My hope is that the management comes out with a statement or Matrix Partners force them to do so, so that the position is clarified. As we know, these stocks seem to swing wildly. So if the management can assuage the fears of the investors, the stock should bounce back. And maybe that is when we should re-enter for the long term. But if the management remains silent, it will be construed as an attempt to to hide something.

If we consider the Business-Management-Valuation, Business and Valuation both stands out well, but worry part is Management. It is unclear why promoters kept pledging more and more shares. Pledged Shares Jumped Massively TO 54.82Lakhs, 43.23% of Promoter Stake in Sep Qtr, VS 39.82Lakhs, 31.57% in June Qtr.

The company is having sufficient cash, why would promoter require so much money and why Pledged shares route? Hope the partners force the management to give an explaination.

Management seem to have pledged their shares to buy the stock. Not sure if this is something other companies/promoters do.

Shareholding pattern for September 30, 2015 shows promoter owning 29.97% (43.23% of which is pledged), where as Shareholding Pattern For June 30, 2015 shows promoter owning 29.82% (31.57% of which is pledged). So net increase of 0.15% in promoter holding (along with increased pledge %)

So it looks like promoters pledged their shares to buy more shares and the price range from Jun 30 to Sep 30 was approximately Rs.300-Rs.470. I couldn’t locate the exact disclosures to figure out the exact buy price by promoters. My sense is that promoters bought more by pledging post the QIP @ Rs.440. This does show their confidence in the company. But then the SES raised concerns on high receivables around late Sep/early Oct. Though company clarified the reason’s for high receivables, the stock started its downtrend, which again was heightened by lower growth/margins last quarter (though management claimed the reason for lower margins were due to highest number of pre-school addition (73 in Q2 FY16)).

Post the initial pledge, as the stock price started falling, they had to increase their pledge for “Creation of Additional Security against Old loan”. So I assume the promoter pledging will increase with fall in stock price (and I would assume that the financial institutions would start selling when the pledge reaches 100% of promoter shareholding and if price falls further).

BTW, company does have cash in hand (post Rs.200 crore QIP) and they seem to be using it for expanding in Delhi/NCR regions along with other locations. Per last confcall, they’ll keep adding more centers in Delhi/NCR and they sounded bullish about the prospects here (and ofcourse they cannot use QIP money to buy shares  and so they pledged)

and so they pledged)

Not sure why the stock hit LC today and if there’s something which we are not aware.

Stock does look like a value buy for a long term (provided management walks the talk w.r.t expansion/sweating their existing assets for optimal utilization and if everything pans out as they expect), but not sure where the bottom is for this stock and what would be right level to buy now.

Disclosure: Invested and planning to add if it falls further.

1 Like

The most surprising thing for me is that Matrix partners bought at 440 but they are not buying when the price has fallen to 170. That is totally absurd, as management is trying to a lot of things to get their act right like selling k-12 business land etc. I my next and last buy would be somewhere around 150 and after that I will go to big sleep like Kumbhakaran w.r.t. Tree House

http://www.nseprimeir.com/Pages/PIT_Summary.aspx?value=zD8loHOugfjM600MSHCcMw==

The link says there has been buying, but not significant over last 3 months.Though 6 months back they bought more.

http://www.nseprimeir.com/Pages/Pledge_Summary.aspx?value=zD8loHOugfjM600MSHCcMw==

Pledge summary gives how they are being forced to pledge on a regular basis over the last few weeks. My guess is with the last few weeks of pledging the total % will be more than 60% of their holding!

The question is where is the money being used which they raised using pledging shares? Is that used for some personal purpose or for business?

Disclosure: Invested and no plans to add further

In Dec, 14 Promoters had 100% pledged shares with pledged share/total capital at 28.94%.

I guess they raised QIP around that time and by March,15 they brought it down to 28.77% pledge with pledged share/total capital at 8.53%. Now by Dec,15 it seems to be going back to 100% again with shares falling so much. But raising money now will be challenging for sure at these prices!.

Disclosure: Invested and no plans to add further

Sorry for some wrong numbers in previous post.

I could calculate now. With latest figures available as of Nov 16th…

http://www.nseprimeir.com/Pages/disPledged.aspx?value=zD8loHOugfjM600MSHCcMw%3D%3D&dvrval=

The pledge % stands at 46.27%. Oct & Nov, nearly a million shares are pledged for creation of additional security against the loan.

I am invested in the stock for last 2 years. I like the business. Never bothered when share price was falling. Didnt bother even about deposit for K-12 segment… thought that even this 160 crores is lost, the existing playschool business is good enough for the share price. But friday fall has shaken… is there something we dont know which market knows? This fall in share price has created fear of further fall if promoters are not able to put up additional margin requirements… or they decide to sell some shares for additional margins. In that situation further sharp falls cannot be ruled out.

Purely on the basis of valuation, and on the presumption that management is telling the truth in reports and in concalls; I am finding the company extremely attractive. I never like to catch a falling knife, but I do plan to add more of it when share prices stabilizes.

No doubt the company is attractive from its playschools business. But this attractiveness of playschool seems to have driven the promoters to take undue risk and start venturing in to asset heavy business and resorted to pledging their shares to meet their WC issues.

The WC capital issue came because of the reckless nature of the promoter of investing the money from playschool to other asset heavy K12 business. Instead of improving playschool business WC/cash flow conditions, the company seems to have just focused on building more schools and showing great income statement… This has definitely attracted many investors for sure and EPS growth made the stock always attractive and pushed the stock price to lofty highs year back. Promoters might have thought a higher share price can always cushion them from their mistakes and they can get out of their pledging after selling their asset heavy stuffs. But it looks like Market didn’t give the time they wanted.

What I see is, the promoters started resorting to pledging shares from the Dec, 2012 quarter. What it started with a small pledge of 1 million shares has now increased to pledging of 6.3 million shares which is close to 15% of total share capital and ~50% of promoter holding. Mr Rajesh Bhatia stake is 99.96% pledged and 72.79% of GEETA RAJESH BHATIA/RAJESH DOULATRAM BHATIA stake pledged.

From GEETA BHATIA stake, 11.39% is pledged, so there are some shares left.

With last week fall, obviously more margin call required and they have to pledge more shares. Seeing Geeta Bhatia stake still intact, was she not part of some of the misadventures of Rajesh Bhatia?

Doing some back calculations, I feel the 60~80 crores what is being raised by pledging shares. But to maintain this loan, the investors have lost now market cap of more than 800crore!!

Worst case I see is, somehow the promoter have to arrange money to release their pledged shares and bring some sanity or time for promoter change as the stake of promoter will be sold openly by banks or will be held by the banks and promoter control of 30% might end up coming down to 10%~15%

2 Likes

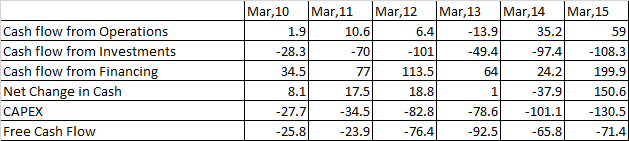

The below table gives the cash flow picture (in Cr). All the while equity route has been used and debt was kept minimum. But instead pledging was done to raise money.

Can you please tell me where you got the Capex figure from? Any website or just the annual reports? I see the other information given on the websites but not the capex figures.

If this comment is inappropriate for this board, I will delete it once I get my answer. Thanks.

1 Like

Tree House Education up Shit Creek & Down Market Big Time at Rs 169

I use www.gurufocus.com for my analysis. It is a paid site, so you may not be able to access the full details. From this site I got the CAPEX. Again CAPEX you can calculate also from the balance sheet also.

According to me , better way to calculate FCF would be to take out Interest cost (which according to Indian Gap is added in CFO and then subtracted in CFF) so Actual CFO will be CFO(As per annual report) - Interest cost and FCF will be much lower and which leads to constant need for raising funds via debt or dilution or pledging

1 Like

So Promoter pledged ~12% of ~30% of his ownership, that is, ~3.6% of company’s shares. If it was a fresh loan then at an asset cover of 2 times on pledged shares, he would have got money to buy 1.8% of company’s shares, but he bought only 0.15%. He monetized his shareholding by pledging it and used more than 90% of that money outside the company (read: put it in his pocket). You have done good work in culling out the data, but I would not agree with your conclusions if a large part of pledging was for new loans and not margin calls. His pledging of shares does not give me comfort, but discomfort.

Anyways, it is easy for me to pontificate, since I never invested in the company. I did not like the financials of the company that claimed very high return on equity, because in my opinion sustainable returns in this business would be much lower. Some analysts were projecting even higher profitability in future.

1 Like

Number of days in working capital are 690 days which is big number.

Loan and advances figure is 236 cr. What is this all about? 236 cr is huge amount if we compare it with Net block of 321 Cr?

Thanks @Prash. I think I will leave my question and your comment because it might benefit other investors too.

Gaurav seem to have updated his blog with more details.

Refer to the section under “Significant Update on Saturday Afternoon,November 28,2015”

The fall has been truly spectacular both in magnitude and in duration. Any contrarians out there? Care to explain the thesis if you’re contrarian and willing to go long / chase the price?

Disc: no position

Once again, an education stock seems to be getting caught up in corporate mis-governance. Like real estate, it seems this sector is filled with landmines which you can walk around for a while but will eventually end up blowing yourself. I dont mean to generalize but after so many corporate misdemeanours in the education sector, it seems like this one was inevitable.

On the face of it, the company looks like a fantastic buy at this price. It seems to be growing rapidly, taking the right steps by trying to sell off assets like the land and building in Baroda and sweating preschool assets by adding day care services. However, the primary question that needs to be answered is about the integrity of the promoters. If there is no problem with that, at this price, the company is a no-brainer. With all the questions being raised about change of company secretary, change in CFO, change in auditors, receivables, possible fund diversion, incessant pledging for reasons not known yet, it is better to stay out and wait for the dust to settle for clarity to emerge.

The best thing for minority shareholders will be for the promoter to come out and explain the current situation and particularly bring some transparency as to the deployment of the 140 crore capital being used to buy rights to manage K-12 schools. Although, it is the personal right of the promoter to do whatever he wants with the capital that he raised through pledging, I think it will also be very helpful for him to clarify how he has used those funds to answer the question as to why there is so much pledging. Bringing a big 4 auditor will definitely help as well as it will give confidence to investors that the numbers are verified and real.