So employees don’t believe in the company’s prospect.

1 Like

I discussed with him and the main thing which separates pitchbook from all the others companies is the speed like how fast they can provide any deals or any data for the companies the customers are tracking and regarding the comapny where my friend work,he mentioned there business approach is little different, first they try to cover all the assets of a firm which they want to have their ascustomer and then offer what they have more

1 Like

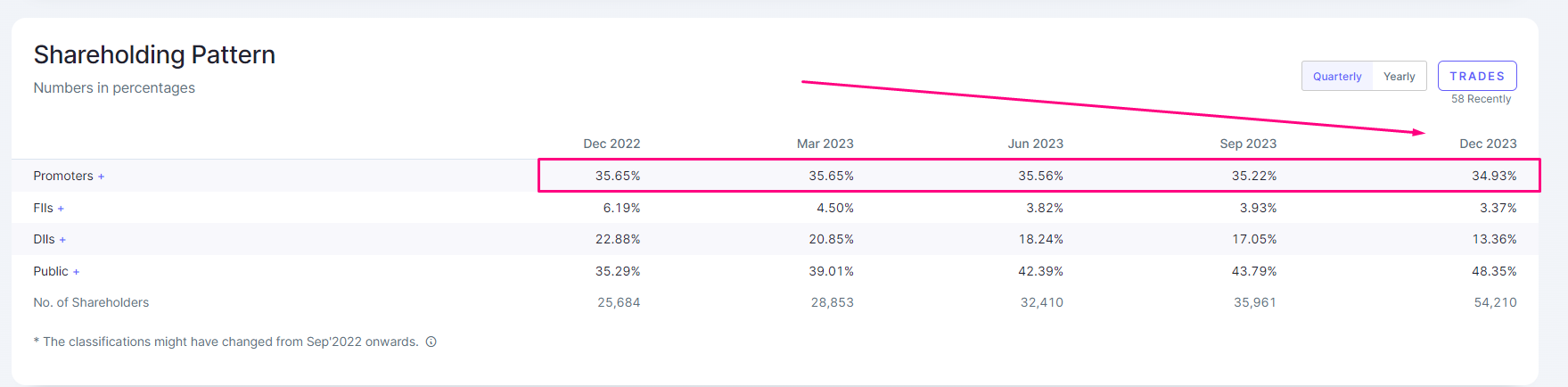

When you give employees stock ownership as part of their incentives, you usually have to issue additional shares to give them. This results in an increase in the number of shares outstanding of the company. When the number of shares outstanding increases without any change in your existing holdings, the percentage of your holdings decreases. This is what I think happened to the promoters’ holdings.

I think this point was asked as a question in the last Concall where somebody pointed out the dilution of equity as a drawback of ESOPs being given to employees. But it’s a standard practice that firms in initial stages of growth use.

6 Likes

This is a pretty suboptimal renewal rate. Pricing is rarely an issue for products catered towards professional investors (Bloomberg charges a fortune & people still prefer it). Clearly, people don’t find the platform as useful as Tracxn claims it is.

This is a potent signal about people’s preference for the platform, a signal from which one can infer why the revenue growth is subdued.

5 Likes

Hi Pranjal,

What would be a good renewal rate? Also, do you know if it has dropped over the years?

I am wondering if this low renewal rate has something to do with lower interest in PE / VC funding. Do you see a drop in renewal rate even for others too? Any idea?

Hi, Just wanted to ask where is this data available, of Pitchbook no of licencees year over year, also is it possible to get data from 2012-2016?

1 Like

Started reading about the company fairly recently. Asked one of my seniors who is working as PE investor for quite a few years now. He said that, he only used it once and pitchbook is widely used. He further said Tracxn is useful for very early stage and the pricing is of course lower as compared to pitchbook.

Disc.- not invested

5 Likes

Very flattish results from tracxn,while the scenerio can change if there are rate cuts in usa which can attract vc money and eventually pickup of business

1 Like

Hopped on the recent call, Tracxn wants to bet on the Bloomberg model of sorts, they want to establish their software in educational institutions so that the graduates who enter PE or VC later are familiar with Tracxn’s software and choose them over other service providers such as Pitchbook. Long Shot?

DC: Invested

2 Likes

I have some experience with Tracxn free version. The issue is that it neglects the US market where all the money is no.1. Secondly they have a free version that almost has all the functionality of the paid one except with restriction on how many investments you can see, etc. My point is either keep it paid like Pitchbook or undercut them. They charge high fees that is cheaper than pitchbook but not by much (30-40%). When your clientele will be Indians, it would be smarter to sell cheaper honestly

2 Likes

I agree to be economical in the Indian Sector, as the price sensitivity is quite high in our geography, In the US and other first-world countries, the quality of data is quite important, and they don’t mind paying an extra 20% for better data or customer service, Tracxn can leverage the customer service aspect of the better value package in first world countries and India by undercutting PitchBook.

1 Like

PE and VC firms who use private company data are rich folks who have shitloads of money and are short on time. They are entirely price inelastic.

This is not a business you can compete on price.

I believe there are no pe VC investors who only use traction and do not use other more premium platforms. Hence I think traction is mostly subscribed as a second option by these rich folks to find any additional information which their most preferred platform might not have.

4 Likes

Yeah makes sense, I recall one of my investment banking associates stating that Tracxn provides good value for additional or misc information.

1 Like

I work for a single family office with reasonable holdings and yet they are very picky on price. See, its not just institutions who use this. It is also HNI’s, SFO’s and LPs who need it. They will be picky and they are higher in number. Remember that the money they earn from a 10 Billion AUM company and a 10 Million AUM company wont be huge as the price per seating is same. They are pretty decent for India and Europe. Not much US as there is no financial info regarding those areas

1 Like

Does anyone know why the earnings release has been postponed from 25 Oct to 8 Nov? Does it indicate some trouble?

Hi guys, have been tracking this company for a while and at CMP this looks like a very good bet on private markets globally as well as domestically.

Growth Potential & Revenue Trajectory

Revenue has grown from ₹44 Cr in FY21 to ₹83 Cr in FY24, with FY25E projected at ₹85.9 Cr, implying moderate near-term growth.

Guidance indicates 20% long-term growth, with revenue estimated to reach ₹170 Cr by FY29, supported by industry tailwinds.

Expansion in global clientele and recurring subscription revenue adds predictability and stability to the topline.

Profitability & Cost Efficiency

The company’s cost structure is improving, with costs increasing at a stable 5-6% annually.

EBITDA margins are expected to expand as the company scales, benefiting from fixed cost leverage.

Valuation & Upside Potential

Valuations seem cheap for a platform business- will be valued on a ARR multiple rather on earnings

Current market price at ~65 could offer entry opportunity considering business bounces back.

Industry Positioning & Competitive Advantage

Positioned as a data-driven investment intelligence platform, Tracxn benefits from increasing demand for alternative data in VC, PE, and M&A.

High renewal rates and strong client stickiness provide a durable revenue base.

Tracxn presents an investment opportunity based on steady revenue growth, margin expansion potential, and attractive long-term industry tailwinds. While near-term execution risks exist, its scalable SaaS model and increasing data monetization support a long-term positive outlook.

Dont personally see a disruption from GenAI, infact a beneficiary.

mgmt has great pedigree and looks like a no brainer at cmp but curious to find out what the thread thinks. Cheers.

Untill the inflation decreases and interest rate cut happen in USA…money flow will not happen to PE/VC funds…till then will see tepid growth as we are seeing for last couple of years

Last 2 years Less than 10% Revenue Growth with OPM halving from 4 to 2%; still trading at EV/EBIDTA of 84!! Unless they discover some new revenue segment and reduce cost drastically using some AI Use case, wont be surprised if the valuation beating continues…

2 Likes

So the thread has been inactive for long.

The main thing which pull me here is the CMP and Mktcap/Sales for this platform saas business.

If anyone has been tracking them, I would be grateful if you can help me in the following matter-

-What should investor really see in the business , apart from what management is talking about?

-Any comments on volume growth, domestically and internationally?

-So, a lot of smart money was bullish about the company in past 1-2 years, Is there any change in the story?

I did a very soft read on the company and will be diving deep if story is intact and business is worth tracking.

Thanks in advance!!

1 Like