As I was saying in my previous post, when Promoters were selling in open market it is actually quietly being picked up by others to a large extent on the same day. See below, this includes the recent sale by the promoters.

All the EPR related names are in strong upwards momentum. Stocks like GRP Ltd, Lead Reclaim, Gravita have been reacting to the EPR buzz but Tinna Rubber is moving sideways since some time. Anyone aware of what could be the reason. The management sounded very confident in the last conference call that Tinna will be beneficiary of the EPR Policy, and the revenue from the sale of credits also will grow at decent pace.

I would say. it is in consolidation mode (under ASM) after a decent run-up. I think it has lot more to offer, other than just EPR. Accumulate and sit tight may be a great idea.

Yes definitely the revenue from EPR Credits will not be very significant for the company, but the EPR norms overall will help the company improve the top line because the consumption for recycled products like RC Modified Bitumen for road construction, etc might increase. But one thing to consider is that the company mostly imports it’s raw material, and has to pay the EPR duties for that, and they still have better margins in this case than if they were to procure the raw materials locally. In this case the raw material is the End of Life Tyre.

Interesting…Tinna, listed only on the BSE, planning for a QIP. Generally, I have observed BSE only stocks have zero or near zero institutional ownership. How will Tinna QIP do?

Seems like Sales (50%) and EBITDA (100%) Growth is not justifying the share price (170%) growth. Wont be surprised if the price correct by 30-40% from here. Dis - Not Invested.

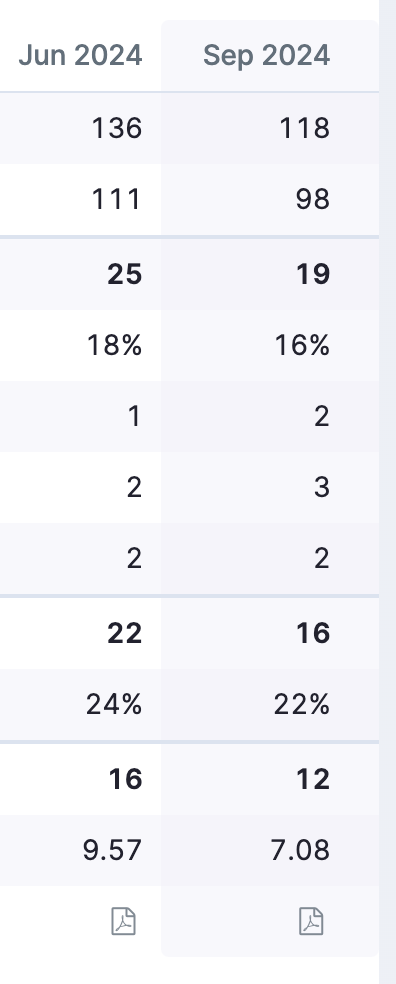

The result looks good when compared on YOY base but with respect to previous quarter, there is reduction in sales(-13%) and margins have also reduced by 2%. This has impacted net profit by 40% wrt previous quarter. This i believe is the reason for lower circuit for last couple of days.

Overall I don’t see the fall continuing for much as result are still decent, It has corrected a lot in last few months and the future prospect looks bright considering tailwinds and expansion plans company have.

Disc - Invested on current levels and looking to invest more.

I recently broke down some key details of this q2 results on twitter. I feel company has solid management and roadmap ahead.

Road infra growth is inevitable along with the fact that every monsoon half of our roads are washed away.

In rubber with bitumen supply for road infra Tinna rubber is monopoly with 60% market share as mentioned in thier investor ppt even after that they are expecting more growth in this segment.

Disclaimer : Added first installment today so views maybe biased.

Honestly its a wrong comparison in my view. QOQ makes sense when you compare companies whcih have annuity business such as banks, Insurance, NBFC, IT but for manufacturing companies its a wrong parameter. In products business qoq comparison does not make sense. Honestly i was expecting your response as weak qoq numbers, not surprised. Its strictly my view and you if you dont agree feel free to ignore.

Makes sense QoQ comparison is not the best way to compare here but for such less market cap I feel atleast there should be no degrowth if not growth in some quarters. Although I do not mind such numbers once in a while as it let’s you accumulate some stock at really resonable valuations.

Also I did not find any anomoly in balance sheet and ppt shared by the company if that is what you were seeking to know. Little bit of margin reduction due to some esops to employee but overall management has done well to keep the ship tight.

I found two red flags in their current result 1. their EPR credits are not realized and are notional based on the company’s base case assumption. 2. without EPR, their Q2 profit before tax is ~4 Cr which is much less than Q2FY 24 PBT of ~10 Cr