Understanding operating leverage properly is perhaps the easiest step with the largest payoff.

Does Transpek have Operating Leverage? Let’s analyze. This requires looking at cost-structure.

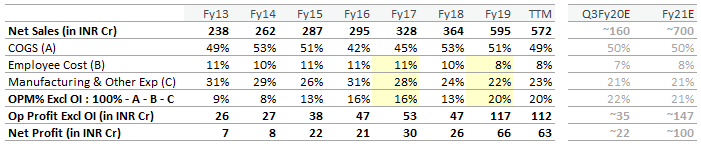

- Fy17: For 328 Cr sales, co spent 45% in COGS (materials), 11% in salary and 28% in manufacturing expense (electricity, logistics, etc). Co earned 16% OPM.

- Fy19: For 595 Cr sales, co spent 51% in COGS, 8% in salary (300bps improvement) and 22% in manufacturing expense (big 600bps improvement). Co earned 20% OPM (though COGS had gone up).

To summarize, the sales has grown 81%, but operating profit has grown 120% from Fy17 to Fy19 as the salary expense remained stable and economies of scale kicked-in. Kind of disproportionate growth.

The above operating leverage is when Fy19 had only two quarters (Q3 & Q4) of full DuPont contract. Benefit could be larger when Transpek gets a full operational year of high margin contracts (say Fy21). Add to this corp tax rate cut benefit from 35% to ~25%, the net margin improvement will be a lot larger.

Q3Fy20 will provide glimpse of steady state OPM%; seems to be first quarter of full operation in Fy20.

Key points -

- Operating leverage driven by 10yr DuPont contract (longevity)

- No one-off

- DuPont contract looks rock solid; got stress tested in ~45 days plant shutdown

- 23% RoE; Return on Shareholders’ Fund % (refer page 73 of the latest AR) is even better

- Debt reduction to further improve return ratios

Disc: Invested. Reentered in early Jan’20 after a wait on sidelines. No major transaction in last 30 days.