Hi @rinkupranjan,

Did you reach out to the company regarding this huge anomaly?

I may be wrong, but the only thing that explains the variance is perhaps the changed classification of Crumb Rubber in the infrastructure tower (refer slide 10 of the FY24-Q1/H2 presentation).

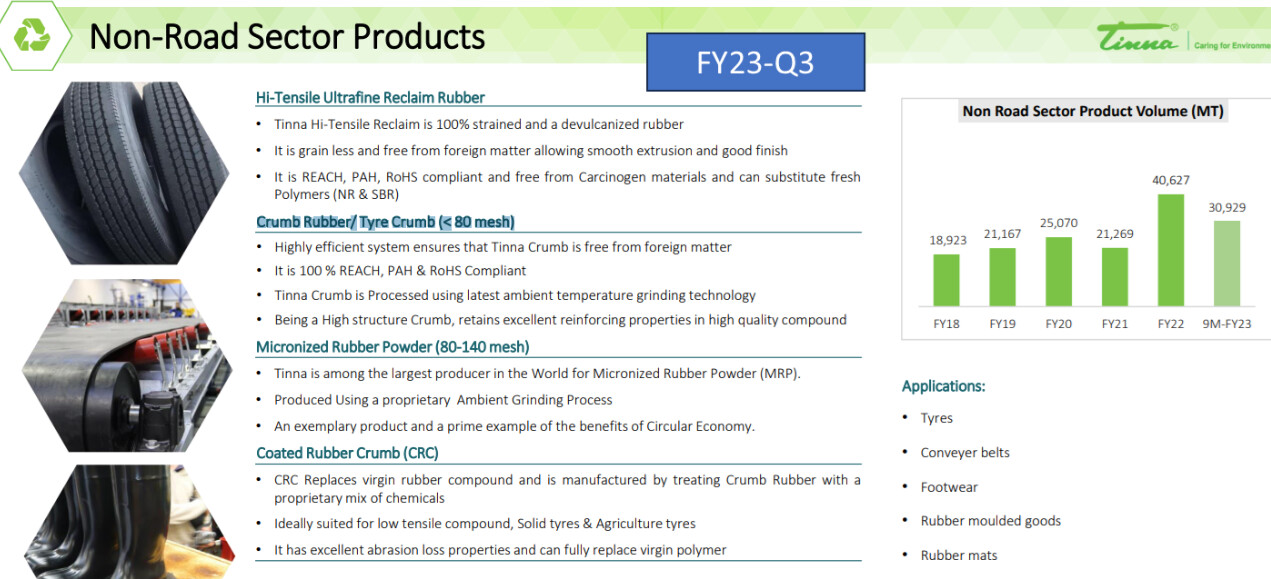

Earlier, “Crumb Rubber/ Tyre Crumb (< 80 mesh)” seems to have been classified under Non-Road (refer slide 19 of the FY23-Q3 presentation).

This explains the infra revenue anomaly, but does not explain the weight split.

Thanks,

Gautam

Hii…

Can any from industry share price trends of Styrene Butadiene rubber raw material for tyre industry.If possible share raw material changes compared to last year

Check out the growth of crumb Rubber globally and Tinna Rubber is a well known player.

Crumb Rubber Market Share, Demand, Analysis 2023-2032 | The Brainy Insights.

Industry and Management discussion at Valorem Meet

3 Likes

Pointers from Tinna Rubber & Infra’s Q4FY24 concall (May 28, 2024)

On capex:

- INR 35-40 crores of capex & process improvement spends expected in FY25

- Debt is being serviced in an efficient manner. Management considers debt as an excellent option for raising funds. Their balance sheet can support it and if needed they will raise debt for any capex requirements as the need arises.

- New plant at Varle can generate INR 75-100 crore topline when operating at full/optimal capacity. The Varle site (it is a 13 acre site viz a viz Chennai which is 5 acres) also has additional space to ramp up operations significantly if needed in the future

- INR 30-35 crores spent on the capex of the Varle plant. The Varle plant can crush passenger car radials which their other plants can’t do.

On growth:

- From a macro standpoint demand for all their product lines remains robust especially the infra sector.

- FY25 guidance is 500 crores (~120 crores a quarter needed to achieve the target).

- FY27 target remains at 900 crores

- 25% cagr growth quoted till FY27 can have a further upside if everything falls in place. More roads are using rubberized asphalt. If the pace of the adoption continues like the last 1-2 years there is a chance they may grow faster than projected.

On margins:

- Setting up a solar plant by Q2FY25 to save energy costs. INR 1.25 crores to be saved annually once the plant is up and running.

- Red Sea impact costs (~10% increase) being passed on to their consumers. Figuring out other ways to hedge against the cost increase.

- Margins have improved due to multiple things like, dealing with better customers - ones that value better service and delivery, better product mix and product lines and operational efficiency.

Other pointers:

- Exports as a % of revenue was 8% in FY24 (INR 24 crores)

- EPR gains first reflect in the topline and then it flows down to PBT. EPR generated for FY23 (~50,000 - 75,000 credits) resulted in sales of INR 6.6 crores in FY24. EPR for FY23 was not entirely sold. The sale that has been made is a direct sale to an OEM manufacturing tyres

- EPR for FY24 is still to be received by the company.

- Oman facility is operating at 80-85% capacity. Not much growth expected here and the business is more for generating cash flows. They may expand to other countries too if good opportunities come up

- 75-80% capacity utilization of plants for FY24

Disc: Invested as a tactical 3-year bet. The recent run up in the stock has made it a decent sized bet in my pf. Will continue to hold as the management has been executing very well.

10 Likes

Insightful video on tyre recycling:

6 Likes

I think honorable minister Nitin Gadkari back as minister for road transport and highways is a big boon for this company.

Discl: Invested and biased.

1 Like

Thanks for sharing this video. This is such a beautiful eco friendly business with so much potential for further usage of end of life tyres.

This video is a must watch for anyone invested in this business or looking to learn more about it. Honestly, I’m surprised no mutual fund has entered this business yet considering the ESG theme/criteria it fulfills.

Disc: Invested

1 Like

That is because of small equity capital and promoters hold the max 73.5% holding, leaving less on the table for FIIs and MFs.

3 Likes

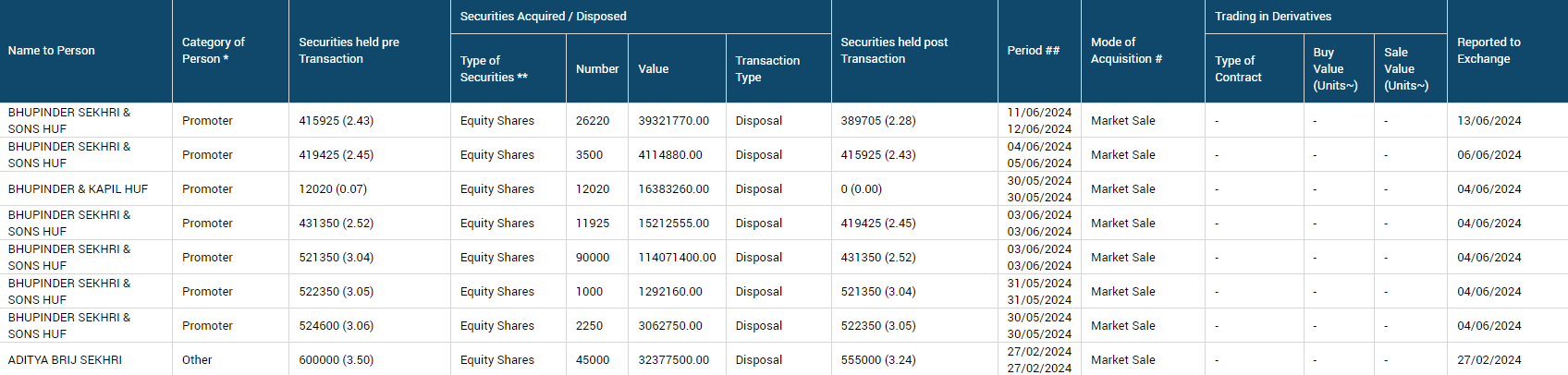

So far the promoters and others have sold 1.9 lakh shares in the open market in 2024. So is it a normal profit booking or something is cooking?

While 1.9 lakh sale appears to be very insignificant as the promoters still hold over 73% in the company. On the other hand, it is to be noted that, about 90000 shares were bought by PGA securities on the same day when the promoter sold.

Could anyone write to the company to find out reasons for selling in the open market. Thanks.

1 Like

Company surely has a foreseeable good future with clear direction by management. Just one apprehension about valuations…Its at PE of 65 while average last 5 years PE has been around 22. How much of the future growth is already priced in? All other metrics are coming in excellent territory, Debtor days, Inventory days, ROCE…all are good.

At this juncture, the stock is surely overvalued (at least to me) and I won’t have the courage to top up on it. In any case, I have a decent sized holding and I’m very comfortable holding on to it, even if the valuation goes higher.

Where the market participants take the valuation of the stock is anybody’s guess. Even when I entered the stock it wasn’t cheap per se. I entered ~4-5 months back when it was trading at a PE of 35-36. However, I figured the company is placed very nicely on the growth front with sales, margins, profits and return ratios set to grow/improve meaningfully. Add to it the EPR revenues that flow directly to the PBT without an additional rupee being spent in expenses by the company. Furthermore, the company is experiencing some amazing macro tailwinds (thanks to the aggressive road construction/infra development taking place in the country). And lastly the modern themes of ESG investing, eco friendly companies focused on recycling etc. warranting more attention made it a no-brainer for me.

On the valuation front, my math was simple. The company was poised to grow its topline by ~35% + CAGR over a 3-year period with margin expansion leading to faster profit growth and improving return ratios. With all the other pointers and tailwinds mentioned above my thought was it trades at a PEG ratio of ~0.70-0.85 and that to me was acceptable as I would double my money in under 3 years (assuming everything falls in place). That the market has re-rated the company to a higher multiple is just a pleasant surprise. Who knows it may be even more irrational and take it to higher multiples.

For the time being, I’ll continue to hold it and keep monitoring the company’s business performance and the stocks valuation to decide further course of action.

Disc: Invested as a tactical 3 year bet. 3rd largest holding in the pf.

10 Likes

This looks like an alternative to Tinna Rubber’s product. Or do they go hand in hand?

“The government is focusing on various alternatives for road construction, including recycled waste material and molasses.”

Thanks for sharing.

Any listed companies working in the space of Bio-Bitumen?

Tinna does not produce Bitumen. Tinna produces Crumb Rubber Modifier (CRM) which is mixed with Bitumen (around 12 to 15 %) in the top layer to bring added strength to the road and increase its life. The technical properties of this bio-bitumen - whether it needs the same amount of CRM or more or less or not at all are not mentioned. Whether this is a threat or opportunity for Tinna depends on that.

7 Likes