The only problem with Transpek is that they are quite conservative - still no guidance on Capex even when the covid uncertainty is getting reduced

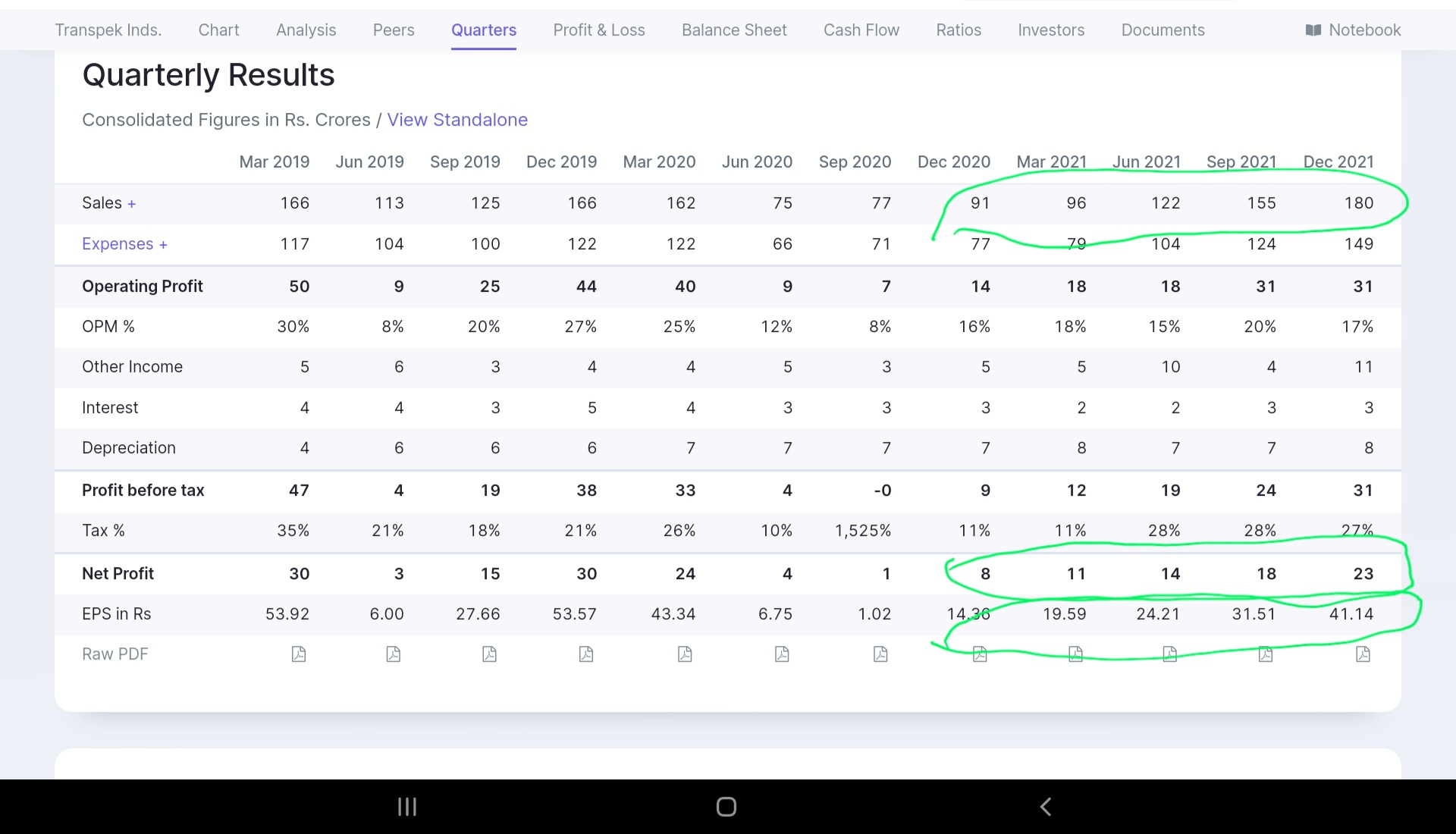

Q2-FY21 result is out and the company continued it’s recovery and reported PAT 17.59 cr- 30% Q-Q growth.

Despite increase in raw material prices hikes, the company has managed to do well. Also most of the airlines across the world are back in air as travel restrictions are lifted across the world, augur well for their main product.

3 Likes

Back to back 3 qtrs improvement, one of very few chemicals companies where QoQ margins have been improving, rightly so as their end client industry are getting back to normalcy.

They have delivered higher end of EBDITA guidance around 20% in Q2 as communicated in Q1 call.

Technical- strong on chart and staying above 50 day moving averages, even in recent pullback in all Chemical stocks.

Although will get to know more details once presentation/call is out for finer details behind good performance, key monitorable

- QoQ performance improvement, this is third quarter - something market likes and hence near all time high prices, can they get past pre corona run rate of 165 cr/qtr+? - aided by new launches as well. High probability.

- Margins are closer to normalcy ( FY 19 and FY 20 being 20%), navigating well amongst RM and overhead volatility - in past they have delivered 25%+ margins when capacities were running high and Qtrly runrate was 165 cr+. Can H2 performance be better than H1?

- Mgmt has in Q1 call indicated peak anual revenue at current capacities around 700 cr( maybe bit more with tolling arrangements) - Q2 they are at 155cr/qtr at 20% margins and having launched new products over last few qtrs as part of derisking - sooner can we expect revival of Capex?

- Performance is supported by better cashflow as well - unlike many small chemicals companies

This one is a good case study of Low expectations and mean reversion when all other chemicals stocks were on fire with high expectations and now correcting. Currently at fair valuations( Q2 annualized 2X sales, 10X EBDITA, 20%+ margins profile, good cashflow) it has potential to deliver a beat of FY 20 base if QoQ trajectory continues, re rating may follow.

Invested

7 Likes

Company has published ppt Q2-FY22 (result was declared sometime back).

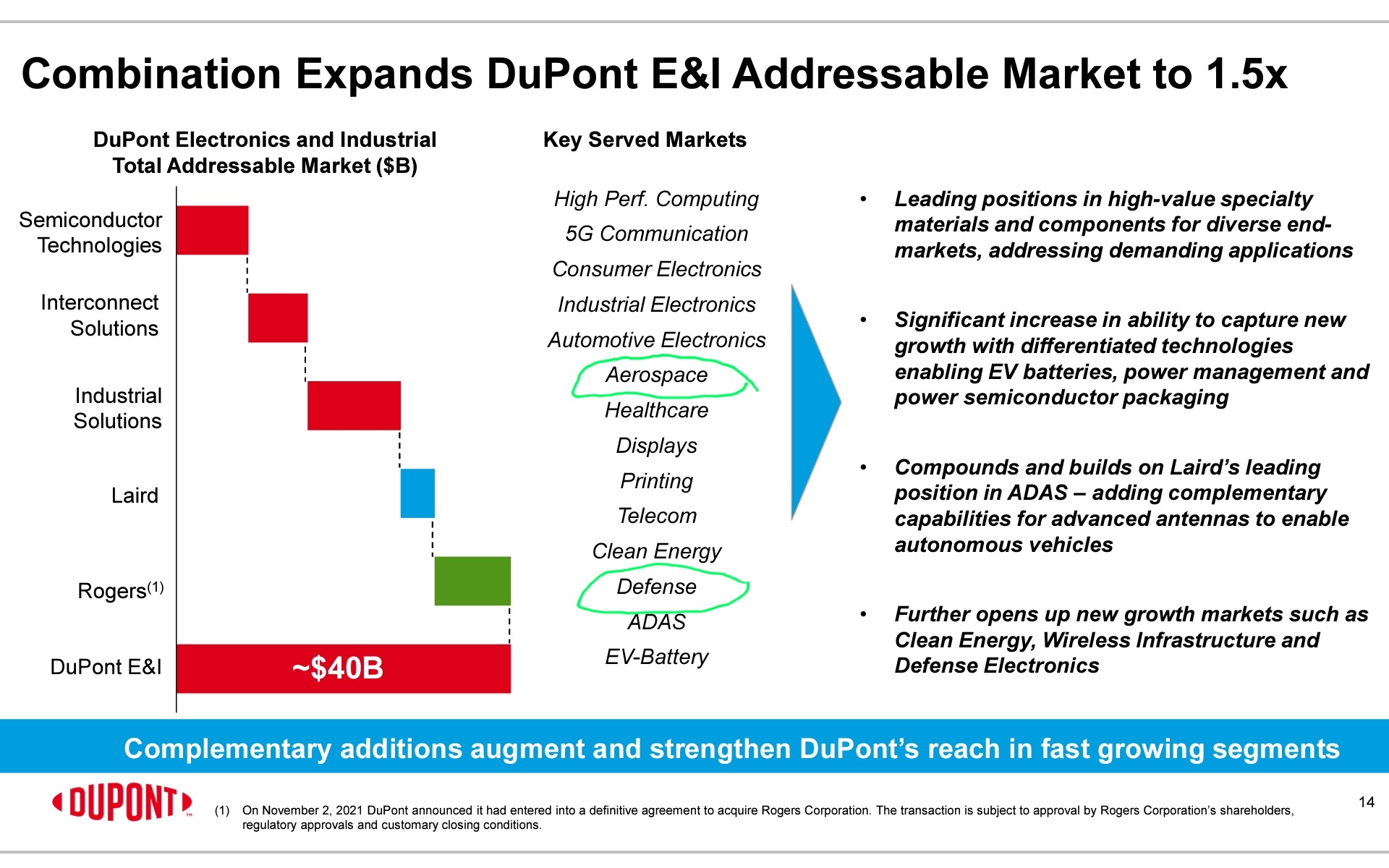

Dupont is selling out some parts of polymers business,

On November 2, 2021, DuPont announced that it has initiated a divestiture process (the “In-Scope M&M Divestiture Process”) related to a substantial portion of its Mobility & Materials segment, (the “In-Scope M&M Businesses”). The outcome of which, including the entry into definitive agreements, is subject to approval of the DuPont Board of Directors

- The businesses that are in-scope for intended divestiture are predominantly those in the Engineering Polymers and Performance Resins lines of business as well as DuPont’s stake in the DuPont Teijin Films joint venture. The in-scope product lines include, but are not limited to, brands such as Hytrel , Vamac , Crastin , Zytel , Delrin , and Tedlar . Combined, these businesses represent approximately USD 4.2 billion in revenue.

Transpek and Dupont collaboration brands scope

Companies like Transpek delivered the same thing at lower cost and as per the available data the business of intermediate was given to Transpek where isophthaloyl chloride and terephthaloyl chloride was to be supplied by Transpek.

- Terephthaloyl Chloride was used by Du-Pont for manufacturing of Kevlar and isophthaloyl chloride is used by Du-Pont for manufacturing of Nomex.

If we put above two together- doesn’t seem that it’s going to affect Transpek scope of brands, infact both the brands Transpek serves to( Kevlar and Nomex) are highlighted as key strategic brands on Dupont site

Here is the Transpek chart - about 25% down from the point of this announcement in first week of Nov - coincidence that all Chemical sector stocks pack did correct from mid October onwards as well( big and small) - though it was linked with subdued margins in Q2 results- which is not the case for Transpek as Q2 was good.

Curious to know if felow VPers has any additional insights/thoughts @dd1474 @paragbharambe ?

Valuations seems to be attractive at 1.8X sales and 9X EBDITA on Q2 annualized basis - of course provided no threat to Dupont contract.

Inested

10 Likes

Thanks for your post and seeking my view. Transpek continue to remain among my top 10 holding, although pre-COVID it was among my Top 3 holding and I have systematically reduced my holding to around 55% of peak level in quantity.

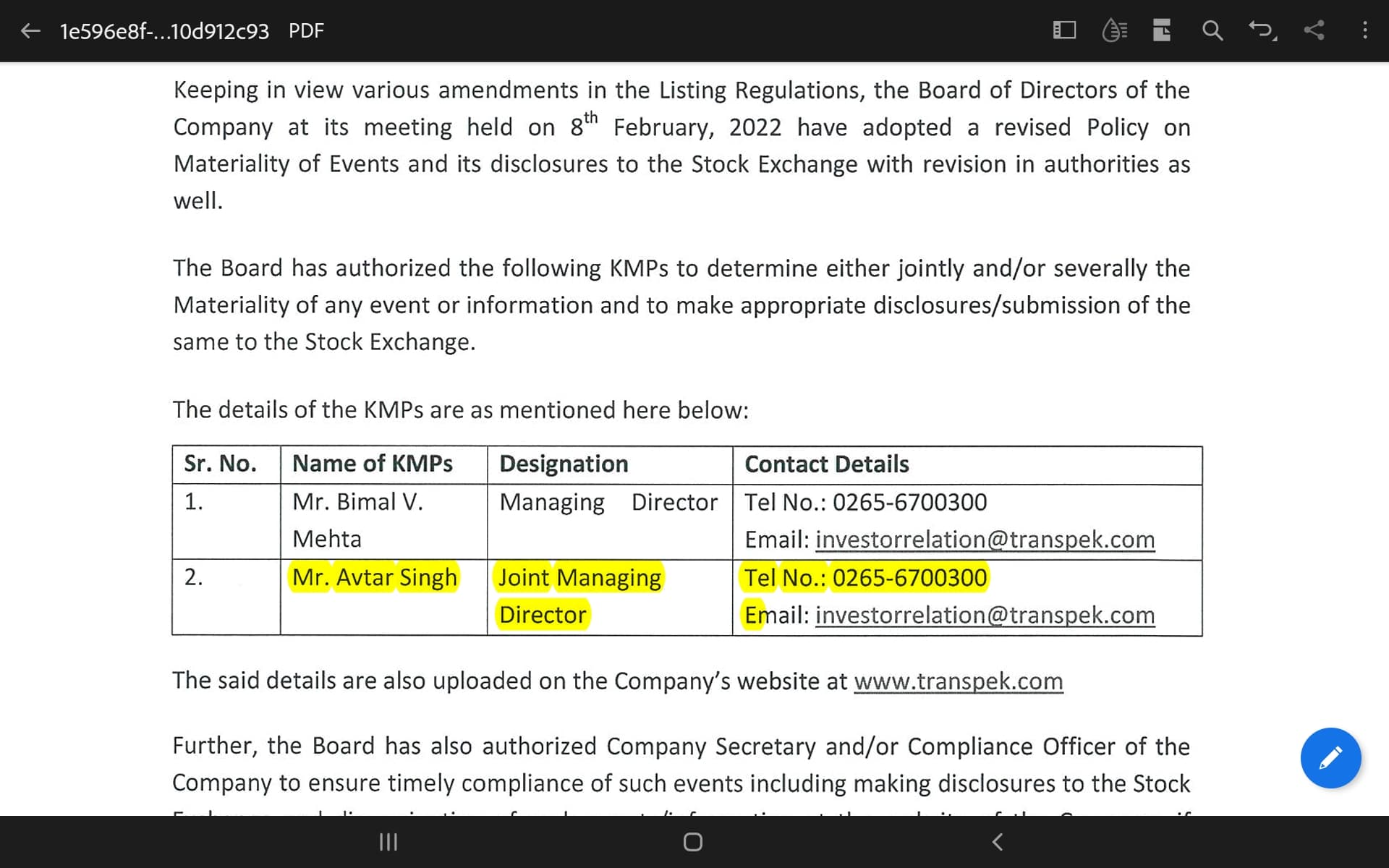

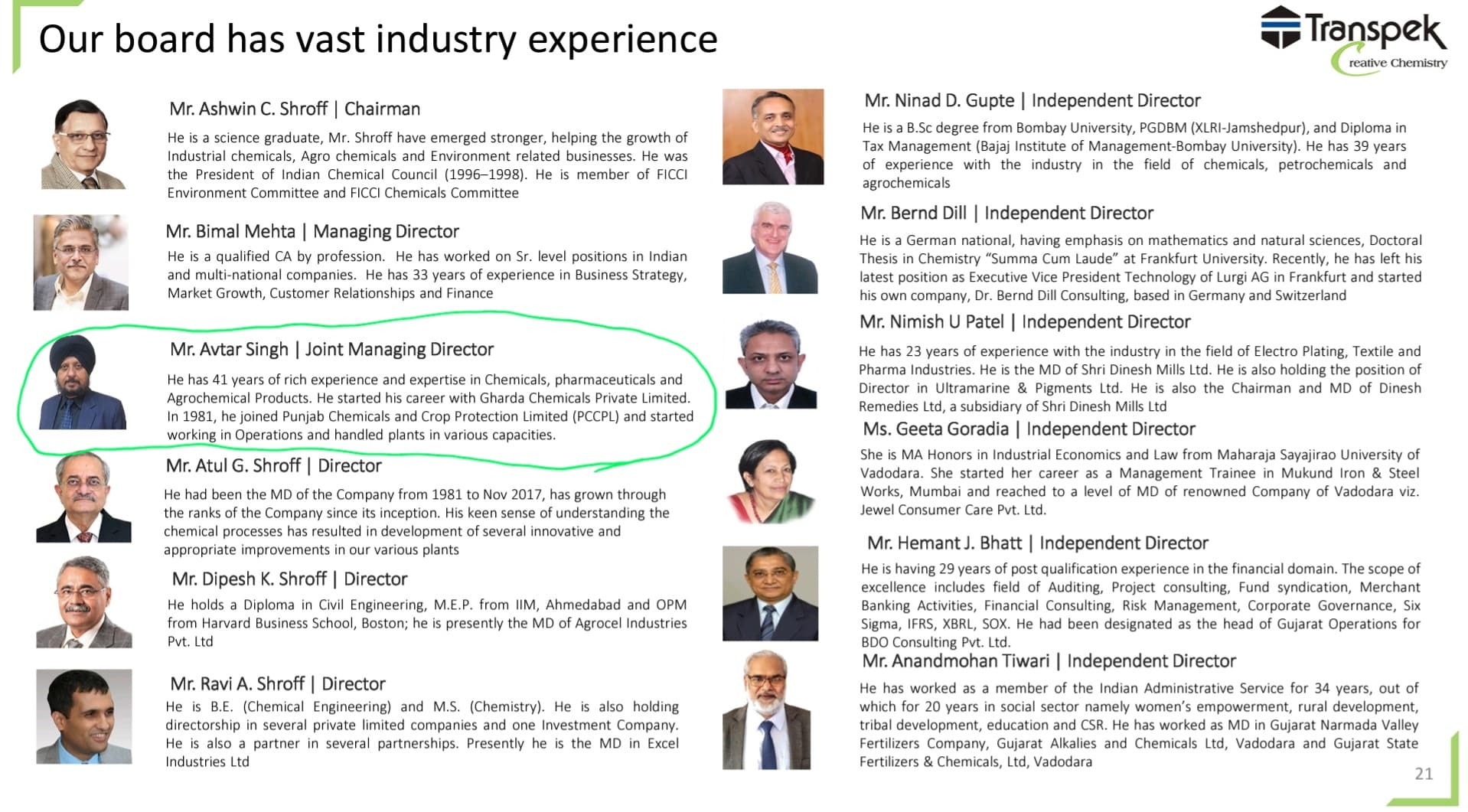

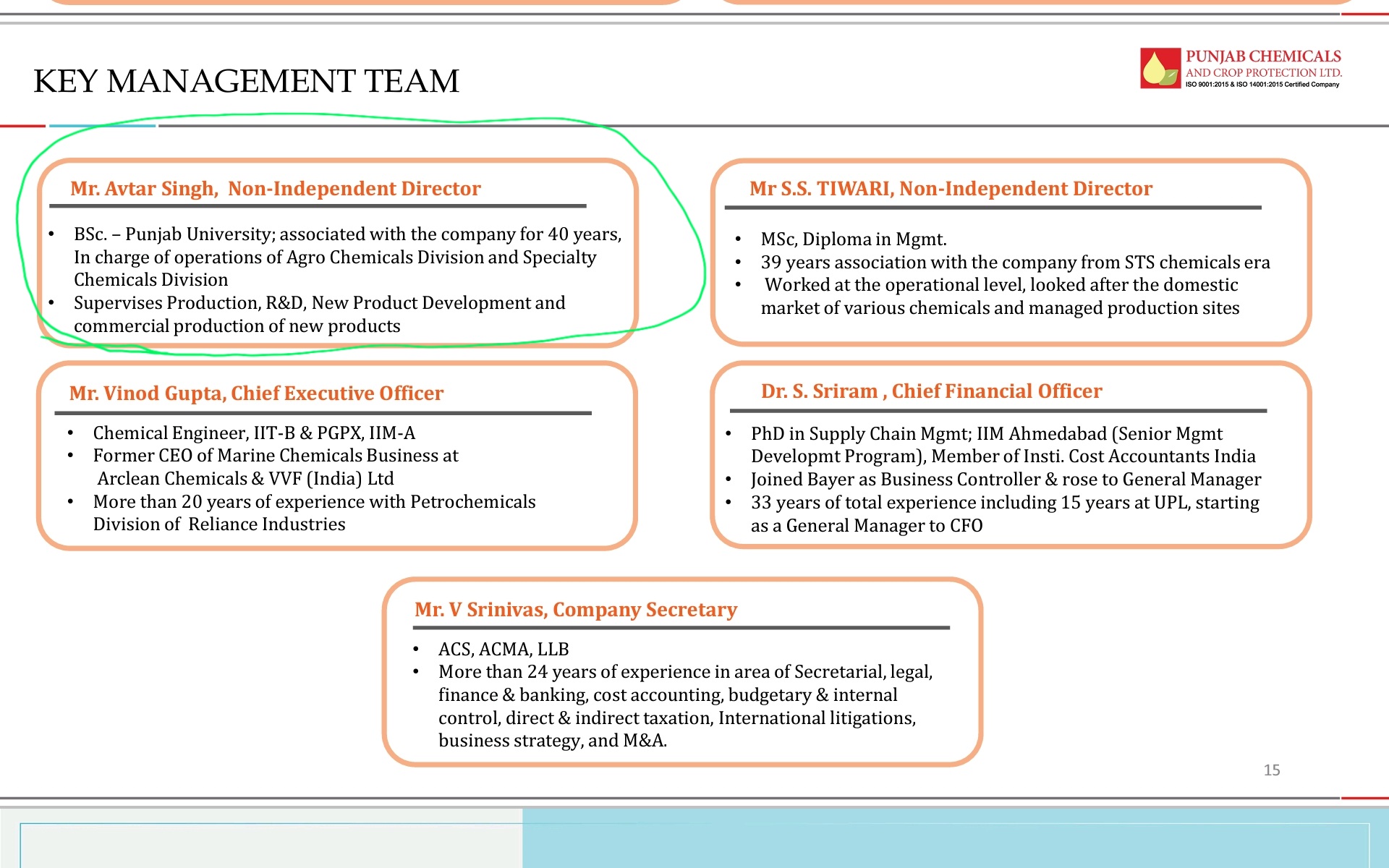

I trust Transpek promoter and Mr. Bimal (MD of the company). However, last quarter or so, Transpek has inducted new Co-MD Mr. Avtar Singh who has also worked for long period with Excel Group promoters.

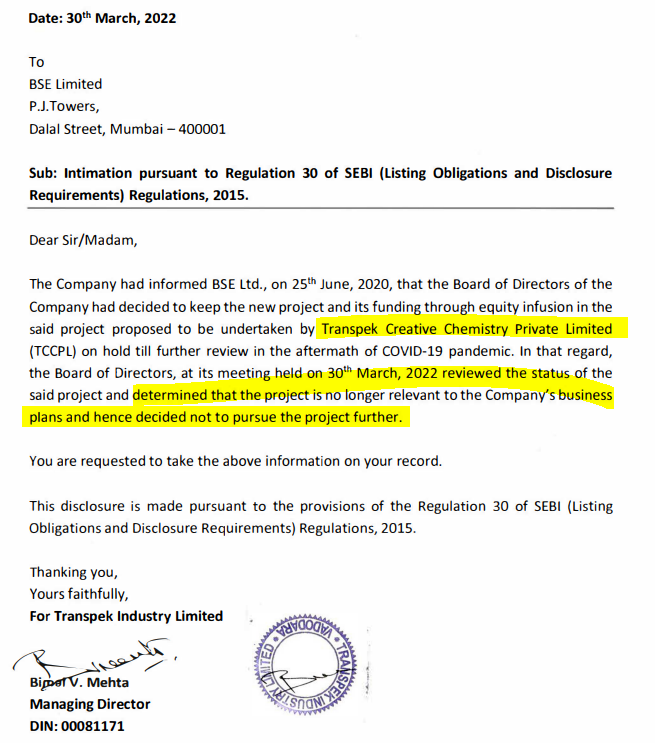

In my limited understanding, Transpek is fairly valued at current level of around 2000-2300 per share. The company has to show some new relationship with clients or new products launches which would provide for future growth. Second factor would be to look at new production capacity as what I understand from various con call and AGM, the company has reached to around optimum level of capacity at current plant. While they have support from group companies capacities which they have been using in past to scale up production, it is high time that they prepare now for new greenfield plant as getting approval from Govt. would also be long process.

Hence, for me, my investment would critically depend on announcement for new capex, new product launches and /or new relationship with reputed clients for next 12-24 months. In case there no new development on these fronts, I may systematically reduce my holding in the company over period.

While it does not answer your specific question, I thought it would be good for me to bring out key moniterable for me in Transpek.

Discl: Not a SEBI registered advisor, Have sold small quantity in last 30 days, Not recommending investment. Have failed multiple times in forecasting future of stock prices and my understanding may be completely wrong .

12 Likes

Thank you @dd1474 , your perspective is quite useful on key monitorable. No point being in microcap if growth ambitions and direction are missing, esp in sector with tailwinds.

- Given FY 20 they did EPS of 130 odd, at Q2 annualized they are in vicinity of same so core biz seems to be on track( heavy lifting by DuPont)

- on Joint MD coming on board, per Q2 deck - He has 41 years of rich experience and expertise in Chemicals, Pharmaceutical and Agrochemical Products. His rich technical experience &

expertise shall be very valuable for the future growth initiatives of the Company - - Looks like future growth Capex may come from newer areas( agchem/pharma) , having learned lessons of client and sector concentration risk in Covid era.

Being a small player few things stand out

- Winning Dupont contract,

- No impact on RM and logistics inflation in H1 22 while every other chemicals company had it

- Agility to identify-pilot and hopefully scale up new chemistries as part of de-risking in short amount of time, joint MD coming on board

Agree with your assessment on tracking growth areas and growth Capex, given capacities should be near full at current run rate.

6 Likes

Thanks @Dev_S for seeking my opinion. Unfortunately, I do not have deep knowledge about Transpeak, but have learned a few things about the company mainly from this forum. I think this thread has wealth of unbiased historic information, which cannot be found anywhere.

I bought into Transpeak last year after the stock corrected to much lower level. My thesis was simple at the time. One of the reasons why company had lower profitability in FY21 was reduction in order size from their largest customer. As per management, it was due to reduction in aircraft related order (e.g Kevlar) for obvious reason that most of the global planes were grounded. So I thought eventually this market will recover and Transpeak will return to normal profitability (“Regression to the mean”), which is what is happening currently.

After listening to con-call and reading what ever is available, I think management seems very conservative or one could say they lack ambition. In the con call, investor community has been asking them for their growth plan, but they are not showing keenness to expand further. One could they are conservative but at the same time, market is throwing the opportunity which they never had so far. Like Deepak Nitrite- which is raising 2000+cr at a high valuation and increasing capacities rapidly, Traspeak has not show then aggression in their act. I think time will tell, how this plays out, but it seems the price has reached it’s fair value based on the available information.

As you have highlighted above, it seems Kevlar (and other products which uses material supplied by Transpeak) is strategic to Dupont. The initial contract is for 10 years out of which 4 have already passed, so we shall see if they had their best days behind or ahead as far as Dupont is concerned.

I know it does not answer your specific question, but I though I can throw some light from a different view point.

4 Likes

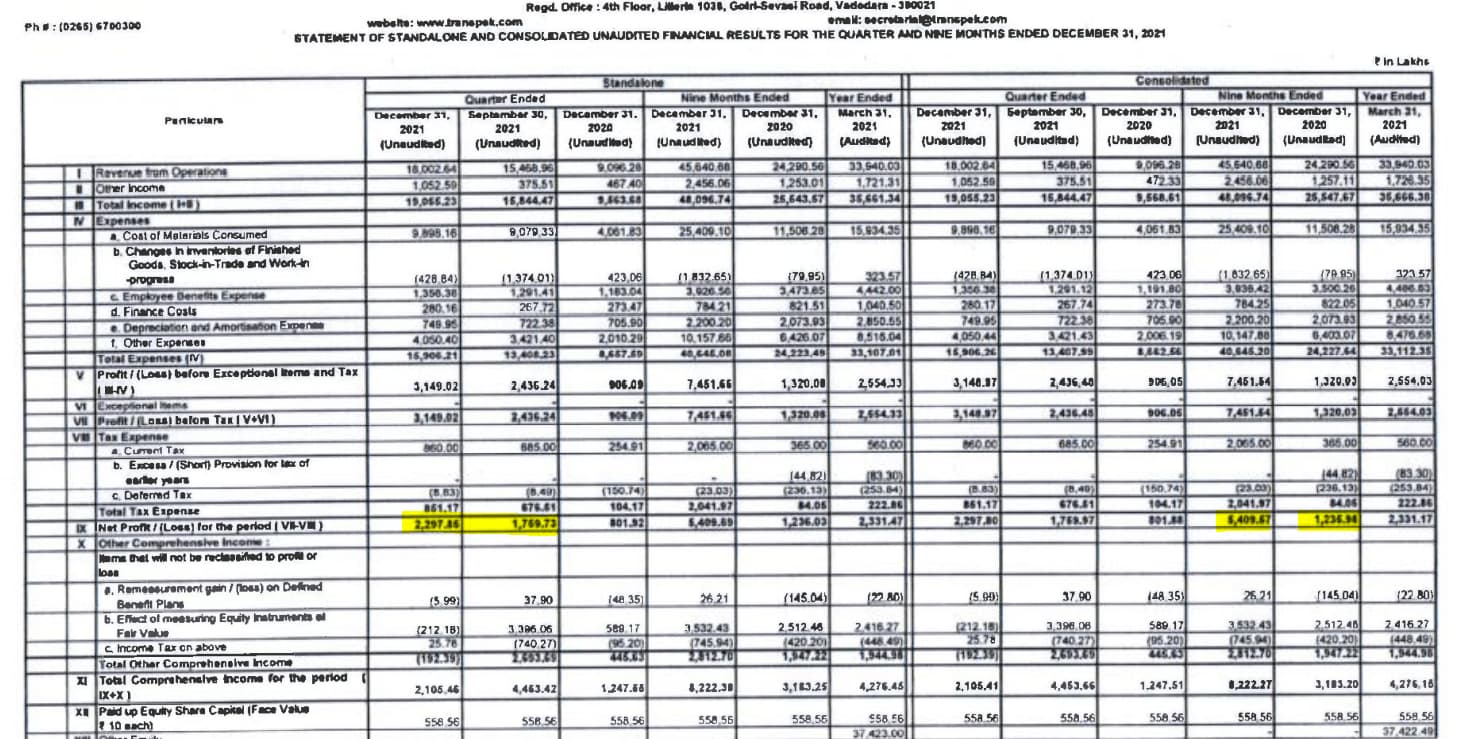

Q3 result is out and company has reported 22.97 cr profit (the press release is not very clear).

3 Likes

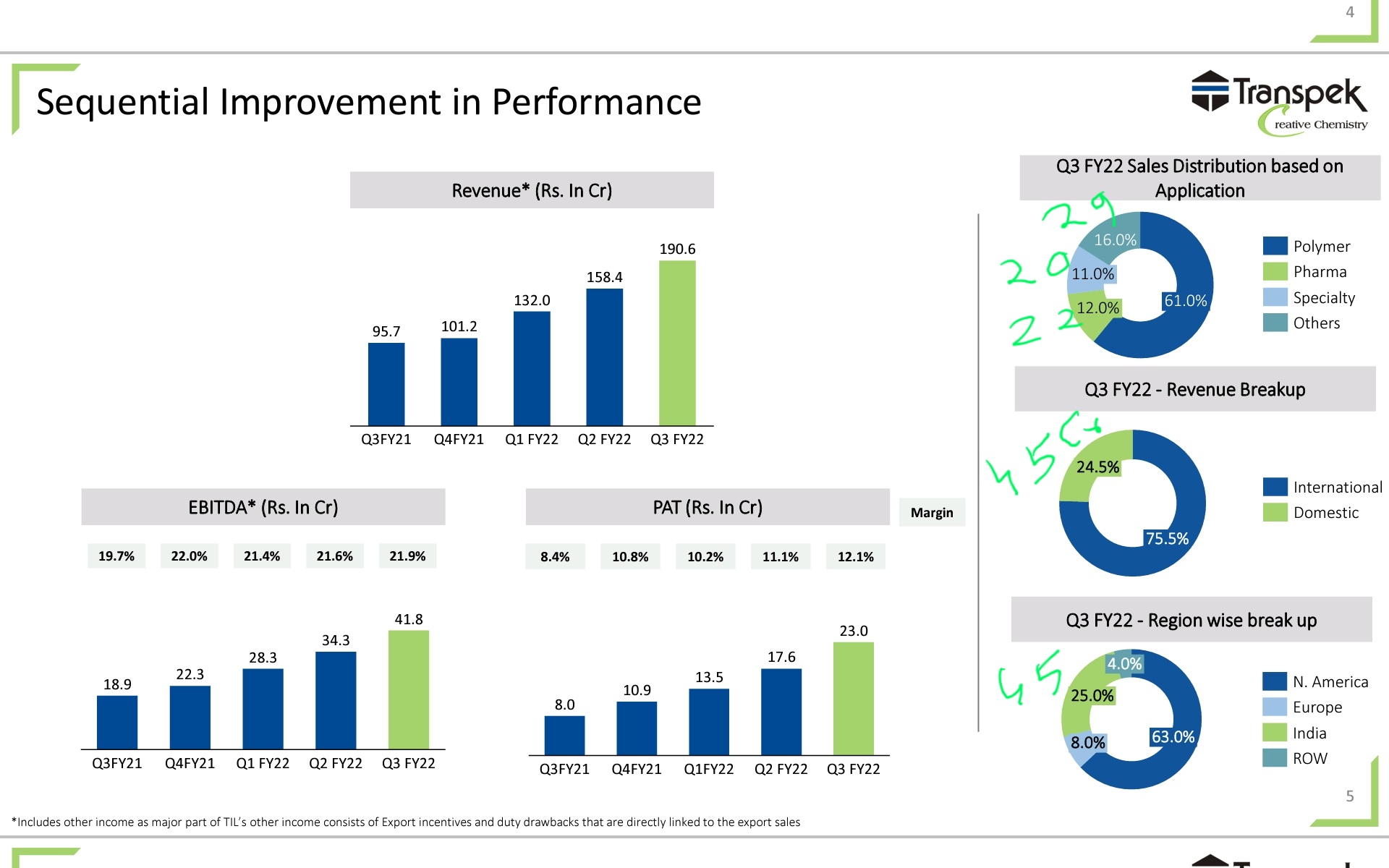

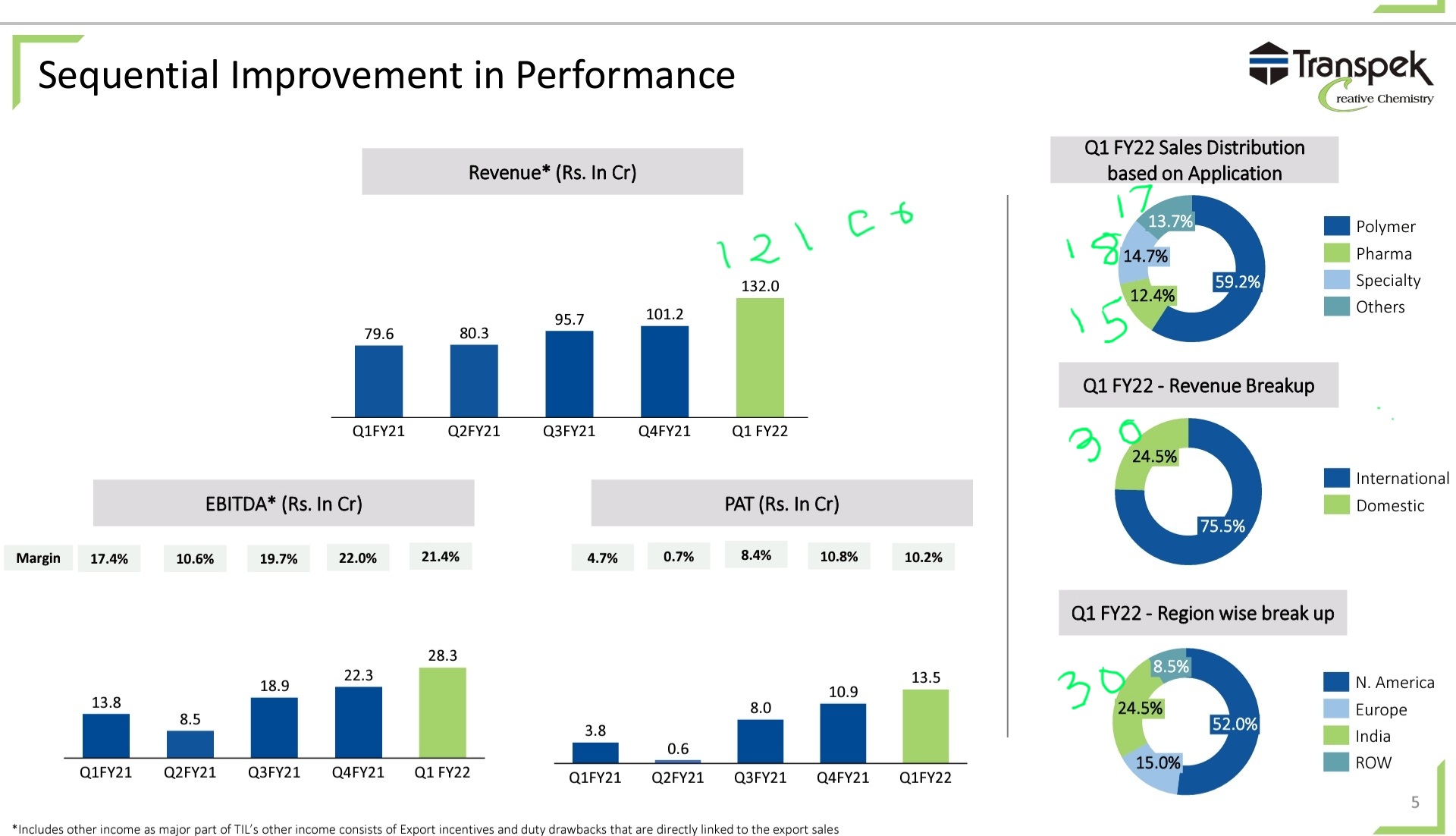

- Indeed good numbers, this is fifth straight quarter of sequential improvement - both topline and bottomline

-

Per Dupont strategy deck for Q3 ( key long term contract), Aerospace and Defence stays as key focus area,

-

One another subtle development is elevation of recen5ly appointed Jt MD per press release( key decision matters) - believe his focus is new products areas( pharma, agchem etc) - precursor to future focus areas?

-

While Q3 revenue are ever highest at 190 cr, op margins are at 17%, however have been much higher in past 20%+( appears partial pass through of cost escalation, higher revenue is likely volume+ value as cost of materials QoQ is 10% up but Rev QoQ growth is 20% type) - hopefully presentation and if concall happens - will give better idea

All in all Q3 annualized is 165+ EPS, 100 cr PAT, scope for margins improvements exists, even at conservative 20 median PE for med term average, fair value can get to 2K cr mkt cap from current 1100 cr.

Key monitorable as @dd1474 and @paragbharambe helped identify is Growth Capex plan and announcement given current capacities close to peak.

13 Likes

2 Likes

We know that Promoter Shroffs family has another listed company connects,( Via Excel crop partnership as well as Salil shroff having stake in both), Other entity being Punjab crop , which has seen very good growth lately in Ag chem CRAMS space.( Agchem sector tail winds with China +1 as well as conscious strategy to focus in CRAMS part of value chain )

- Common Jockey - Wouldn’t it be logical to take a key operations player from Punjab crop and plug into Transpek, leverage synergies and build on common strengths.

- Common product profiles

Thanks to @harsh.beria93 - here is chemistry capabilities profile of Punjab crop

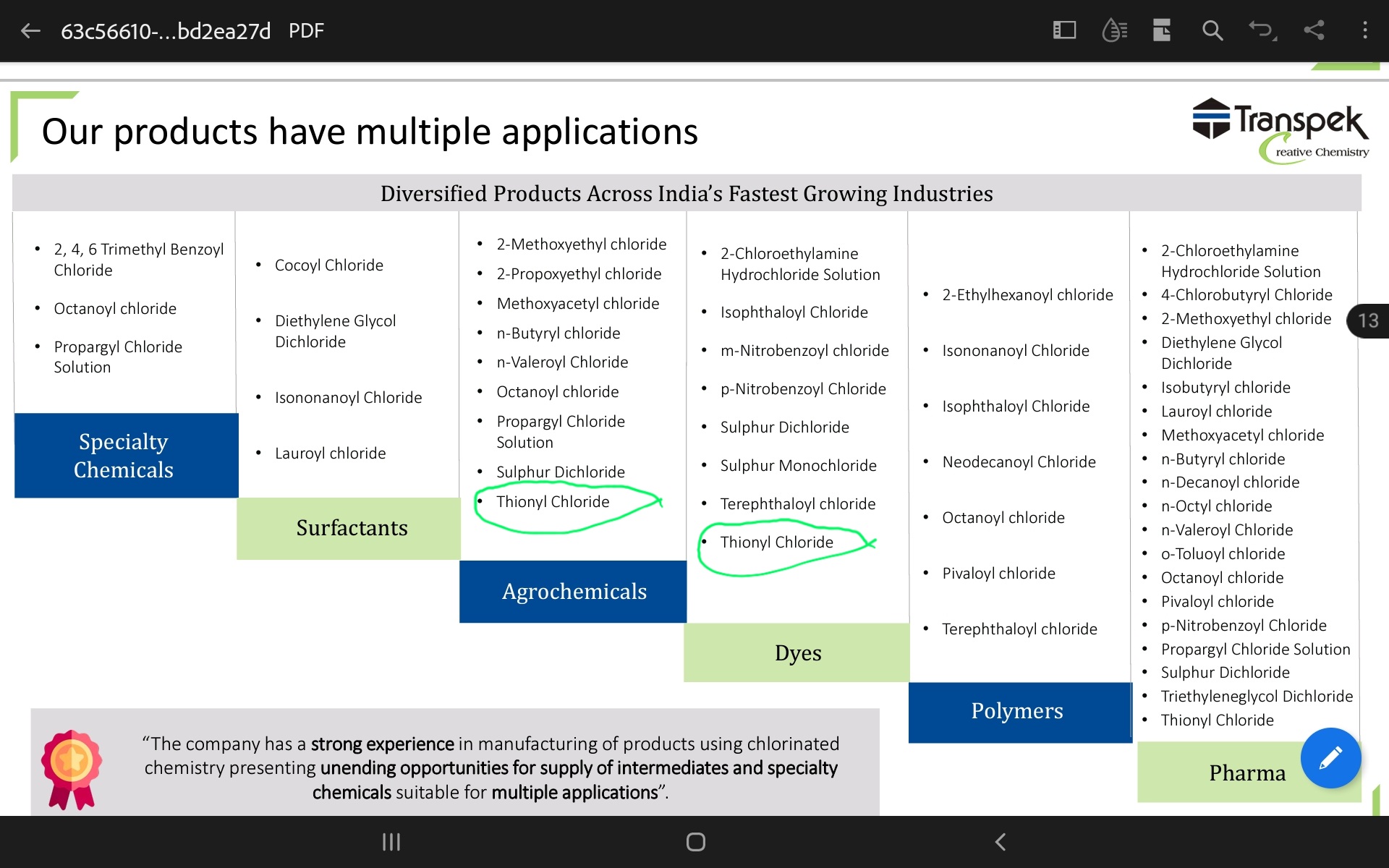

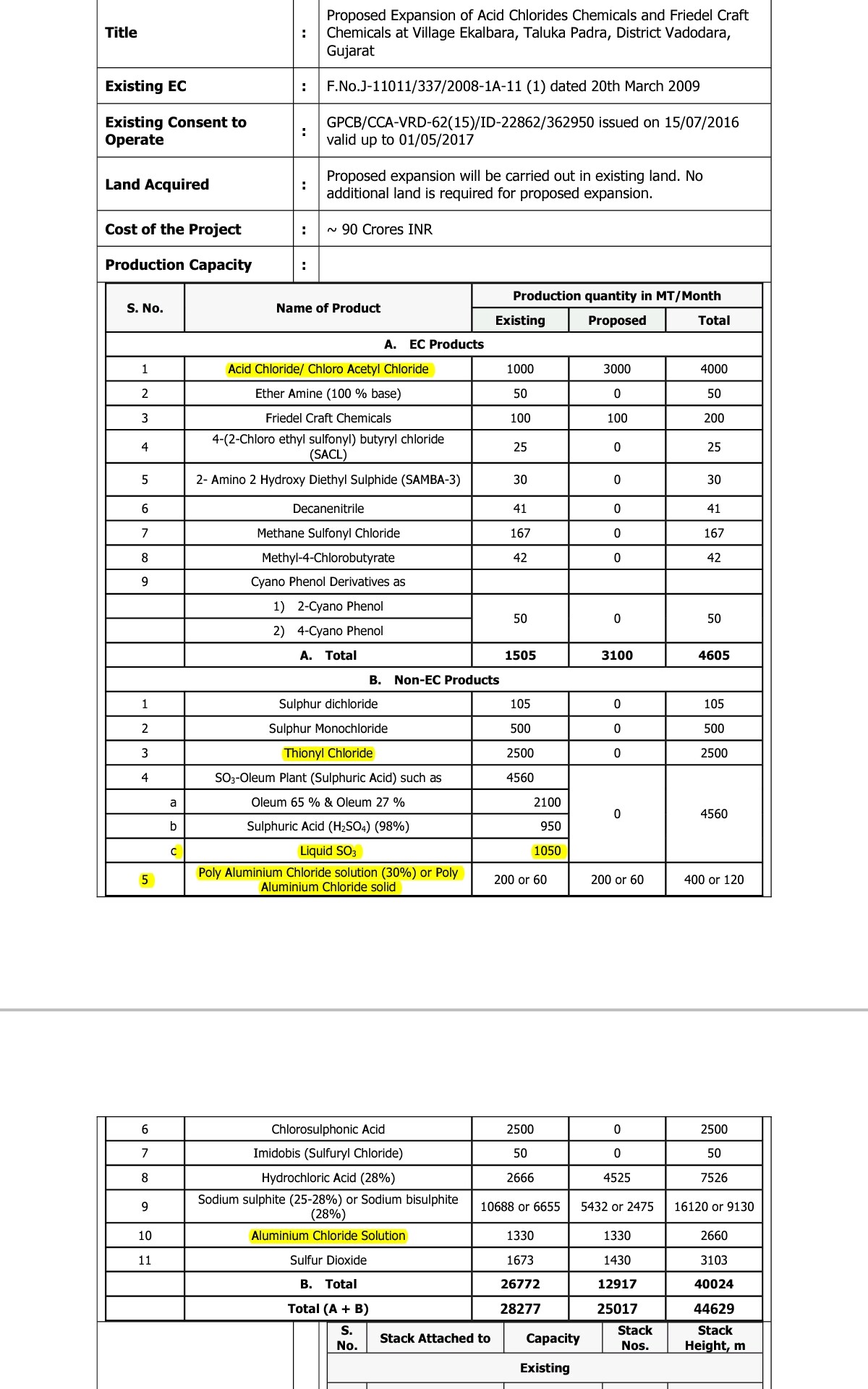

Punjab crop need critical RM( e.g Thionyl Chloride, Aluminum chloride etc ) to deliver expanding basket of molecules. Chlorine is Transpek key capability.

Below from EC of transpek

- Mr Singh sits now on both Companies and a veteran from Punjab Crop, if above hypothesis were to come right, should we see PRODUCT mix of Agchem/Chem & India as growing ? That would mean India contributions going up meaningfully - is this happening over last few qtrs? Note revenue numbers are core ops( not including other income)

Q3 22( 180 cr revenue, international 135cr, India 45 cr)

Q2 22 (154 cr rev,international 120 cr, 34 cr India)

Since no presentation in Q2, numbers are derived with 9M - ( Q1+Q2)

Q1 22 ( 121 cr, International 81 cr, 30 cr India)

Summary

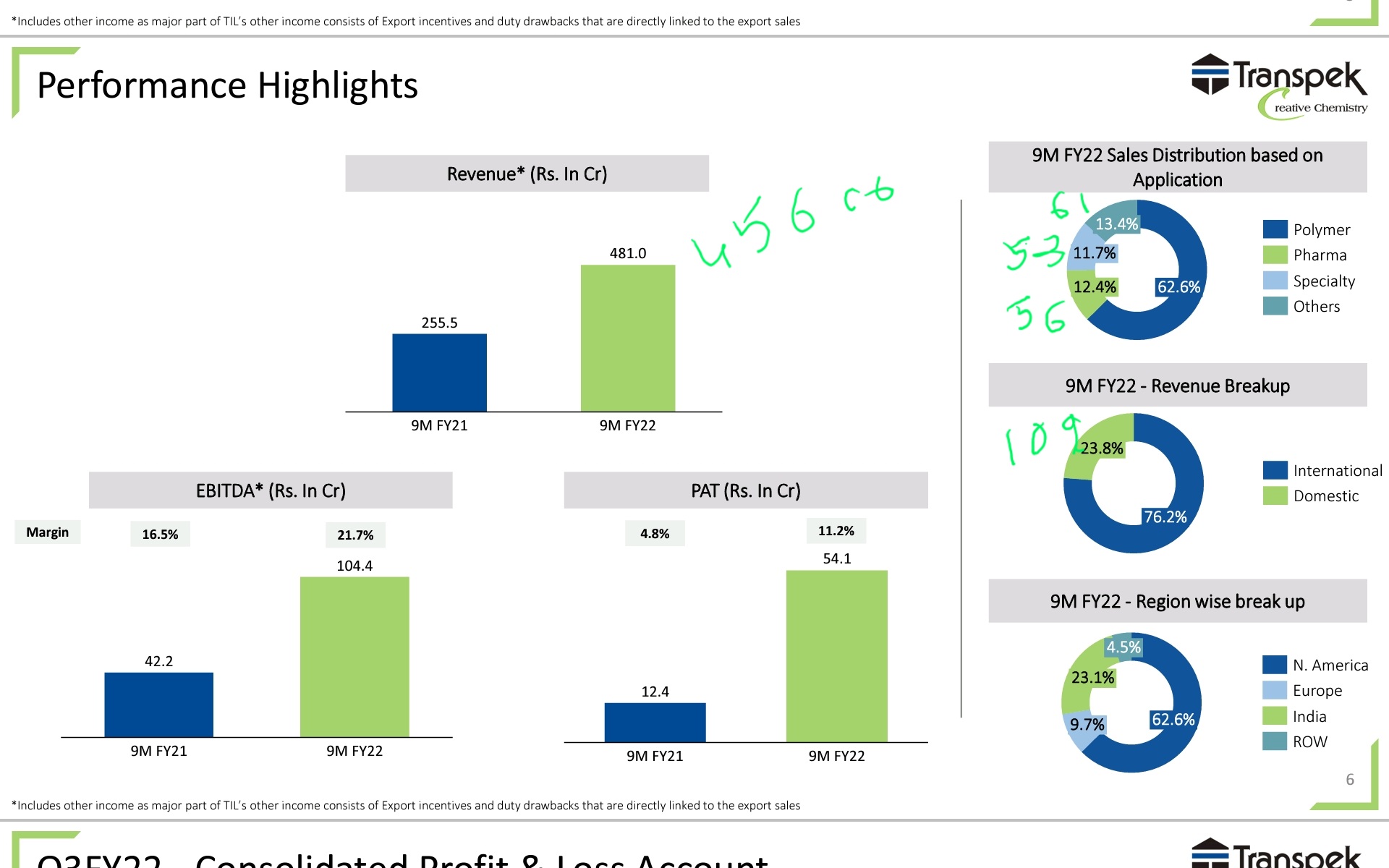

- Seems to be trend of healthy pick up in India / domestic being 25% of revenue for all periods ( 109 cr at 9Mo)

- Specialty - Q1 at 18 cr, Q2 at 15 cr , Q3 at 20 cr

- Others - Q1 at 17 cr, Q2 at 15 cr , Q3 at 29 cr

- Pharma - Q1 at 15 cr, Q2 at 19 cr, Q3 at 22 cr

Too early to conclude a secular trend, but visible signs of India contributions high at 25% inspite of full ramp up in Dupont.

- Growth Capex has been a missing point here - some call outs in Q3 deck - need to understand more in concall

Some questions that may help understand future trajectory better

- Agchem - does it tie to Others as category in presentation? Is it primarily driven by India geo? How do we see this over next few years.

- current utilization and Production capacity increase - is it happening as brownfield and how much additional throughput and revenue potential? Which area - Agchem/pharma/ Others? Also in past mhmt alluded to switch products and use current production- is this the case?

- Full scale runrate of Dupont contract?

- Geo mix few years out? Is domestic margins similar profile as global?

11 Likes

A little titbit:

The promoter entity also hold about 17% stake in TANFAC Industries, which got recently acquired by Anupam Rasayan.

It appears promoters have built up stakes in different companies catering to different chemestries as TANFAC is into Fluoride.

Regards

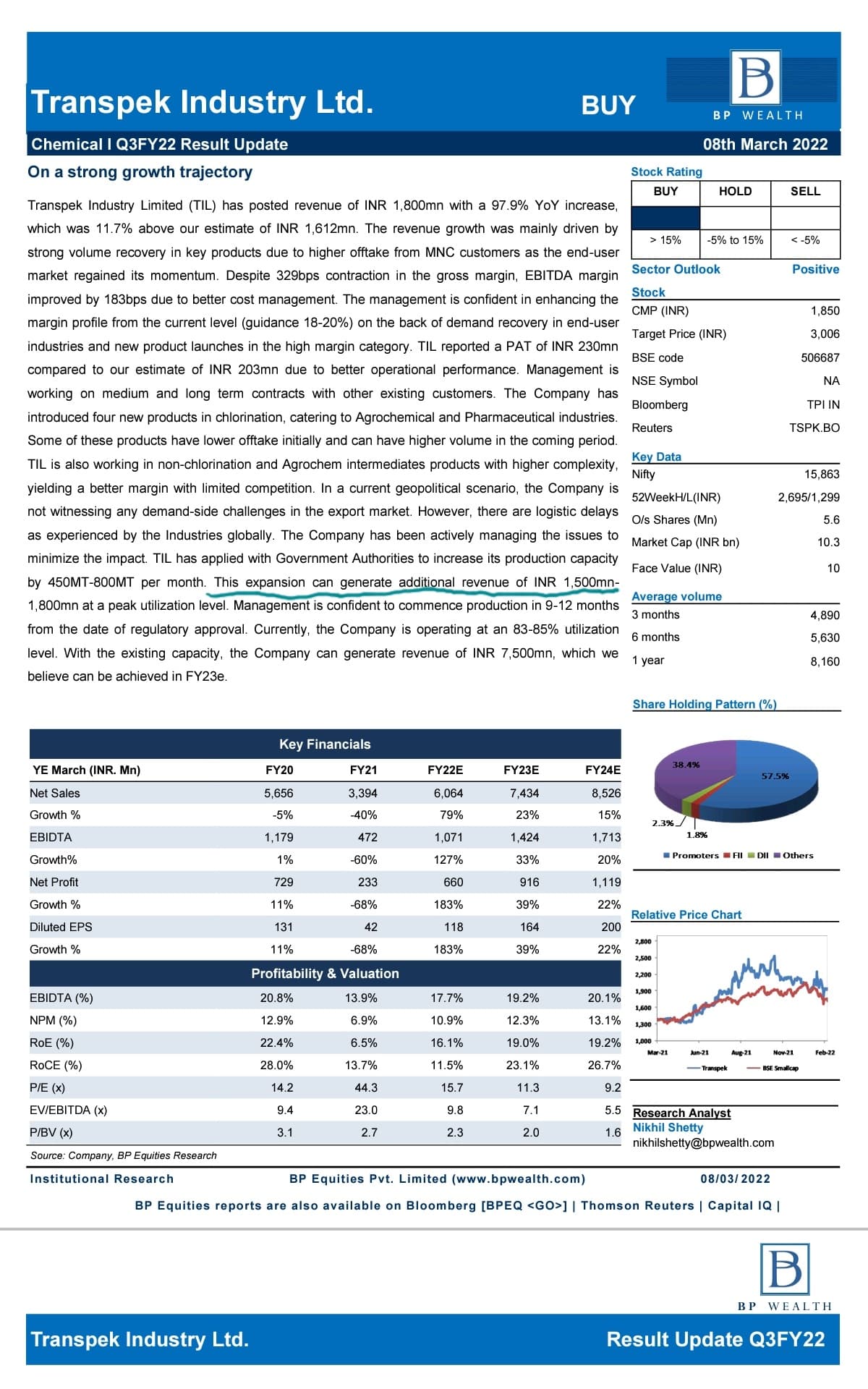

Research report on Transpek, seem to be after concall and has referred new Capex ( awaiting govt approval) with potential to potentially add upto 180 cr revenue by FY 24.

Wasn’t able to attend concall, can anyone who attended share their views.

6 Likes

Excellent information about Mr Avtar Singh @Dev_S and @harsh.beria93 .

Management reaffirmed most of the things you have mentioned in your above posts in Q3 con call.

Here are few additional points I can think of from the call:

-

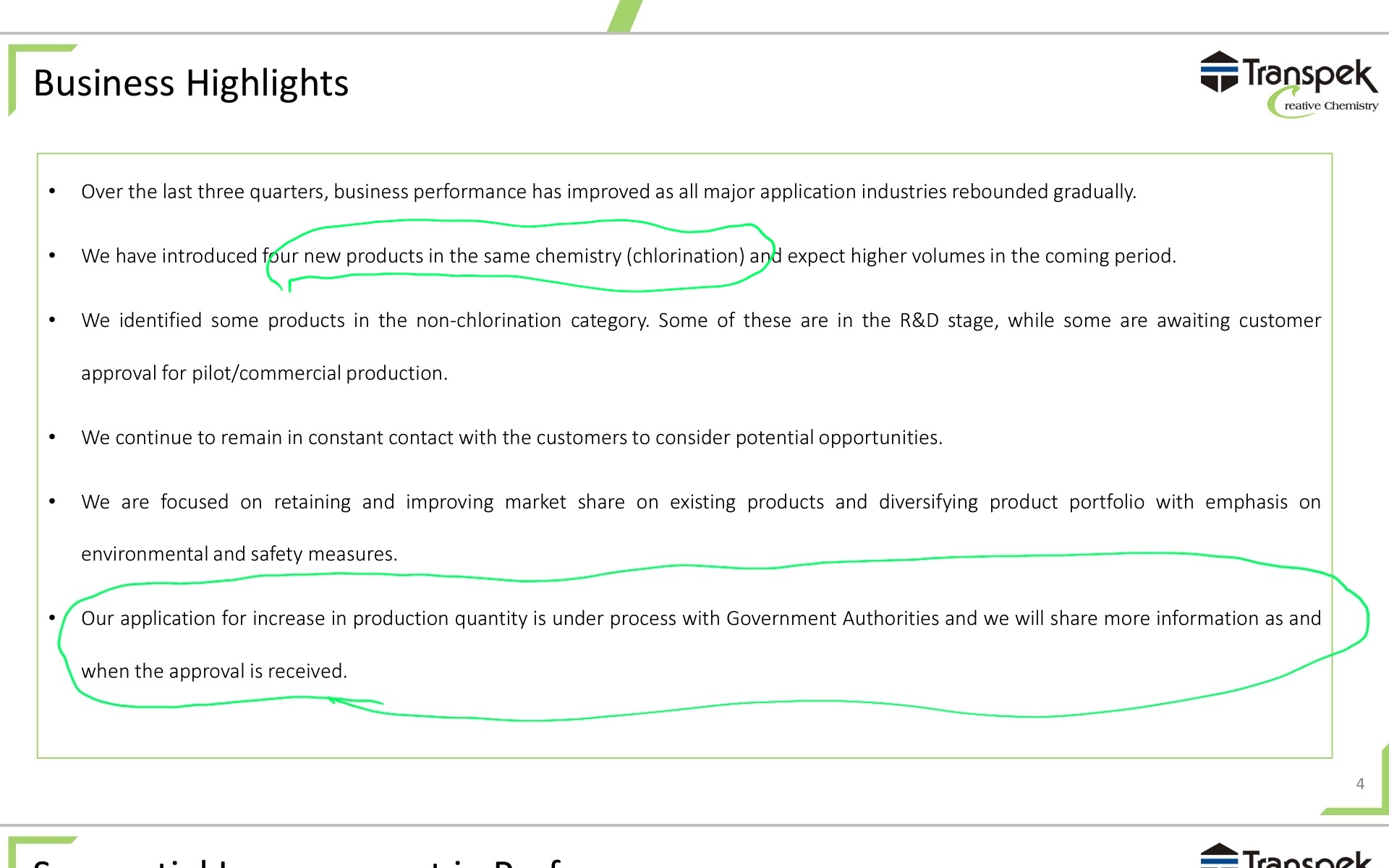

Mr Avtar Singh has joined the company with an objective to:

- Enhanced Value Added segment

- Improve complex chemistry products

- Focus on multi-step chemistry products. -

Transpeak has introduced 4 new products in the last 9 months, and they have contributed around 21 cr sales so far, which is around 3%. Most of these are pharma and agrochemical products, and their sales may gain further traction in the coming quarters depending upon customer acceptance.

-

With Mr Singh joining the company with a clear focus, I think value-added contribution may go further from next year as they are sharpening focus on execution.

-

The major revenue and profit contribution will continue to be from DuPont, and management expects good traction going forward.

-

They also said that the product is used in new plane manufacturing and not in servicing existing aircrafts.

10 Likes

Good information. Correct me if i am wrong, that i believe its product used in new plane manufacturing and not in servicing existing aircrafts is a negative since aircrafts requires constant servicing and is more lucrative.

The specific product they make(monomer) has multiple usages in producing the polymers(Tranpek makes monomer which is used by their client to make polymers). These polymers are very high end one with huge strength to weight advantage. There usages are into aircraft, bullet proof jackets, fire resistant materials etc…

Transpek is able to sell it’s entire production to their customer without any issue. For them sales is not an issue. The issue is on the capacity side, where they do not have any approved facility to cater to growth beyond FY23.

You may like to listen to their conference call. There are good enough details.

Q3 update from BP wealth.

Regards,

Raj

Disc: Invested

4 Likes

At ~900 crore mkt cap with ~100 crore of annualized profits, Transpek is at the cheapest valuations it has ever been at!!

Nibbling it waiting for Q4 results.

3 Likes

From jun 19 to jun 20 it was available for < 7 EV/EBIDTA

1 Like