Summary

Titan Biotech is a manufacturing company involved in producing certain chemicals and equipment utilizing a mixture of chemical synthesis, fermentation as well as core manufacturing. Their products are used in Downstream industries like Nutraceuticals, Diagnostics, Pharmaceuticals, agriculture, animal nutrition. Company did turnover of 70cr in FY20 and is classified as an MSME. Company has 2 factories (both in Bhiwadi, Rajasthan). Company has existed for roughly 30 years (since 1992). Company is benefiting from strong (though partially temporary) tailwinds due to Covid-19 pandemic and subsequent increase in demand for Viral Transmission kits (which the company makes).

Core Business

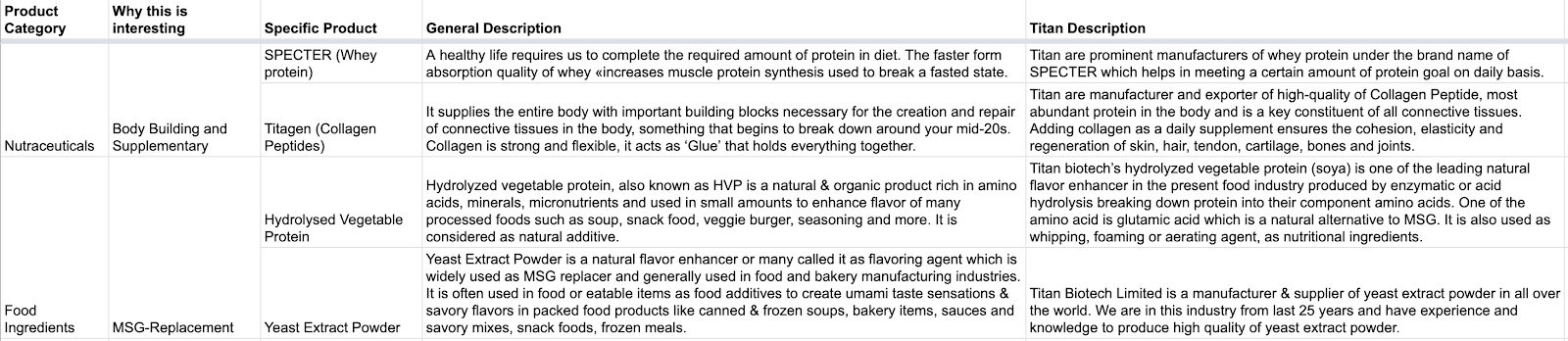

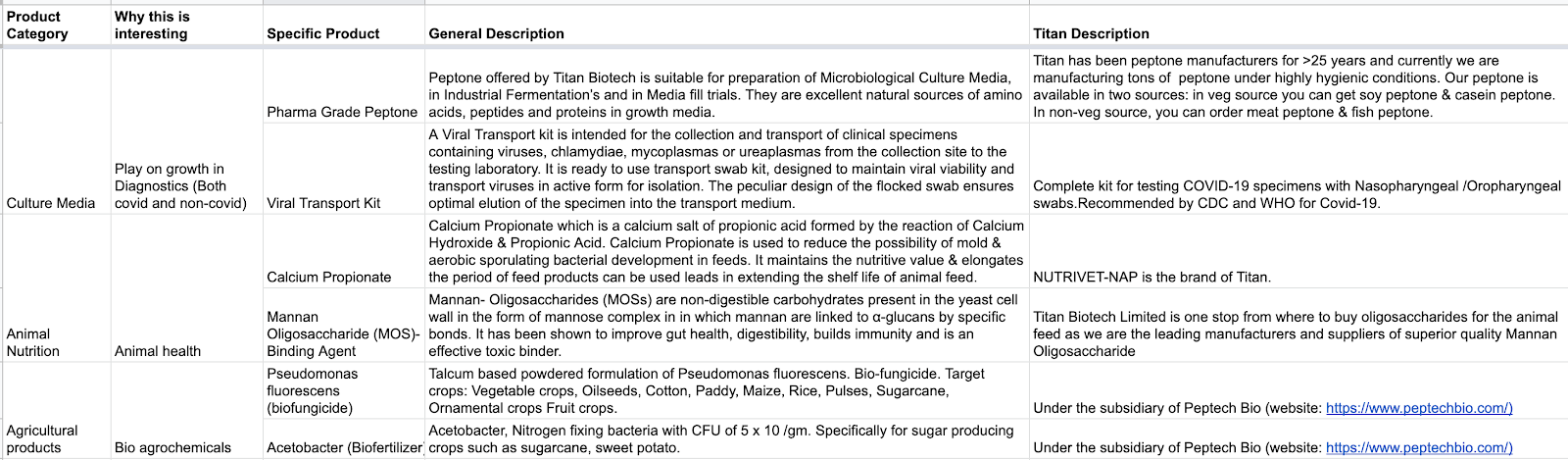

Titan Biotech Limited manufactures and sells biological products in India. The company offers food ingredients, including hydrolyzed vegetable protein, yeast extract powder, calcium propionate powder, potassium sorbate, and calcium lactate; collagen and protein products, such as specter whey protein, collagen peptides, brown rice protein, fish collagen, pea protein isolate, chicken protein isolate, soya protein isolate, milk protein, and protein hydrolysate; and nutraceutical and pharmaceutical products comprising sodium caseinate, chondroitin sulfate, hyaluronic acid, methyl sulphonyl methane, chelated minerals, peptone, OX bile extract, cholic acid, cerebroprotein hydrolysate, methyl sulphonyl methane, iron protein succinylate, medicinal yeast, and brewer yeast protein, as well as liver, meat, malt, and yeast extracts. In addition, it provides products in the areas of animal nutrition, including binding agents, chelates minerals, mold inhibitors, proteins, and yeasts. The company’s products are used in the field of pharmaceuticals, nutraceuticals, food and beverages, biotechnology and fermentation, cosmetics, veterinary and animal feed, agriculture, microbiology culture media, plant tissue culture media, etc. The company also exports its products.

Subsidiary Peptech Biosciences

As one of the leading Biotechnology based Company, we have spent more than 20 years of valuable period in particularly Microbiological segment which we have integrated with our latest fermentation technology Agricultural benefits products, have proven to increase the yield significantly which can be absorbed fast and directly by crops, improving soil structure, increasing bunch weight and quantity and other great effects. It is the one which can be relied on to reach another peak of yield record, at the same time preserving our soil in the best condition for our next generation.

Peptech Biosciences Ltd. is oriented to B2B (Business-to-Business) selling to all Marketing & Distribution Companies that can sell the products under their Brand Names in the Global Market.

Financials

| Attribute/year | 2020 | 2015 | 5-yr CAGR |

|---|---|---|---|

| Revenue (in Cr) | 79.88 | 40.71 | 0.1443197426 |

| Cost of Material Consumed | 40 | 31.38 | 0.04973918845 |

| Employee Expenses | 12.5 | 2.73 | 0.3556559146 |

| Finance Costs | 2.33 | 0.99 | 0.1867087519 |

| Depreciation and Amortization | 1.8 | 0.83 | 0.1674515942 |

| Other Expenses (Manufacturing, Operating, Administrative, Selling & distribution) | 8.28 | 3.61 | 0.1806050239 |

| Net Profit | 7.83 | 1.63 | 0.3687206878 |

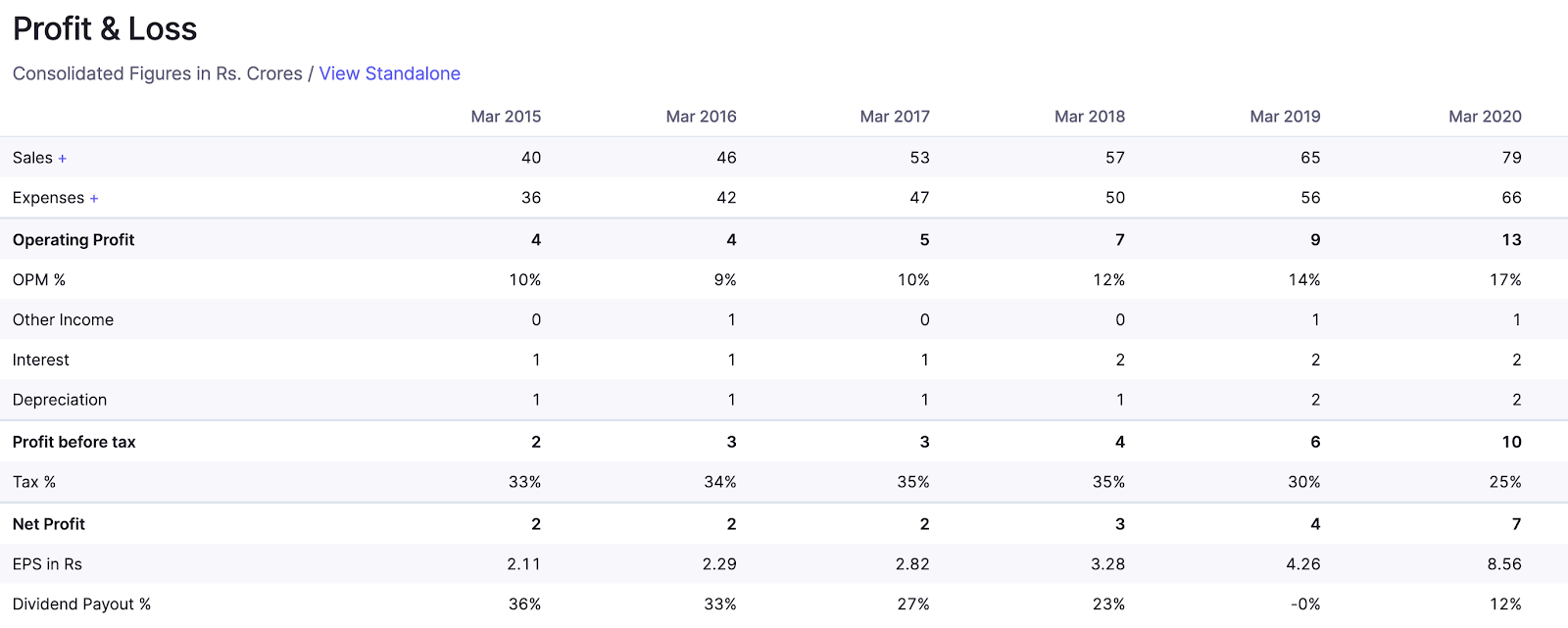

We can see that revenue has grown by ~15% in last 5 years. Profits have grown by ~37%. This is due to large % of expenses being raw material costs, which have not grown much (~5% CAGR in last 5 years). This shows that either product mix has changed, with contributions from better products, or due to appreciation of final selling price.

Management

Company/Management has given regular dividends. This shows that it is shareholder friendly.

When the earnings rose due to Covid-19, Management clearly outlined that the revenue was growing disproportionately due to Covid-19. In fact they outlined exactly how much the jump in revenue was due to Covid related sales.

Investment thesis

The company revenues and profits were compounding well even before Covid-19 hit. Company creates products which are consumed in industries with good tailwinds: agro, diagnostics, animal nutrition, human nutraceuticals etc. It remains to be seen whether any of the elevated sales due to Covid-19 are sticky or purely one-off. If the company is able go create new relationships with clients leading to sustainably higher business, then the investment thesis becomes much better.

Valuation

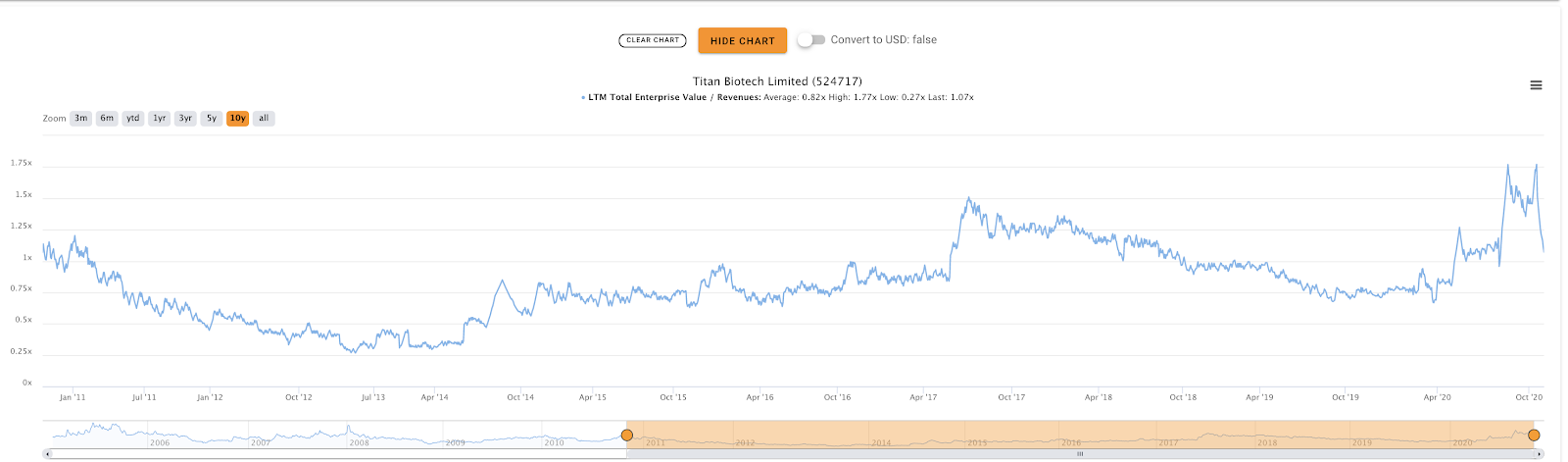

Looking at the last 10 years it has been valued at close to 0.8x revenues. This is common in small and illiquid companies like Titan. Investors pay a discount due to the high probability of failure. It is available at 1.1x sales right now, which is a bit above average valuation.

One has to take their individual call regarding valuation but I would be comfortable buying little quantities at these levels and either average up (if the business improves) or average down (if business improves but price collapses due to any factors).

Risks

- Peanut-Buttering: For a company of this size, they seem to be spreading themselves too thin. What surprised me was the absolute number of products they manufacture. As per my estimation, from all the 3 websites, this number is around 50. While some products would share processes, this is still a fairly large number of products. One risk to the investment thesis is that possibly they do not manufacture all these products, some of them could potentially just be traded. Trading companies are not as exciting as manufacturing companies.

- Scale-up: This is a small company (70 cr turnover). There is always the risk that they would not be able to scale up. Here are some articles that demonstrate in an unrelated industry (auto), how hard it has been for Tesla (US listed auto-maker) to scale up (link1, link2).

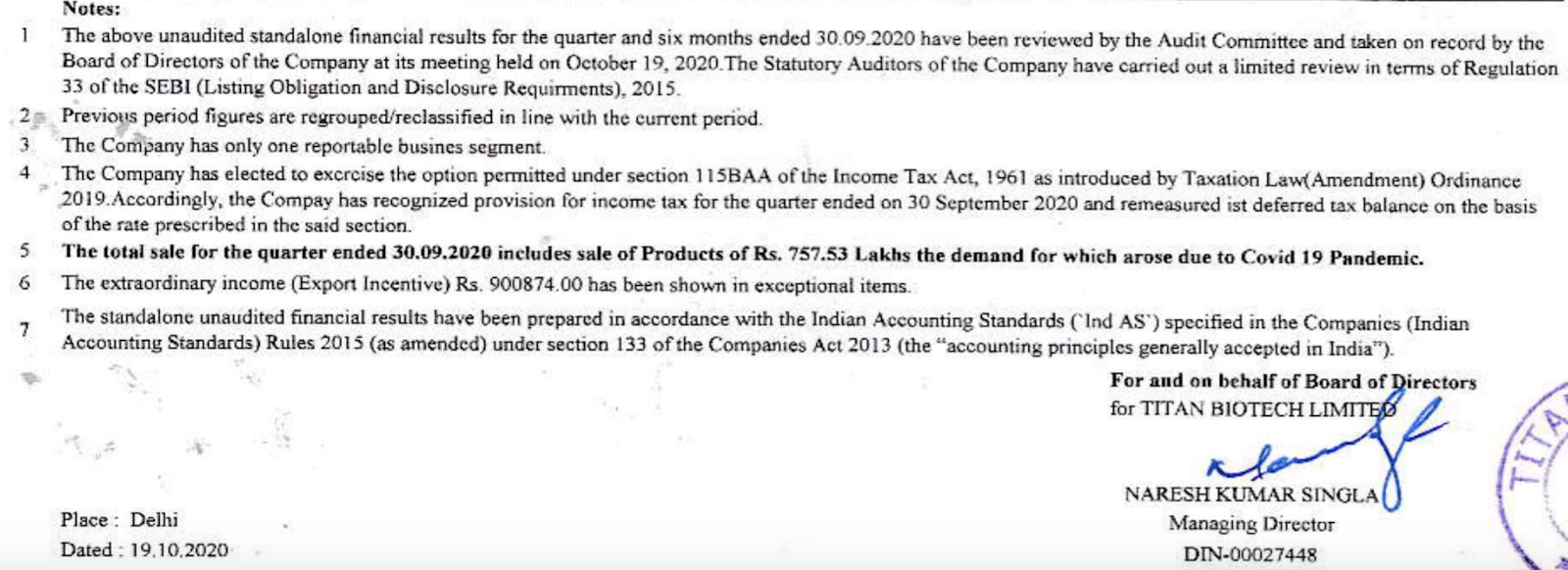

- Valuations: One key monitorable would be about the nature of covid-19 vaccine. If it turns out that Covid-19 would need regular vaccines (say twice a year for life), then the company’s revenues from TMMedia (Viral Transmission Kits) are potentially scalable since people would need to get tested regularly for Covid-19. In this scenario, the revenues would probably remain at elevated levels, in years to come. On the other hand, if it turns out 1 covid vaccine lasts a person immunity for lifetime, then these elevated revenues (7cr additional sales in Q2FY21) would go away. In such a scenario, the current TTM earnings are superficially elevated and hence, the company is available at a steep valuation compared to its usual earnings.

- Investor-Friendliness: In a small company like this one, it is also difficult to know what is going on inside the company. As the reader can see in the second post, investors had asked some very good questions about the company’s functioning, but all of them were not satisfactorily addressed by the management. This remains a risk of investing in such a small company. Unlike mid and large sized companies, we cannot expect communication with management more than twice (Annual Report & AGM) a year.

- Pricing Power: While the company claims to be a Biotech company, most of their products are commodity in nature (as per my understanding) and hence it is not possible for Titan Biotech to have any pricing power: their profitability is completely a function of demand-supply dynamics which are difficult to forecast for outside investors.

PS: I could find an older topic for Titan Biotech, but it was perhaps closed due to an incomplete first post. Hence, i started a new topic. Would be happy if we want to merge the two.

Sources:

[1]: Annual Report for FY20: https://www.bseindia.com/xml-data/corpfiling/AttachLive/75d0c16a-d332-4e20-b0f5-30f2c86cdcda.pdf

[2]: AGM for FY20: https://www.youtube.com/watch?v=FvBpXhEZgMw

[3]: Company Website: https://titanbiotechltd.com/

[4]: Subsidiary Website: https://www.peptechbio.com/about/

[5]: Company Brand (TM media) website: http://tmmedia.in/

Disc: Not invested yet, looking to add small quantities in coming few weeks.