History

Thomas Scott 1.0

Thomas Scott (India) Ltd. was incorporated on October 22, 2010. Company has been engaged in apparel, textile and retail market . The company was incorporated after the demerger from Bang Overseas Limited which focusses on Trading & Exports into Thomas Scott (India) Limited .

The brand name Thomas Scott was created after the LVMH acquired Thomas Pink business which was being licensed in India by Bang Overseas.

Before CY 2022 - The company was engaged in the men’s apparel business especially in the formal shirts and semi formal shirts business .The major brands under which they used to sell their formal & semi formal shirts were as below

- Thomas Scott

- Hammersmith

- Bang & Scott

- Italian Gold

The company had struggled over the years to increase its revenues with the sales being stagnant between FY 13 to FY 21 with no revenue growth through the years. The company had only one manufacturing plant in Solapur (Forever Clothing Company ) and was fully a B2B manufacturer

Thomas Scott 2.0

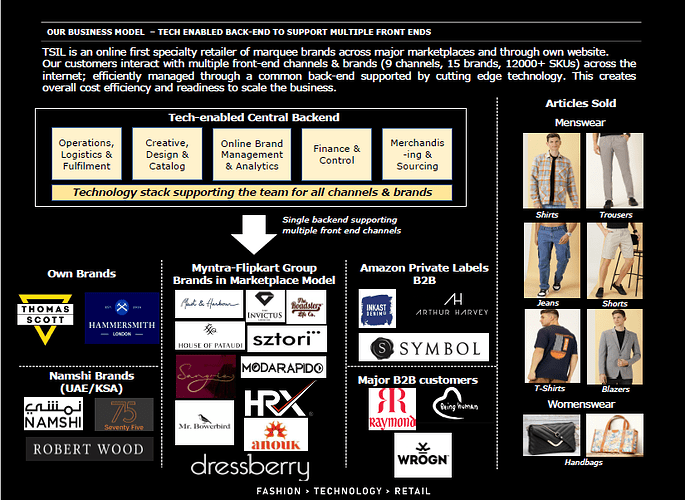

The transition of the business started from FY 2022 onwards with the introduction of the 2nd generation Mr. Vendant Bang Linkedin Profile in the business .The business has been transitioned from the traditional men’s formal / semi formal shirts business into an tech-enabled online Fashion retailer focusing on the following verticals for growth

- Sales from Own Brands ( Thomas Scott )

- License from Brands to be sold on the E-Commerce portal

- B2B Business and Private Label Manufacturing for Market Places

Source : Investor Presentation

Thomas Scott has not only diversified horizontally across sub segments , but has also strategically expanded across markets with the launch in UAE Markets of their own brands and selling Namshi Brands ( Namshi is the largest e-commerce marketplace in UAE )

Industry Overiew

E-Commerce Industry Growth

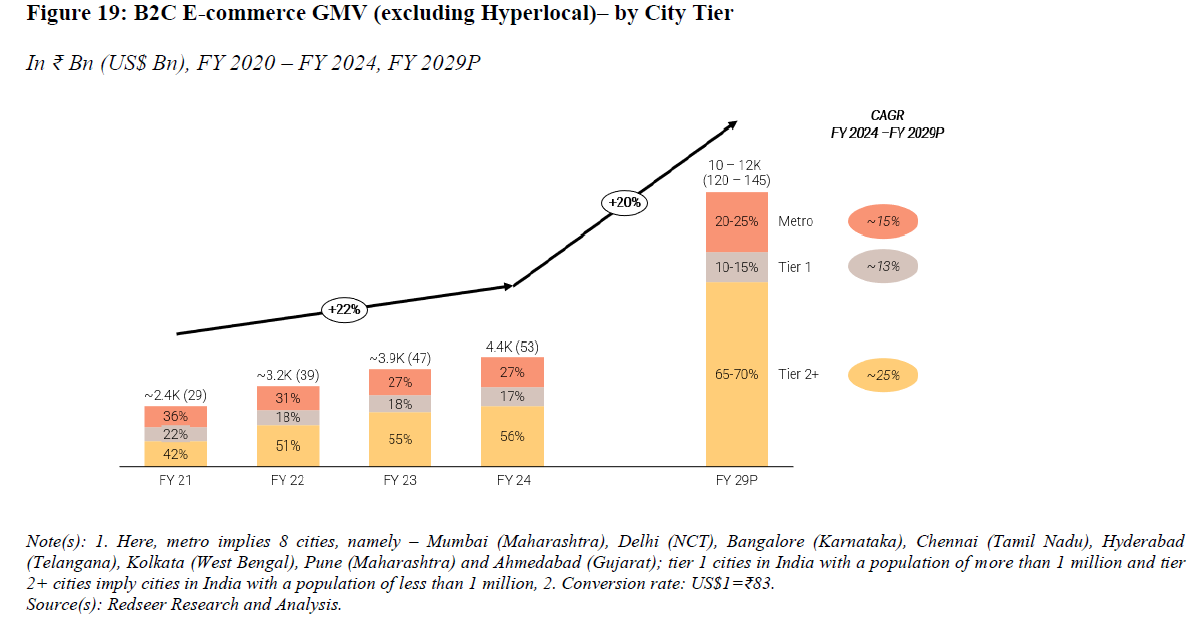

Ecommerce Industry in India is projected to grow at 20% from FY 24 to FY29 .

Source : E-Com Express DRHP

Within the E-Commerce space D2C brands are meant to grow exponentially at 40 to 45 %

Source : E-Com Express DRHP

Within the Organized Apparel Market, the E-Commerce as a segment is estimated to grow by 23% till FY27 . The TAM of E-Commerce in FY27 would be over Rs. 261507 crores

Source : Style Bazaar DRHP

The rising per capita income , the growth of internet / smartphone and social media influence on fashion , the increasing share of youth and working population preferring organized brands and ecommerce over traditional retail act as strong tailwinds to the growth of ecommerce and fashion retail as a whole

Moats of Thomas Scott

- 2nd Generation Promoter propelling the stagnant business

Mr Vedant Bang joined the business in FY 22-23 .

Qualifications of Mr Vedant Bang

- Fellow Actuary ( Institute and Faculty of Actuaries , London )

- Chartered Financial Analyst ( CFA Institute )

- Chartered Accountant ( ICAI )

Actuarial Science is comparatively one of the most coveted and comparatively difficult degree to obtain ( Institute and Faculty of Actuaries , London has less than 33000 actuaries across the world & Institute of Actuaries of India has less than 1000 members as on date ) .

Actuarial Science members excel in assessing and managing financial risks, particularly those related to uncertain future events . They excel at statistical and probabilistic models to real world problems. They excel at creating models to manage financial risk and have similarities to the data analytics & data science background

Past Experience

2018 to 2021 Deloitte : Worked as a Management Consultant with Deloitte ( primarily investment banks in Europe and UK doing consumer behavior modelling ) . He has worked for global investment banks like Nomura, Credit Suisse, JP Morgan, SBI, and HDFC Bank as a management consultant designing models for forecasting, risk management, and pricing. Source

The key moat here is how the qualifications and past experience of the new gen promoter is being leveraged to grow the business from a B2B manufacturer to a ecommerce first fast fashion brand leveraging data and tech as the cornerstone of their business for growth

This can also be seen by a shift in how the company has gone from a B2B to B2C .

Before joining the family business : B2B 100% B2C 0%

Current TTM ( as of Dec 2023 ) : B2B 28% B2C 78%

- Data & Tech As Pillars of the Business

Thomas Scott has transitioned from B2B business and has focused on data analytics & technology stack as the key pillars for their success.

His past experience in Consumer Behavior Modelling can also been seen from the article written on IndianRetailer regarding Consumer Behavior in Fashion Retail Industry

The company launches 200 to 300 unique products monthly, leveraging data analytics to identify micro-markets with supply-demand gaps. This data-driven approach allows them to avoid highly competitive markets and focus on emerging trends with less competition. Data Analytics also play a crucial role, informing decisions on inventory levels, location, and timing based on factors like delivery times and seasonal events. Data analytics also determines optimal product sizing and production quantities .

Automation and continuous monitoring of processes and workflows are implemented, using tools whereby notifications are sent to WhatsApp to track order dispatch, identify breaches, and address warehouse issues ensuring efficient e-commerce operations.

This technology stack has also been vetted by Shankar Sharma in the following video to a Business News Channel . Shankar Sharma holds 6.2% of Thomas Scott as per September 2024 holdings

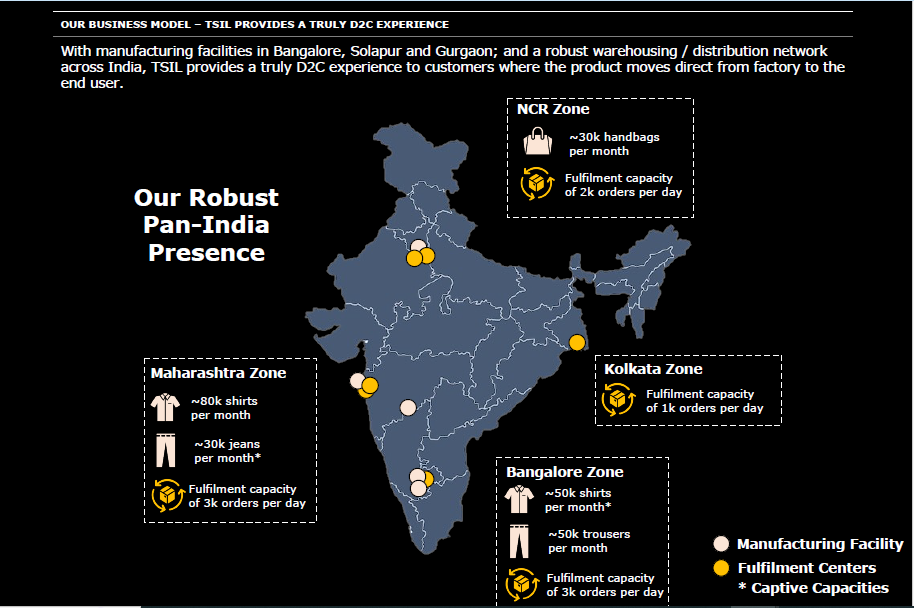

- Scaling Up Operations and Faster Delivery Options

From being a B2B brand at start of FY 2022 with a single manufacturing facility in Solapur , Thomas Scott has quickly expanded the reach throughout the country with manufacturing spread across Maharashtra , Bangalore & NCR area and fulfillment center across all corners of India with a capability of supplying 9000 orders per day.

Another unique moat due to their own manufacturing facilities and being integrated is that they start of with small lot sizes ( 120 MOQ ) of any style for manufacturing which is 1/4th of MOQ if you want do not have your own manufacturing , and then based on the demand for the style they can decide whether to create more styles or not .

They are targeting a 2 day delivery to over 30% of their customers based on their pan india fulfillment center , which is essential as customers preference is leveraged more towards products with faster delivery options . This can be vetted by checking their delivery times across various platforms ( Myntra / Amazon / Flipkart / Ajio )

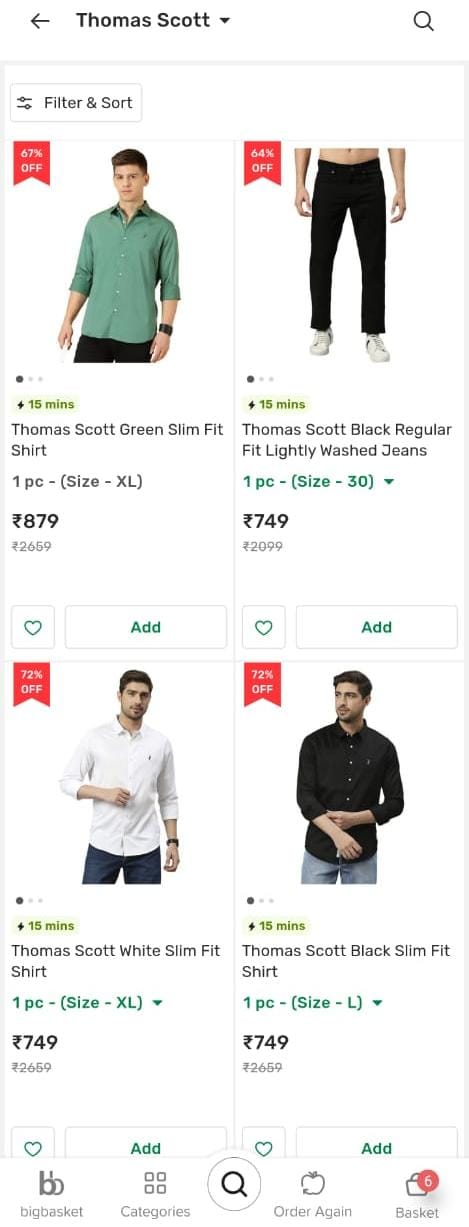

In fact in Bangalore , they are also doing Hyperlocal deliveries partnering with Bigbasket ( delivery within 10 to 15 minutes )

Thomas Scott has become an Alpha Seller on the ecommerce platforms. Thomas Scott was leveraging its related party Bang Overseas for selling on ecommerce platforms as Thomas Scott was not granted the Alpha Seller status due to financial entry

barriers imposed by certain channels . Source Annual Report FY 2024

Now that Thomas Scott has been granted the Alpha Seller status the related party transactions between Thomas Scott and Bang Overseas should reduce in the coming years. This is a key monitorable in my opinion .

Financials

From FY23 onwards we can see an exponential increase in the revenues of the company

This along with the Industry Growth rates and the TAM , if the execution continues in the coming years could ensure that at least 30 to 40% revenue CAGR can be continued over the next 3 to 5 years .

ScuttleButt

As a part of their future plans Thomas Scott ( India ) has launched 5 stores in Bangalore on CoCo & Franchisee Options. The CoCo stores are over 2000 sq ft and the only franchise store currently is around 600 to 800 sq. ft.

I have visited the Franchise Store at Marathahalli and below are my observations

-

Wide range of products majorly in Shirts & T-Shirts . Quality was good

-

Pricing is good . Shirts & TShirts in the range of 799 , Trousers & Jean in range of 999 , Blazers starting from 3000 and handbags

-

The fresh stocks are first displayed in the stores , every 15 days fresh collections ( 100 to 150 SKUs ) are provided to the stores and they can send the non-selling SKUs back which are then supplied on the ecommerce marketplace. This was also validated by the manufacturing date of a few shirts I tried and all of them were either Sept / Oct / Nov manufacturing by Forever Clothing Company. The store manager was mentioning there is no problem of stocks supplied by the company

-

They are actively looking for Franchise options . 2 more franchises are about to be signed in Bangalore .

5.The store I visited was the smallest store around 600 Sq. Ft and during my visit I was the only customer in the store.

- POS System in place and the store godown was full with inventory

Couple of photos from my visit.

Risk :

Related Party Transactions with Bang Overseas must be done at arms length price. It was mentioned that due to financial backing , they were not able to obtain Alpha Seller license which has now be granted to Thomas Scott. The related party transactions must reduce gradually for Thomas Scott

Other Info

Niveshaay Hedgehogs has recently taken a position on the script from the Open Markets at approx Rs. 356

Some other articles about the company

Summarized

Thomas Scott has successfully pivoted its business model from a B2B led brand to B2C brand focusing on the data analytics , technology , faster delivery , quality and premiumization as the pillars for its growth . The sectoral tailwinds and the promoters past work experience and qualifications could ensure that the brand can comfortably grow over the next 3 to 5 years .

Disclosure : Invested and biased … forming 2% of my existing portfolio .

Update : 23/12/2024 . Adding a detailed research done by @CA_Swapnil_Kabra on X

Main Report.pdf (1.5 MB)

Thank you for the PDF @Souresh_Pal