Acquired 51% stake in Posco-Poggenamp Electrical Steel.

Any ideas what’s his acquisition all about ?

Acquired 51% stake in Posco-Poggenamp Electrical Steel.

Any ideas what’s his acquisition all about ?

Backward integration of sorts by ensuring a good supply of CRGO steel that’s a must for making transformers but somehow is in short supply .

In Yesterday’s budget, focus was on consumer spending and general consensus is lesser focus on power sector in terms of capex.

Is it going to be painful year for TARIL and it’s competitors (or entire power sector)?

Not really. Last year due to election , they couldn’t tendered and awarded order for first four months. This has resulted in lower spending by almost 10% .This time capex amount is same as last year So practically there will be 10% rise in spending if they achieve the capex target. Further demand will also generate due to rise in consumption by private sector due to expansions of facilities by FMCG , Auto and auto ancillary, tourism etc.Private sector may kick in.

Does the market know something which we are not aware of?

I beleive trump policies on import tarifs may hit Apar industries but don’t see impact on Taril especially they mentioned in concall that demand is high in India so they are not especially looking for export market… is market still worried about tarif on India?

Price corrected almost 40% from high that too on very good results and beating estimates.

Wrong conclusion ImHO. Transformer oil is not a once in lifetime thing for transformers. It needs to be replaced periodically hence low demand for transformer oil does not mean low demand for new transformers . The low margin is also partly due to Chinese competition in transformer oils .

Agree !

Agree.

Both Statements are equaly true in general.

Based on my understanding :

This is past. > If i use simple logic which i mostly do, if we look at Order book current order book. its 4k Crore. they can do 5K crore top line FY26..

The future > The budget capex for power increased 20%, Taril having nanother 4K crore as order book by FY27 ?, i am just hoping it does. FY27 they can continue same pace. i just pulled number from space not from the ground ![]()

Margin improvement > with their recent CRGO core & Radiator integration. think can improve on costs by 10%…if an expert can shed more light on here. would give more clarity.

Overall, i am okay to hold it , since ive from lower levels. if it goes down little bit i plan to add, ive been adding mindlessly through this fall.

And yes they also mention bonus in last board meeting i guess. it does help in increased participation if they issue bonus..yes ?

Its good to see fellow Members attention in this counter. With more comments and insights. we shall have more clarity going forward.

Disc. - No recommendation. Me a starter. Me no expert. Me no registered analyst etc.

ea9c9883-8b9e-4095-bd16-bf8cc962d217.pdf (997.8 KB)

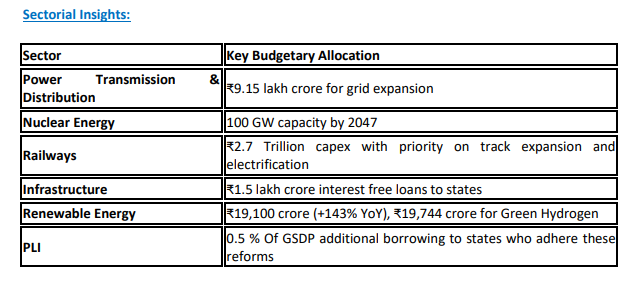

A note released by the company stating its take on the budget for the transformer sector.

Have any other companies made a similar budget update like this, emphasizing its strategic importance and alignment with their sector?

From what I’ve seen, not many, if any, have done this.

This approach conveys a strong sense of bullishness and confidence.

It’s clear these guys are poised to capitalize fully on the energy transition, railway sector growth, and their ongoing capital expenditure initiatives. They’re positioning themselves to ensure maximum capacity utilization. This is a once-in-a-lifetime opportunity for TARIL, and they seem well-prepared to seize it.

To me it appears that they are worried about their stock price going down. Why are they so insecure? Same thing I noticed with E2E. They should let numbers do the talking, and the Market will reward them for it.

Disc: not invested

I believe that the 5% circuit limit caused the price discovery process to take longer than usual after the results and overall negative market sentiment led to an overreaction in the market. Additionally, there is a high level of public holding in E2E, so panic tends to set in quickly.

In the case of TARIL, the management after 7-10 LC, clarifies the budget impact for investors. Similarly, E2E’s management had to provide explanations regarding the impact of Nvidia chip import restrictions on their business.

It’s ironic that just a week ago, during a call, management dodged few questions by stating that certain details were trade secrets and couldn’t be disclosed publically. They mentioned having a lot of orders but were currently prioritizing the highest-margin orders with better payment terms. Now, just a week later, they have come out to clarify the budget, announcing an 11% increase in capex from last year, despite the overall situation being the same. Highlighting Power and Transmission will be the biggest beneficiaries.

This situation exemplifies classical price action panic!

Interesting, so @tarunks9 & @HighCAGR you feel this PR is done purely as an attempt to protect any potential downside on price?

Even if it is so - while I don’t think it is, entirely, but let’s also give some points to promotors having that occupy some part of their thought process, as it may, for every promotor of every listed company - let’s pause for a moment and really ask - when is the last time, in our lifetime, that we have experienced energy an transition of this magnitude?

Let’s think about it’s impact on transformers, switchgears, cables, and so many other components of the entire value chain. Is it path defining for many or all of the impacted businesses?

Personally, trying to protect downside on price, is the last of their worries. The horses have arrived, and they are preparing their stable.

In normal situations you are right. However, in this case ,it’s in every shareholders interest that the downslide be arrested sooner than later because, the company had declared a plan for 750 crore QIP . At that time share price was between 1200-1300 and now it has eroded by 40% . Accordingly if they do the QIP , it will result in significantly more dilution than before . The business ,which needs money to expand and capitalize on the opportunity can’t wait indefinitely for market bellyaches to cure with time.

As I see it, the management has done the only thing they could have done in this scenario .They would not have needed it if the details were read out during budget day but hardly anyone reads the budget document to read the fine prints.

Disc: Invested .

This is clearly visible by now after government increase of allocation at budget.I think there arent many doubts.

Its path defining for many businesses at transformer,switchgear,cables.

To my understanding

The competition at switchgear,cables is intense and many may see margin erosion.

At Transformer the players are liimited compared to witchgear,cables. Further at Power Distribution Transformer used in power to end-users (e.g., 33kV) and Power Transformer Used in transmission (e.g., 110kV to 400kV) there are very few like TARIL,Voltamp, Indotech etc.

Disc- Holding.

There are many well known players in 220kV and above transformers. TRIL, CG Power, TBEA, Atlanta, Hitachi, GE, Seimens, Indo tech, Bharat Bijilj, Technical associates, Skipper, Hammond Power, Meiden limited and many more. Many are unlisted. Competition is very high in Power Transformers industry. However if demand is high evening looks good. Little bit slowdown in demand, everything will normalize and start reversing. Increasing capacity hardly takes 1 to 2 years for existing players.

Ravindra, solid insights! Always a pleasure to get wisdom from someone who probably dreams in winding diagrams and flux densities. I figured you are a power transformer design engineer by and experienced at analysing transformer stocks.

Now, coming to my question—I’ve been poking around the high-voltage (HV) and ultra-high-voltage (UHV) transformer space, trying to figure out which listed players are really charging up. There is a Nuvama report analysing transformer space in this same thread (![]() : link), and i continue to seek answers on

: link), and i continue to seek answers on

The report lists out different capacity segments. i am getting following list:

| Manufacturers in HV transformers (220kV & above) | Manufacturers at the 765kV level |

|---|---|

| Siemens | TRIL (since FY12) |

| GE T&D | CG Power (since FY09, earlier via Toshiba JV) |

| Hitachi Energy | BHEL (since FY12) |

| TRIL | Hitachi Energy (since FY09, earlier via ABB parent) |

| BHEL | GE T&D |

| Bharat Bijlee | Siemens (since FY09) |

| CG Power | Toshiba (Private) |

| TBEA India (Unlisted) | TBEA India (Private) |

| Toshiba (Unlisted) | - |

So, filtering out the unlisted names, we get listed names: TRIL, BHEL, BB, CG, GE, and Hitachi.

Now, here’s where I’m scratching my head:

Would love to hear your thoughts—because if the sector or a name is about to light up, I don’t want to be left standing in the dark.

D-Holding & Adding.Not a recommendation.Not an expert or registered analyst.

You list for 765kV is very accurate, but in 220kV there are tens of companies to be added to your list. Yes, current order book of the company is very good. TRIL historically shows 1 to 1.2x order book which is currently 2x. However, lot of capacity will be added in next 1 to two years so definitely maintaining current margins is very difficult going forward and market punish the stock as soon as it senses margin contraction. Currently I am seeing a trend that there are lot of openings for transformer engineers and technicians, all this suggests capacities are building up.

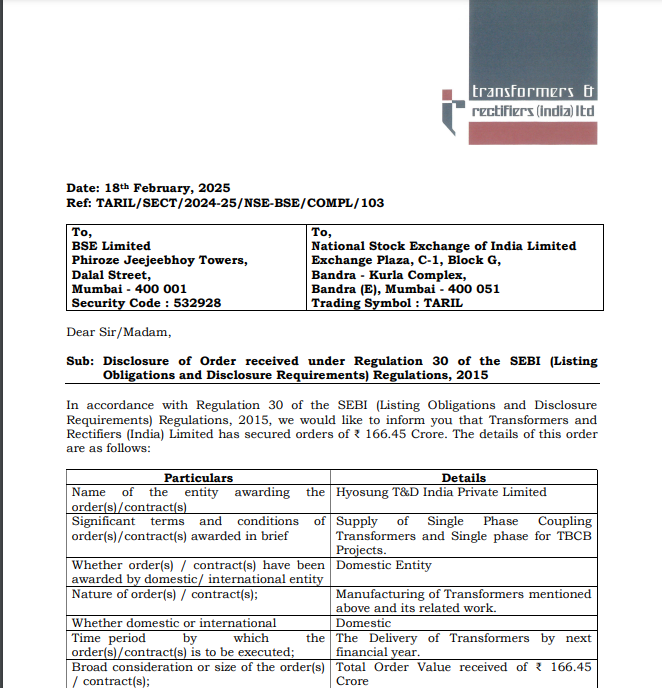

Transformers & Rectifiers (India) | Order Win

a. Secured ₹166.45 Cr order from Hyosung T&D India Pvt Ltd

b. Scope: Supply of Single Phase Coupling Transformers for TBCB projects

c. Execution Timeline: Delivery by next financial year

Transformer & Rectifier | Management Guidance

a. Orderbook: Stands at ₹4,200 Cr with the latest order

b. Revenue Guidance: ₹2,000 Cr for FY25, ₹3,500 Cr for FY26

c. Order Pipeline: 20% of ₹18,000 Cr worth of enquiries may convert into orders in the next 2 quarters

d. Margins: Expecting 15-16% margin in FY26

TARIL | Management Interview

Watch the management interview here