We visited Triveni Turbines factory in Peenya, Bangalore and came away impressed.This is one of the cleanest hi-tech automated manufacturing facilities that we have visited and houses some of the most sophisticated 5-Axis CNC machines for manufacturing high-precision turbine blades and rotor shafts. Integrated CAD/CAM and Advanced Data acquisition S/w used in seamless manufacturing and testing.

Triveni Turbines Limited listed on BSE in Oct 2011, consequent to Triveni Engineering Ltd. demerging its Turbine business. Triveni Turbines is the market leader in the 0-30 MW Industrial Steam Turbines in India with over 40% market share and had grown to touch a Topline of over 600 Cr in FY11 and needed a separate focus. The company sees significant potential in the Steam Turbines business and has entered into a JV with GE for manufacturing higher-end 30-100 MW Turbines.

The modern Steel & Glass Corporate office building looked impressive. we were amazed to learn this was constructed ~30 years back. Seemed like a Management with foresight - investing in state-of-the-art machinery for the last 5-6 years, managing to utilise the capacity well, getting GE as a technology partner in the JV, the infrastructure in place that we witnessed - all seemed to point to a progressive Management!

Salient Points:

- )- 0-30 MW Steam Turbines Annual market size of 1500 Cr in India. With over 600 Cr in Annual sales, TTL has a dominant position with over 40% market share in India

- )- Over 2500 installations in over 30 countries. Exports segment contributes 20-25%

- -Competitors - Siemens, a Japanese player Shin Nippon, and a couple of Chinese players

- -Additional 30-MW Steam Turbines market estimated to be ~1500 Cr market in India opens up for TTL with JV with GE. TTL will be manufacturing these turbines and has the marketing rights for India, while GE has the marketing rights for developed markets

- -Totally 12 orders in 30-100 MW Turbines were booked in India in FY12. TTL has booked 2 of these orders, which will get commissioned in FY13 and establish the JV credentials

- -9m FY12 TTL has delivered 490 Cr in Sales, with an EBITDA of 112 Cr, EBITDA margin of ~23%.

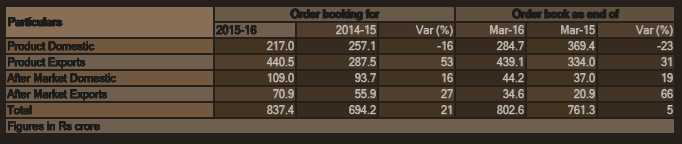

- -Orderbook of 540 Cr as on January, 2012

- -According to the company, its focus on after-market service has proven to be a decisive differentiator from competitors. After-market service segment constitutes 16% of total revenues and is higher-margin business

- -With 5bays & 19 test beds, plant capacity is 150 turbines per year. Management indicates there is room for some 40% growth without incurring any significant further capex.

- -TTL has a negative working capital cycle, as it receives 20% advance from all customers and maintains low inventory

- -The company expects 5-8% growth in FY12 and over 15% growth for FY13.

At CMP 43, TTL quotes ~16x estimated FY12 earnings.

Views Invited.