The product margins depend on Crude Oil, which is on the rise. There will be an impact in the coming quarter, Q1.

Time Technoplast -

Q4 and FY 26 results and concall highlights -

Q4 outcomes -

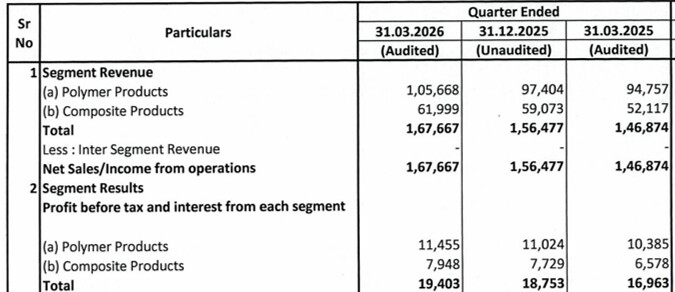

Revenues - 1681 vs 1470 cr, up 14 pc. Volume growth @ 13 pc

EBITDA - 245 vs 215 cr, up 14 pc ( margins stable @ 14.7 pc )

PAT - 131 vs 109 cr, up 20 pc

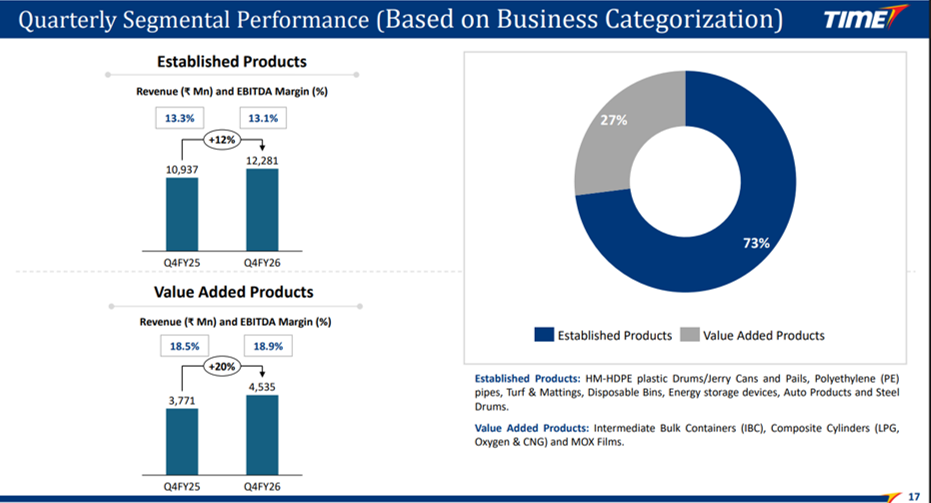

VAP grew by 20 pc. Established products grew by 12 pc

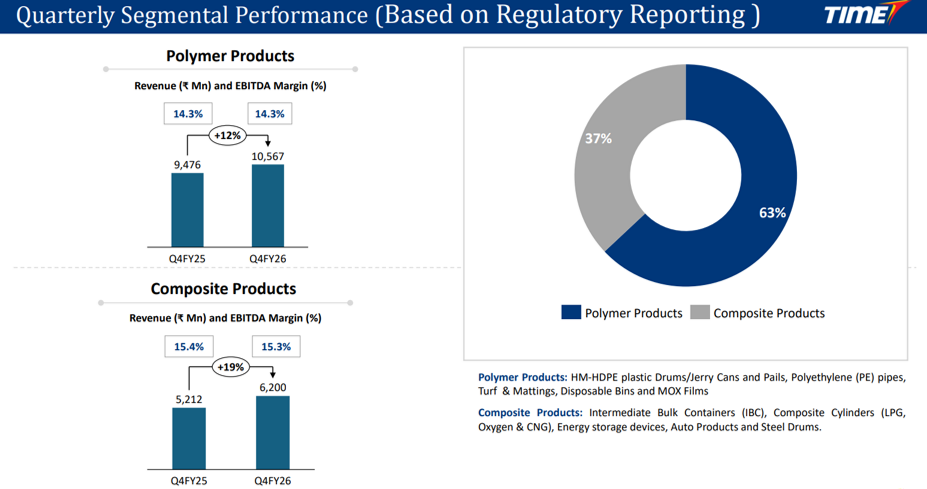

Composite cylinders business grew by 22 pc

FY 26 outcomes -

Revenues - 6114 cr, up 12 pc. Volume growth @ 13.5 pc

EBITDA - 901 cr, up 14 pc ( margins @ 14.7 vs 14.5 pc )

PAT - 468 cr, up 21 pc

VAP grew by 18 pc. Established products grew by 10 pc

Debt reduction of 409 cr over FY 26

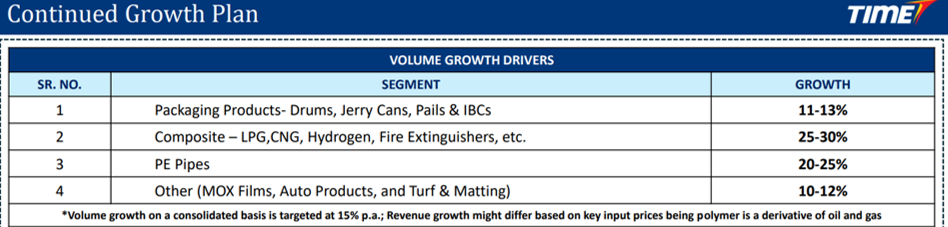

Product wise volume growth guidance for FY 27 -

Packaging products, drums, Jerry cans, IBCs > 10 pc

Composite cylinders, fire extinguishers > 25 pc

PE Pipes > 20 pc

Mox Films, Auto parts, Turf and Matting > 10 pc

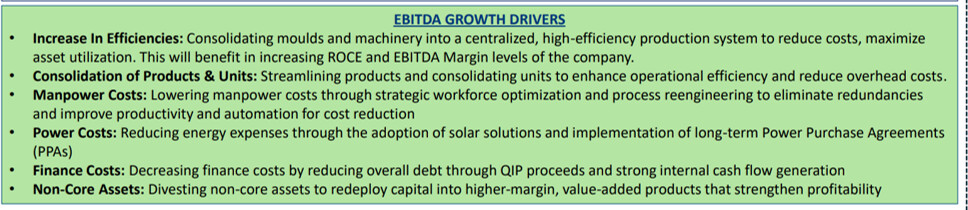

Drivers for profitability enhancements -

Power costs: Reducing energy expenses through the adoption of solar solutions and implementation of long-term Power Purchase Agreements

Finance Costs: Decreasing finance costs by reducing overall debt through QIP proceeds and strong internal cash flow generation

Non-Core Assets: Divesting non-core assets to redeploy capital into higher-margin, value-added products that strengthen profitability. Have identified non core assets worth 134 cr to be sold over next 1-2 yrs

Increase In Efficiencies: Consolidating moulds and machinery into a centralized, high-efficiency production system to reduce costs, maximize asset utilization

Consolidation of Products & Units: Streamlining products and consolidating units to enhance operational efficiency and reduce overhead costs

Manpower Costs: Lowering manpower costs through strategic workforce optimization and process reengineering to eliminate redundancies and improve productivity and automation for cost reduction

Imp highlights from previous concalls -

QIP - successfully raised Rs 800 cr @ Rs 201 / share in Q2. Equity dilution caused due a/m QIP @ 8.7 pc

Have set up a new subsidiary - TIME ECOTECH - focussed on recycling and reprocessing industrial packaging. Will invest 120 cr over next 3 yrs in this new initiative

Have developed a low cost, low maintenance, high performance battery for E-Rickshaws named - E Start with SELINIUM. Current mkt size of such batteries is 6400 cr / yr and is expected to grow @ 25 pc CAGR for foreseeable future

Committed to source 75 pc of its energy requirements to Solar sources - to reduce its energy costs. This would result in annual energy savings of 20-30 cr

Currently developing OP-Z batteries. OP-Z batteries (Ortsfest Panzerplatte - Stationary Tubular Plate Flooded batteries) are high-performance, 2V industrial-grade lead-acid batteries used extensively in the power sector for critical backup and energy storage. They are characterized by a long service life of over 15-20 years and excellent deep-cycle capabilities

Company received approval for manufacturing of Type -3, fully wrapped, fibre reinforced composite cylinders. These find applications in storing hydrogen in fuel cell driven UAVs and Drone applications. Time Techno is the first company in India to have such an approval

As part of its international expansion, Time Technoplast has set up a new step-down subsidiary, Elan Steel Containers (FZC), in the Sharjah Airport Free Zone, UAE. This marks the Group’s entry into steel drum manufacturing in the Middle East and complements its existing polymer packaging business. The facility, built with cutting-edge automation and quality controls, will help meet rising regional demand and strengthen the Group’s position as a complete packaging solutions provider

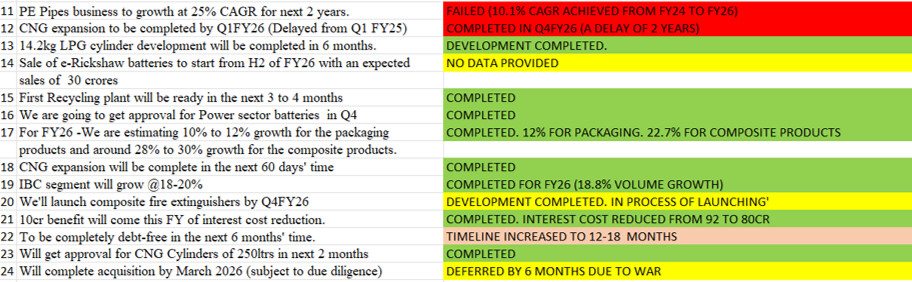

Company is undertaking a capacity expansion project for expanding its capacity to produce CNG cascades. This capex has the potential to add 400 cr to company’s revenues ( they r already doing 400 cr of business from CNG cascades )

Company has submitted its designs to IOL, HPCL, BPCL for its 14.2 kg gas cylinders. Approval should only be a matter of time ( was previously making and supplying only the 10 kg Cylinder ). Company may have to undertake capex to expand their capacities, post approval

Time Technoplast Ltd.'s subsidiary, PowerBuild Batteries Pvt. Ltd. (PBBPL), is focusing on advanced VRLA (Valve-Regulated Lead-Acid) stationary batteries that serve mission-critical applications, including data centers

Partnership and Supply: PBBPL has signed a multi-year exclusive agreement with Bulgaria’s listed company Monbat AD (Europe) to supply these advanced VRLA stationary/reserve-power batteries in India. This includes pan-India technical support, installation, commissioning and after-sales service

Composite facility @ Daman could make 30k composite cylinders 480 / cascades per yr. Capex was under taken at that plant. It’s nearing completion now. Commercialisation should begin in Apr. This plant’s new + old capacity together now has a revenue potential of Rs 800 cr / yr. Company can also make Hydrogen cylinders from this plant

Company’s new plant @ US is now completely ready. Helps them circumvent the tariffs. They previously had 4 plants in US. This is their 5th plant

Have been allotted with a new land parcel in Odisha. Shall be setting up packaging + PE pipes facility here. Company’s existing PE pipes manufacturing facilities are located near Silvassa and Hyderabad

TPL Plastech ( their 75 pc subsidiary ) is growing at a descent rate. They r expanding their facility @ Lote Parshuram. This should help them sustain their growth momentum. At present, they contribute 8 pc to company’s consol revenues. TPL’s ROCE is > Time Technoplast

Notes from Q4 concall -

Ebullient Packaging Private Ltd, Acquisition Update- Following the Board’s review of the MOU executed in FY 2025–26 and a thorough assessment of prevailing geographical market conditions, it has been decided to extend the review period before arriving at a final decision regarding the proposed acquisition. Further updates will be communicated to Shareholders in due course

Demand momentum in the composite products continues to be extremely strong

VAP contribution to total sales now @ 29 pc vs 27 pc in FY 25

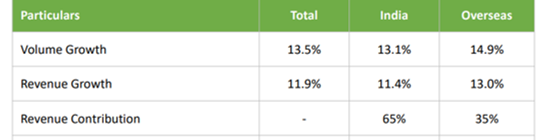

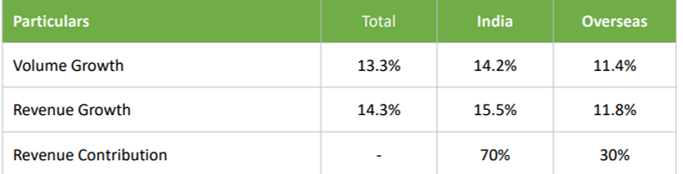

India : Overseas revenue share @ 65:35

Capex in FY 27 @ 370 cr. Out of this 200 cr was maint capex

Aspire to be debt free in next 12-18 months time frame

Energy sourcing of upto 75 pc from solar sources should happen in next 24 months. Already saving Rs 10 cr on power costs via their investments in Solar energy

Delay in launch of 14 kg LPG cylinder due Iran war. Continue to see good demand for 10 kg composite cylinders

Initial tgt audience for composite fire extinguisher cylinder shall be OMCs which require 8 lakh of these / yr

Have commissioned first recycling plant under Time EcoTech in Q1 FY 27

Guiding for EBITDA and PAT growth of > 15 pc and > 20 pc for FY 27

Cash flows were depressed, inventories and receivables elevated @ the end of FY 26 due to the ongoing war. Should normalise by end of FY 27

Normal capex requirements / yr for the company shall be in the range of 200-250 cr for next 2-3 yrs

Polymer prices went up sharply post commencement of war. Company is able to pass them on with a 1 month lag. Continue to stick to their EBITDA and PAT guidance despite the surge in input prices. But the eventual pass through of RMs is 100 pc

LY, they did a business of aprox 600 cr wrt composite LPG + CNG cylinders. Should be able to clock 750 cr in FY 27

A single CNG cascade comprises of 60 X 156 Lit CNG cylinders

Total VAP sales @ 1741 cr in FY 26

Acquisition of Ebullient Packaging is deferred at present. May re-consider it post the war is over

Confident of maintaining revenue and PAT growth in Q1 as well

Disc: investment position, not SEBI registered, biased, posted only for educational purposes

14 Likes

Bharat bhai was very clear and confident as always in his concall the good thing is there value added product segment which is 35 percentage of overall sales and growing at 18 percentage and ebitda at 18 percentage

Market has to differentiate that and give a higher ev for that

The remaining 65 percentage sales yes can be valued as plastic commodity player

Qip was placed at 201 should be anchor for some time have a good ocf of around 500 550 cr this Yr suppressed because of inventory issue even with 250 Capex with reduced interest cost to 40 cr and no debt fcf will improve

Let us hope the market rates the value added segment separate instead of rating at Blended basis

Trading at the base value of its pe on forward basis once crosses the qip anchor price I think market may notice or waiting for the war cloud to over

Disl invested chance of confirmation bias

6 Likes

27/05/2026

•

• Value added products grew by 18% in FY26 as compared to FY25, while established products grew by 10%.

(FY26)

• Value added products grew by 20% in Q4FY26 as compared to Q4FY25, while established products grew by 12%.

(Q4FY26. Overseas volume growth impacted by Iran War (Middle-east operations). It’s down from 15% to 11%)

• Orderbook – 400cr for Packaging products (vs 425 PQ)

195cr for Composite Cylinders (CNG Cascades) (vs 165cr PQ)

265cr for PE Pipes (vs 275cr PQ)

•

•

• Sale of Non-Core Assets: Company has identified total non-core assets worth ~₹134 Cr for disposal, with a targeted realization over the next 18-24 months’ time. (It had been 37cr PQ. Company has identified 100cr more non-core assets)

• FY26 ROCE at 18.9% (vs. 20% target), reflecting short-term impact of QIP-led automation investments; targeting 1.5–2% annual improvement.

• Acquisition Updates: Ebullient Packaging Private Ltd.: Following the Board’s review of the MOU executed in FY 2025–26 and a thorough assessment of prevailing geographical market conditions, it has been decided to extend the review period before arriving at a final decision regarding the proposed acquisition.

• Green Energy- Conversion of Electricity Units consumed to Solar Power: Power Purchase Agreement (PPAs) across Karnataka, Tamil Nadu, Gujarat, and West Bengal have already started generating annualized benefits of ~₹11 Cr, with additional benefits from Maharashtra and Uttarakhand expected from Q3 FY27.

• Update on LPG Cylinders (14.2 kg): Following the strong response to its 10 kg composite LPG cylinder, the Company is working towards launching a 14.2 kg variant in collaboration with Public Gas Distribution Companies.

Current Update: Considering current geopolitical uncertainties, the Board has recommended pursuing JV/tie-ups with private gas distributors to establish an independent LPG distribution network, while continuing discussions with government authorities for approvals and tenders.

•

• CNG (Higher Capacity Cylinder): The Company currently manufactures CNG cascades using 156-litre cylinders and is in the process of obtaining approvals for higher capacity variants of 250 litres and 350 litres. These larger cylinders are expected to enhance cascade efficiency by reducing cylinder count, manufacturing time, and overall costs. With the expanded Morai facility, the Company is also well positioned to serve Original Equipment Manufacturers (OEM) demand for composite cylinders in the automotive sector.

• Hydrogen (Higher Capacity Cylinder): The company has existing approvals for Type III/IV for applications in Drone and Hydrogen Storage Systems, with enhancing size range we will be able to serve a wider range of drone applications along with increasing storage capacity for Hydrogen Storage Systems. Globally, the drone market stands at ~USD 30 Bn.

• FIRE EXTINGUISHER: The Company has developed 6 kg and 9 kg composite fire extinguishers that are significantly lighter, corrosion-resistant, and offer enhanced safety. We are also engaging with suppliers to bring the product to market. The initial target segment is oil refineries, which collectively require approximately 800,000 fire extinguishers annually.

•

•

•

(Improvement in EBITDA margins for all segments with value-added products showing more improvement)

•

•

(Value-added products reaching nearly 19% EBITDA margins for the qtr)

• Revenue for FY26 (in cr.)

o IBC– 808 (vs 698 in FY25) (15.7% growth)

o Composite Products – 762 (vs 622 in FY25) (22.5% growth)

o Infrastructure (PE Pipes, Energy storage devices) – 402 (vs 377 in FY25) (Growth of 6.6%)

CONCALL NOTES:

• COST INCREASE PASS-THROUGH: In Q4 FY '26, polymer prices witnessed a sharp increase. However, given that 92% of our business operates under a B2B model, with industrial customers, price revisions are implemented through mutually agreed monthly or quarterly mechanisms. This enables us to effectively pass on cost increases and maintain the stability of our absolute EBITDA.

We operate on a B2B model serving industries like specialty chemicals, FMCG and pharmaceutical with long-term industry relationships on a mutually agreed pricing formula enabling us to maintain our EBITDA

If you ask me in the month of the March price increased by 50%, we’re able to get a 25% increase from the customer in march. Balance of 25% will be recovered in the month of April. In April, if there are higher prices, than we recover in May. So as far as you will see stability if the same thing continues, you will find in the April, May, June quarter result, there is definitely upside of the revenue part. There was a 30 days effect already accounted in my profitability.

Whatever is the increase in the polymer prices, it is passed on to the user on a 100% basis. Maybe there is a lag maybe about 15 days, 30 days or of a quarter. But definitely, these are all passed on to the customers on a 100-plus basis.

• We remain committed to becoming debt-free. As per our internal calculations, we are estimating a time line in the next 12 to 18 months.

• FY '26 ROCE is 18.9% versus 20% target, reflecting short-term impact of QIP-led automation investments targeting 1.5% to 2% annual improvement.

• The company is committed to transitioning 75% of its power consumption to green energy over the next 2 years through its partnership with solar power producers.

Power purchase agreements across Karnataka, Tamil Nadu, Gujarat and West Bengal have already started generating annualized benefits of about INR11 crores, with additional benefits from Maharashtra and Uttarakhand expected from quarter 3 FY '27, The payback period on these equity investments is close to about a year.

• LPG CYLINDERS: The company has been working towards 14.2 kg cylinder, which has already been finalized and accepted by the OMC. Because of the ongoing shortages in terms of LPG availability due to Iran U.S. war, there is a slight pause with regard to the launch of these new sizes as 14.2 kg.

• Volume growth on a consolidated basis is targeted at 15% per annum. Revenue growth might differ based on key input prices as polymer is a derivative of oil and gas.

EBITDA growth will be around 17%. PAT growth to be minimum 21%, may exceed further because as the interest cost is reduced.

• INCREASED WORKING CAPITAL CYCLE: When I bought the inventory in the month of February and March and the prices have increased. So last quarter, cycle time has also little increased because I need to continue on minimum inventory level to continue the customer service. So, we have certain inventory for the composite product, which is largely dependent on the overseas market because India – nobody is manufacturing the inputs which are required for the composite number carbon fiber, for special polymers, some kind of special carbon fiber, glass fiber. So, we carried the inventory for 6 months. Whatever happen, I cannot disturb the supply to my customer.

But this will be normalized. We have said my 3 years target when my working capital cycle time was 100 days, we said it will be going to be in next 3 years’ time, 90 days. So, I’m very clear, we are on that line only.

Our understanding with the customer, therefore, would be that while they reimburse you the ups and downs of the polymer prices, the value addition or the margins or the EBITDA, they continue to be fixed. So, your contract is always ensuring that your margins are not really disturbed.

• We are not revising any guidelines. We are continuing our guidance, whatever been given.

• Target for the next 5 years: To reach in the next 5 years’ time more than $1 billion business. We are continuing. We are not changing anything.

• COMPOSITE SEGMENT: More than 25% growth we are projecting for FY27.

We are sure in the next 2 years’ time, we’ll have to see further expansion because some of the new composite product development, which is hydrogen cylinder is just with this plant, we can do very small quantity, we can manufacture. So, we are watching very clearly, we are understanding the customer requirement for the hydrogen cylinder, for the power project, for the gas project, for the automotive sector.

Automotive sector: As the new capacity is ready now, we can offer to the automotive sector cylinders separately. Every automotive OEM, we will start talking to them. In the next 6 to 8 months’ time, visibility will be there, how much – because we have to develop their capacity. We have to develop the tool based on their retail capacity.

CNG for cascade is a standard 156 liter. Then we have started now 250 and 350 developments under process. We will update the market as we get the approval from the authority. If I use 156-liter CNG cylinder in my cascade, I need 60 cylinders in 1 cascade. Then if I will use 250, it will reduce to 36 or something. Then if I will go back to 350 liters, it will go down more. So, my capacity in number of cylinders is significantly more. So remaining capacity, I can use manufacturer automotive cylinder, and we can supply to the them.

• Finance cost will be around 35-40crs for FY27

• PE PIPES: Pipe business, I have order book of INR260 crores. But now I don’t want to supply at this price because prices have increased. So, government should revise the prices to the EPC contractor, then if they will revise, I will start supplying. I’m not going to supply into older prices which the government has finalized to the EPC contractor.

• HYDROGEN CYLINDER: INR2 crores, INR2.5 crores, the trial order from Navratna PSU, that is already supplied. – is under their testing. Couple of projects which are under discussion. And as the outcome will come – because certain R&D with the government, with the other company, Navratna, they all will have to do the trial – after getting a trial, they will wait for 2 or 3 months, get the results, then they will come back and then we’ll talk about that.

• If you take the volume growth of 15%, now if the current prices continue for whole of the year, then revenue growth, maybe 40%.

• There will be a reduction in the requirement of growth, in HDPE pipe business. Till government gives the increase, then no EPC contractor will put the loss in their money. his government is also considering because government cannot afford any, in fact, at the cost increase by 50% or something.

But on the other hand, you have also known that because of the LPG shortage situation, government has advised that CNG pipeline should be increased so that they can replace the LPG demand. So, there are avenues of growth that are also coming up in these difficult situations also. So overall, that is how we are reflecting a growth position.

• 400crs debt of higher cost repaid and new lower cost debt of 400crs taken up (for working capital requirements I presume)

• EBULLIENT PACKAGING ACQUISITION: My Board has suggested there is a current situation of the ongoing war, war Asia. Prices have increased substantially. So let us study that situation normalized, then see what is the 3 to 4 months or 6-month revenue is there, how they are able to sustain EBITDA. Put up again to the board, then we’ll take forward with them because we can’t get that exactly apple-to-apple comparison of the whole year in the current situation.

It’s wait and watch till the situation normalizes.

THINGS TO TRACK:

• CNG CASCADE DEMAND: How will new facility ramp-up? Can 25%+ growth guidance be delivered? How will Supreme Industries entry into this segment play out?

• LPG 14.2KG CYLINDER PROGRESS

• PROGRESS OF NEWER PRODUCTS: Drone application, fire extinguishers, water heaters, oxygen cylinders, PE Pipes for Gas distribution industry.

• PROGRESS OF AUTOMOTIVE APPLICATION

• IMPACT OF INCREASED RAW MATERIAL PRICES ON SALES AND MARGINS

• IBC SEGMENT GROWTH: Will increased competition hurt its growth rate?

• EFFCIENCY TRACKER: How much gains in cost reduction will come from solar power + Automation & re-engineering.

• FIBC COMPANY ACQUISITION PROGRESS

4 Likes

Monitarables tracker for TTPL. Execution has been decent, apart from the delay in commisioning of new CNG Cascade facility which was delayed multiple times.

All major targets are delivered and are on track (15% volume growth, 25% composite product growth, 20%+ PAT growth, ROCE Improvements)’

Due to war and sharp escalation in raw material prices, working capital and debt has increased in the short term but is expected to normalize going ahead.

All in all, company is set for strong compounding growth of 20%+ PAT over the next 2-3 years. (next 1-2 qtrs maybe up and down, depending on impact of war and raw material prices)

DISCLOSURE: INVESTED

12 Likes