“The management and administration of every School shall vest with a individual / Trust / Society.”

So if the regulations are implemented in its current form, for profit companies like TreeHouse will be forced adopt complicated entity structures to provide services to Pre Schools, like they have to in K-12 space. While the regulations are still in draft stage, there is a risk that

Is this going to be a cause of big worry? Nevertheless, am trying to analyze this in Lynch style, without involving too much complications:-

Concerns : Education is not looked at, as a for Profit sector in India. Several politicians have created Educational Empires in the country, but they generally operate thru complex structures, usually various educational trusts. So changes in Govt policies will always be a threat and private / for profit players are vulnerable.

From where further Growth will come :

(i) The mgmt has indicated that the next big opportunity for growth within preschool segment would come from Tier II & III towns in India.

(ii) New avenue for revenue - The Day Care services : According to the management, Day Care services also has an equally large opportunity / market size, if not bigger than the pre-school segment

My Edge : Have visited the nearest center in my locality and very much willing to put my son there in Nursery. But could not do so, as it is relatively far and there are no school operated buses/vans. The center seemed quite good with well equipped toys/material, good staff, very well designed interiors with paintings and stickers/cartoons, a very good student – teacher ratio. Got to know that they follow CBSE pattern with activity based learning.

Valuation : My fellow boarders has already done it. IMHO, it is fairly valued at 28/29x at CMP (as on 30-06-2015).

Discl : Already invested and wanted to add more. But seriously thinking if this share could be a part of long term portfolio.

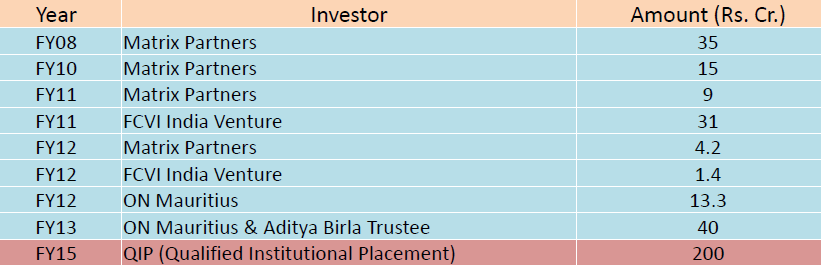

no doubt about it that promoters stake is low at 30% but if you see they have grown aggressively from 1 branch in 2004 to 637 branch in 2015 so it was a very high growth and it needs more equity so they bring into some PE partner by giving them shares and doing some QIP. Now moving ahead they are well funded for further high growth and even business is generating good cash flow to fund high growth so i think now they don’t need to scale down their holding going forward. And about pledging it is done for their personnel reasons even it is at 30% of the promoters holding.

Thanks. How do you see competition from other slew of pre-school education companies - both organized and unorganized ? Zee Learn, Euro Kids and several others. Any moat with Tree house ?

about pledging of promoter’s shares - Would you like to elaborate pledging for personal reasons? Doesn’t this mean that promoters are not interested in their stock itself?

Earlier, promoters pledged their share to subscribe the share warrant issued to them and now they are pledging more shares to increase their holding in the company by way of purchasing more shares from open market. so, it is not true that they are not interested in their stock.

If anyone going to AGM of Treehouse on 25th Sept, Please raise one question on behalf of me that **We have provided Rs.28 crs as a Deposit for K-12 schools in this year and we are allocating these deposits since Fy11. all to gather we have provided around Rs.151 crs as K-12 deposits ,So how long we are going to allocate these deposits from hereon and how much more we are expecting?

Please raise this question on my behalf as i can not attend AGM due to some personnel reasons.

Hello,

Did anyone attend the AGM? The stock price has been consistently falling ever since the article in Business Standard regarding its receivables. SES seems to think the receivables figure of 42 cr. at the end of FY15 is fishy. Company has already issued a clarification stating that receivables are owing to K-12 services business (B2B model). Would like to know if this was discussed in the AGM and what was the management response to the queries.

Any first hand experience would be really appreciated.

I have a question after reading the annual report 2014-15.

Why TreeHouse need to invest in associate companies JT Infrastructure Private Limited & Mehta Treehouse Infrastructure Private Limited??

The Company has entered into a joint venture agreement with Jayshree Builders (‘JB’) to construct and rent a school building. As part of the arrangement, the Company and JB have agreed to equally contribute to the share capital of Mehta Treehouse Infrastructure Private Limited, a company in which both Treehouse Education & Accessories Limited and JB have equal share holding. The Company has a 50% interest in the assets, liabilities, expenses and income of Mehta Treehouse Infrastructure Private Limited, a company incorporated in India. The operations have not yet commenced.

I could not find any information about these companies. Can anyone throw some light on this?

Hi,

I have been trying to analyze why the TreeHouse stock is in a downward spiral.

From the positive sides, there are many such as,

Presence in growth market

Good Brand Recall

Strong return on investment capital

Asset light model

Healthy balance sheet

Presence in growing markets

7.Compelling Valuation

From the negative side I can list a few but would love to know more,

Muted growth in last quarter

Concerns about repeat of last 5 years growth trajectory

Corporate governance (pledging!)

Regulatory risks

Higher expense due to Marketing

Issues with latest QIP? Has management over promised?

Because of constant expansion, no free cash flow

For my valuation, I consider generally a company has a competitive advantage if it can maintain >40% gross margin, SG&A < 30% and >20% net margin. In case of THEAL, it is beating on all these counts. Even if THEAL net margin drops to by 500 basis points, it will be still above 20% net margin,which is great as it enjoys currently 28% net margin.

One question always comes to me is, why promoters are so willing to take equity route to raise capital and eventually dilute the shares? Is it because of prevailing high interest rates or worried about debt routes?

Receivables don’t seem a cause for concern. Per the latest September quarter results, those seem to be getting taken care of.

I think the downward spiral is because of pledged shares by the promoters. The more the price falls, the more the lenders will make them pledge to keep the loan reasonably safe. I think this is causing the downward spiral.

I am not sure though, because Matrix (buying as high as 440 a share) would have raised concerns. There is no press release and no word coming from the management. This seems to be exacerbating issues. Some folks have been begun to comare it to Pyramid Saimaira. unamused:

i think its good to stay away from it until managers send out some clarification and future action plan…what says?

Discl: not invested, under watchlist

See markets are irrational. As of now the business trading at a very cheap valuations. I think this fall will make management understand that how much people are against them venturing into K-12 school. Let’s hope that from next quarter onwards we see some change in management commentary.

Disclosure- Bought first at 440 and have been averaging (present average price is around 300). It forms 20% of my portfolio now and if management screws this up then I will loose whatever gains I had ever made in the market.

It closed today at 20% lower circuit (price now is 169). I agree, the price is not the only criterion, but folks are wondering if there are skeletons that are gradually coming out of the accounting cupboard, that the ordinary man on the street is unaware of.

Just this very month, a brokerage based in Malaysia, put out a buy recommendation. See the report from Maybank:

So the point is how even analysts were kept in the dark.

Now if we go by the logic that the company is facing a few financial issues (like no free cash flow) and that the receivables situation is improving, could we treat this as a market over-reaction?

It can then become a screaming buy at slightly lower levels.

@roysavio thanks for sharing the link. I see so many recommendations from different brokerage houses despite the fact of cash flow issue and still something is cooking behind the screen which is unknown to everyone? clueless what to do but looks like stock is beaten down harshly. Yes, a risk taker can think of making position below 150. Any thoughts?