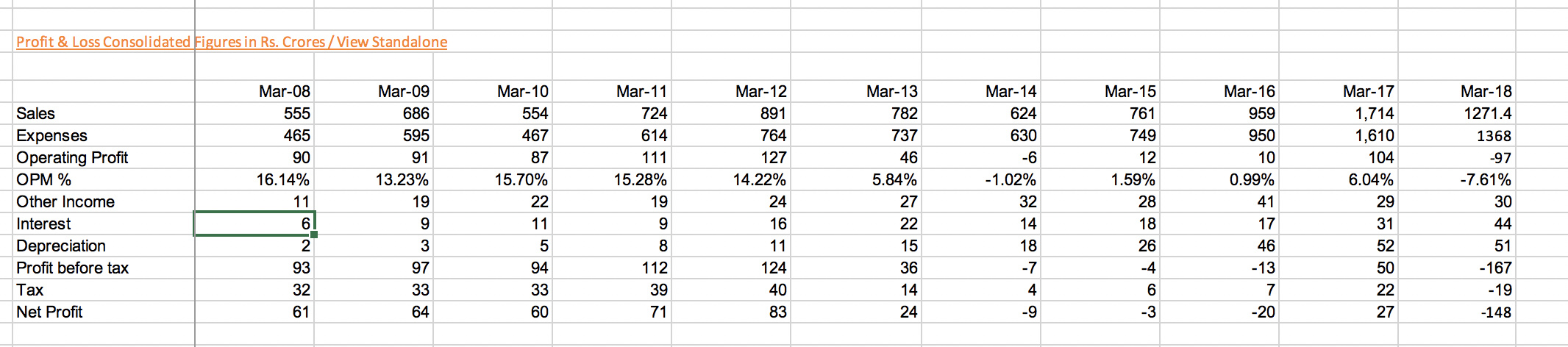

Wagon and rail equipment manufacturers have had an torrid time over the last 4-5 years with orders from Indian Railways not coming and private capex being non existent. While there have been noises of Indian Railways modernizing or doing this and that, on the ground this has not translated to actual orders for the wagon manufacturers and this has told on TItagarh Wagon’s financials as seen below.

Just note the contrast between the numbers between 2008-12 and 2013 – 18. While there have been a few mirages along the way there are some indicators this cycle is finally turning, while I will discuss this in greater detail below, just wish to make the point that this is an industry with huge fixed costs, Titagarh has been operating at like 20-25% capacity utilization over the last couple of years and operating leverage impact if and when it happens will be huge.

Now coming to the turnaround, a few pointers or green shoots if you like:

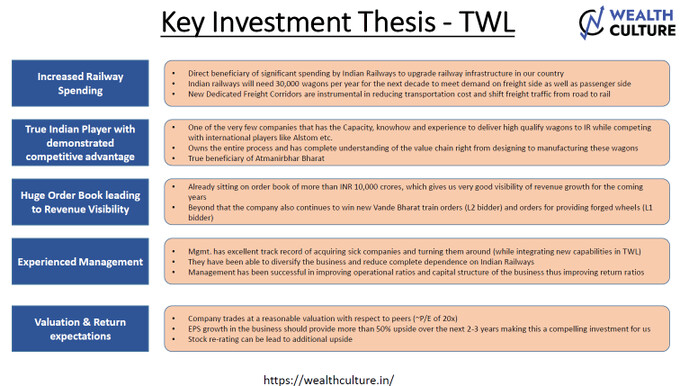

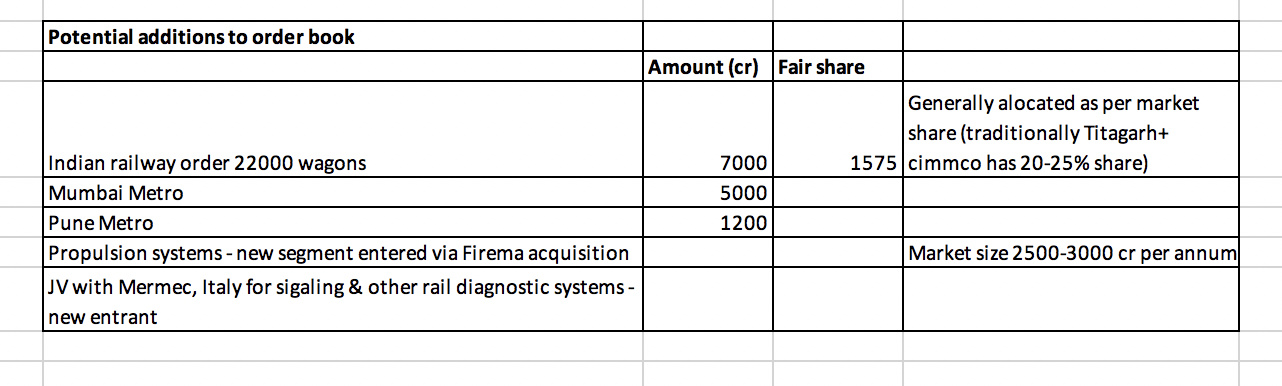

a) Firstly there have been increasing orders from the Indian railways, one tender of 10000 wagons was closed last year and another of 22000 wagons will be finalized this year. To put this in perspective total manufacturing capacity in India all manufacturers is less than 30000 wagons, so this is pretty much 2 years business for them.

b) Private sector orders seem to be slowly coming back. Titagarh is getting orders from wagon leasing companies, container train operators and this may get a further fillup with the Railways last month restarting the Wagon Investment Scheme which was discontinued in 2012. In this a customer can invest in a customized rail wagon e.g. car carriers may design a wagon that can carry more cars as compared to the standard rail wagon. Ditto for other industries such as steel etc. This private sector order fillup is reflecting in current order book, given at end of point c.

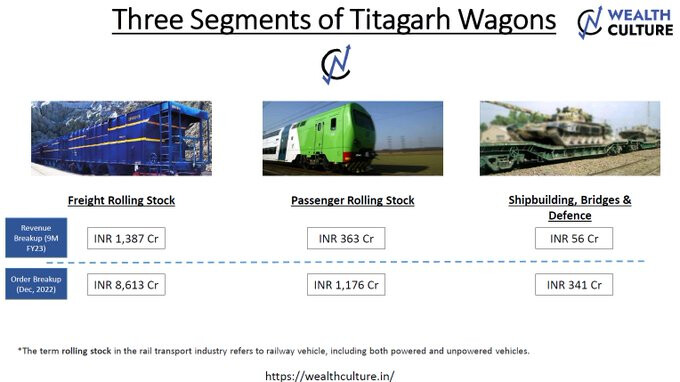

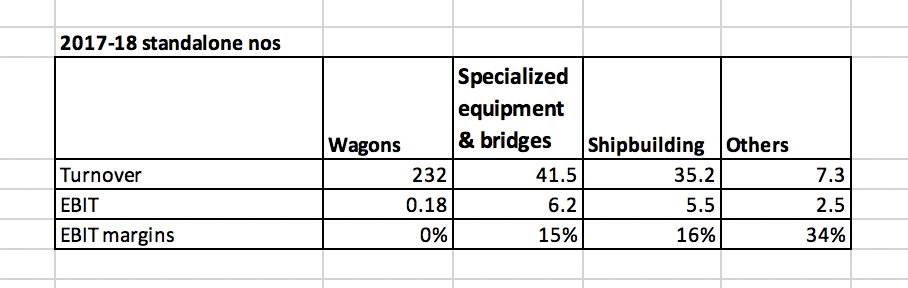

c) Titagarh has made a lot of efforts with varying degree of success to diversify itself, both geographically and segment wise. They have entered new segments such as shipbuilding, defence & construction of bailey bridges and specialized equipment, while these are smaller segments they are much more profitable, with EBIT of over 15%.

d) In terms of geographical diversification Titagarh has made 3 acquisitions, one a French company called Arbel Fauvet Rail in 2010 (now known as Titagarh AFR), in 2014 Cimmco Birla an Indian company in the same segment and in 2017 an Italian company called Firema. On the plus side all these were loss making companies picked up on the cheap without straining the balance sheet, on the minus they were bought in a down cycle and are all as of date loss making.

The huge loss in 2017-18 relates mainly to Firema, it had a lot of disputed and loss making contracts, for which provisions have been made and the losses written off in 2017-18 (this issue was known at time of purchase and is reflected in acquisition cost). The purchase of Firema though gives Titagarh a lot of design capabilities and the opportunity to participate in metro tenders as they have that experience. If played well, this can have major positive impact.

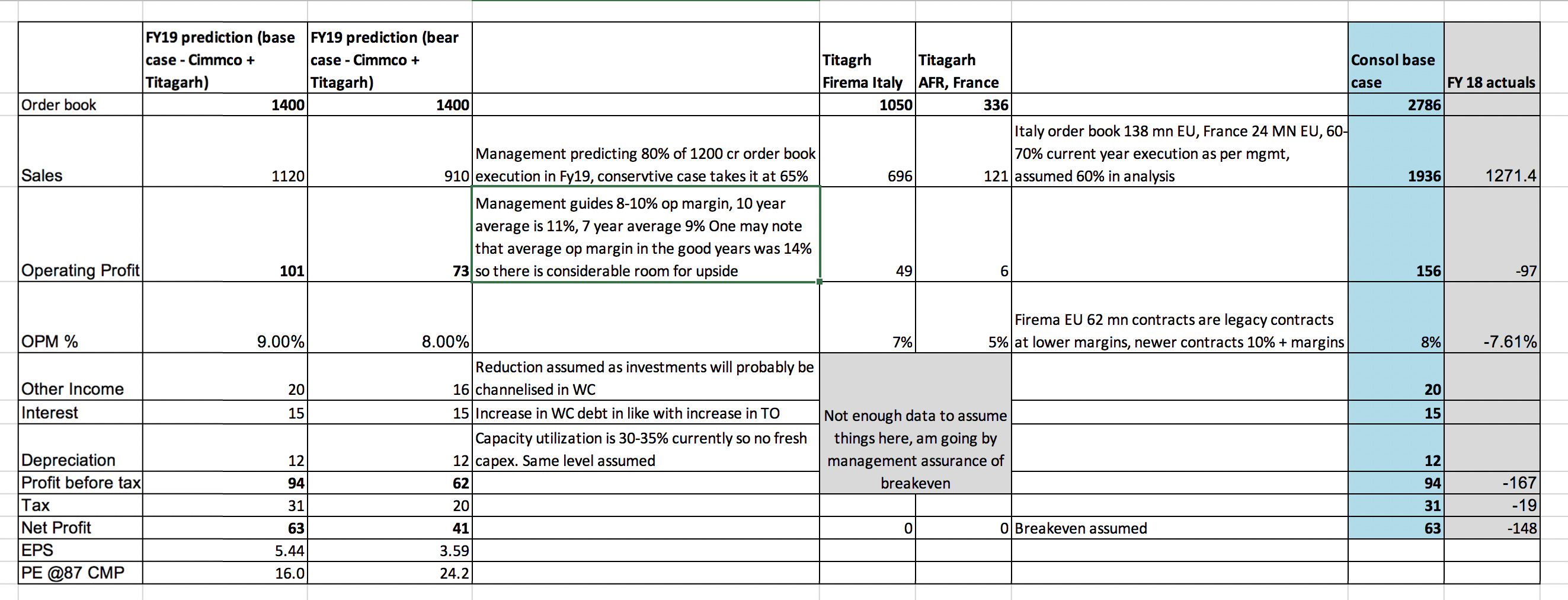

Now the main story, losses in foreign subsidiaries are stabilized and management expects breakeven at PBT level in 2017-18. Coming to the Indian operations the larger order book, 80% of which management expects to execute in the current year will turnaround financials, which is already starting to show in Q1 results. My projections…

FY19 base case frankly only shows that the company is reasonably priced at CMP, and overpriced in bear case but the point is that this is only with the company operating at 40% capacity on current order book without taking into account any revenue from the 22000 wagon order, when this comes in capacity utilization will move to 60% range (more private orders will push this even further), this should jack up operating leverage even further and make valuations compelling. Please note Indian railways distributes orders among multiple vendors and TItagarh + Cimmco is pretty much guaranteed to get around 20-25% of the order. There is no chance of no orders coming.

Second huge potential upside here is metro rail orders, post the acquisition of Firema, TItagarh is eligible to bid for metro rail tenders, it had bid for Nagpur Metro contract and lost out by margin of 0.1% to an Chinese company. However post the same GoI has changed procurement policy of the government and now mandates two things

- Minimum 75% of the coaches must be manufactured in India

- There will be a price preference of up to 20% of domestic manufacturers compared to imports.

This excludes all the Chinese players & restricts the field to 4; Alstom, Bombardier, BEML & Titagarh. As per management concall Bombardier, Alstom and BEML have the order books full for the next 2-3 years. This does not mean Titagarh will get orders but may impact bidding patterns. Also the other Indian company BEML does not have the technology so need to pay technology fee to their collaborators while Titagarh owns the technology and has a price advantage.

Quantum of potential upsides given below, only 2 metro tenders announced though given that multiple cities are going in for metro, there should be a slow and steady stream of tenders albeit at India’s Elephantine pace! There are a couple of new segments entered, not assuming any revenue from those, though there they have got the 1st propulsion system order.

Pricing

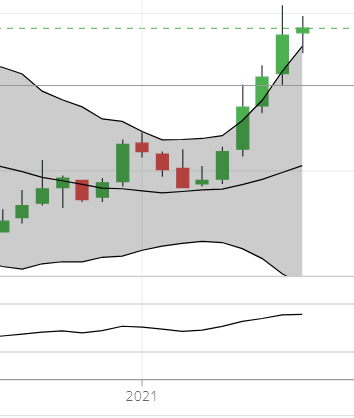

At CMP of 87 Stock is down over 50% for 52 week high, about 20% above the lows. Not cheap on current financials but once it gets the Indian Railways order or by chance a Metro order, rerating is very possible. This is more of a 12-18 month play and has it’s risks (given below) but has good upside potential and reasonable revenue visibility so IMO is a bet one can take.

Also if one sees the price chart it has a trend of shooting up mostly around budget period so if one buys around the lows there is always a trading upside coming. I have been doing this for some time!

Risks

-

Order finalization has been delayed for years, nothing to guarantee it will not be delayed for years more. But in general after this 3-4 year furlough, logically it is about time things start moving.

-

Quality issues in order execution, E.g. some technical problem in French order last year led to huge loss on contract in French subsidiary.

-

While metal prices are a pass through in most contracts, there is a delay which can impact QoQ numbers, also there have been fixed price contract in past in European subsidiary, by earlier management which caused heavy losses. Current management has mentioned they don’t want to go that road in one of the concalls.

Disc - Invested

Links

https://titagarh.in/annual-reports.php

TWL_Concall_Transcript_for_Q1_FY_19_Results.pdf (601.3 KB)

TWL_Concall_Transcript_for_Q4_FY_18_Results.pdf (662.7 KB)

From metro coaches to warships, Titagarh hits the fast track - The Hindu BusinessLine