Company won new order of 2752 cr!

5 Likes

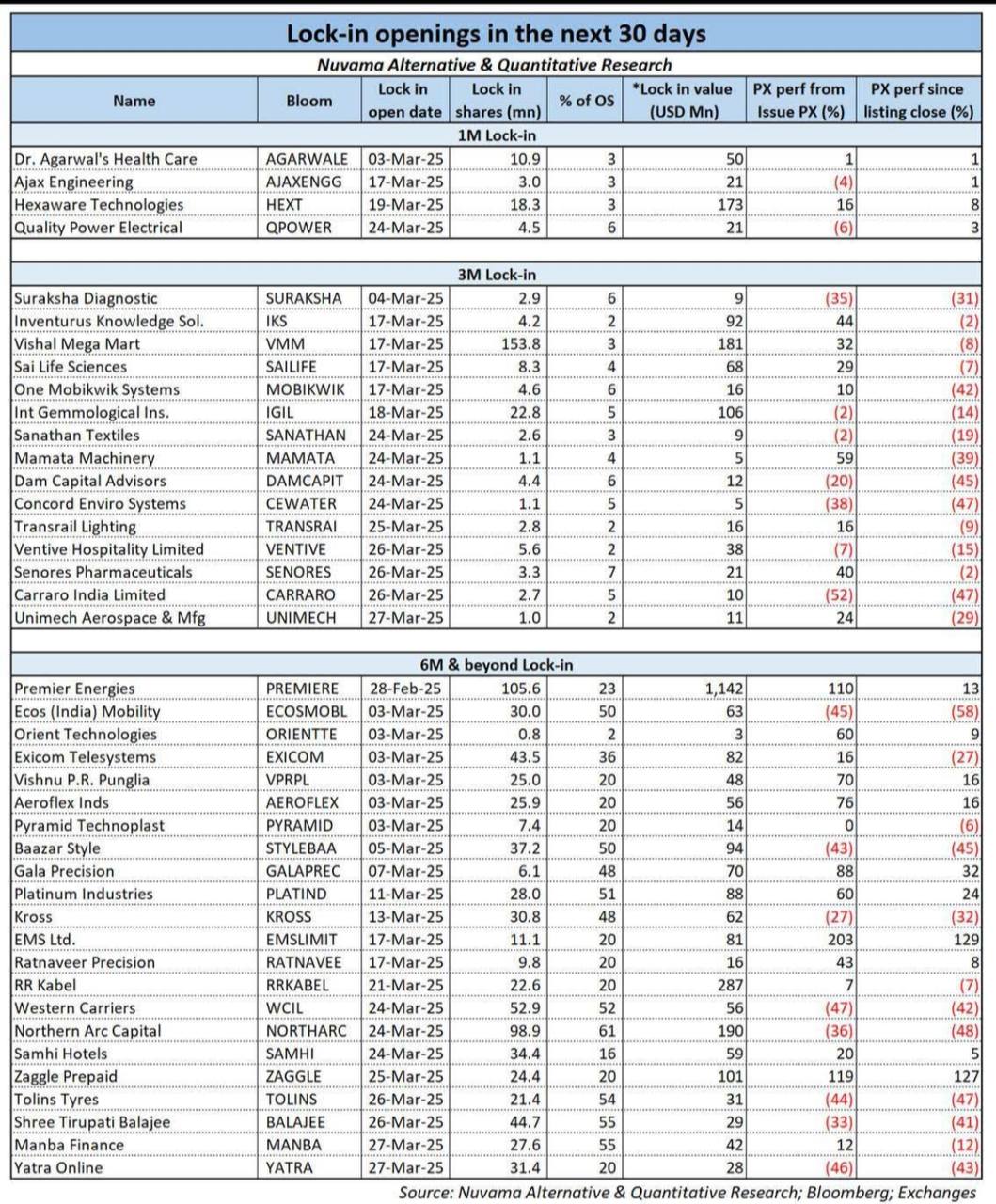

@rankamoksh - can you share how did you get this doc ? I understand the source is Nuvama Alternative research but from where to get it?

Sir I didn’t understand what is this showing?

@sanni_kumar promoters generally have a lock in after IPO, post lock in expiry the are allowed to sell their shares.

@prabal_jain This was forwarded by a friend, I think you can find this on twitter.

Although it has been regularly sharing updates about the order wins of big figures, but i had written 2 times to investor relation regarding details about the order wins but no update received from their side. and secondly, if the future looks so gloomy why are the insiders selling.

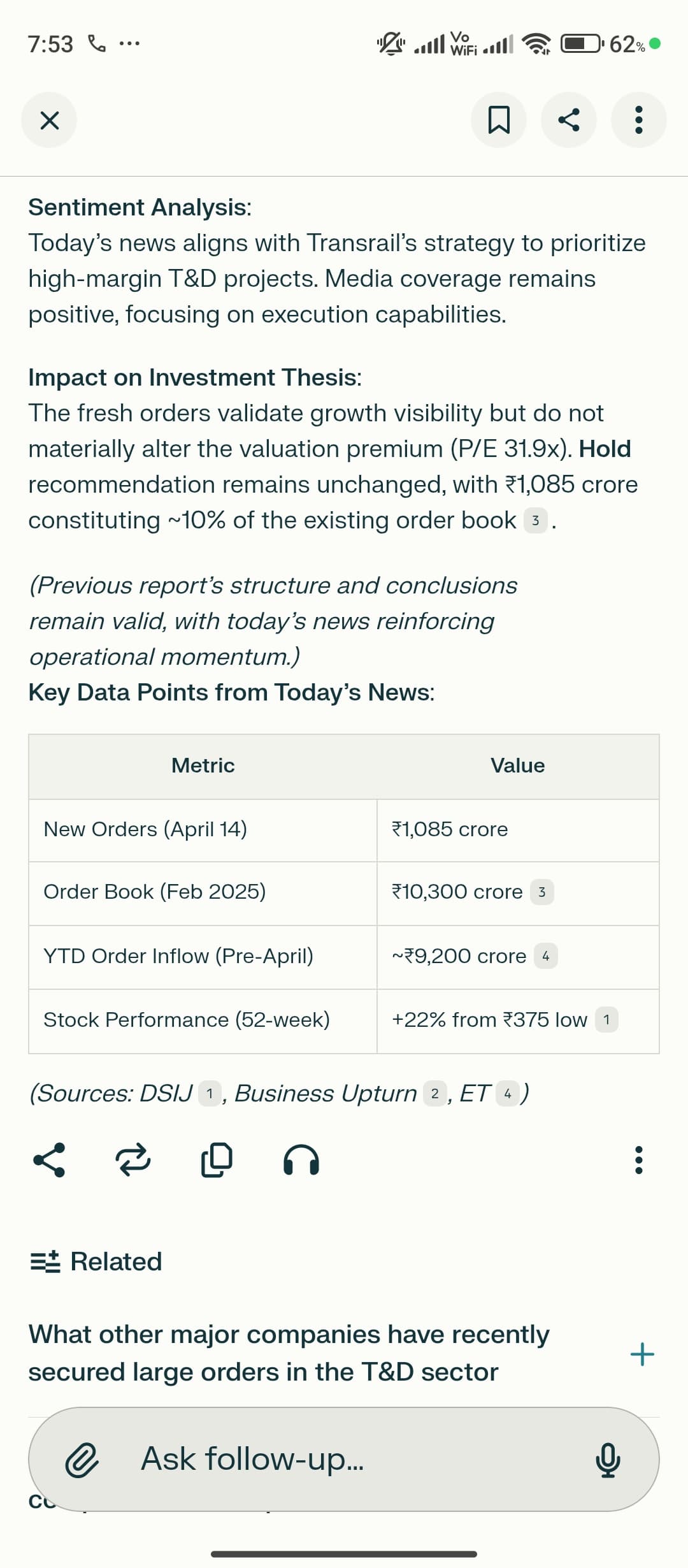

In last few days itself it has disclosed order wins of around Rs.4,399 Cr, but yet the market isn’t rewarding it. either someone knows more than us, or market is being irrational.

7 Likes

Transrail Lighting | Management Interview

-

Company has secured orders worth Rs 1647 crore this quarter, contributing to an overall order book of approximately Rs 15,000 crore.

-

Total orders for the quarter stand at Rs 4000 crore, with the company projecting 28-30% revenue growth for FY25.

Watch the interview

2 Likes

3 Likes

A few things worth noting about the business is:

Just comparing it with peers such as Kalpataru, KEC, Skipper etc the trade payables is higher by about 100 days (>3 months) and also if you look at the interest costs vis a vis the borrowings on the B/S the borrowings on the B/S is about 600 Cr on that the Int cost is about 200Cr and the company is guiding the COD ~ 11-12% so this high diff in interest cost and the very much higher payable days indicates that the company is doing reverse factoring which is leading to such high interest cost on such low debt.

Also coming to the growth prospects- The kind of growth the co is guiding for is the same growth other players are reporting in this segment so that might not be a concern achieving this growth, the concern that might be is what happens to the growth beyond next 3 years? will similar kind of growth sustain post the next 3 years? I doubt so.

Discussion on Valuations: If you compare it with peers you would argue that it’s trading at a cheaper earnings multiple. But there’s a very good reason for that I feel. See the other players mentioned above have a mix of various businesses ranging from T&D, Data Centers, Railways, Oil & Gas etc etc and some of these segments are growing at a much faster clip and although the other players like Skipper are guiding for similar growth it is quite evident that their actual growth will easily surpass their guidance and hence the premium valuations they trade at. So we can’t just extend their valuations to a pure play T&D business like Transrail.

In conclusion I feel that the company is fairly priced at these valuations and any upside re-rating feels bleak.

I also doubt that the business would stay at these valuations if we don’t get a clarity on the kind of growth rates beyong FY’28-29.

Disclosure: Not Invested!

5 Likes

The T&D sector is currently undergoing major tailwinds, Skipper management in their concall mentioned how they’ve barely scratched the surface and hence see a huge runway for the next 10-15 years. So growth might not just sustain but even surpass the 20% guidance that these companies are giving after three years.

Transrail operates in multiple business domains including railways, T&D, renewables and infrastructure. Rerating, while not certain, is quite possible.

6 Likes