Polycab is just the latest trigger but its beyond that as you have mentioned.

To be honest as anyone who has run a business of any size, knows exactly how books can be cooked to cover regular needs. So these things are cooked/disregarded into valuations. The problem when scale of the cooking exceeds expectations, then it causes deratings.

On second point of MNC/promoter group companies in same lines of business. You are indeed correct, another big issue in Indian Markets which will never go away.

My broader point was on how to value these gaps and have an mental arithmetic for discounting it. In other words what metrics should be used to give an x+y% valuation discount. I beleive as an CA you would be well placed to through more light into the matter.

Thank you for your observations. My question is what methodologies do we use to segregate these companies say into A/b/c segments and what would average valuation discount be given, As it is personal judgement let us stick to known problem areas. Would love your arithmetic on this.

One thing that can be done is to go deep and link all the aspects of business to the reported numbers, and see if there is any connection or disconnect to the facts found and the market price. If we perceive something to be not right, and cannot be ignored, then it would have been noticed by many, but still if price is in upward trajectory, either we can go along with the market with the knowledge that at some point something can happen, may be it will or it will not, or choose to not participate. There was a new company that was introduced to the forum recently, wherein, someone replied not to invest but did not give any rationale, for obvious reasons, which can be interpreted as the person knows something. Of course, these in general are small stocks, and the element of price management always happens, price is volatile, so investors are usually careful, more so when the shares are traded in lots.

Also, there are threads in the forum, where certain aspects are questioned, and members raising some objections, later something happened and such members are proved to be correct etc.

Another thing that I read is that, managements may have done something wrong in the past, but they have become clean since then, so there is new interest from the market participants.

I personally cannot weigh the issues, even if I have found any, and I don’t know how to connect the found issues to valuations.

And there exist members who have shown interest in the stocks even if something has happened, after price has fallen sharply, to them, these are opportunities.

Thanks for this. I remember reading the corporate misdemeanor thread fully when i joined VP. Need to relook again.

The thing is with sme and smallcaps these things keep coming out of the woodwork. One reason i dont invest in sme is this.

P.s : I have absolutely no problem in investing in turnaround and corp governance hit companies. Invested in CG Power after Murugappa group takeover(Turnaround was not guaranteed). Invested in Suzlon at 6Rs and BCG at 10 Rs :). But Suzlon and BCG i knew that its just a ride and sold when i made 150%. Did not want to risk more.

So as long as u understand the investment basis and fully have the drawbacks in mind along with knowledge it can all go to zero, then you can invest.

Pointing out couple of core paras rather than making my points, Below is taken verbatim from the essay.

View each quarter as one more datapoint in a continuing trajectory, not in isolation.

""Answer starts with making such pictures, so as to internalise inherent lumpiness of long-run trajectories of good businesses. And then incorporate the same into short-run expectations. Use business history, rather than strangers’ estimates, as our guide to analysis of quarterly financials. Realize that that even the act of producing precise quarterly estimates is as arrogant as it is futile. Over the long run, good business invariably do fine, while following a path that is assuredly and extremely volatile. To borrow Pulak’s quote, “Nothing goes up in a straight line”.

Since all trajectories are bumpy, keep wide bands.

Awareness of long-run trajectory makes a compelling case for banning ‘basis points’ as unit of financial analysis. Plus or minus 25% swings in typically tracked metrics (revenue growth, EBITDA margin %) are a feature not a bug. For a company with 15% long-run average margin, a 12% or 18% quarter is normal, not exceptional. Ditto for revenue growth or working capital intensity. Explanations for deviations sound plausible but are actually made-up, usually to fob off pesky questioners on conference calls.

Approach financial results with wide error bands around a general long-term trend. Swings within this band generally merit a shrug of the shoulders, not activation of neurons.

Focus on controllables: relative over absolute performance, balance sheet over P&L.

Companies have little control over the metrics we obsess over – revenue and profit growth – at least over the short run. These are determined by industry growth, stage of business cycle, commodity inflation, exchange rates and base-period. Often, these effects are extreme.

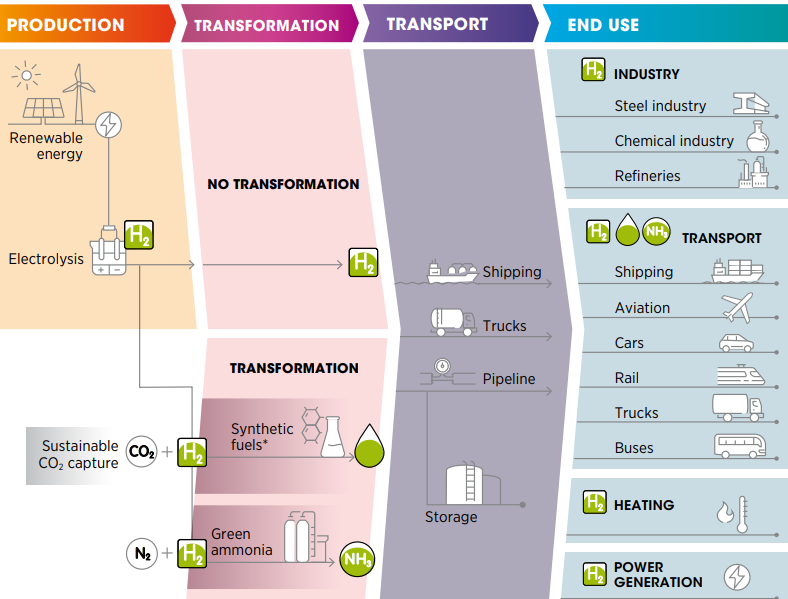

Hydrogen as theme, it would be better to look at pipelines, hydrogen storage and maybe a few of processor companies. No point buying RIL or any of the large caps as even at peak Hydrogen will form small percentage of revenue.

InoxCVA, Confi petro and time techno are involved or contemplating hydrogen storage.

Read below for more understanding, We have two options. Proton Excgange Membrane and Anion Exchange Membrane. Corrsponding advantages and disadvantages mentioned below.

Conscious decision to build a more researched and concentrated PF.

Few additions. Mostly added to existing Pf or companies in which i had been invested before like CG Power.

Kalyani Steel is under study. Strong promoter background, upcoming plant in Odisha should change their trajectory to higher range of products. Missed out on Solar play so have added swelect.

HCC i bought and sold twice in last two months. Overall average at 33.5 Rs.

CHolafin is only one where i am unsure what to do. Holding since last six months and above.

Have Sold out SJVN which provided huge profit for this current fiscal year. Overall, pretty good year.

Expect next year to be tougher for equities.

Also have 25% in MF with PPFAS Flexicap on SIP basis.

So, BSE I had originally bought in may of last year from 520 till 700 and then foolishly sold it at around 1200 odd.

Missed buying it again at 2200 two months back.

This was a opportunity to buy it back for me and me making amends for selling it early like a fool.

The Rationale is simple. The BSE thread has great insights and details I do not want to repeat here.

My outlook is even lets say the markets slow down and derivates volumes cut by 25% we are still looking at it doing 1000-1100 CR topline and 600 Cr bottomline at worst estimates.

BSE cash turnover has started going up and I am hopefull will stay strong.

At 50x PE it’s still cheap for something which has a long runway ahead even in bad times.

Equity markets have just started to take hold in India at a mass level. The management is aggresive and launching new products.

There will be redflags out there like this sudden penalty but I believe its more of a buy on dips opportunity.

Added REC on Friday and today. Have added funds to this to purchase. Have made it 15% of portfolio

This is before news of BSE 100 addition.

Two things that led me to take the plunge is robust loan uptake, a good cleanup of NPA.

Can anyone point out what % of its borrowings are short term and % long term. In case in second half of the year we get RBI rate cuts, how does it impact NIM.

Exited Swelect on Friday. Was a short-term play and felt overvalued based on results. Will most probably rue this but it is what it is.

Wanted to put some more thoughts on why picked REC.

Power and Infra is going to be the extremely important over next 5 years.

India is estimated to spend at least 7 lakh crores across on power-renewable+thermal+nuclear and distribution.

So REC wants to grow loan book from $62 billion to $ 130 Billion in 6 years. that puts it at CAGR of roughly 14-15%.

Using green bonds and overseas borrowings to reduce cost of funds. Improvement in NIM and final spread.

So it will be story of scale. Non POwer Infra loans will get better pricing and NIM’s.

The cake has been eaten in the last one year since price has tripled. However i beleive there is room here for a solid 10-15% + dividends type of growth.

At portfolio level this year I have pursued and now Continuing to keep a barbell type of PF with highly risky investments in Wockpharma and HCC and a more solid companies in Tata consumer and REC/GAIL.

Will keep adding this year based on SIP.

I will be happy if I can pencil in 15% CAGR at pf level over next few years considering the good returns last few years.

Was listening to the Thermax concall last two quarters.

I am astonished by how clearly Mr. Ashish Bhandari speaks. He just owns up to the fact that in one or two projects how they missed up operationally because of XYZ reasons and takes responsibility for improper execution or planning.

.

I am not invested here but extremely refreshing tone. Hardly see this in many company calls. Most concalls the CEO or promoter explains away something because of external reasons but never take responsibility.

This is one company that i regret not investing in despite tracking for last one year. Was always put off by the PE and how expensive it was, and it just keeps going up.