Sold out BSE today. Not played upto expectations even before last 2 days and wanted to add cash for next set of buys.

@Mudit.Kushalvardhan

You were right. Got battered yesterday. But long term looks extremely cheap and stable. Will keep holding and if goes below 400 will look to add.

1 Like

Was just looking at Differentials between US listed companies and the Indian subs of the same for research purposes over the last week.

Cummins Inc

Market Cap: $37 B

Revenue: $32 B

Net Income: $1.94 B

ROE: 19.6%

P/S: 1.3

PE: 18

Cummins India

Market Cap: $12B

Revenue: ~$1.1 B

PAT: ~$200 Million (other income of $50 million)

ROE: 28.8%

P/S: 12

PE: 63

Yes, Indian sub is growing faster at 30% vs 10% but P/S and PE are out of whack. And historical PE ratio is approximately 32. Yes, I know about CPCB4 series on engines.

Same story for ABB, Siemens, Hitachi and others where Indian subs are at PE of 80/100/120 vs Main company at sub 20 PE. The entire cap good space is indefensible in terms of pricing. Below I have attached chart for NSE MNC index PE ratio

The Green line refers to PE ratio and is almost touching 50 now. Would love alternative comments on this.

Have exited BSE.

While it has considerable growth prospects, the govt is showing considerable intent on cracking down on F&O activity. Whether it be from statements from RBI, FM and SEBI.

Have exited with minor losses around 2750 and 2650 over last 2 weeks.

2 Likes

Added 2 positions last week and this week,

- 2% PF addition on Manali Petro.

- 3% PF addition on Swan Energy.

- 3% PF addition on Religare Enterprises

Have ample cash but waiting to deploy.

Worked out well at the end of the day.

1 Like

Would you plz share the rational for these and the exit triggers?

Thanks

- Religare is more of a special situation play where Burman’s have a real probability now of taking over. It has ample corporate gov failures in past and present is not so good. But it has a good insurance franchise and some other decent assets. As a negative, however this story is playing out for last 18 months and probably will continue for some more time.

2 On Manali Petro: @LarryWink Kindly help out the gentleman.

3 Swan: Pure punt I have taken. If they are able to execute of Floating Storage and shipbuilding oppurtunities they can do well. However its an extremely risky play as company has multiple moving parts, managment execution and quality is suspect and ofcourse CG concerns exist.

I will not add more to all the three positions taken here and fully expect to lose money on atleast one of them.

1 Like

Manali is the only chemical stock i have in PF, where i recently bought some, @~93, ~1% of PF. In my understanding its one amongst few in chemical sector which are bouncing from bottom, to me its part of technical + funda bet.

As per my understanding We have good petrochemical demand going forward, if we look at the India’s manufacturing push as a whole.as govt is mulling anti-dumping duty on flexible slabstock polyol(i havent study details on its impact on manali but if implemented it would be nice for it)

Here are threads on VP >Manali Petro- Capacity Expansion - #35 by nitin_g, 52 week highs and all time highs strategy - #937 by hitesh2710

and …?, i am the new recruit, who is learning to be a good follower. so it might be far from an expert view or recommendation, !

1 Like

Have not shared updates here for almost 6 months.

Have been churning the PF regularly. Main reason not to post updates.

Will post current investments and what I am looking at tommorow.

1 Like

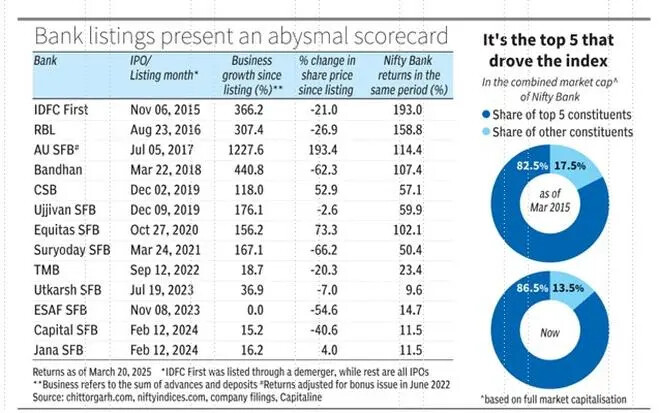

The Search for Next HDFC Bank- Boomeranged???

More money has been lost by trying to invest in ‘The next HDFC Bank’ than in doing nothing and allowing inflation to erode it away. Any doubts, check with the long-term investors in bank IPOs over the last decade..

Very interesting read. A sobering reality that there is no next HDFC Bank.

1 Like