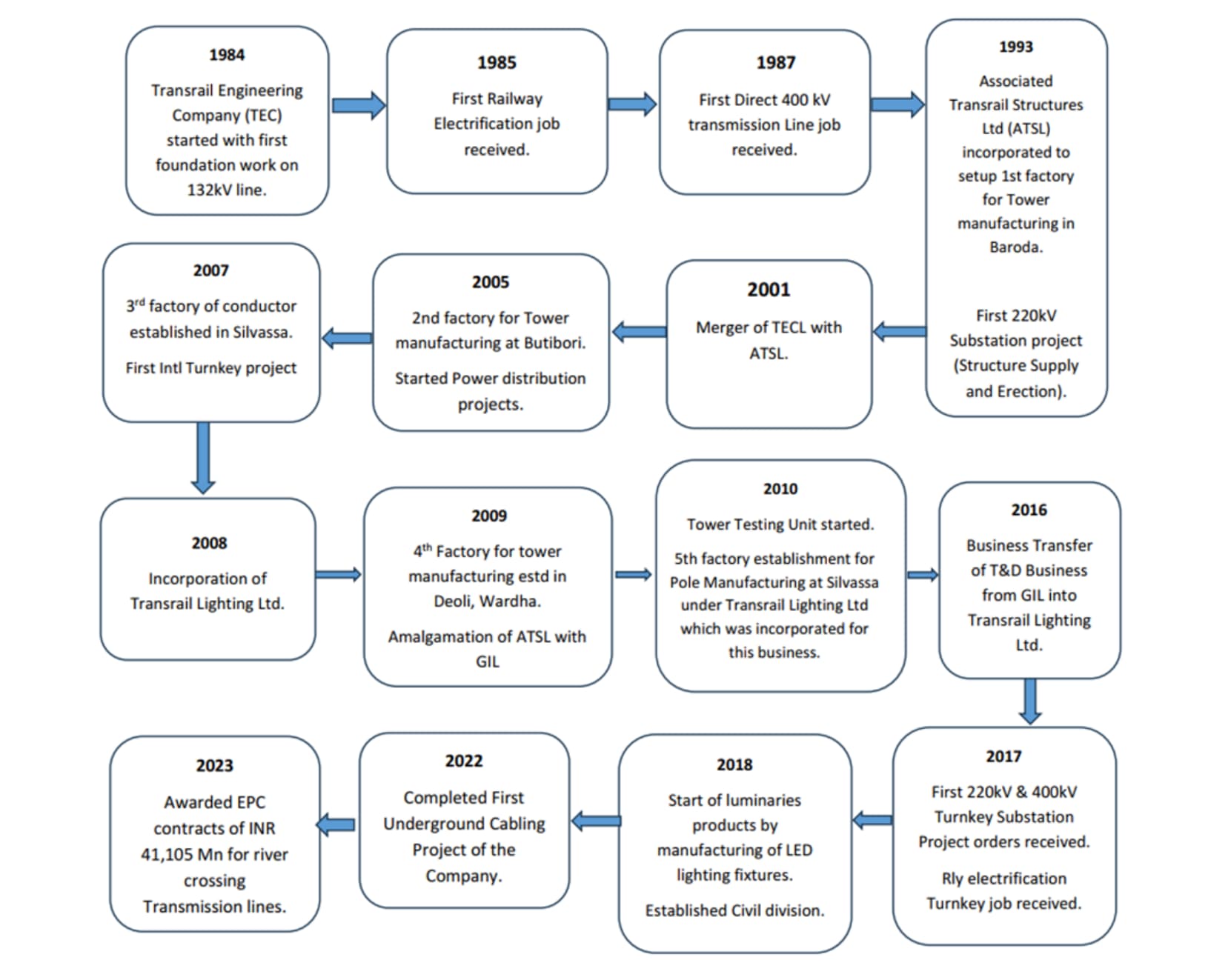

Transrail Lighting Limited, established in Mumbai in 2008 under the leadership of Digambar Chunnilal Bagde, an EPC industry expert with over 40 years of experience, has grown into a prominent player in power infrastructure.

History of the business:

- Entry into Railway Electrification: Transrail’s involvement in railway electrification began in 1985, with its first electrification job. By 1987, the company successfully completed a direct 400kV transmission line project. In 2017, it strengthened its presence in this sector by completing turnkey railway electrification projects, cementing its role in supporting modern railway infrastructure.

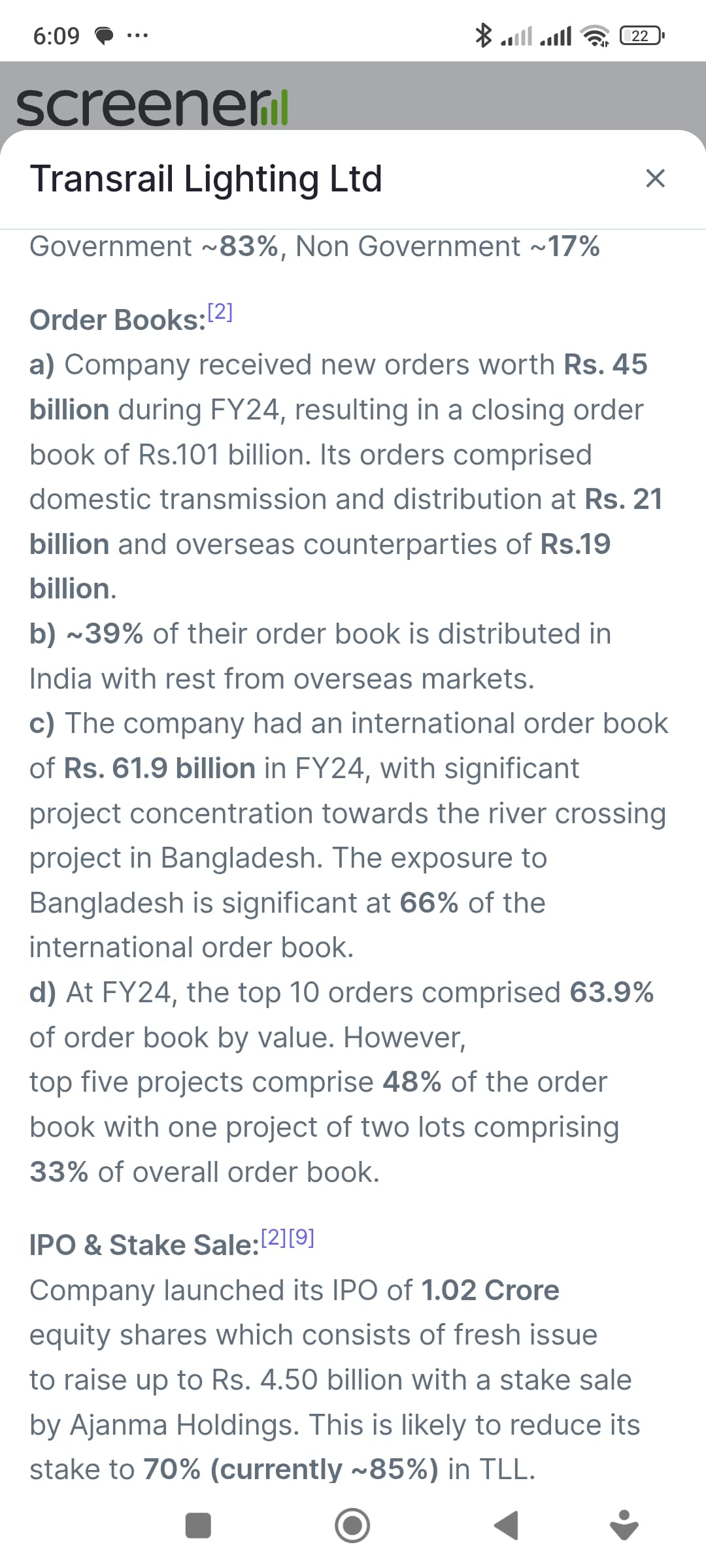

- Lighting and EPC Projects: In 2018, the company expanded its portfolio by introducing LED lighting fixtures and establishing its luminaries division. It further demonstrated its capabilities in EPC (Engineering, Procurement, and Construction) by securing major projects, including river-crossing transmission lines worth INR 41,105 million in 2023.

- Conductor Manufacturing: Transrail entered the conductor manufacturing business in 2007 with a facility in Silvassa. This marked its focus on producing essential components for power transmission, enhancing its manufacturing base over time.

- Growth in Transmission & Distribution (T&D): A major milestone came in 2016-2017, when the company acquired Gammon India’s T&D business. This acquisition included manufacturing facilities in Deoli, Baroda, and Silvassa, transforming Transrail into a fully integrated T&D company, capable of handling end-to-end power transmission and distribution projects.

- Underground Cabling Projects: In 2022, the company completed its first underground cabling project, showcasing its ability to execute complex infrastructure projects and further establishing its presence in the power sector.

Key Business Segments:

1. Power Transmission and Distribution (T&D)

This segment is the largest contributor to Transrail’s revenue, accounting for 83.83% of their total revenue from operations. The company offers comprehensive T&D solutions globally on a turnkey basis.

Services:

- Designing, manufacturing, testing, installation, and supply of galvanized steel structures for power transmission and distribution lines up to 765 kV.

- EPC services for both air-insulated and gas-insulated substations (AIS and GIS).

Key Products:

- Galvanized Lattice Towers

- Galvanized Monopoles

- Conductors:

- Conventional overhead power conductors.

- High-temperature conductors (HTC).

- High-temperature low-sag (HTLS) conductors.

Track Record:

- Completed EPC for 34,654 circuit kilometers (CKM) of transmission lines.

- Executed 30,000 CKM of distribution lines as of June 30, 2024.

Manufacturing Facilities:

- Vadodara, Gujarat: Galvanized lattice steel towers.

- Deoli, Maharashtra: Galvanized steel towers.

- Silvassa, Dadra and Nagar Haveli: Two facilities for manufacturing conductors and poles.

2. Civil Construction

This segment contributes 9.33% of total revenue and focuses on specialized civil construction projects.

Services:

- EPC for railway sidings.

- Construction of roads and highways.

- Building construction and industrial structures.

- Pre-engineered buildings.

- Water tanks.

Notable Achievements:

- Constructed some of the tallest natural draft cooling towers (NDCT) in India.

Manufacturing Facilities:

- While this segment relies on engineering and project execution, there are no dedicated manufacturing units explicitly mentioned for civil construction.

3. Poles and Lighting

This segment contributes 4.40% to total revenue and focuses on manufacturing and supplying a wide range of poles and related products.

Products:

- Transmission and telecom towers.

- Monopoles and high masts.

- Street lighting poles.

- Decorative poles.

- Flag masts.

- Traffic lights.

- Signages.

Recent Developments:

- Expanded their facility to include a dedicated unit for manufacturing signages.

Manufacturing Facilities:

- Silvassa, Dadra and Nagar Haveli: Two dedicated units for poles and conductors.

4. Railways

This segment focuses on the Indian market and contributes 2.43% to total revenue.

Services:

- EPC services for railway electrification projects.

- Supply and installation of Overhead Equipment (OHE) structures.

Where do they get machinery from?

![]()

Are they equipped with the necessary certifications to qualify for bidding on projects?

New products under development:

Proceeds from IPO:

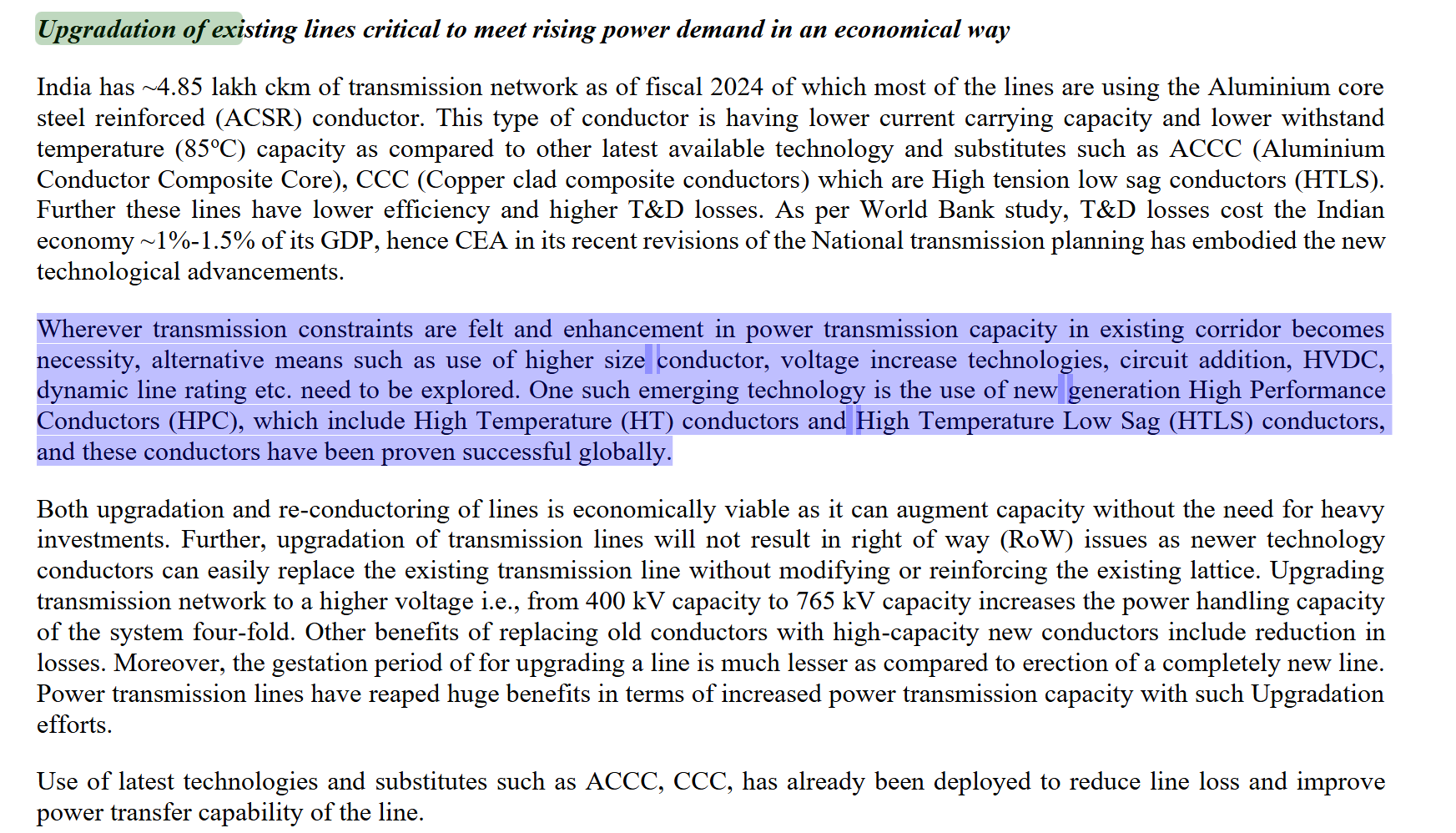

Transrail intends to utilize ₹907.25 million from the net proceeds of its Initial Public Offering (IPO) to fund capital expenditure projects. These projects encompass the enhancement of manufacturing capacity, specifically for high-temperature, low-sag (HTLS) conductors. The company also aims to invest in transmission stringing equipment to bolster on-site construction activities.

Upgrading conductors is more economical than building new transmission towers as it increases capacity without requiring additional infrastructure, avoiding high costs and right-of-way issues.

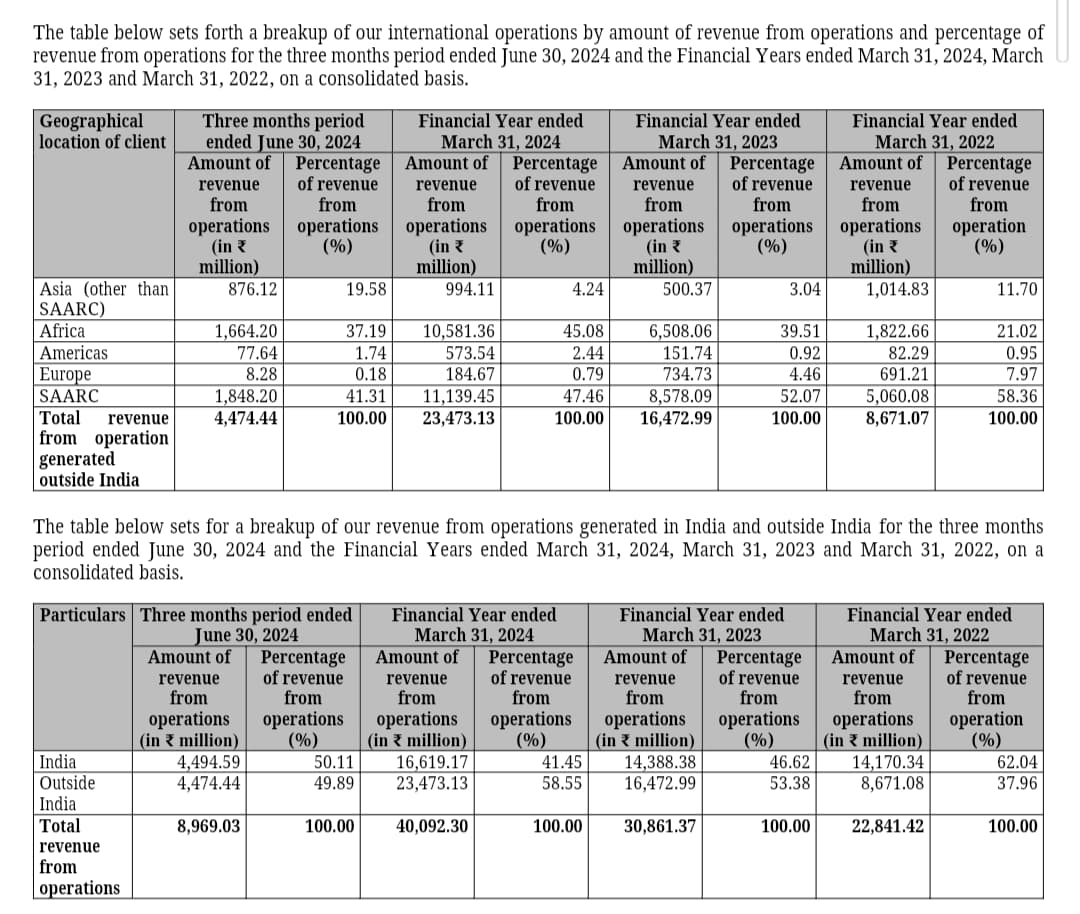

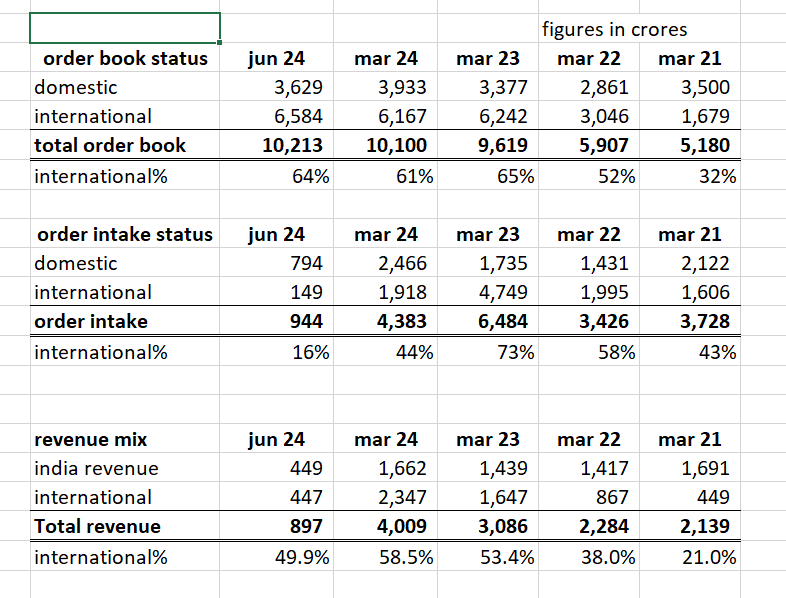

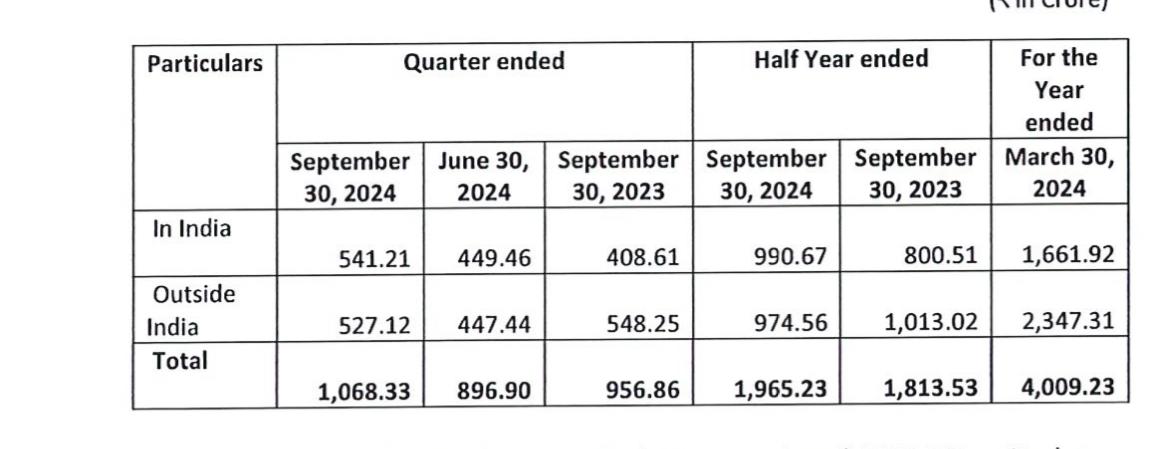

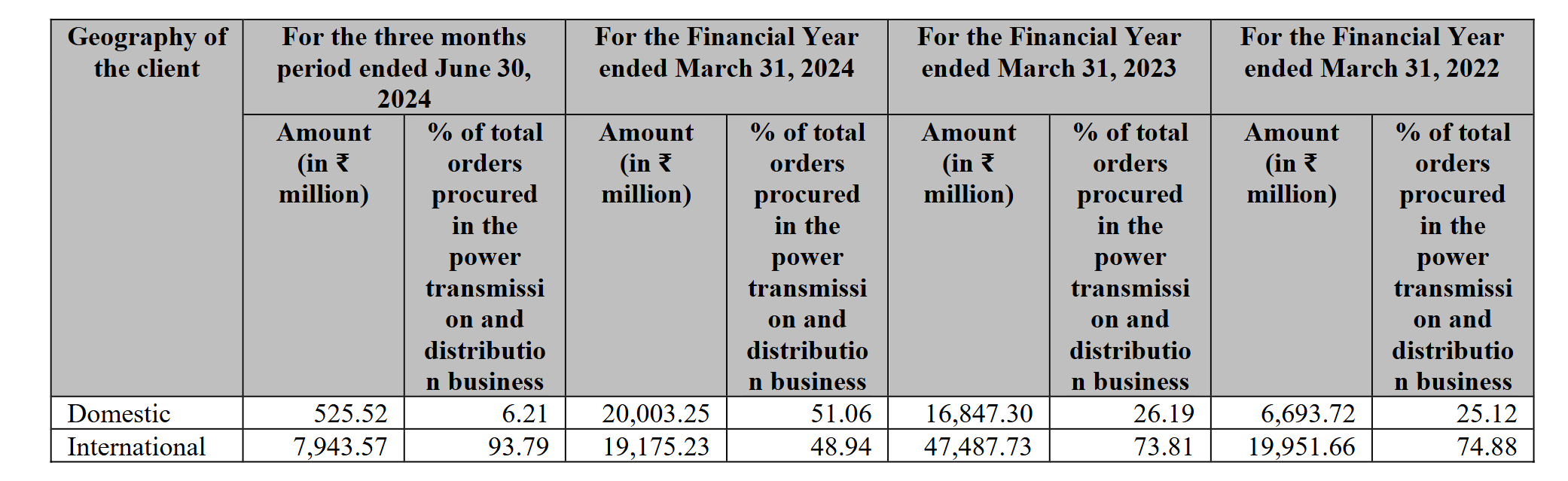

Revenue Mix:

The international revenue mix has seen a significant increase starting from Q1 FY25.

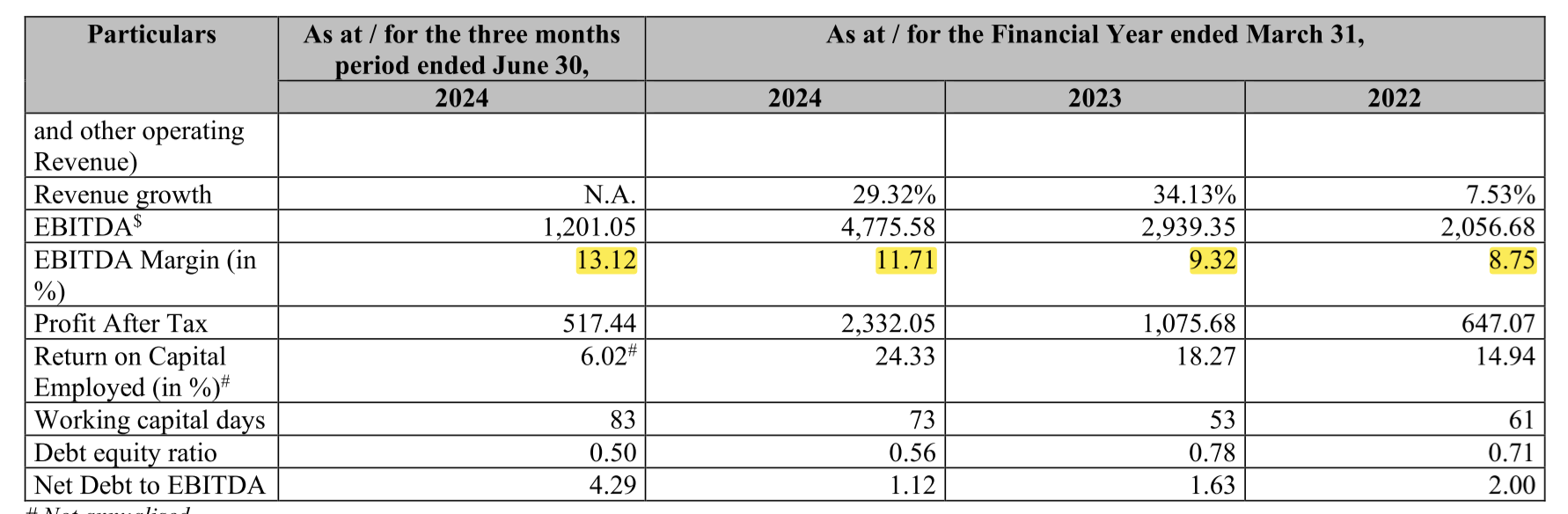

Margins:

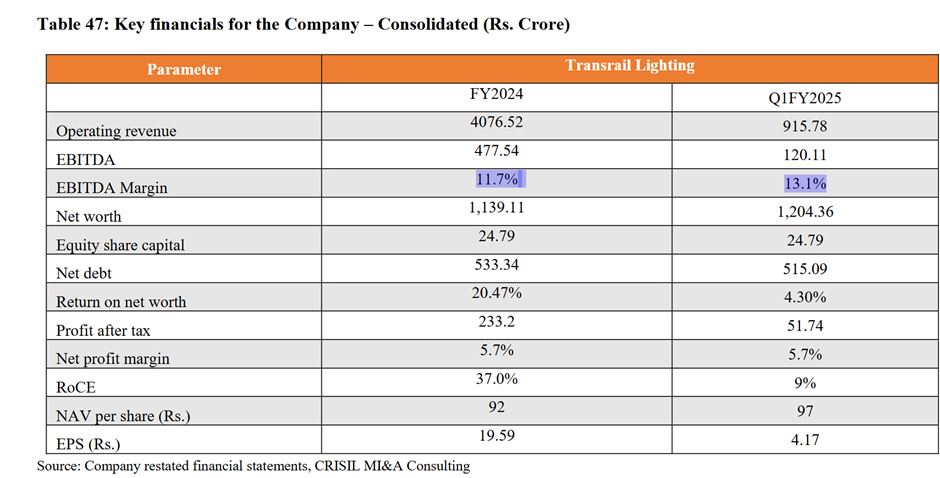

Transrail has managed to increase margins from 11.7% in FY24 to 13.1% in H1FY25 which is the best in T&D sector and this is due to high margin international projects which have higher margin.

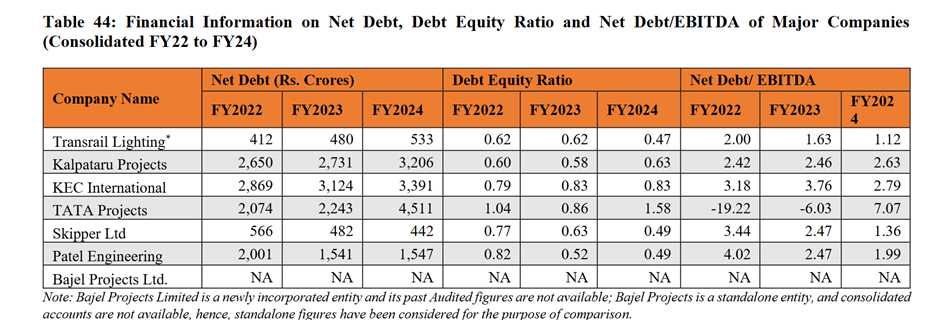

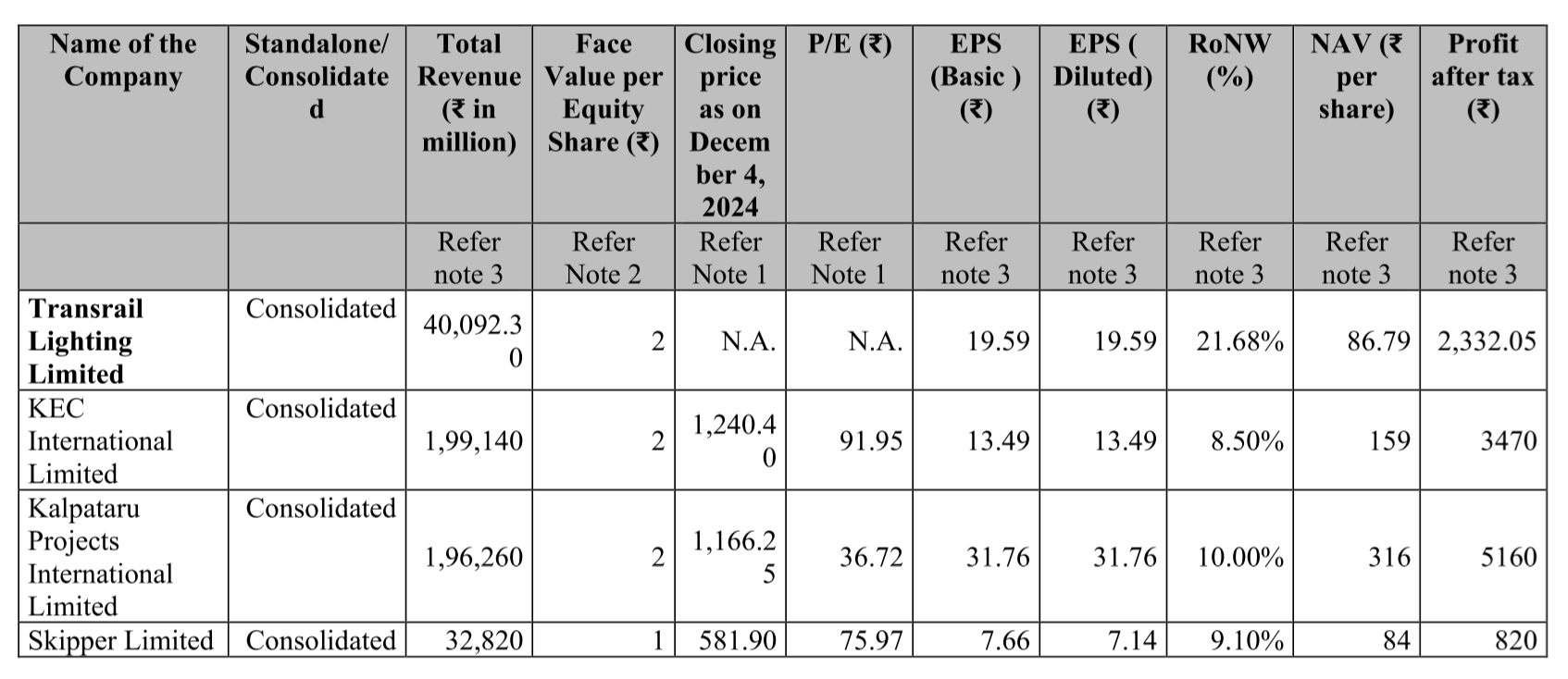

Skipper, a key player in the T&D sector, claims to be the lowest-cost producer in this domain due to its backward integration and has guided for EBITDA margins of 10.5%. This raises concerns about the sustainability of Transrail’s current margins in the long term, especially since the RHP does not provide a detailed margin breakdown across business segments, making it challenging to identify their exact competitive advantage behind achieving higher margins.

Summary of Risks mentioned in DRHP:

Awarded projects can be cancelled/terminated:

EPC contracts have long execution cycles:

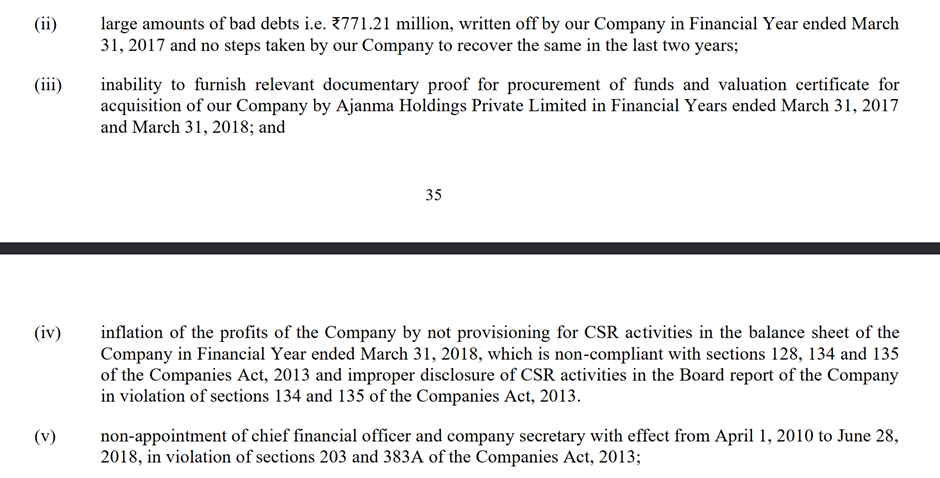

History of non-compliance:

Critical Legal and Regulatory Exposures with Potential Material Impact:

Various criminal litigations and tax proceedings against the company:

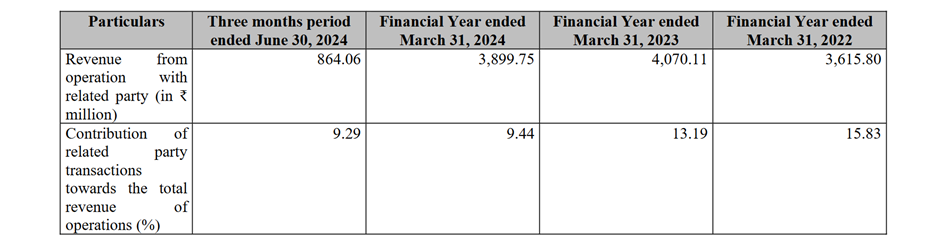

Related party transactions:

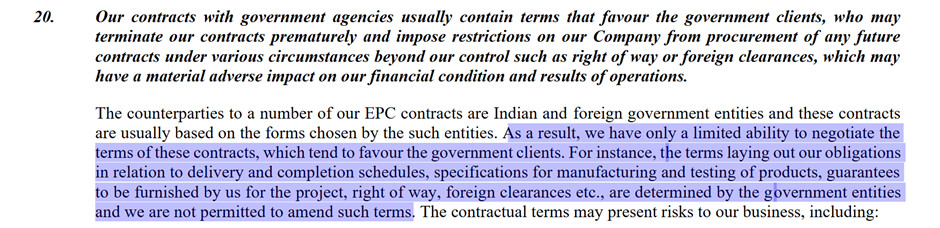

Risk in government tenders:

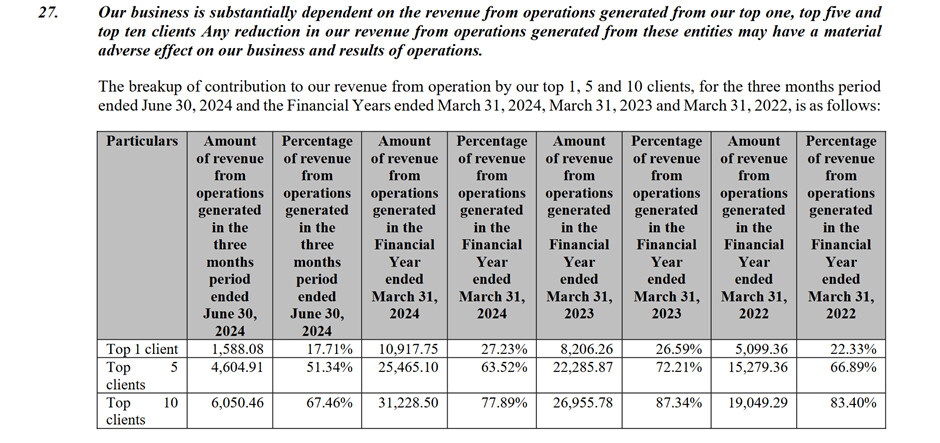

Client concentration risk:

Transrail has the best margins and return ratios in the T&D sector but it has tons of red flags.

Disclosure: Allocated shares in the IPO and planning to exit shortly