@vinay_chauhan absolutely they are targeting fast fashion and the fast fashion industry is here to stay. Reliance is opening a Yousta store every 10 days or so , Trent probably every 5 days says a lot that young and aspiring Indians across India are no longer looking for clothes as a yearly festival buying but wanting to buy the latest trending season collections at the earliest or wear a new cloth on every occasion , thanks to digitalization & social media consumption and influence of the Western World . Preference has changed to style and trends over fabric quality and durability of a product .

Selling premium brands does not mean it may not be fast fashion . It is merely that the fabric quality , variety of cotton or mix used any specific features of the fabric and most importantly marketing which will make a difference in the pricing and premium appeal of a product

In any business, the lower the lead time from idea to market ,the more will be the consumption / demand for the product .

Look at our personal examples : Why are people preferring 10 /15 minute Quick Commerce over Amazon / Flipkart ?

Their offline expansion is measured and like I mentioned being FOCO based , the initial investment on new stores is very low. E-Commerce is their primary channel of growth and offline is miniscule presently and till the time they expand in cities where they own the manufacturing or warehouses it makes sense . New collections are displayed in these offline stores for 15 days and fresh stock is delivered every 15 days . The stocks returned back are then sold on the online platform , so basically till now a part of the ecommerce inventory is itself on the offline stores for 15 days and then moved to their ecommerce platforms if there is no demand for it at the stores.

This means that their offline stores expansion must also be measured and tracked to ensure that the offline store growth does not exceed ecommerce growth .

The problem is everyone has access to data but only few are able to make meaningful information of such data . The problem interpreting data increases manifold as the number of variables increases . What you fail to realize is Vedant Bang professional credentials . Please read about Acturial Science , what do they excel at and then question why others are not able to make the same sense of data that this guy Vedant Bang is able to make ?

I work as a business process data mining consultant working with the largest software product company of Europe , and even biggest of MNCs across the globe are struggling making sense of their business data due to distributed systems , huge data generated from different systems / IOT devices working in silos and lack of visualization tools to make sense of the data .

Extracting information from data is not easy for MNCs , so expecting a traditional contract manufacturer to get the same quality of information would not be easy.

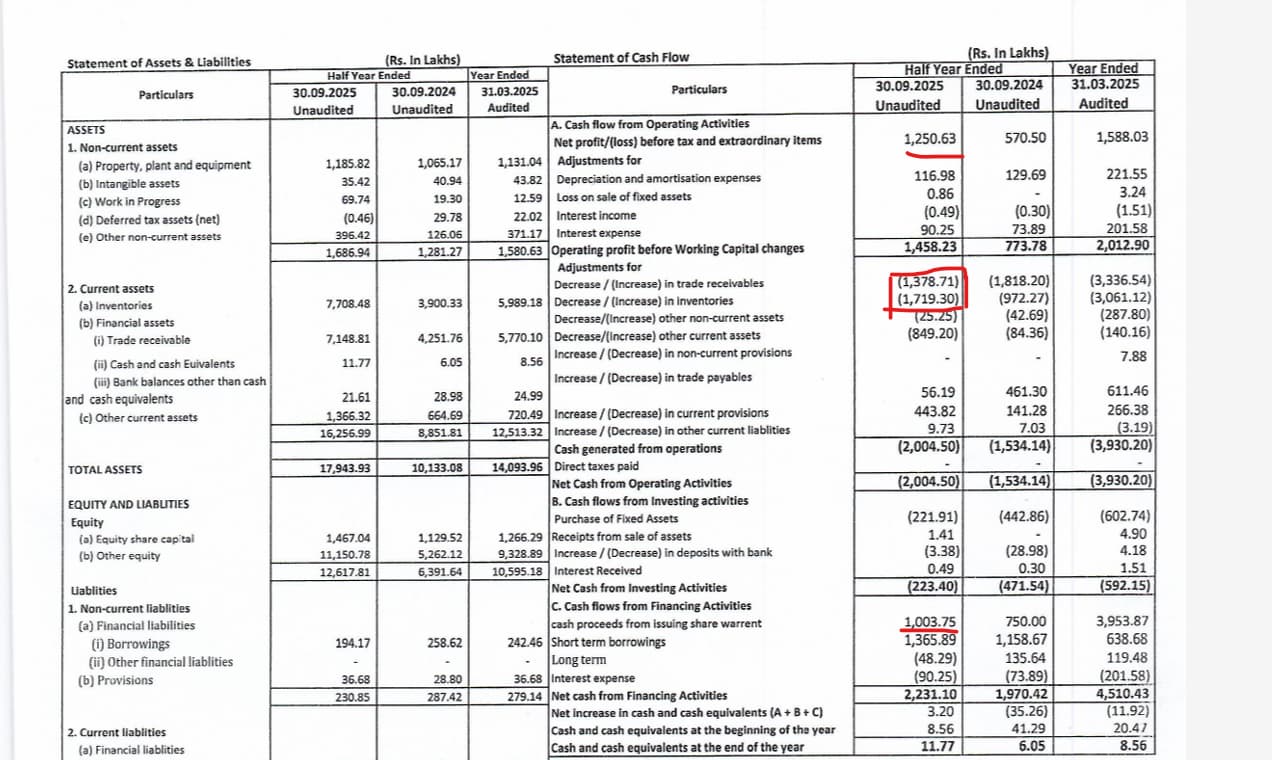

PDS operating profit margin has never been over 4% since 2014 as per screener data.

Not sure why but maybe you can highlight their inefficiencies as well which makes them earn meager operating profit margins even after working with top Europe and US retail giants .

PDS acquiring Thomas Scott while your wishful thinking, would mean they are doing something right which PDS has not been able to crack even after so many years