vishal, wat is taxation? since it offline and there is no stt …

Hey in what terms are you speaking for taxation.??

-

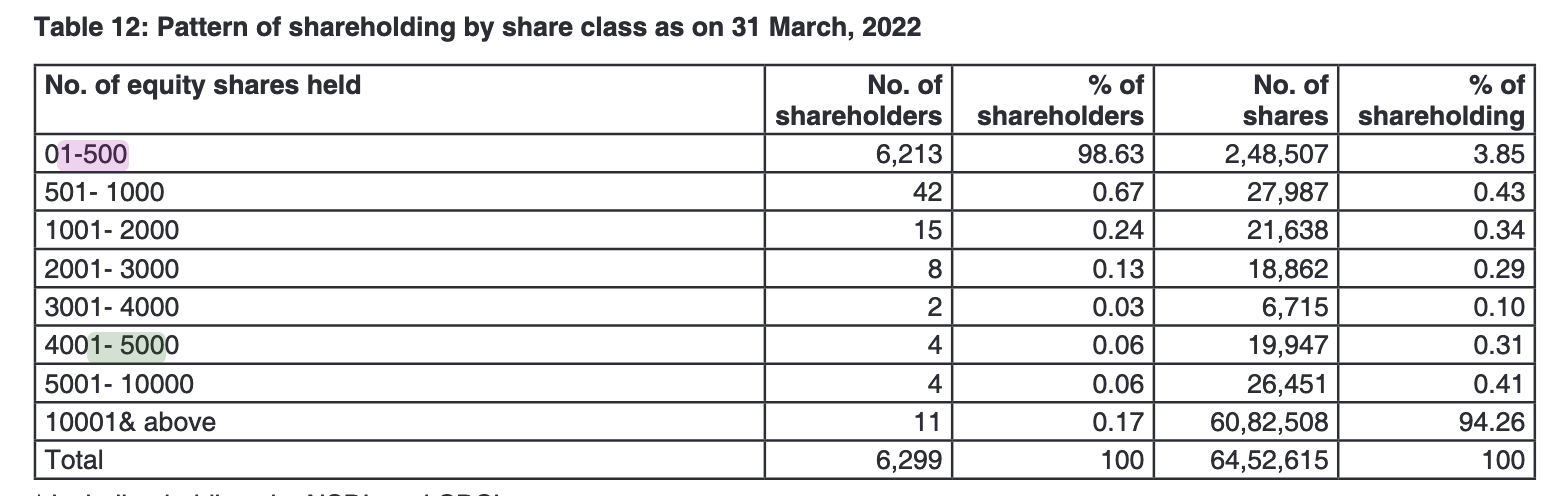

Kama Holding is doing buyback, which is just 0.53% of the total Equity Shares. You need to have 189 shares (worth 25 Lakh) to be eligible for 1 proportionate share in buyback.

-

To be considered as small investors, you need to own ~15 share or less. Not sure how many of these small investors will get even 1 share eligibility in 15% buyback quota, ( 1/15 = 6.66% ~> 12.5 x 0.53)

-

Around 6000 shareholder own average 40 shares each.

-

Seems most of the investors holding share between 1-8, and 16 -189 will not be able to participate, Or does every one gets minimum one share eligibility

?

?

5 Likes

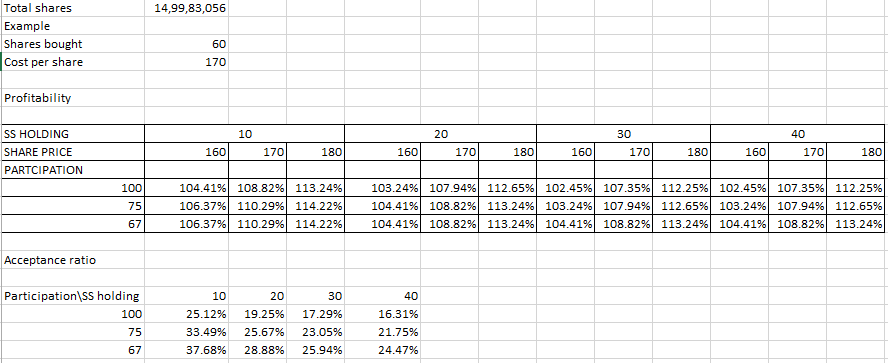

New SS idea - Welspun Enterprises Ltd - Special dividend and Tender offer buy back

The company on 30/12/22 announced a special dividend of ₹7.5 per share (record date - 11/1/23) and a buy back through tender offer of a maximum of 11,750,000 shares at ₹200 per share (235 Crs). The record date for the buy back is yet to be decided.

The company’s shareholding as on 23/12/22 was as below:

Promoters - 53.76% - 80,625,003

Retail + Body corps + NRIs - 40.98 - 61,468,766

Others - 5.26 - 7,889,287

Total shares - 149,983,056

FY22 AR says only 8.12% of shares were held by small shareholders (less than 3000 shares). In reality even less as, probably 5-7% max.

Buy back - 7.84%

Promoters intend to tender a max of 5,350,000

Reserve for Small shareholders - 15% of the buy back

Assumptions

*SS = hold 10% or 40% *

Participation = 100%, 75%, 67%

Share price after buy back = 160, 170, 180

I have approximated the acceptance ratio to 1 in 6, 1 in 5, 1 in 4 and 1 in 3.

The potential upside could be anywhere between 2 to 15%, including the special dividend but it could very well be more than this if the cost is lower or the acceptance ratio is higher.

Most probably this trade can be completed before the end of Feb so, the annualized returns look even more appetizing.

Please point out any mistakes in my estimates.

Disclosure - Not yet invested. Mulling

6 Likes

Very well summarized. Got into same conclusion. But with past buyback experience, suggest you to add 20% increment in the expected retail shareholders - 1 reference for the same could be shareholding pattern. Public holding have increased from 40.24% to 41.95% in Dec 21.

I have back calculated with the expected selling price of remaining shares. On that basis, I got any price below Rs 157-160rs (excluding special dividend) is a good price to enter. I have assumed worst case price Rs 140, where last swing made, which gave me technically support price. Fundamentally, stock seems to be above of fair price.

Disclaimer: Just an opinion. Not a recommendation.

2 Likes

Gyscoal Alloys Ltd - Rights issue

The company aims to issue 174,103,116 Fully paid-up Equity Shares of Rs. 2.75 each at Rs.1 per share aggregating to ₹478,783,569.00. The entitlement ratio is 110 entitlements for every 100 shares held. The record date was on 23/12/2022 and the closing date on market renunciation and issue closing date will be on 9/1/23 and 12/1/23 respectively. The total shares outstanding are 158,275,560 meaning the rights issue will increase the share base by 110%.

Shareholders get to participate even more than their proportionate right, in the rights issue when the applications received are less than the issue and hence could get allotted more shares than the rights entitlements in hand thereby bringing down the cost per share allotted.

But I don’t know if one has to own the shares before the record date to get this privilege or if buying the entitlements would suffice.

The share price dropped from a high of ₹4.2 on the record date to a low of ₹3 but has recovered to ₹3.3 as of the date of writing this. The entitlements are trading between ₹.15 and ₹.2.

Example:

Cost of entitlements - ₹.15

No. of entitlements bought - 200

Extra application and allotment - 1.5X

Shares price after allotment - ₹3.1

The total cost of this bet = ₹855 (2002.9 + 1002.75)

Realisation after allotment = ₹930 (300*3.1)

Profit % w/o transaction cost = 8.77% in 1-2 months

Of course, this is a tailor-made scenario. Any of those or all of those assumptions could turn out to be false thereby materially changing the outcome. I am interested in discovering the ways in which rights offers could be exploited to one’s benefit. As this is an experiment, I am simply making bets on paper. Real bets could be really risky as I am still experimenting. Do your due diligence.

Disclosure: paper trading.

2 Likes

ABI Financial Services Ltd (₹ABIRAFN)- Buyback

The company has announced a buyback of 10% of the shares outstanding - 600,000 for ₹28 each amounting to ₹16,800,000.

Reserve for shareholders - 15%

Total outstanding shares - 6,000,000

Small shareholding (Assumption) - 25%

The estimated acceptance ratio for small shareholders

- If 100% participation -14.5%

- If 75% Participation - 19.33%

- If 2/3rd Participation - 21.75%

Current market price - ₹23.9

Premium over current price - 17.15%

The stock has been hitting the upper circuit so, it might be difficult to buy the shares and similarly, it might become difficult to sell if everyone wants to dump the shares after the buyback. It’s a micro-cap so, be apprehensive about the liquidity.

Disclosure - Just an idea, not invested.

1 Like

Jaysynth Dyestuff India Ltd - JD Orgochem Limited Merger

For every share of JDIL, 14 shares of JDOL will be allotted.

Current Price

JRIL - 76

JDOL - 6.8

At current prices:

Every share of JRIL worth ₹76 can be exchanged with ₹95.2 worth of JDOL shares, meaning a 25% upside.

1 Like

Which share I should buy JRIL OR JDOL in case of this situation.

JDIL* not JRIL, sorry

Where did you find this information ? When is the last date for buying. Do you have any information ?