The stock did not shoot up because of announcement of sale of hydrogen- it shot up on the news of 50 percent stake sale in the subsidiary of Middle East, showing managements commitment to reduce debt. The management has been very clear that hydrogen is proof of principle and a prototype that has got approved - and as of now because of the ambiguity in future of fuel sources of automotive engineering, management is being prepared to have first mover advantage. The extreme short term bearish or sideways view may be correct because it seems the market doesn’t like 15 percent guidances nowadays, but the company is exactly walking the talk and at the exact same timeline they said. The concall had terrific clarity about growth runway and management vision. The new capex will come online this year and may be a trigger for rerating - also the management said that the LPG order may be announced in 15 days or so because they are already continuing to deliver - that may also be a short term trigger for an upmove. It surprises me that all news is in public domain and yet at announcements and results we keep reacting at 4-5-10 percent stock movements.

Q4 FY2024:

• Volume Growth: 19.3% YOY

• Net Debt at 591cr - reduced by 117cr - total debt at 745cr

• Share of Established v/s Value added products: 74:26 (P.Y. 77:23). Value added products grew by 32% in FY24 as compared to FY23, while established products grew by 12%.

Value added products grew by 48% in Q4FY24 as compared to Q4FY23, while established products grew by 10%. Margins 18.2%

IBC (Including Inner Containers) sales 622cr vs 501cr.

Composite Cylinders (LPG cylinders and CNG cascades) = 518.2cr vs 345.7cr (49.9% growth)

• Order book- PE Pipes = 125cr. PE Pipes sales = 251.4cr vs 204.6cr. (22.9% growth)

• Order book- Composite Cylinders (CNG Cascades) = 175cr.

• (RoCE) has improved to 16.4% in FY24 and the management intends on achieving an RoCE of ~20% over the next 2 years

• Development of technologically advanced TBS (Transparent Container Batteries) and E-Rickshaw batteries in Lead Acid and Lithium, by NED Energy Limited (subsidiary) at their existing unit. TBS is a type of lead-acid battery commonly used in power segment for backup power systems and, other applications requiring reliable and long-lasting energy storage. Development of these batteries will take around 6 months’ time and has a huge potential market ahead

• Due Diligence process is ongoing for disinvestment of 50% business in Middle East. We estimate to complete this disinvestment transaction by June 2024 including signing of the SPA, unless mutually extended by both parties.

CONCALL NOTES:

• 15% Volume growth for the next 2 years – EBITDA margins to improve (In existing business – no LPG or Hydrogen sales and expansions considered)

• Increase in freight cost due to geopolitical issue in the Middle East region and due to high business in the PV pipe division, that also affected margins by 10 or 20 basis points in the last quarter

• HYDROGEN CYLINDERS: We should get approval for manufacturing in the next 2 months’ time.

• AUTOMOTIVE SECTOR: Automotive sector approval itself takes 8 to 12 months’ time. So, we have initiated talk with them, design taking everything.

• Now every day, we are hearing that so many CBG plants are also coming and Reliance, Adani, many people are working on CBG plant, they will need our type of the cylinder, CNG cylinder

• Composite cylinder business: Which is currently in the '23-‘24 around INR300 crores, which we are projecting in the next 5 years’ time, it can be INR2,500 crores or INR3,000 crores our company’s own business.

• Lpg cylinder: Two years back, the price difference between the metal cylinder and composite cylinder was more than 30%. Today, it is reduced to almost around 15%. As the volume will increase, we can also offer you very, very competitive prices of this.

• FY '25 interest cost to be around INR70 crores. (So 30crs benefit flowing directly to bottomline, which is 10% of FY24 bottomline)

• Variance in the EBITDA margin will be up to 50 basis points because whenever price increase, actual fluctuation, it takes time to pass on with the gap of 25 to 30 days. You will not find any much variance into the period end. We try to keep target EBITDA margin in the range of 13.5% to 15.5%, we are keeping the range depending on the established product mix and the value-added product mix.

• LPG CONTRACT RENEWAL: New contract is already in process. Everything is finalized and quantity, I will be able to let you know in the next 15- or 20-days’ time.

• CNG cascade competition: First, when it comes to the price difference, the price difference between the cascades that we offer in the market, and the one that is being offered by importing these cylinders and then assembling them here, they are in the region of somewhere between 15% to 18%. So, we are in a position to provide that advantage to the buyers, and being a domestic Class 1 supplier as they call it in the government terms, there is an automatic preference coming to us. That’s number one

Access to this technology is very difficult. There are very few people who manufacture these products globally. We fortunately have been in the composite business for the last 20 years. So, we had the good experience of manufacturing these cylinders and we are able to graduate much faster.

• As of now, we don’t see any domestic competition in India and we are fairly confident of great growth in the next few years at least.

• We don’t want to keep the assets idle as we have experienced in LPG cylinders. We have invested 10 years back, but government took interest and started buying since last 2 years, 3 years only. So, it is better to go slowly. But yes, always, we will be the first mover advantage. As we are keeping ourselves ready, I tell you hydrogen cylinder, we are developing it. We will be the first advantaged. We will have a first mover advantage. But we know that requirement of hydrogen cylinder is going to come after the – at the end of the '25, '26 only, not now, but we’re keeping ourselves ready. We are doing investment for that.

The turnaround from a underperforming business to a good one is complete. The management has walked their talk and made many of us rich in the process. (From sub 11% ROCE to 16% ROCE along with reducing debt, From faltering growth to steady growth)

The journey from a good business to a great one begins. The growth drivers are in place. Only part remains is the execution and I have a high confidence on the management on doing so. (ROCE of 20%+ along with negligible debt and consistent growth)

If they can indeed deliver on their potential of 2500-3000cr revenues from CNG segment, along with LPG orders from other 2 PSU’s and Hydrogen segment begins delivering growth, then this can be a 5-10 bagger still from current price in the next 5 years.

(Supreme industries trades at 3 times the valuation multiples of TTPL. Which is justified due to higher ROCE’s, lower debt etc. But if TTPL delivers on it’s strategy, then we can see valuation expansion here as well)

[Slide 1 - Time-Technoplast-Monthly-Pick.pdf|attachment]

(upload://4Y1S5sjL64X3UPUz1gy9Vx8eQIg.pdf) (1.1 MB)

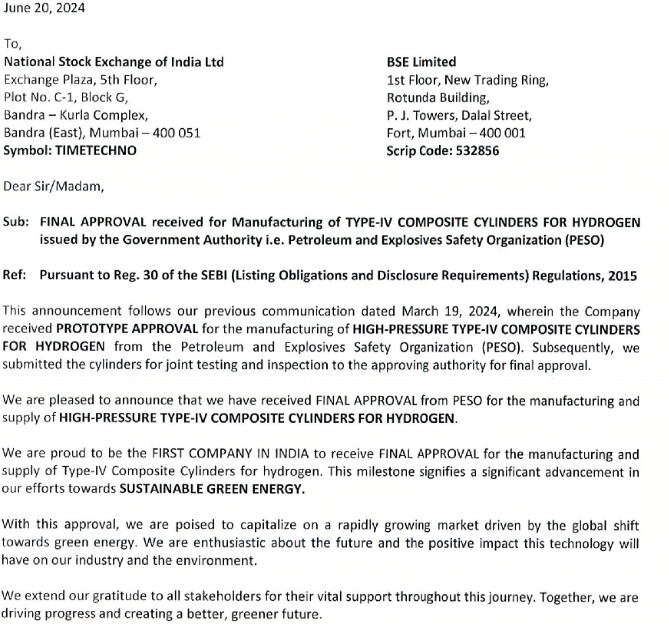

Time Technoplast : Co Says Final Approval Received For Manufacturing Of Type-iv Composite Cylinders For Hydrogen

My overall impressions from FY24 results:

Divestment - After small divestment in West Asia (Middle East region), no more selling of overseas business expected in FY25. India facilities/land will be consolidated and some real estate may be sold with proceeds mostly used to pay off still considerable debt. With prolonged due diligence activity for overseas business divestment not resulting in anything, I’ll wait for final figures on real estate sales, ignoring management’s current numbers for now.

CNG Cascades - FY25 sales expected to be ~80-85% more than FY24 with same % profitability.

While a current customer (Confidence Petroleum) claims to be ready with Type-4 CNG Cascades by this year, it is unknown how near they’re to PESO certification (atleast 1.5 years process). Surprisingly Confidence Petro has good amount of CNG Cascade Type-1 business both stationary/mobile with enterprise customers like BPCL. Not sure if/why Time Techno hasn’t cracked this segment.

LPG - going on BAU mode with expected IOC repeat order (~7.6L) utilizing most realizable capacity of 1M. Similar revenues for FY25 as FY24.

IBC - After revenue growth with big capex last year, expect a slightly smaller growth.

Overall a lot better than expected results, pleasantly surprised that company beat my estimate of 650-675 crores FY24 EBITDA. Expecting ~800-820 crores EBITDA this year, driven more by CNG Cascades expansion playing out + earnings improving as debt reduction leading to lesser interest out-go.

Company had low utilization of LPG Type-4 capacity since 2013 when they launched. While they expanded capacity in 2017, still it took till 2023 for full utilization. Don’t see LPG being growth contributor for atleast another year.

Company has clarified in last cc that currently there’s no hydrogen cascade use-case and they’re just being ready. Not sure if today’s stock jump is just due to hydrogen cascade PESO certification news. FWIW hydrogen narrative really helps for visibility.

Discl: Invested since 2018, added more till 2023, big part of portfolio both by cost(16.5%) & value (21.6%).

Confidence Petroleum is not trustable. You can go over their last 2 years’ PPT they are claiming the same but have not reached anywhere.