Time Technoplast -

Q3 FY 26 results and concall highlights -

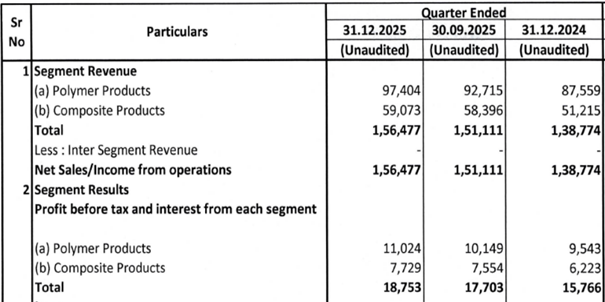

Q3 outcomes -

Revenues - 1567 vs 1389 cr, up 13 pc

EBITDA - 236 vs 202 cr, up 17 pc ( margins @ 15 vs 14.6 pc )

PAT - 126 vs 101 cr, up 25 pc

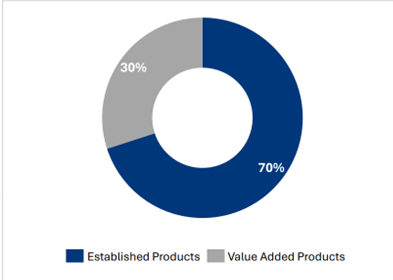

Value added products grew by 19% in Q3FY26 as compared to Q3FY25, while established products grew by 11%. The company’s focus remains to increase the share of value-added products in its revenue and improve margins

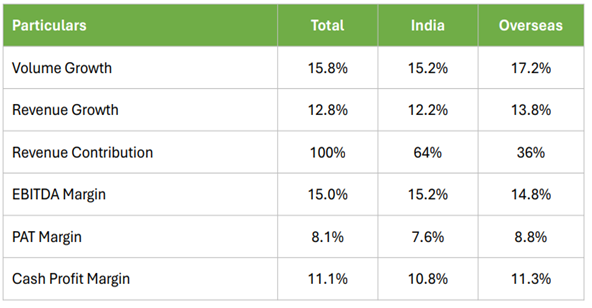

India volume growth @ 15.2 pc

Overseas volume growth @ 17.2 pc

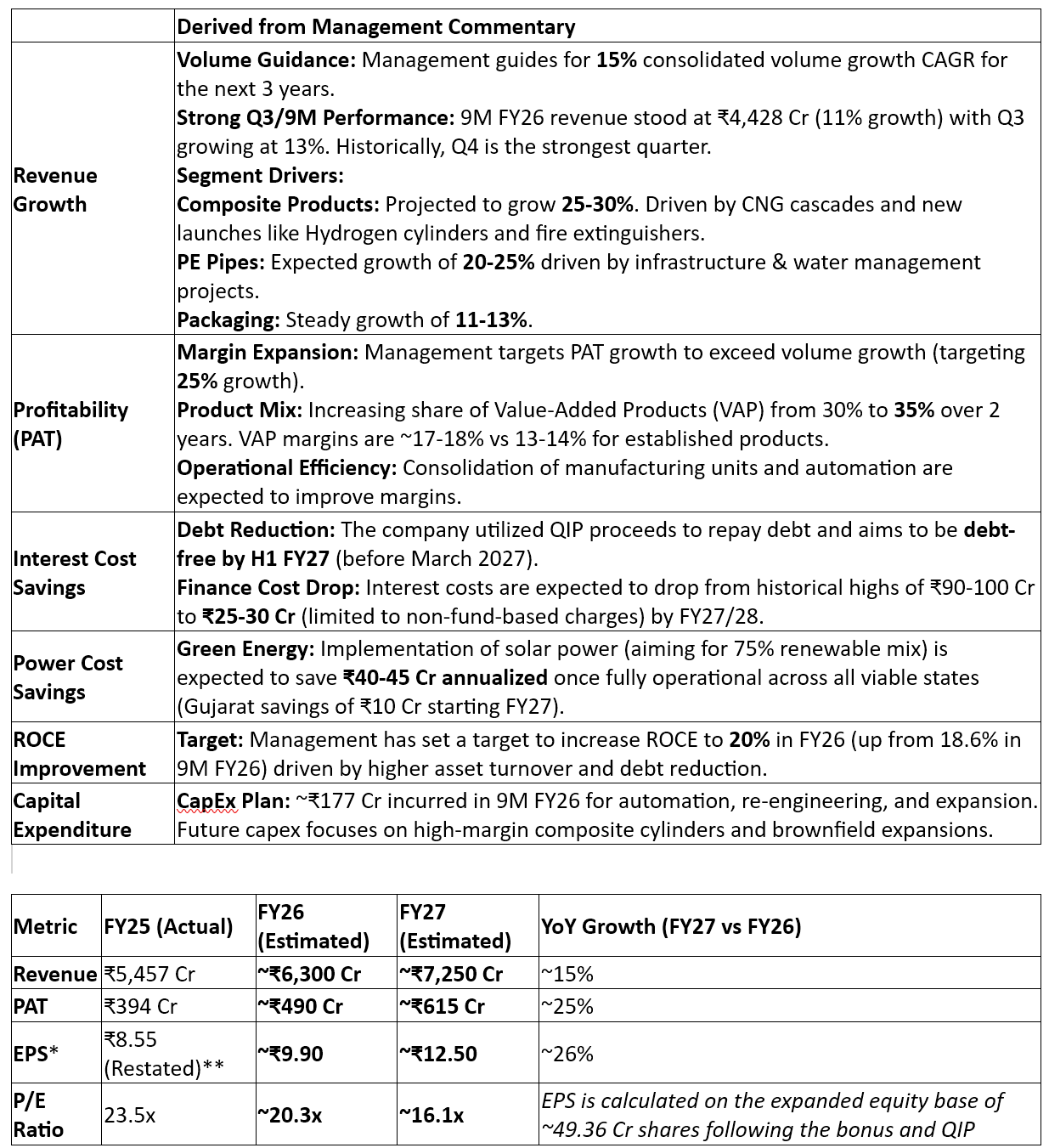

Debt on books @ 266 vs 646 cr - debt reduction of 380 cr led by infusion of QIP funds

9Ms FY 26 capex @ 177 cr

9M breakup of India : Overseas business @ 64 : 36

Composite Cylinders witnessed 23 pc growth in 9Ms FY 26

Notes from previous Concalls -

QIP - successfully raised Rs 800 cr @ Rs 201 / share in Q2

Equity dilution caused due a/m QIP @ 8.7 pc

Have developed a low cost, low maintenance, high performance battery for E-Rickshaws named - E Start with SELINIUM. Current mkt size of such batteries is 6400 cr / yr and is expected to grow @ 25 pc CAGR for foreseeable future

Have set up a new subsidiary - TIME ECOTECH - focussed on recycling and reprocessing industrial packaging. Will invest 120 cr over next 3 yrs in this new initiative

Committed to source 75 pc of its energy requirements to Solar sources - to reduce its energy costs. This would result in annual energy savings of 20-30 cr

Products under development and approval -

• Composite Fire Extinguisher

• Power Sector OP-Z Batteries

• Composite CNG Cylinder of more than 200 litres capacity

• Composite Hydrogen Cylinders

• Composite LPG Cylinder of 14.2 kg or higher capacity

OP-Z batteries (Ortsfest Panzerplatte - Stationary Tubular Plate Flooded batteries) are high-performance, 2V industrial-grade lead-acid batteries used extensively in the power sector for critical backup and energy storage. They are characterized by a long service life of over 15-20 years and excellent deep-cycle capabilities

Utilisation of QIP funds -

Reduced debt by 380 cr

Purchase of machinery and equipment - 125 cr

Investment in Time Ecotech - 55 cr

Money kept for inorganic opportunities - 240 cr

Company received approval for manufacturing of Type -3, fully wrapped, fibre reinforced composite cylinders. These find applications in storing hydrogen in fuel cell driven UAVs and Drone applications. Time Techno is the first company in India to have such an approval

As part of its international expansion, Time Technoplast has set up a new step-down subsidiary, Elan Steel Containers (FZC), in the Sharjah Airport Free Zone, UAE. This marks the Group’s entry into steel drum manufacturing in the Middle East and complements its existing polymer packaging business. The facility, built with cutting-edge automation and quality controls, will help meet rising regional demand and strengthen the Group’s position as a complete packaging solutions provider

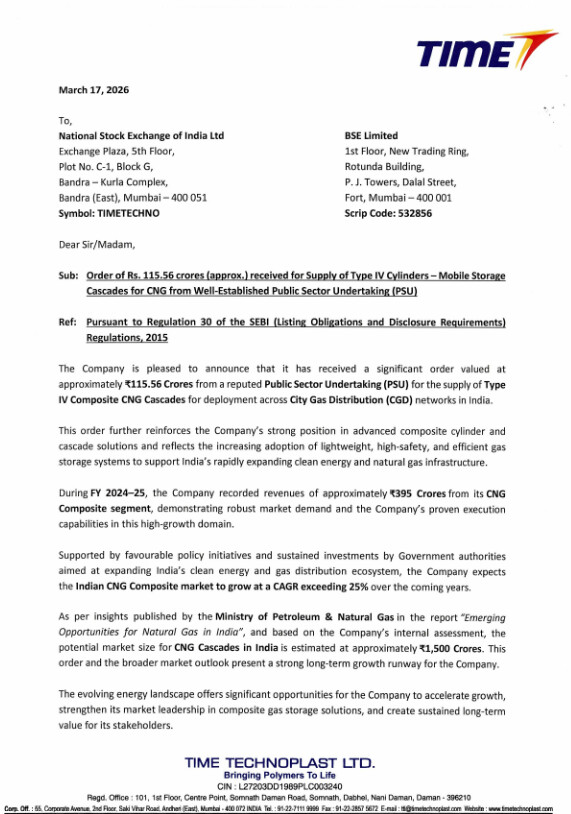

Company is undertaking a capacity expansion project for expanding its capacity to produce CNG cascades. This capex has the potential to add 400 cr to company’s revenues ( they r already doing 400 cr of business from CNG cascades )

Company has submitted its designs to IOL, HPCL, BPCL for its 14.2 kg gas cylinders. Approval should only be a matter of time ( was previously making and supplying only the 10 kg Cylinder ). Company may have to undertake capex to expand their capacities, post approval

Company’s tgt acquisition candidate is Ebullient Packaging Pvt Ltd. Should be able to buy 74 pc stake in this company for a sum of Rs 150 cr

EPPL specializes in manufacturing Flexible Intermediate Bulk Containers (FIBCs) and other packaging products. The acquisition is expected to be completed in 4 to 6 months, subject to due diligence. EPPL projects revenue of ₹250 crore for FY 2025-26 with an expected EBITDA margin of 10%. This strategic move marks TTL’s entry into the flexible industrial packaging segment, complementing its existing rigid packaging portfolio and expanding its market presence

Post acquisition, Time Technoplast is confident of improving EPPL’s EBITDA margins from 10 to 14 pc - mostly on account of better buying and bargaining capacity that Time Techno has vs EPPL. FIBC packaging is growing at much faster rates ( > 20 pc ) across the world. That’s an added advantage

Notes from Q3 concall -

For 9Ms FY 26, growth in sales of VAP @ 17 pc. Share of VAP now stands @ 30 pc vs 27 pc as on 31 Dec 25

India vs Overseas margin profile is very similar

Company aspires to be debt free by H2 FY 27

Commercialisation of composite fire extinguishers ( both 6kg and 9 kg products ) should happen in Q1 FY 27

Company’s CNG cylinder ( 250 lit ) should also go commercial in Q1 FY 27. Their 136 Lit CNG cylinder is already commercial

Have submitted all the documents for approval of Hydrogen cylinders for drone applications

Time Technoplast Ltd.'s subsidiary, PowerBuild Batteries Pvt. Ltd. (PBBPL), is focusing on advanced VRLA (Valve-Regulated Lead-Acid) stationary batteries that serve mission-critical applications, including data centers

Partnership and Supply: PBBPL has signed a multi-year exclusive agreement with Bulgaria’s listed company Monbat AD (Europe) to supply these advanced VRLA stationary/reserve-power batteries in India. This includes pan-India technical support, installation, commissioning and after-sales service

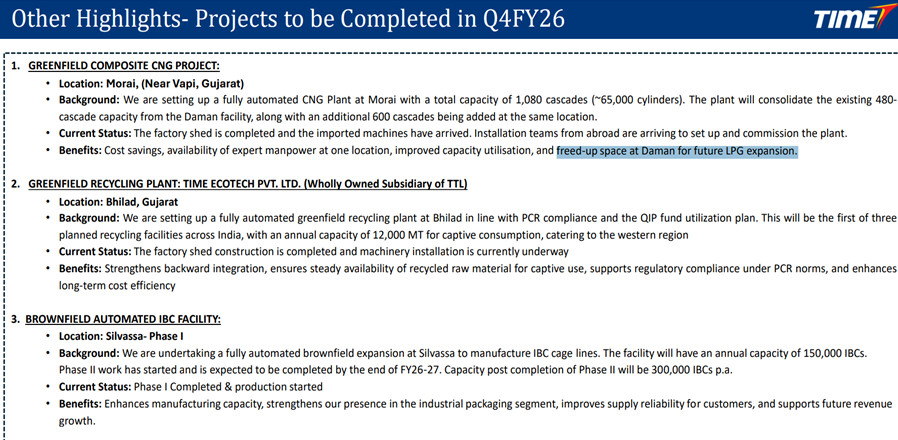

Time Ecotech’s first plant should go commercial wef Q1 next FY. Ecotech intends to set up 2 more plants for their recycling business ( a total of 3 plants ie )

Composite facility @ Daman could make 30k composite cylinders 480 / cascades per yr. Capex was under taken at that plant. It’s nearing completion now. Commercialisation should begin in Apr. This plant’s new + old capacity together now has a revenue potential of Rs 800 cr / yr. Company can also make Hydrogen cylinders from this plant

Have been investing aggressively behind automation. Their Silvasa plant is now highly automated. Saves a lot of money on manpower costs. This plant’s Phase 1 is now operational - can make 1.5 lakh IBCs / yr. Phase 2 shall go commercial at a later date

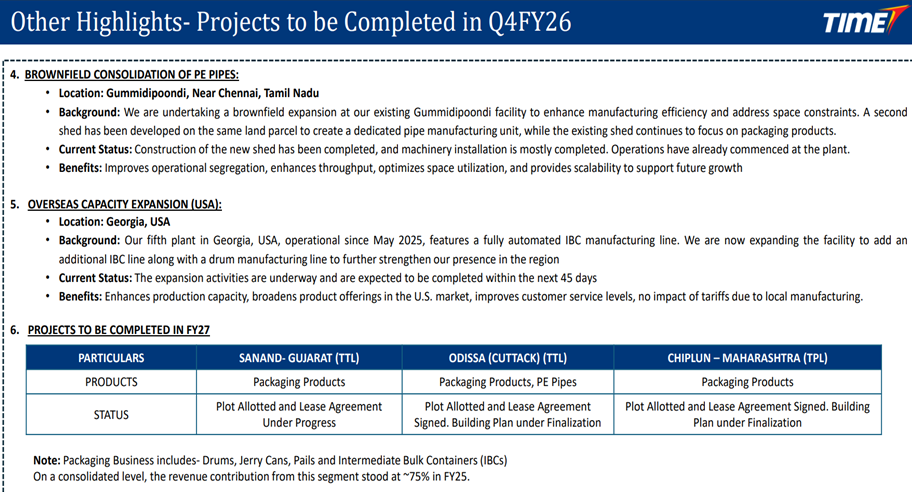

Another of their plant near Chennai - Making packaging materials + PE pipes - should go operational by Q1 next FY

Company’s new plant @ US is now completely ready. Helps them circumvent the tariffs. They previously had 4 plants in US. This is their 5th plant

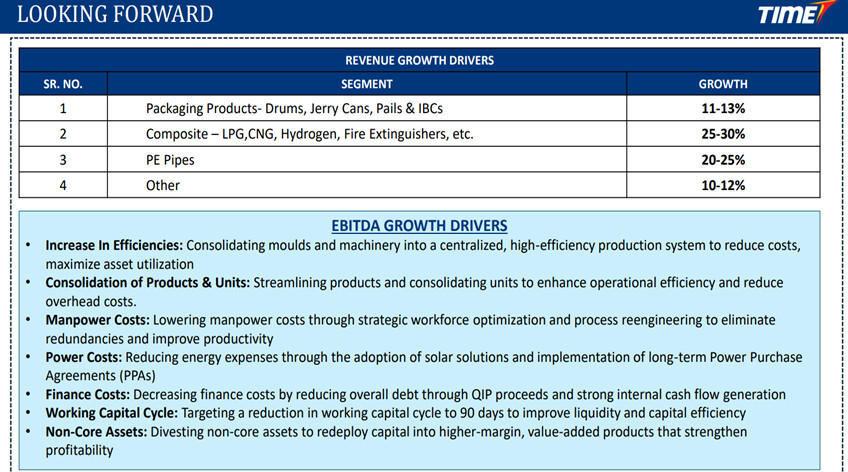

Guiding for a consolidated topline growth of 15 pc CAGR for next 3 yrs - should be led by composite / value added products

Have been allotted with a new land parcel in Orrisa. Shall be setting up packaging + PE pipes facility here

Another land parcel in Maharashtra has been allotted to the company - shall set up IBC manufacturing capacity here. Its located near a big chemical manufacturing zone - should be able to easily find customers here

Company’s packaging products should grow @ 10-12 pc CAGR, Composite products should grow @ 24-26 pc CAGR - resulting into a 15 pc CAGR growth at a company level

Company’s existing PE pipes manufacturing facilities are located near Silvassa and Hyderabad

Company intends to expand EBITDA and PAT margins by > 100 bps / yr on the back of - cost reduction programs + automation + better product mix + lower finance costs + lower power costs ( by using greater share of renewables ) + lower working capital days

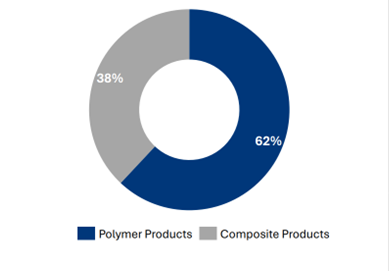

Current share of composite product sales is around 27 pc of total company sales. Company estimates - this should be > 35 pc after 3 yrs or so

Should clock EBITDA of around 900 cr in current FY ( indicating an EBITDA around 250 cr for Q4 ). Interest cost savings should incline the PAT by a greater percentage

Should announce the acquisition of - Ebullient Packaging Pvt Ltd by Q1 FY 27. Should be a value accretive acquisition for them ( as explained above ) + it has the potential to grow its topline @ 20 pc CAGR over medium term

PE pipes can clock 450 cr / yr kind of max sales ( vs 350 cr expected to be clocked in FY 26 ). With Odisha + Chennai investments, potential topline of this business can keep growing in a handsome way over medium term

TPL Plastech ( their 75 pc subsidiary ) is growing at a descent rate. They r expanding their facility @ Lote Parshuram. This should help them sustain their growth momentum. At present, they contribute 8 pc to company’s consol revenues. TPL’s ROCE is > Time Technoplast

Availability of solar power is good in TN, Karnataka, Gujarat, Maharashtra and Odisha. Company has 33 manufacturing plants in India, 17 outside India

Company intends to consolidate some of its Indian manufacturing facilities

PAT growth should inch towards 25 pc CAGR over next 3 yrs

Disc: core holding, biased, not SEBI registered, not a buy/sell recommendation, posted only for educational purposes