Transrail Lighting Ltd. has recently announced significant order wins totaling ₹421 crore, which includes a large transmission line contract in a new African country, marking a strategic expansion for the company and bolstering its international portfolio.elitewealth+2

Key Details on the Latest Order Win

The ₹421-crore orders are led by international transmission & distribution (T&D) projects and include contracts in Poles & Lighting segments.tndindia+1

The major highlight is a new transmission line EPC contract in a previously untapped African market, underscoring the company’s global growth.capitalmarket+1

These additions have propelled Transrail’s FY26 year-to-date (YTD) order inflows past ₹3,500 crore as of August 2025, displaying an impressive 78% year-on-year growth in its order book.moneycontrol+3

Recent months have also seen order momentum with major contracts, including ₹701 crore of orders in August 2025 and an earlier ₹837 crore international EPC/product supply deal.upstox+1

Result tomorrow , doubts in people’s mind and shakeout by any means . In moneycontrol, there are rumours about 6 Transrail employees being abducted in Angola ! Another is someone made a presentation somewhere and raised many red flags ..hence the drop . If the results are not good we will surely get to hear a lot about how it is overpriced …pumped up etc. etc . . :)

Disc: Not invested .

I don’t track this company, but thought it’s important for those who do, to go through this presentation given by Nitin Mangal at the Alpha Ideas 20 20 meet yesterday.

This is the reality of many companies in India. Especially those who deal with the Government. This country runs on greasing the wheels. We shouldn’t read too much into such stuff even though it is probably true.

The second biggest business group in the country has done similar things multiple times at a much larger scale. No one bats an eyelid anymore unless it’s an outright fraud.

@Anurag4

By working capital Transrail has its own methodology, a slight deviation from generally accepted concepts.

So if you look at screener data, it would show much less.

Here it is how transrail calculates,

Working Capital Days=[(Adjusted Current Assets−Adjusted Current Liabilities) Revenue from Core Operations × 365]

Adjusted Current Assets — Includes:

Inventories

Trade receivables

Partial contract assets (likely portion expected to be billed/received within 12 months)

Retention money (classified under other current assets)

Indirect tax credits (GST etc., if recoverable within 12 months)

Excludes:

Cash and cash equivalents

Bank balances (e.g. fixed deposits, margin money)

Intercompany or related party loans

Advance income tax / deferred tax assets

Prepaid expenses (likely excluded if non-operating)

Adjusted Current Liabilities — Includes:

Trade payables (excluding acceptances)

Statutory liabilities (e.g., TDS, GST payables)

Accrued operating expenses

Operational provisions (e.g., warranties)

Excludes:

Trade payables under acceptances (LC-backed)

Short-term borrowings and working capital loans

Lease liabilities

Current maturities of long-term debt

Non-operating provisions or financial liabilities

So generally the high Working Capital is attributed to 2 things.

High Trade Receivables in current asset. Thats because these companies usually have Govt contracts & usually the payment cycle from govt is long dated.

Higher inventories, as these companies keep high stock of raw materials due to hedge against price volatility & seasonality.

These 2 are the major moving parts for Transrail. & therefore higher Working Capital Cycle.

Now compare this with its competitors like Kalpataru, KEC, Skipper & you would get the idea if its industry wise same/ near-about or other companies have a specific moat & shielded against this phenomena.

Would help you to understand if a company’s balance sheet is strong or weak.

And any companies who have contracts with govt usually would be having high trade receivables.

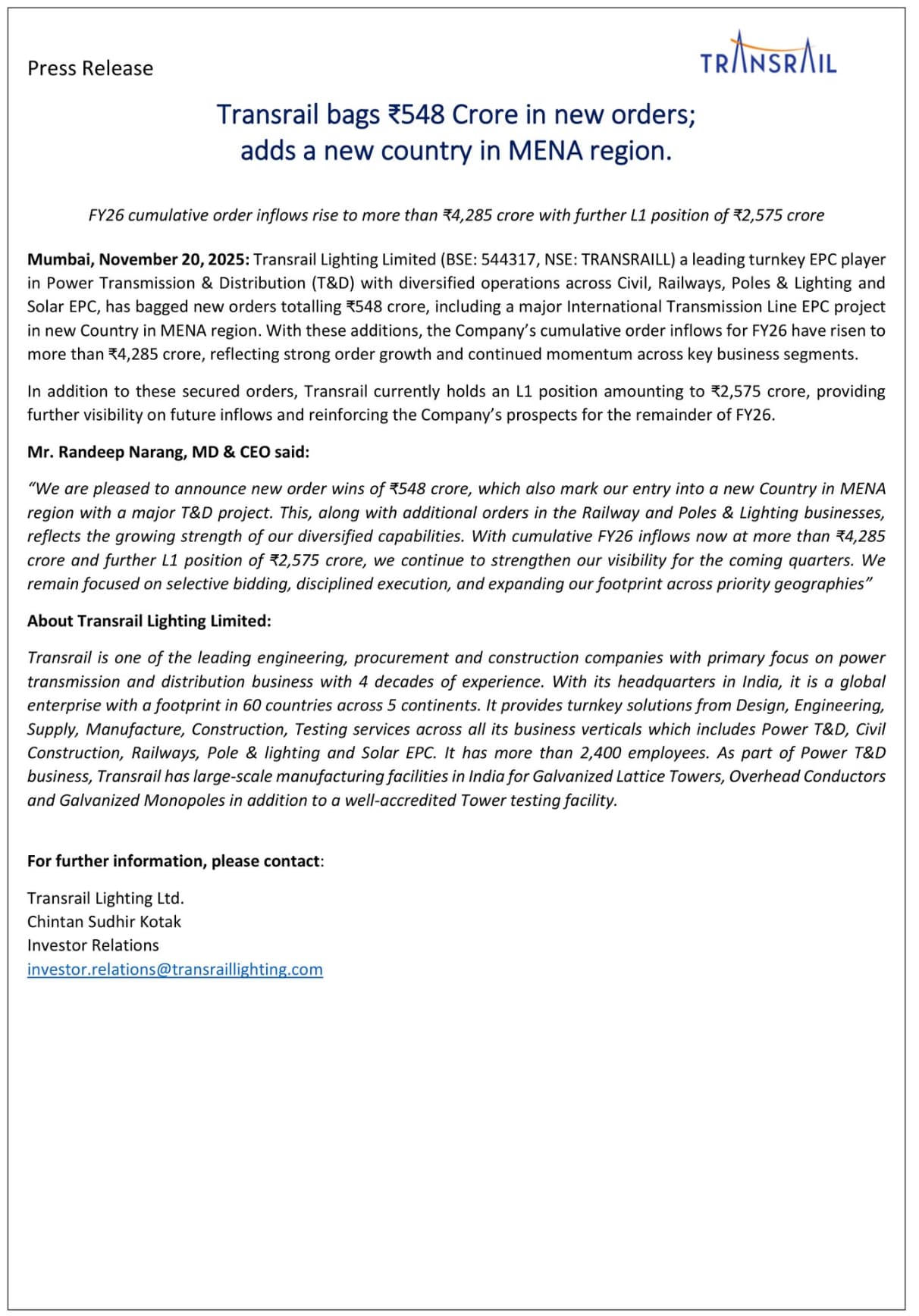

TRANSRAIL LIGHTING LTD — Major Order Win Update !

Secures ₹548 crore in fresh orders, including a large international T&D EPC project in a new MENA region market.

Thanks @vivek_lakhani for breaking this down. The adjusted methodology makes sense and gives a clearer picture of operational working capital. I will compare it with Kalpataru, KEC, and Skipper

First its main intention seems to be to prevent overcapacity of solar cells and Govt wants to protect prices. It wants to avoid China-style price crashes and NPA cycles/ unused inventory in solar manufacturing. In fact the note is only fundamentally detrimental to those manufacturers who were contemplating capacity expansion and new entry in this area.

The note seems to infer that solar cell supply capacity in the country is now considered sufficient for upcoming EPC demand. This is similar to norms tightening seen in steel & cement industries. This means solar EPC tenders are still expected to continue but possibly at a moderate growth and our National Power Transmission Plan 2032 is on track.

Stable module pricing is actually margin-positive for EPC players.

Second MNRE note is a advisory / guidance, not a binding RBI or statutory rule. MNRE cannot legally force NBFCs to stop lending — hence they have recommended caution only. NBFCs will reassess risk, tighten terms but not stop lending.

Coming to Transrail, its pure solar EPC exposure is small - One notable overseas solar EPC order (Jamaica) and all domestic RE-linked work is mostly evacuation / grid, not generation. Hence its mostly second-order impact on Transrail, in case even it happens.

The company announced the completion of its greenfield expansion at the tower manufacturing plant in Butibori, where commercial production has commenced.

The company also said that its brownfield expansion projects at tower manufacturing facilities in Deoli, Baroda, and Silvassa have been partially completed.

Following these developments, the total installed capacity of the companys tower manufacturing facilities has increased significantly from 84,000 MTPA to 1,72,400 MTPA.