Hi Ghanshyam,

I agree that NAM looks like a good opportunity, given their MNC background which generally fetches higher valuation in Indian markets and strong recovery in investment performance. The broader investing style of NAM is value investing which is very similar to HDFC, and both have seen exceptional recovery in performances in past few quarters.

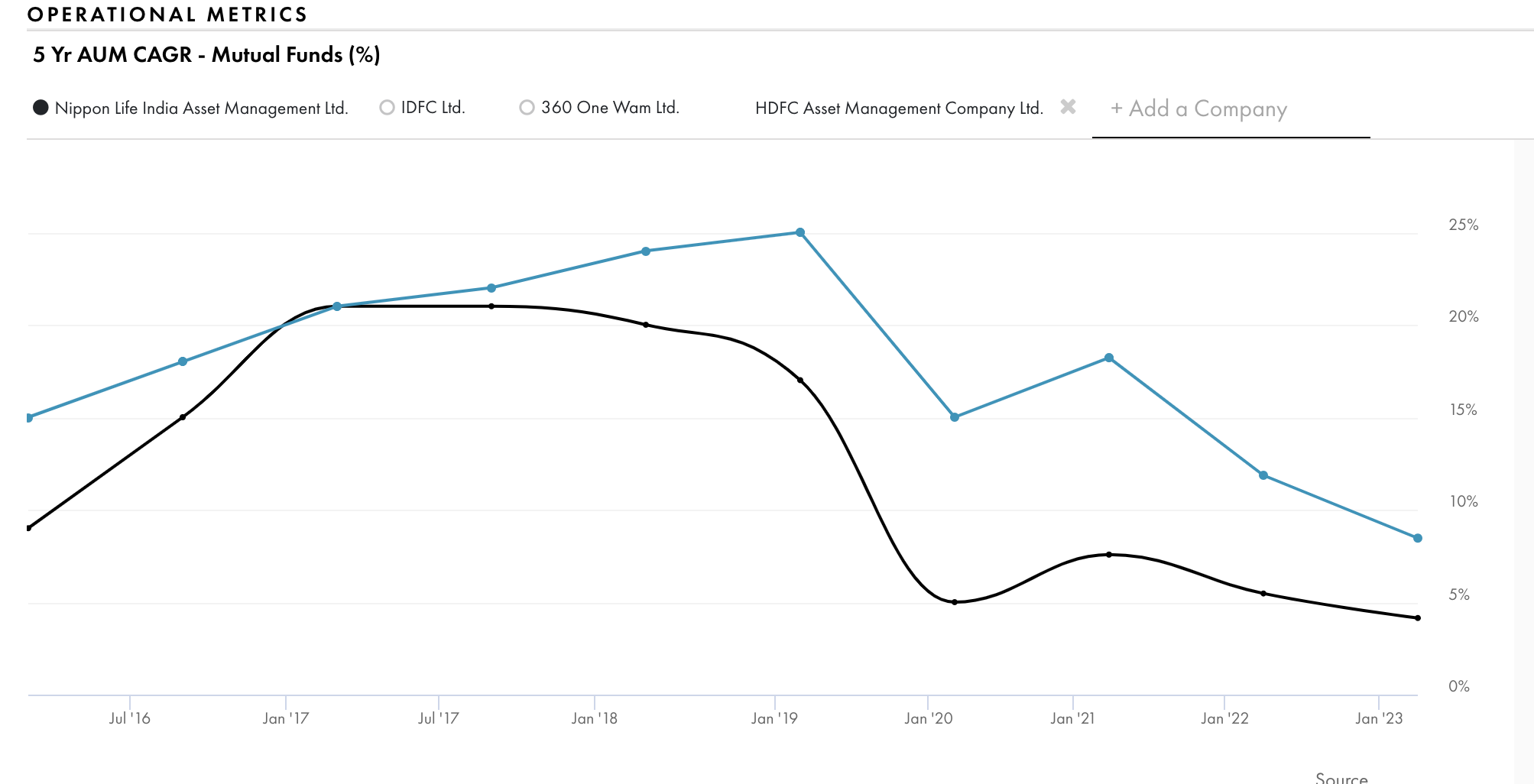

This being said, I feel bank backed MFs have a structural advantage over non-bank backed MFs (superior network). This is clearly visible in growth over longer periods of time. Until March 2023, HDFC AMC always had higher AUM growth.

Even from March 2023 to June 2023, HDFC AMC witnessed higher growth (@15% from 449bn to 516bn) vs NAM’s growth of 12% (from 295 to 329bn).

ETFs are very low yield commoditized businesses and most ETF money is driven by one large customer (EPFO). If we see a shift to ETFs over a long period of time in India, the entire industry profit pool will evaporate. Just as an example, I am also invested in a German asset manager who are leaders in ETF and passive products. This co trades at very low valuations. I try to buy them when their enterprise value becomes negative (meaning business becomes free) or their absolute dividend yield approaches 10%. I am worried if ETF trend picks up in India, consequence might be catastrophic for AMC businesses.