Time Technoplast -

Q4 and FY 25 results and concall highlights -

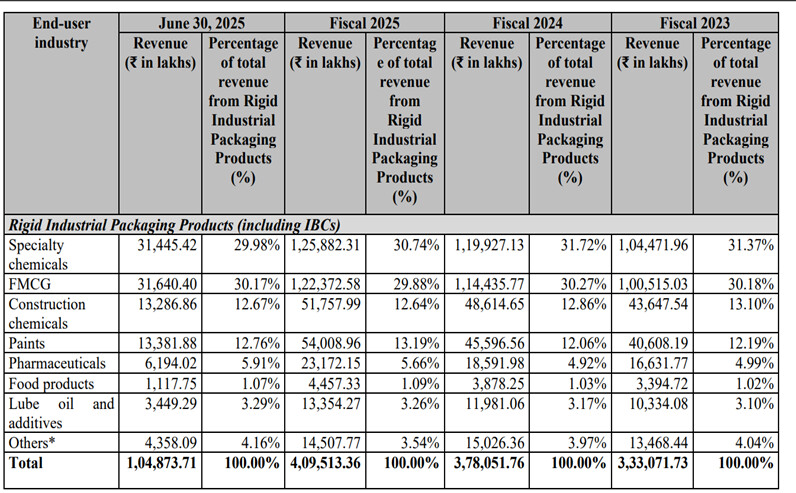

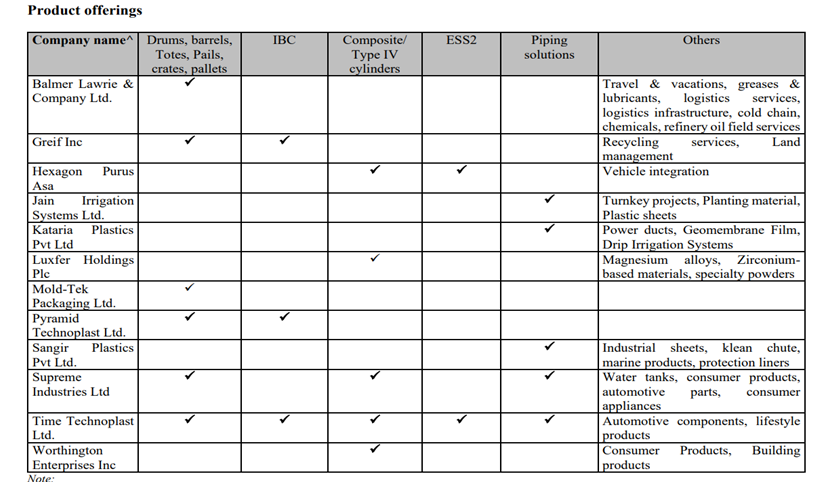

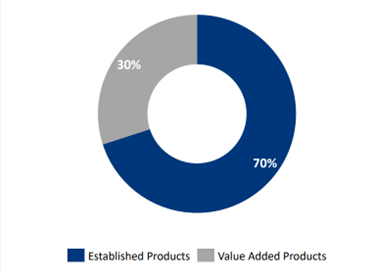

Company’s products -

Polymer products like - Drums, Jerry cans, Polyethylene pipes, turfs and mats, disposable bins, MOX films, steel drums

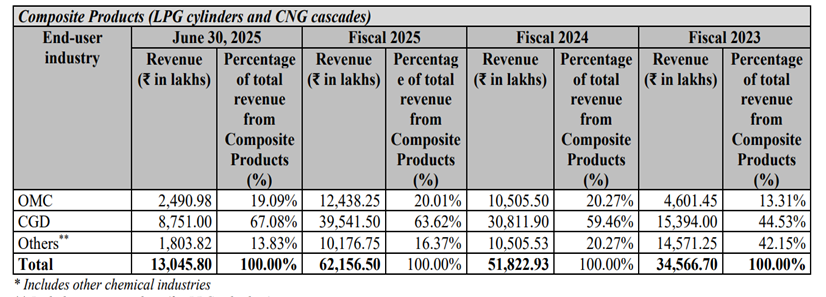

Composite products like - Intermediate bulk containers, composite cylinders, Auto parts, energy storage devices

Out of the products listed above, the value added product segments include - Intermediate bulk containers ( IBCs ), Composite CNG,LPG cylinders and MOX films

Established products include - Drums, Jerry Cans, auto components, air and hydraulic tanks, their Lead - Acid batteries, door mats, PE pipes. Their batteries are used in Telecom sector, railway signalling and other Industrial applications

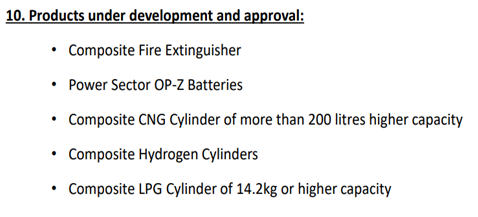

The metal cylinder used in households for LPG supply is of 14.2 kg. Currently, the company is supplying 10 kg composite cylinders as its replacement ( currently supplying to IOC + BPCL + HPCL ). These composite cylinders are growing > 50 pc CAGR. Company has now been asked to develop 14.2 kg cylinders by the Govt Oil Marketing PSUs. Should be able to start supplying these in H2 next FY. Once 14.2 kg cylinders r approved, the growth rates in this segment should increase further !!! Company may also be required to undertake capex for the same. The QIP money should then come handy

FY 25 outcomes -

Revenues - 5462 vs 5006 cr, up 9 pc

EBITDA - 790 vs 705 cr, up 12 pc ( margins @ 14.5 vs 14.1 pc )

PAT - 388 vs 310 cr, up 25 pc ( due fall in depreciation and interest costs, lower tax rate @ 25 vs 27 pc YoY )

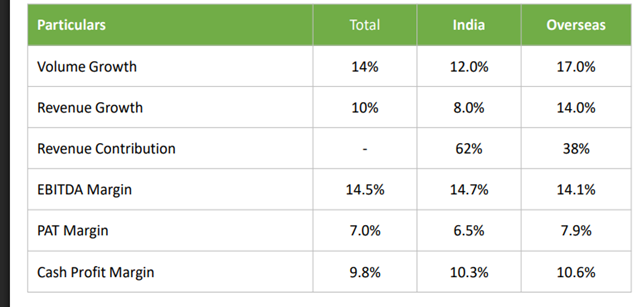

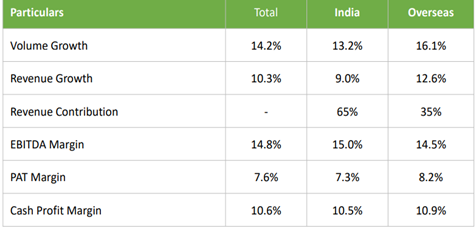

Company’s volume growth @ 13 pc. India, International volume growth @ 12 pc and 15 pc respectively

India : International revenues @ 66 : 34

India : International PAT margins @ 6.8 : 7.7

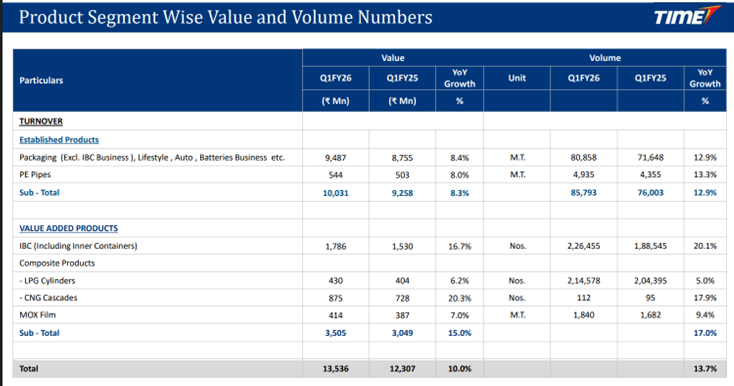

VAP grew @ 15 pc, Established products grew @ 7 pc in FY 25 ( VAP sales now contribute to 27 pc of total revenues - aim to take this share to 35 pc over next 2 yrs. This should result in descent margin improvement )

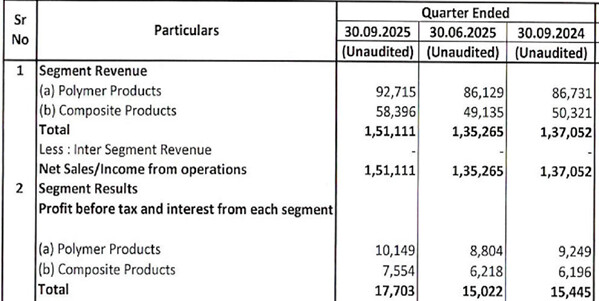

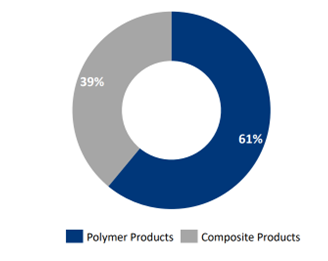

Polymer products revenues @ 3493 cr, up 7 pc. EBITDA margins @ 14 vs 13.6 pc

Composite products revenues @ 1963 cr, up 13 pc. EBITDA margins @ 15.3 vs 15 pc

Q4 outcomes -

Revenues - 1470 vs 1405 cr, up 5 pc

EBITDA - 215 vs 197 cr, up 9 pc ( margins @ 14.7 vs 14 pc )

PAT - 109 vs 92 cr, up 19 pc

Value added products grew by 10 pc, Established products grew by 3 pc

Company received approval for manufacturing of Type -3, fully wrapped, fibre reinforced composite cylinders. These find applications in storing hydrogen in fuel cell driven UAVs and Drone applications. Time Techno is the first company in India to have such an approval

The Company has incorporated Time Ecotech Private Limited (TEPL), a wholly owned subsidiary in India, focused on recycling and reprocessing industrial plastic packaging. In Phase I, a greenfield facility will be set up in Gujarat, launching a nationwide green recycling initiative. The long-term plan in a period of 3-4 years involves an investment of approx. ₹120 crores in fully automated recycling plants across key Indian regions (West, North, South, East) with the capacity to process up to 60,000 MT of plastic annually. This initiative underscores Time Technoplast’s commitment to building a greener and sustainable future, supporting India’s circular economy goals

Our subsidiary i.e. Power Build Batteries Private Limited has developed a low cost, high-performance E-Rickshaw battery in the brand name of “e-START with SELENIUM”. With advanced lead-acid technology and enhanced with selenium, these batteries offer superior performance, safety and efficiency. The growing demand for e-rickshaws is supported by eco-friendly policies. Our battery solution meets OEM standards and ensures reliable power output and quick recharge, contributing to the expansion of clean mobility in India

As part of its international expansion, Time Technoplast has set up a new step-down subsidiary, Elan Steel Containers (FZC), in the Sharjah Airport Free Zone, UAE. This marks the Group’s entry into steel drum manufacturing in the Middle East and complements its existing polymer packaging business. The facility, built with cutting-edge automation and quality controls, will help meet rising regional demand and strengthen the Group’s position as a complete packaging solutions provider

Capex for FY 25 @ 195 cr ( 85 cr were spent towards maintenance capex, rest for growth capex )

Aim to sell 51 cr worth of non-core assets in FY 26

Aim to grow the composite materials business @ 30 CAGR for next 2-3 yrs. Aim to grow company’s consolidated topline @ 15 pc CAGR for next 3 yrs

Aim to keep improving their EBITDA margins by 30 bps / yr for next 3 yrs

Capex guidance for next 3 yrs @ 200 cr / yr

Aiming to make the company debt free in next 2 yrs ( ie by Mar 27 )

Receivable periods are higher in polymer products vs composite products

E- Battery business shall start with company catering to secondary market’s demands ( and not OEM’s demands ). Secondary market is quite big since India already has 16 lakh E-Rickshaws on the roads with 4 batteries each. These batteries cost aprox Rs 10k and last for aprox 1.5 yrs. Company claims that their batteries can run for 140 km / charge vs 100 km / charge wrt existing batteries in the mkt. They think, this business will start slowly ( clocking 40-50 cr of sales in 1st yr ) but can gradually pickup going forward

Once company gets the nod for 14.2 kg cylinders ( form IOC, HPCL, BPCL ), they r likely to go for the fund raise via QIP. Also looking to get export approvals for these cylinders. Expecting to receive Indian approvals within H1 FY 26

Disc: holding, biased, not SEBI registered, not a buy/sell recommendation, posted for educational purposes