B. International Competition and the “China Factor”

Globally, TTL is recognized as the second-largest manufacturer of sub-100 MW industrial steam turbines by volume, trailing only Siemens Energy. Other notable global competitors include GE Vernova, Doosan Škoda, Mitsubishi Heavy Industries, and Baker Hughes.

-

The Chinese Threat: Chinese state-owned enterprises like Harbin Electric and Dongfang Electric represent formidable competition, particularly in emerging markets across Southeast Asia, Africa, and parts of the Middle East. Their primary competitive lever is aggressive, subsidized pricing and the ability to bundle turbines with larger state-sponsored EPC (Engineering, Procurement, and Construction) financing packages.

-

How TTL Outcompetes China:

1. Gestation and Delivery: TTL operates with a remarkably short gestation period. The time from order receipt to manufacturing and delivery is typically just 6 to 9 months. Chinese OEMs often struggle to match these rapid turnaround times for highly customized turbines.

2. Feedstock Agnosticism & Customization: TTL’s R&D focuses heavily on customized blade machining and thermodynamics tailored to the exact input feedstock (e.g., municipal waste, biomass, industrial exhaust). This tailored efficiency provides better lifecycle economics than off-the-shelf Chinese variants.

3. Aftermarket Proximity (Triveni REFURB): Industrial turbines face significantly higher wear-and-tear than utility turbines. TTL mitigates the threat of cheaper initial Chinese pricing by leveraging its Triveni REFURB division, offering superior, localized aftermarket support, spares, and annual maintenance contracts that Chinese competitors historically fail to match post-installation.

13. Risk Factors Affecting Future Growth

While TTL possesses a robust balance sheet and a strong order book, its transition into a global turbomachinery and energy transition player exposes it to distinct macro and execution risks.

A. Geopolitical Volatility and Tariff Escalations

With exports constituting roughly 60% of its total revenue, TTL is highly sensitive to global trade dynamics.

-

U.S. Expansion Risks: The company recently incorporated Triveni Turbines Americas Inc. in Houston, Texas, to tap into the lucrative American refurbishment and API-compliant turbine markets. However, the looming threat of escalating U.S. tariffs and protectionist trade policies creates significant friction. As management recently noted in earnings calls, clients in the Americas occasionally defer final order placements due to uncertainty regarding ultimate tariff levels, which complicates pricing models and revenue recognition timelines.

-

Global Supply Chain Disruptions: Broader geopolitical conflicts (such as unrest in the Middle East) have periodically delayed mechanical run tests and site readiness, forcing TTL to hold finished goods inventory longer than anticipated, which can temporarily stress working capital.

B. Oil Price Cyclicality and the API Turbine Segment

A massive engine for TTL’s recent margin expansion has been the sale of API 611 and API 612 compliant drive and power turbines. These are mission-critical components for petroleum refineries, petrochemical plants, and fertilizer units globally.

- The Capex Risk: Demand for API turbines is intrinsically linked to the capital expenditure cycles of global oil and gas majors. A sustained collapse in global crude oil prices—driven by macro slowdowns or oversupply—could lead refineries in the Middle East and the Americas to sharply curtail or delay their capacity expansion and modernization projects, directly hitting TTL’s high-margin order pipeline.

C. Adoption Rates of Energy Transition Technologies

TTL is aggressively allocating capital to next-generation decarbonization technologies, specifically CO2 supercritical energy storage, advanced mechanical vapor recompression (MVR), and industrial gas expanders.

-

The Execution Risk: These technologies are largely in the pilot or early commercialization phases (such as the 160 MWh LDESS project for NTPC). There is a distinct technological risk that these mechanical solutions might be outpaced by rapidly falling costs in alternative storage technologies, like grid-scale lithium-ion or solid-state batteries.

-

Industrial Decarbonization Delays: A key growth vector for TTL’s new heat pumps and gas expanders involves capturing waste heat in hard-to-abate sectors, particularly the global steel and cement industries. The transition to green steel (utilizing green hydrogen and electric arc furnaces) requires massive capital outlays from steelmakers. If the macroeconomic environment forces the steel industry to delay its broader decarbonization and green hydrogen adoption targets, the corresponding demand for TTL’s specialized low-grade heat recovery and energy transition turbines could be heavily deferred, stranding some of the company’s R&D investments.

D. The “Wage Code” and Regulatory Cost Pressures

As witnessed in Q3 FY26, the company had to absorb a sudden ₹15.7 crore exceptional charge due to obligations arising from the implementation of a new wage code. Operating a highly specialized R&D and engineering workforce of over 1,000 employees means that any further regulatory shifts in labor laws, provident fund structures, or specialized engineering talent shortages in India could apply structural pressure to the company’s currently stellar EBITDA margins.

----------------------------------------------------------------------------------------------------

Compiled Notes From Here & There. No Buy/Sell Recommendation.

----------------------------------------------------------------------------------------------------------------