Anyone tracking TRIL? It has formed lower low pattern on chart and went below 21 week MA first time since April 23? Signs of weaking in transformer space and this stock?

Presentation> https://www.bseindia.com/xml-data/corpfiling/AttachLive/b074122e-2221-4222-a36c-3104e5c2d42c.pdf

Audited results>https://www.bseindia.com/xml-data/corpfiling/AttachLive/6e3808ab-845a-4f91-b385-642a765d5128.pdf

I think good set of results by TARIL

Going by results and their oder book…if look at past trends and existing orders, ball park can be taken another 700Cr for H2 FY25? in that case total FY25 it may do topline of much more than 1500Cr FY25.

It Starts with UC today, Previously they were negotiating 17k cr enquiries …now it increased to 18.5K cr…In my opinion it should continue doing good.

Can someone help me calculate forward PE ?

D- Holding from lower levels…post is for my studies/tracking…no recommendation, i am new recruit etc.

Superb results. Haven’t heard the Con call yet, but apparently the management is very bullish.

Holding this since a year, and maybe for a few more years. The entire sector is poised.

I wonder why Mr. Kela has reduced stake to below 1pc. Very strange move.

1 Like

Profit booking I reckon, he entered sub 200 and it was a substantial stake. I remember him mentioning it on an interview after the first time he trimmed his holding, something along the lines of I believe in the company but its run up a lot so I booked some profit to invest elsewhere.

Premature. Also, isn’t Cohesion MK Best ideas also MKela? Appears under FII holdings.

Taking TRIL results + Q2concall into account - we are witnessing a mammoth turnaround and if the management continues to execute, FY27 could be mind-numbing.

Holding tight - once in a lifetime opportunity for the company, and shareholders.

3 Likes

4 Likes

Aquisition of controlling interest in CRGO steel (Electrical grade ) manufacturer by TARIL.

Strategic move which ensures uninterrupted supply of scarce CRGO which constitute 35% of RM.

Microsoft Word - 9. Stock Exchange Letter_2024-25

3 Likes

Great results by company. Company declared 1:1 Bonus as well as 750 CR QIP.

3 Likes

Excellent results! QIP was the need of the hour I guess because of terrible CFO to EBITDA conversion over last 5 years, so no cash to fund the growth.

4 Likes

As i try to look at future orders…they are still negotiating good numbers…though inflow might have slowed due to various reasons.

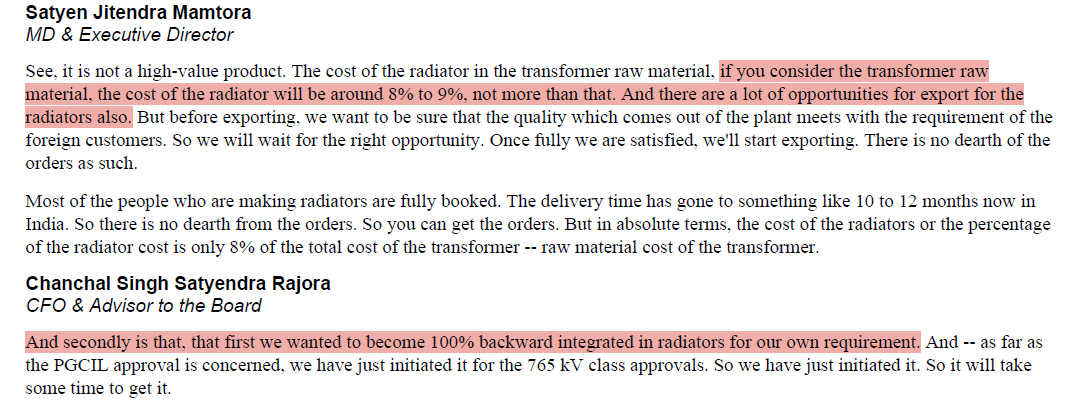

I noticed they now want to integrate transformer radiators as they did with CRGO cores…I think radiator is ~15-20% of a transformer cost…this shall improve bottom line. though it may take time to set radiator thing up and running.

D-Holding.

4 Likes

#TARIL: Q3FY 25 Key Updates ![]()

1/ Revenue Goals: Targeting ₹2,000 Cr in FY25 & ₹3,500 Cr in FY26, maintaining the $1 billion long-term vision.

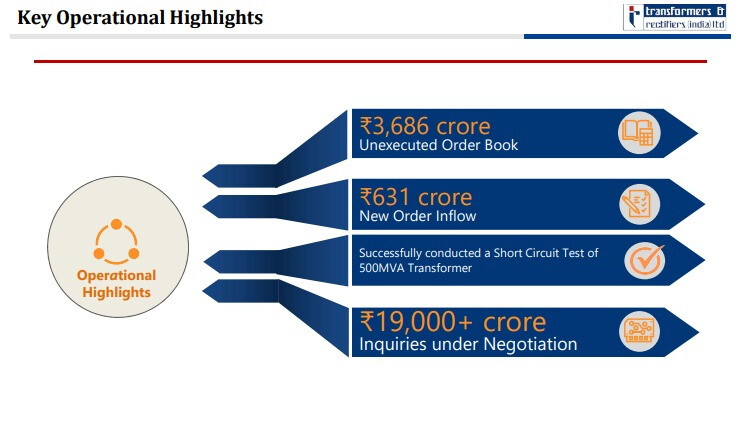

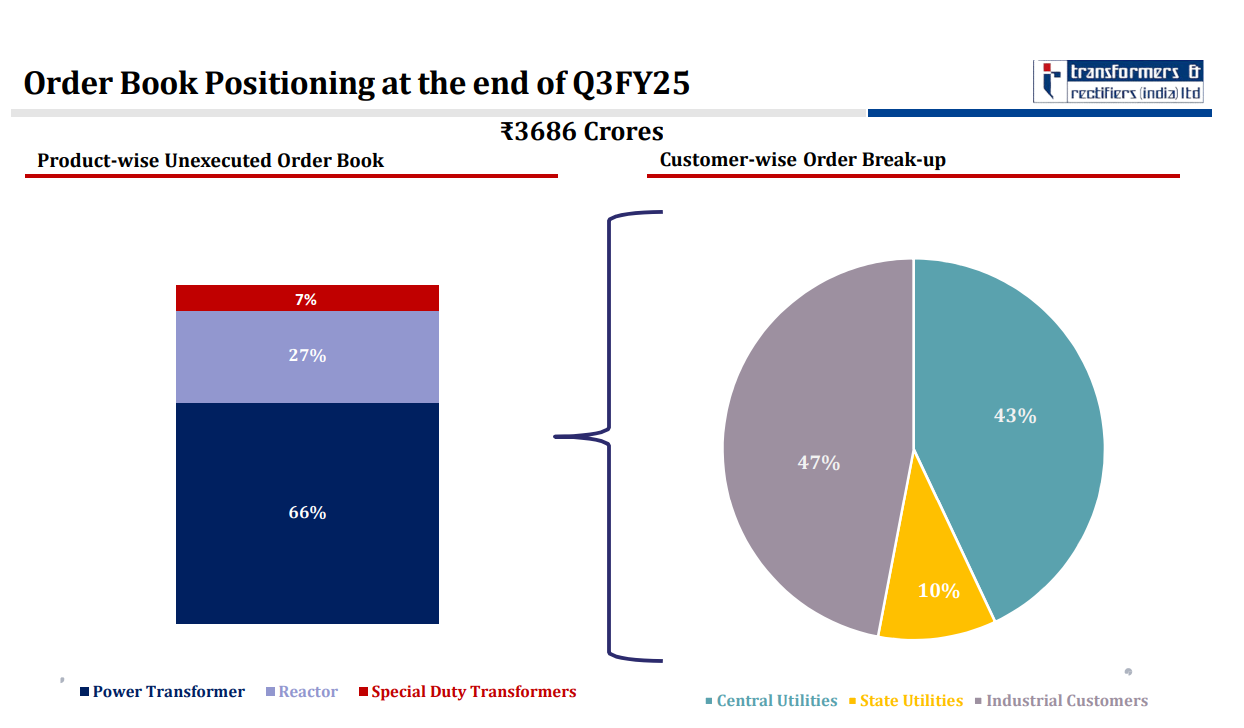

2/ Order Book: Strong at ₹3,686 Cr with ₹631 Cr in fresh orders this quarter. ₹19,000 Cr pipeline; focusing on high-margin, favorable-payment projects.

3/ Facility Expansion: New 15,000 MVA facility ready by Q1FY26. CRGO backward integration to reduce raw material costs by 4%, boosting margins.

4/ Profitability: Current PAT margin at 9.12%; aiming for 10% soon. Improved debtor days with no overdue government payments.

5/ Financial Update: QIP approved but no fundraising planned for the next 2–3 quarters. On track to becoming debt-free in the near future.

6/ Innovation & Exports: Green hydrogen transformers in the prototype stage; expanding internationally with Europe & America orders on FOB terms.

6 Likes

Q3FY25 Concall Notes:

Financial Performance:

- Revenue Growth: The company experienced a strong year-on-year revenue growth of 49%, with standalone revenue from operations reaching ₹545 crores in Q3 FY25.

- Profitability: There was a significant increase in profit after tax (PAT) for Q3, showing a year-on-year growth of 276% with a PAT margin of 9.12%.

- Operational Margin: The company achieved an operational margin of 15.69% for the quarter.

- EBITDA: EBITDA for the quarter was ₹87 crores, a 136% increase compared to the previous year.

- Debt Reduction: The company is focused on streamlining its balance sheet, reducing debt, and optimizing inventory management to become a debt-free company in the near future.

- Working Capital Management: Emphasis is placed on the CPI model (cash payable, cash receivable, and inventory management).

Operational Performance:

- Order Book: The company secured new orders amounting to ₹631 crores in the quarter. The unexecuted order book as of December 31, 2024, stands at ₹3,686 crores. They also have inquiries worth ₹19,000 crores under negotiation or in the bidding stage.

- Order Strategy: The company is being selective about orders, focusing on high-margin and high-momentum opportunities instead of taking every order available. Management admitted that they can take 1000 orders a month, but they are limiting themselves reason is stated below.

- Market Dynamics: The market is very good and those companies that are not taking orders are quoting higher margins.

- Capacity Expansion: A 15,000 MVA expansion project is on track and expected to be completed by February-March with operations beginning early next year. Post expansion they’ll be at capacity of 55,000 MVA levels.

- Backward Integration: The company acquired a controlling stake in a CRGO (Cold Rolled Grain Oriented) processing unit, making it 100% backward integrated for this key raw material. A supply agreement for mother coils has also been established. This backward integration will eventually help the TARIL to increase its operating margin as CRGO contributes about 35% of raw material. The company expects a 4% reduction in total raw material costs by using their own CRGO.

- Technology Tie-ups: Three technology tie-ups have been entered to support backward integration goals, expected to be operational by quarter 4 FY26.

Industry Trends:

-

Strong Demand: There is a high demand for transformers across various sectors including renewable energy, private industries, and power utilities.

-

Infrastructure Development: There is no slowdown in infrastructure development in India, which is driving demand for the company’s products. “The opportunities are quite huge in India are much better than the other parts of the world.”

-

Limited Export Focus: The company aims to keep export orders to 20% of its business, focusing primarily on the Indian market.

-

Radiator Market: The market for radiators has high demand with other manufacturers facing long delivery times.

Future Outlook:

- Revenue Growth: The company anticipates significant growth in revenue, targeting ₹3,500+ crore in the next financial year. The company aims to have an order book of ₹4,000+ crore by the end of the financial year. The company aims to achieve a US $1 billion revenue target in the next 3 to 4 years.

- Margin Expansion: The company is looking to move towards a 17%+ margin by FY27 through backward integration and improved efficiencies.

- Backward Integration Benefits: The backward integration initiatives are expected to improve the company’s bottom line and top line, with an expected minimum 4% increase in PAT by having all the projects online. Benefits of the CRGO processing unit will be seen from Q1 next year.

- Green Hydrogen Transformers: The company is the sole qualified supplier of green hydrogen transformers. However, this is still in the prototype phase, and projects have not yet commenced.

Government Capex:

- Infrastructure Spending: The company does not see any slowdown in government spending related to infrastructure development.

- Transmission Projects: The company does not keep track of the total number of transmission projects in progress but notes that the requirements keep getting bigger due to new solar plants coming up.

- PGCL Approval: The company has initiated the PGCL (Power Grid Corporation of India Limited) approval process for its fully automated radiator facility for 765 KV class.

CRGO Steel Update:

- CRGO Scarcity: CRGO is in scarcity in India, and there are not many good processing centers.

- Internal Use Priority: The CRGO produced will primarily be used for internal consumption with any excess capacity not exceeding 15% to be sold to other companies.

One question from my side is that if not everyone but big players of this transformer industry starts doing backward integration like TARIL has done, what will happen to companies like Vilas and Jay Bee? What I see is that in the longer term these transformers makers will do as it’s margin accretive and better control over order fulfillment.

12 Likes

To be honest, I would rather look at the long term trajectory and not worry about day to day price movements. Day to day movements are rather random, like that of a drunkard walking down the street.

I would instead think of future growth and more importantly, how much of it is already priced in.

6 Likes

Nuvama said TARIL’s Q3FY25 results were in-line with its estimates on stellar execution (up 51.4 per cent YoY) and strong operating profit margin (OPM) at 15 per cent-plus. With order book of Rs 3,700 crore (2.9 times FY24 sales) and Rs 19,000 crore-plus prospects, it finds strong sales visibility, doubling over FY25–27.

“We maintain ‘BUY’ on tailwinds of high demand for HV transformers coupled with TARIL’s backward integration adding to our confidence of margin expansion. We are raising FY25E/26E/27E EPS by 10 per cent/17 per cent/29 per cent and target price to Rs 1,450 from Rs 980) at 40 times FY27E PE multiple (from 35 times),” Nuvama said.

For Antique Stock Broking, Q3 results were also in-line with expectations. TARIL, it noted, is undertaking an ambitious capacity expansion program, which will not only make the company India’s largest transformer manufacturer, but also one among a few with control over key inputs through backward integration.

Given the unprecedented demand tailwinds, we increase our exit multiple to 45 times from 40 times and revise our earnings estimates upwards for FY25E/ 26E/ 27E by 30 per cent/ 16 per cent/ 7 per cent maintaining BUY rating with a revised TP of Rs 1,424 (earlier Rs 1,187)," it said.

TARIL is confident of achieving its revenue guidance of Rs 2,000 crore and margin guidance of 14 per cent for FY25 and is hopeful of booking revenue of Rs 3,500 crore and margin of 15–16 per cent by FY26.

The company reiterated margin expansion would be on account of backward integration & improved demand which will lead to better realization. TARIL has already started on the journey towards backward integration of key critical components & has signed a technology agreement for three critical components expected to be operational by December 2025. It is targeting $1 billion revenue in the next three financial years

“We expect TARIL to report exponential growth over the next three years, with revenue and PAT rising by 3.6x and 10x in FY27 from the base of FY24. Despite a meaningful re-rating in 2024, it trades at a discount to its peers. We believe that the valuation gap should narrow over the coming years given the company’s growth objectives and accelerated earnings delivery,” Antique said.

point being people who have benifited from run up pre results are selling any meaningful correction will be a very good opportunity growth trajectory in line and peg < 2 currently

15 Likes

Bang on. I’ve been invested from lower levels but despite the run up and the valuations being exorbitant, it does feel like there’s still opportunity on the table.

FY28-29 Rev at 8000 Cr with a 10% PAT and exit multiple of 50 is a 40000 Cr mcap company. That’s a sweet return with decent margin of safety as well.

More than this, I think its an even longer runway with not just domestic power demand but the revamp that’ll happen in grids in Europe & US. The wait times for power transformers there runs into years as per Mr Mamtora.

I do see 2 risks though. At these valuations, there’s no room for any missed guidance and one has to look at how competitive intensity increases (this will take time so I’m not concerned short term) and be wary of over supply getting built with time as these are far from recurring sales.

9 Likes

Agreed, the only caveat being that it may not be prudent to give a high exit P/E to a company in what is essentially a deep cyclical industry. Let us not forget the dire straits transformer companies were in, not so long ago.

But the good part is that with all the multiple tailwinds (massive movement into the cloud, massive demand from AI compute, the electrification of more and more things, such as transportation, the increase in infra due to renewables, and so on, creating what Munger would call a lollapalooza effect) I don’t see demand abating at least in the next 5-7 years.

4 Likes

Yes, exactly. The tailwinds are such that while the 50 exit multiple looks high in isolation, its actually pretty conservative for FY28. They are talking of 1bn rev at 10% PAT. If they actually do 5x their PAT in 3yrs, I’d be surprised if the multiple is 50 given how long the runway looks. Mr Mamtora said in the last concall that he could book 1000cr of orders every month if he wanted such is the demand but he just cannot serve that many.

5 Likes

Anyone attended Jan 2025 concall? Anything most of the people are missing? Stock price has taken a -21.6% hit even after strong sector tailwinds, strong result and order book.

On the other side, GE vernova (equivalent player in US domestic, listed in US) is surging with similar results as TARIL. (Ref: GE Vernova Inc. (GEV): Strong Financial Growth and AI-Driven Innovations Advancing Sustainability and Energy Solutions - Insider Monkey)

1 Like

Yes, nothing said on the call explains the drop. The call was bullish. I’m not an expert on price action but as I see it, its due to a weak market in general plus profit booking due to the incredibly rally in the stock price.

3 Likes