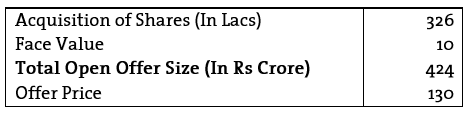

Tracking Buyback Case study of Tips Industries:

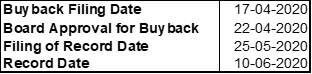

Company announced the approval of buyback dated February 13,2020. The company has fixed Friday April 3, 2020 as the Record Date for the purpose of determining the entitlement and the names of the equity shareholders who are eligible to participate in the buyback.

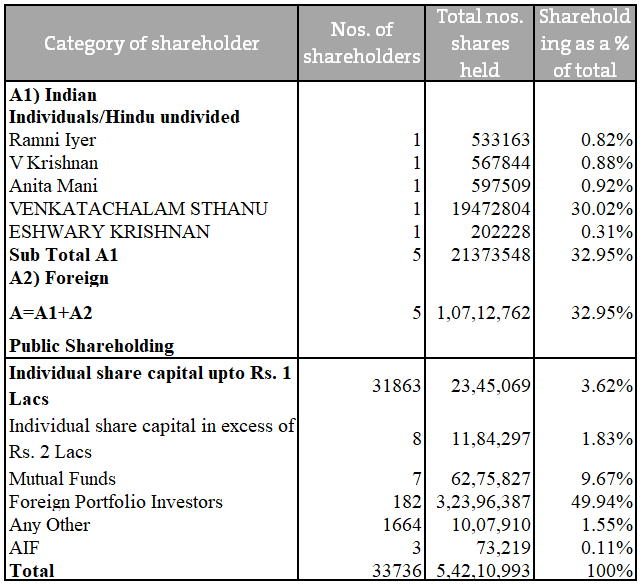

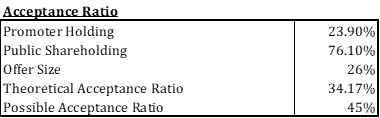

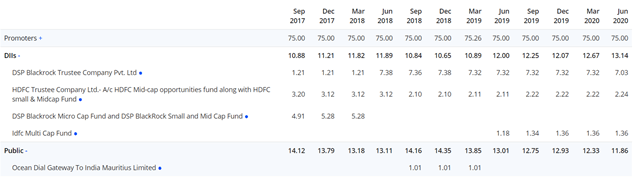

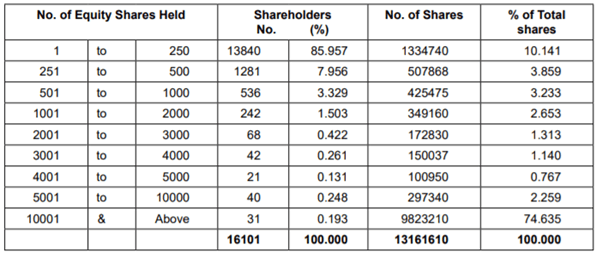

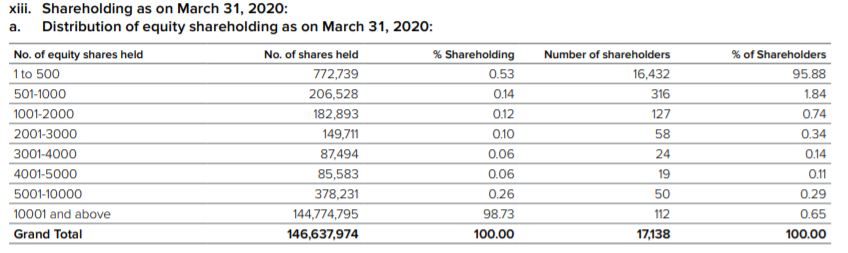

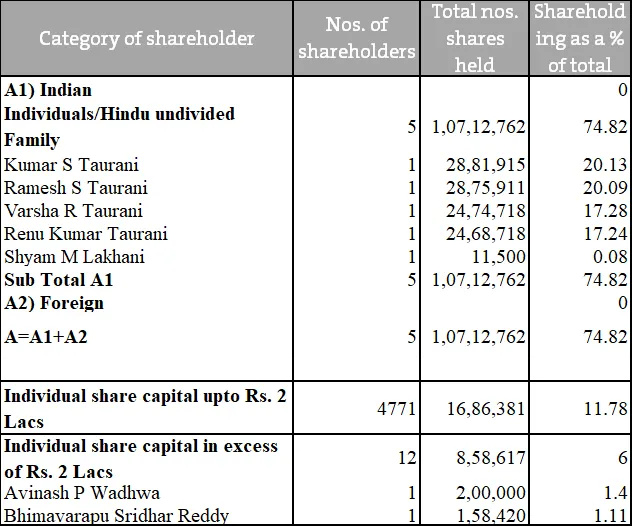

Shareholding pattern as on Dec 2019

Analysis of Buyback

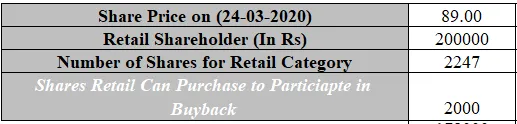

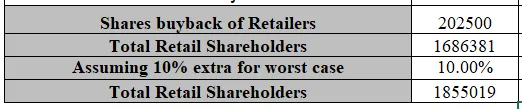

Now, the retail proportion is buybacks tends to be 15%. Hence the available shares of buyback for the retailer comes out to be 2,02,500 number of shares.

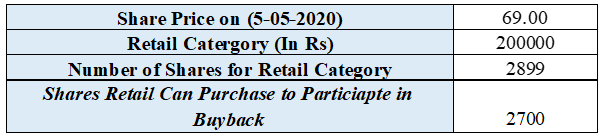

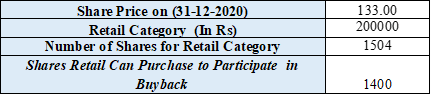

Here the retail shareholders can go for 2247 share, but considering the point that the share price can increase till buyback one can go for 2000 shares which will almost cost around 1,78,000 Rs (considering the price of 89Rs).

Not let’s consider the point, that the number of retail shareholders in Tips Industries is 16,86,381. In order to understand the data of retail shareholders of Dec 2019 (Individual Share Capital Upto 2 Lac) we have considered that there is 10% increase in the retail shareholders, considering the increase in participation of the buyback and the steep fall in the share price of the company. This turns out the total estimation of retail shareholders as 18,55,019 shares.

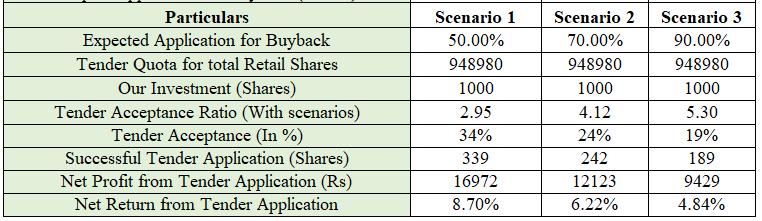

Understanding the Calculation

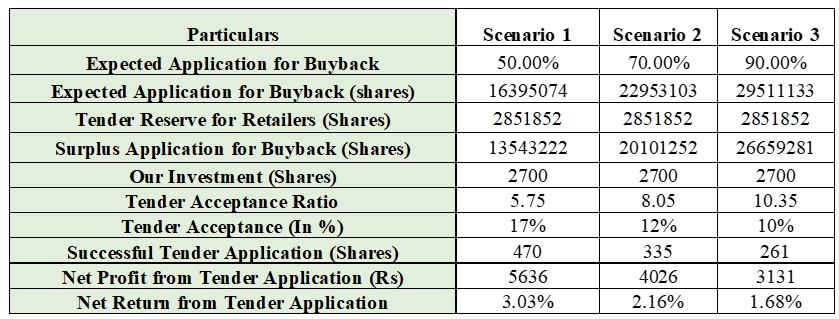

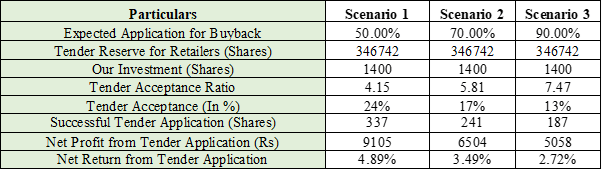

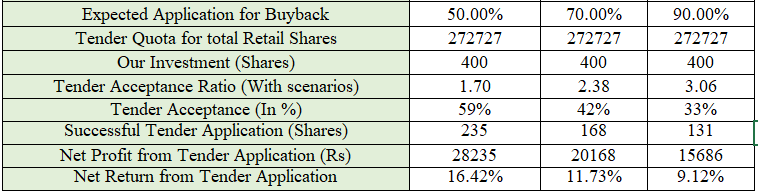

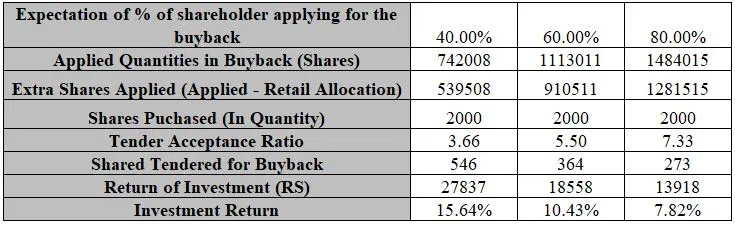

By taking scenario 1 where it is expected that 40% of shareholders apply in the special situation;

So the applied quantity of shares would be 40%*18,55,019 (total retail shares) i.e. 7,42,008 (number of shares).

Now the extra shares which would be left over would be applied quantities – retail shares in buyback (7,42,008 – 202500) i.e 4,72,727 which means shares applied for the buyback would be 3.66x.

So the actual shares which could be tendered for buyback would be 2000/3.66 i.e 546 number of shares.

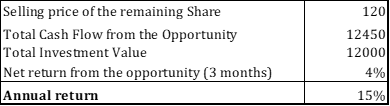

Now if we calculate the return on money it will give us;

(140 – 89) * (546) = 27,837 Rs

i.e. (buy back price – current market price) * shares bought back

And the investment return for the same would be 15.64%

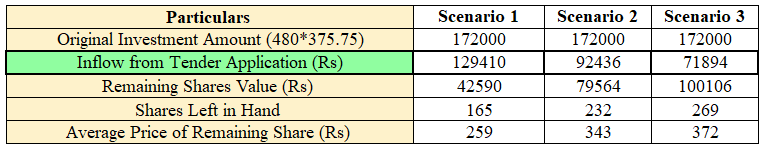

Now out of 2000 shares only 546 were tendered and 1454 shares were still left in our portfolio. So after our return from applied buyback, our total investment value in Tips Industries would be 1,01,586 Rs.

Our initial investment in the company was 1,78,000 Rs. With 40% applied ratio on buyback, the return we get from the the buyback shares would be 76,414 Rs (546 * 140) i.e. Shares Tendered for Buyback * Buyback Price.

So after buyback our net investment value in the company turns out to be 1,01,586 Rs (1,78,000 – 76,414) i.e. Total invested price – Return from applying for Tender. So the average price of our investment after buyback is 70 Rs (1,01,586 / 1454) i.e. Shares value left in buyback / Remaining shares after Buyback.

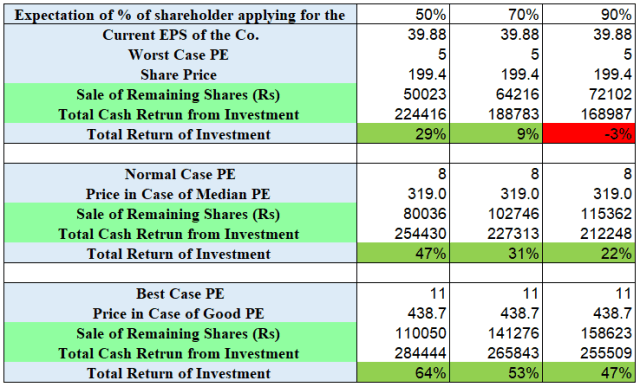

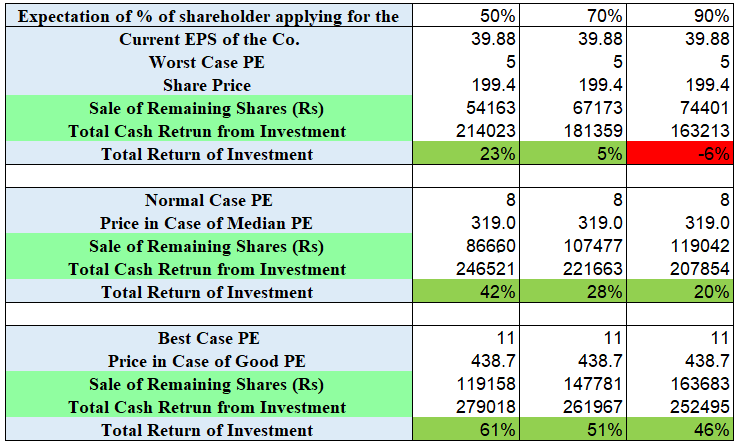

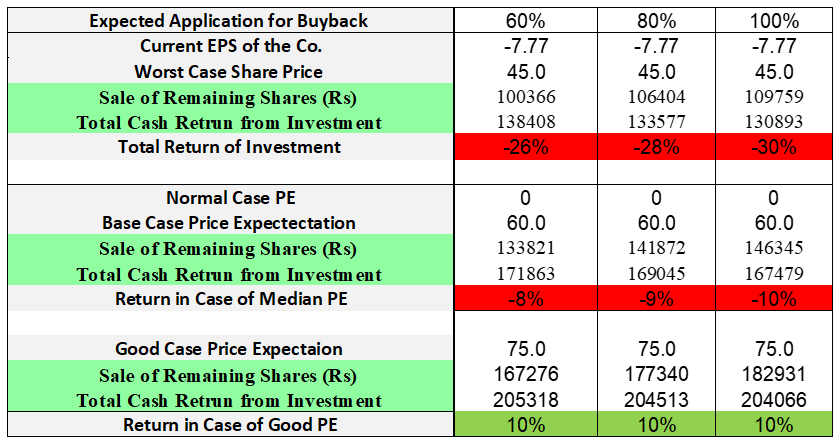

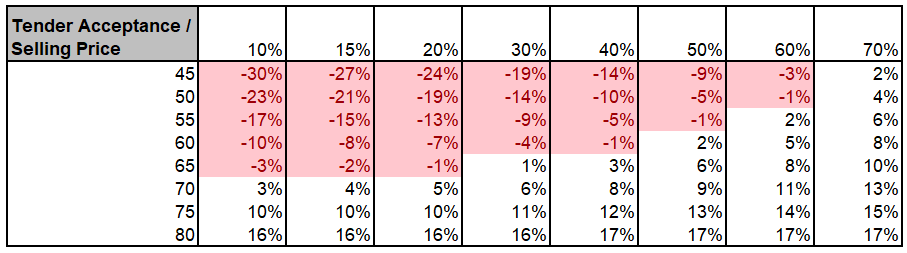

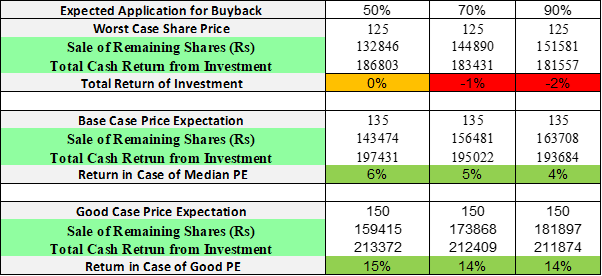

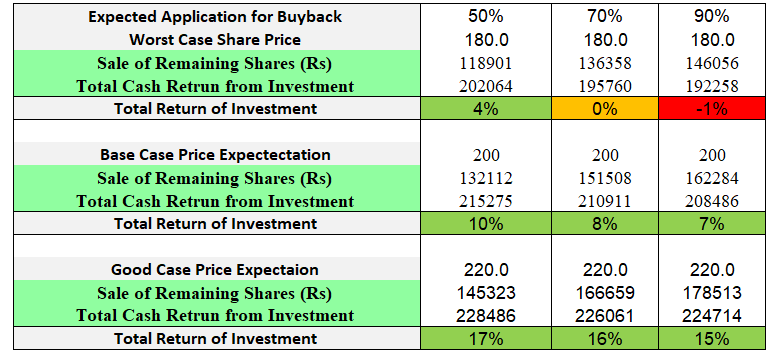

Now we have considered 3 different cases, of price of Tips Industries after the buyback. Looking at the historic price and historic PE of the company, the lowest PE of Tips Industries is 1.95. Hence taking the average of past 8 quarters during the worst period, the average PE of the company turns out to be 6. With the expected PE of 6 the intrinsic value of the company turns out to be 49.5Rs, making (-29%) return with 40% tendered application, (-36%) return in 60% tendered application, and (-39%) return in 80% tendered application.

Now taking the current PE of the company (which is 11.3) considering that the company will atleast maintain its current PE, the expected share price of the company would be 90.8Rs and the return turns out to be 30% with 40% tendered application, 17% return with 60% tendered application and 12% return with 80% tendered application.

The highest PE of the company has remain 80, while median PE value of the company is 22, while the current Industry PE is 16. But considering with the current market scenario assuming the best case PE of 14 the share price turns out to be 115.5Rs and the return turns out to be 65% with 40% tendered application, 49% return with 43% tendered application and 12% return with 80% tendered application.

As 6 out of 9 different scenario turns out to be in good favour for buyback, this opportunity indicates a positive signal, however there are still certain risk associated for playing the buyback:

Points to Consider:

- Tips Industries is a small cap company, with Market Cap of 127 crore (as on 24-03-2020), hence there is liquidity risk associated with the company.

- Current market turmoil can decrease the price of the company and there are expectations of going to the worst case as well.

- Promoter itself have tendered 12.6% of the total amount of the buyback.

Reference: here