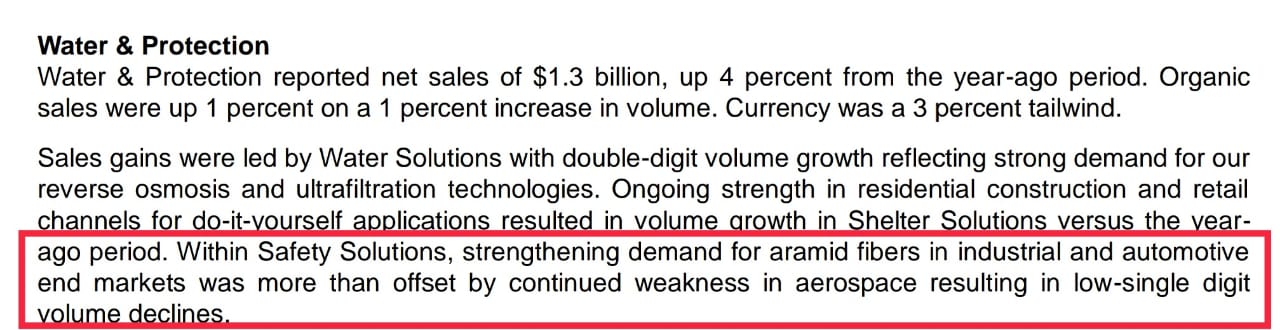

Transpek Industries Conference call 1 March 2021

Opening Remarks:

The company started its operation in 1960s, diversify in Chemical business in 1970s. Developed process for Chrlorination. The company has developed specialty in dealing two hazardous chemical, Sulphur and Chlorine. Polymer, Pharma, Paint/Pigment, Agrochemical are major end use of products manufactured by the company.

Polymer business details

The recent growth in last 2 years, has been driven by long term supply contract which company entered with MNC Chemical Company. The company supply a monomer to customer. Customer converts this monomer which is heat resistance/ fire resistance property. Such polymer are also of light weight and high strength and find their application in Aerospace, Defense and Automobile. While margin for polymer business (specifically in long term contract) are comparable to other products, the long term contract in past provided very large volume to the company which resulted in improvement in overall performance.

With Covid heating the global market, Aerospace and Automobile (polymer mainly in used in high end luxury/racing car in Break plate and Clutch Plate) adversely affected. Further, expenditure in defense sector also got lower priority as compared with large expenditure on healthcare in developed. These factors adversely affected off take of volume of monomer from the company’s end, which also reflected in poor sales and profit margin.

While situation is improving and volume off take is also increasing during December 2020 quarter, the management find it difficult to project when the volume would reach to pre-Covid levels. Having said that, they are reasonably sure that sector (Aramic fiber, broad segment of polymer which is was monomer of the company cater to, is expected to grow at 10% p.a. in volume till 2027 as per published reports) Hence, the question is more of when the demand would reach and exceed pre-Covid levels.

Medium term growth prospect

The company is in process to two develop two products in Pharmaceutical intermediate for which are various stage of development. The sample are shared with customer for both the products. However, the process to get order and materialize same in sales would be reasonably long as same also governed by expiry date of final patented formulation. The customer of the company would only be able to manufacture product after patent expiry, while it may tie-up intermediate supply much before the patent expiry date.

The company has total capacity of around 66,000 p.a. including various captive used chemical capacity. Adjusted for captive products, the net capacity would be around 16,000 tpa. In addition, the company also have access to 3 Job work supplier located in same manufacturing complex for which company has entered into Job work arrangement. These three units can provide additional around 12,000 tpa, resulting in total capacity of 28,000 tpa. During April 2020 to January 2021 period, the company utilisation of capacity was around 35%, currently, this utilisation improved further to 60%. Hence, the company does not find any major capex requirement for new products growth. With existing products, the company can achieve around Rs 500-700 Cr sales along with around 15-20% EBITDA margin.

However, there are various discussion with customer for new products/ application of existing product. While many of them are in medium term nature and moderate volume, in case there is major order, then company would evaluate situation and plan for major capex and inform the investor. At this stage, the company does not perceive requirement for major capex.

The company can also launch new products by way of working on product exchange without getting Environment approval. The company is finding increasingly difficult to get EC approval at existing location. However, it continue to take the matter with appropriate government authorities to get EC approval for expansion. Of 100 acres complex, currently only 49 acres land is utilized in manufacturing plant.

Increase diversification

While with new long term contract business, the company able to show major growth in topline and bottom line in past two years, the sales of the company was highly concentrated in polymer business (to extent of 70%). The company now intend to launch new products/application of existing in products in non-polymer application to diversify the end segment. Over next 2-3 years, the management expect, polymer business to account for 45-50% sales as against current level of ~70%. The objective is not to reduce sale of polymer, but to show higher sales growth in non-polymer business to reduce volatility in business.

Arrangement with JVs

The company has into JV agreement with 3 companies which are related parties. These company assist company to manage usage of co-products and by-products usage, which ensure sustainability of manufacturing for Transpek. Transpek Industries pay job work charge on cost plus basis to these JV companies.

Summary of notes:

While polymer business volume growth is resuming, there would be 2-3 quarters time to reach to pre-Covid level. The management is trying to address this slow down by introducing new products in non-polymer segments, specifically in Pharmaceutical. There are no major capex plan during next year for capacity expansion, although there would capex for reconfiguration of capacity for launching new products.

The company is in discussion with various customers for various new products. However, at current stage the company does not see requirement of major capex. In view of above, in my understanding, the company would take at least 6-12 months’ time to reach FY20 performance.3

Disclosure: Transpek Industries is among my core investment in portfolio. My view may be biased due to my investment. I am neither SEBI registered analyst nor recommending any investment decision in the company. There is scope of misinterpretation/ mis-communication from my side while taking note of conference call and reader shall consider that fact while reading this message.