CMP - INR 216/- Macp INR 285 Cr. Sales 2015 - Rs. 541 Crs Loss at Net level (2015) INR 6.41 Crs

Transformers and Rectifiers India Limited (TRIL) is a company whose fortunes fluctuates wildly with economic cycles. Established in 1994, it manufactures Industrial and Power transformers ranging from sub 33 kV to 765 KV…. The entire sector faced dramatic stagnation for last 5 years.

The breakup of end use of transformers are

Sub 33 KV — Distribution transformers used by Discoms and small & medium enterprises (demand is a function of industrial up cycle and distribution network up gradation)

33 KV to 220 KV — Power transformers used by Discoms, Transcoms and Large Industries (demand is a function of up gradation of state transmission networks)

220 KV to 765 KV — Power transformers used by State Transcoms, PGCIL and Generating Companies (demand is a function of interstate transmission network and power generation and evacuation capex)

There are many unorganized player in sub 33KV segment. And major players up to 220 KV segment and above are: ABB, Alsthom T&D, Siemens, Crompton Greaves, BHEL, EMCO, TBEA India (Chinese company), Vijai Electricals, Bharat Bijlee and Voltamp Transformers. Total industry capacity is about 400,000 MVA and industry wide capacity utilization till recently is about 66%. Total capacity of TRIL is about 33,000 MVA.

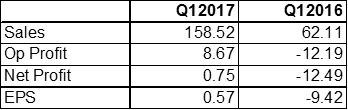

The price per MVA and OPM for all players taken a hit during last 5 years and seems to have reached a bottom this year. In spite of huge drop in price of Crude, Copper and Structural Steel, the price of CRGO (Cold Rolled Grain Oriented) steel sheets which constitute 40% of RM cost remained strong during whole year negating any benefit of commodity fall for companies in this sector. TRIL had a large pending order book from PGCIL with very low and negative margins, execution for which have just completed. All the negatives, working together resulted in meagre 4% level EBITDA margin and loss at net level for the company for last year and current year till date.

During last economic up cycle, the OPM was in the range of 15% at its peak (presently it is 5%).

The industry is plagued with overcapacity, intense price competition and problems related to tender based procurements from cash strapped SEBs. I expect any new capacity addition is unlikely in this unattractive sector. With the demand pick up through ordering by PGCIL and State Discoms, I expect price stability will probably come back.

During the tough time of last four years, TRIL ventured into export market and also focused into relatively profitable segment of Arc Furnace Rectifier and got few orders from Iran. It also entered into technology agreement with Fuji Electric Company of Japan in December 2014 for generator step up transformers of higher ranges for sale in India only. The agreement is valid for 10 years. The company has also received a Rs. 400 Cr. order for supply of 300 mid-range transformer to Algeria. Only 95 of these transformers have been shipped so far. During the latest Concall, the company confirmed that from April onwards 30 transformers per month would be shipped against this order.

Earlier their sales mix was 80% Power Sector and 20% Industrial sector. But gradually during the last recessionary phase company increased its share in the industrial segment and presently the ratio is around 55 : 45. Going forward, it may possibly act as a cushion against wild fortune swings.

Currently the order in hand is about Rs. 1050 Crs. and management as per last Concall expect EBITDA margin to improve from current paltry 4% level to 8% level in next one year. But it is pertinent to note that management, on a few occasion earlier, failed to deliver on its promises made in TV interviews. Their last 9 months sale is 328 Cr vis-à-vis 378 Crs in previous 9 months, which is somewhat unexpected but management claims a huge FG inventory has been build up as some delivery got delayed for “short circuit” testing.

Financials of the company presently have nothing worthwhile to discuss (people interested can review it from exchange websites or elsewhere). Company came with an IPO in 2007 at Rs. 465 apiece but I guess it mostly quoted below issue price since listing as market and the entire sector tanked since those days.

Discom capex is picking up as feeder separation scheme, which has been launched about 18 months back is showing traction and reduction of T&D loss has been made mandatory for financial rehabilitation for SEBs forced them to invest in transmission segment. The gradual expansion of order book with possibility of higher margin and export foray are some comforting factors.

Since companies in this sector work with huge operating leverage, I expect TRIL to be an interesting story going forward as an opportunistic investment theme. However, it is to be noted that many a time working capital cycle gets unpredictable as off take of transformers depends on other extraneous factors related to the project for which transformers are being procured. Also, significant devaluation of Chinese currency may act as dampener in the industrial segment to some extent.

We may watch and monitor closely as the story unfolds.

Company latest presentation is attached….

http://www.transformerindia.com/download/Investors-Presentation-Q3-FY-2016.pdf

Promoter has pledged 22% of its holding and it it pledged for last 6 + years. Total Promoter holding is 75%.

Disc.: Invested (>3% of portfolio). No trading in last 30 days.