VFC seems to be an interesting stock to analyze. However, looking at the chart, I feel that market might be knowing something that we are probably overlooking. Other than, D/E ratio going to 2X from 0.5X, I can’t find anything bad so for.

Question:

Why did the Debt/Equity jump suddenly during CY19Q4?

When these debts are maturing and are they facing refinance risk?

@harsh.beria93 How does the change in debt taxation figure in your future international investments ?

The change in taxation to income tax slab & not as capital gains looks to me like a significant deterrent for future investment.

Please let us know your thought process.

Hi, I am a non-resident Indian living in Switzerland, so these tax rules don’t apply to me.

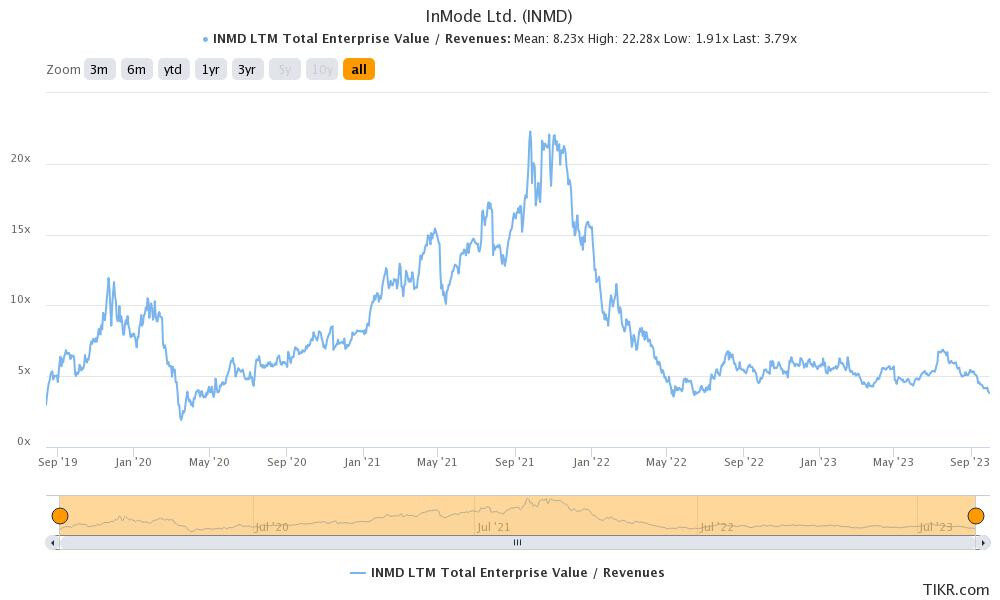

If I was investing from India, I would have still diversified globally because of the massive opportunities abroad. For e.g. last year I was buying InMode which is an amazing business (80%+ gross margins, 40%+ EBITDA margins, 40%+ ROIC) growing at 25%+ rates and I was able to buy it at 10x PE. There is not a single business in the Indian listed universe which has these kind of risk reward.

Similarly, I bought Markel (speciality insurance co) at book value or the largest German AMC business at negative enterprise value. These kind of opportunities are just not available in India and I am happy in participating in these even if I have to shell out higher taxes. Hope this clarifies my thought process

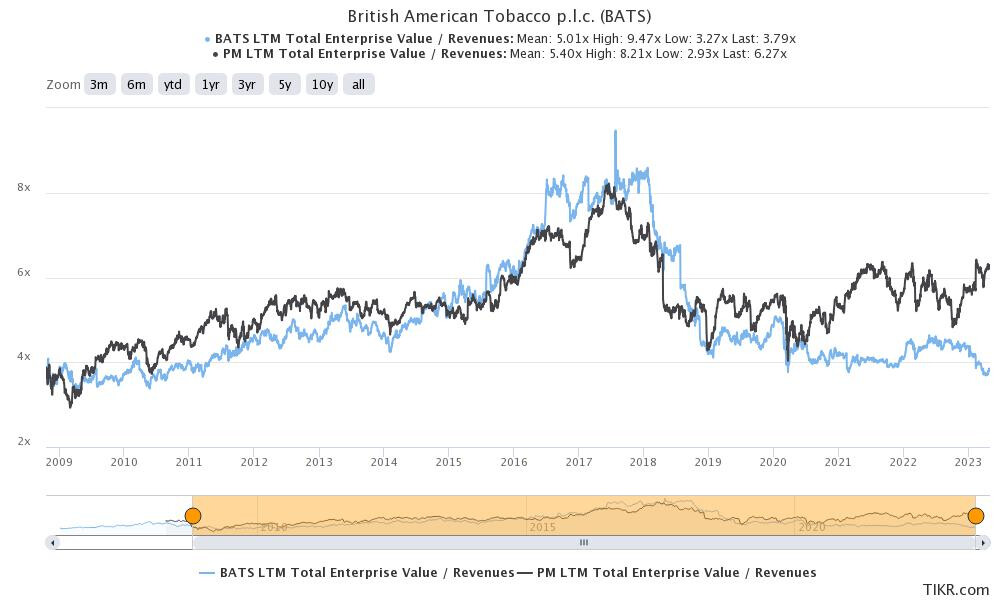

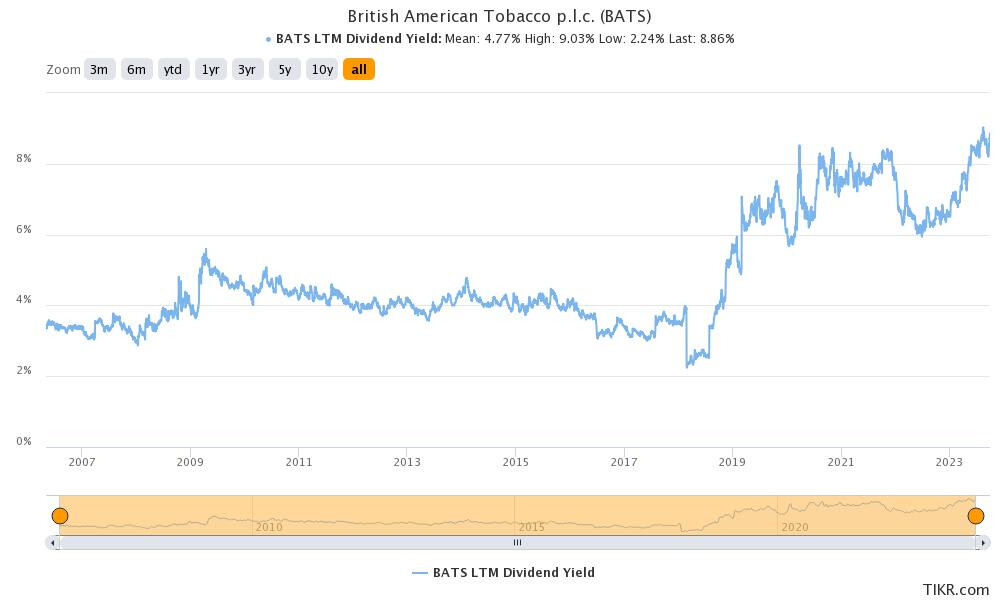

As of today, I switched from Phillip Morris to British American Tobacco. BAT has much higher dividend yield and almost the same business profile as Phillip Morris.

In terms of EV/sales, both have traded at similar multiples except since 2020 when valuations have diverged. I attribute this partly to problems in UK and general risk aversion of investors towards UK market.

To value, you have mentioned to EV to Sales across multiple businesses. Do you feel it is a right metric for almost all stable businesses? Or is it just a sample and you use other relevant valuation ratios too?

Your thesis points are heavy on business model, triggers and valuation. Do you also study the books of accounts in depth? Do you think the chance of accounting jugglery in large and established US businesses is low given relative tight laws?

As of today, I have added 2 stocks to the portfolio. This reduces cash to 11%.

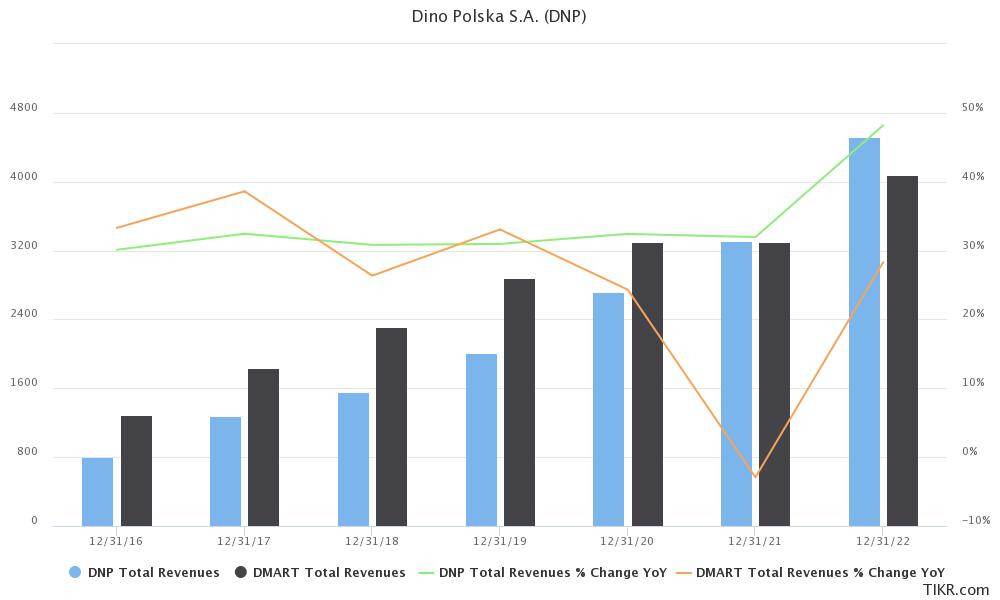

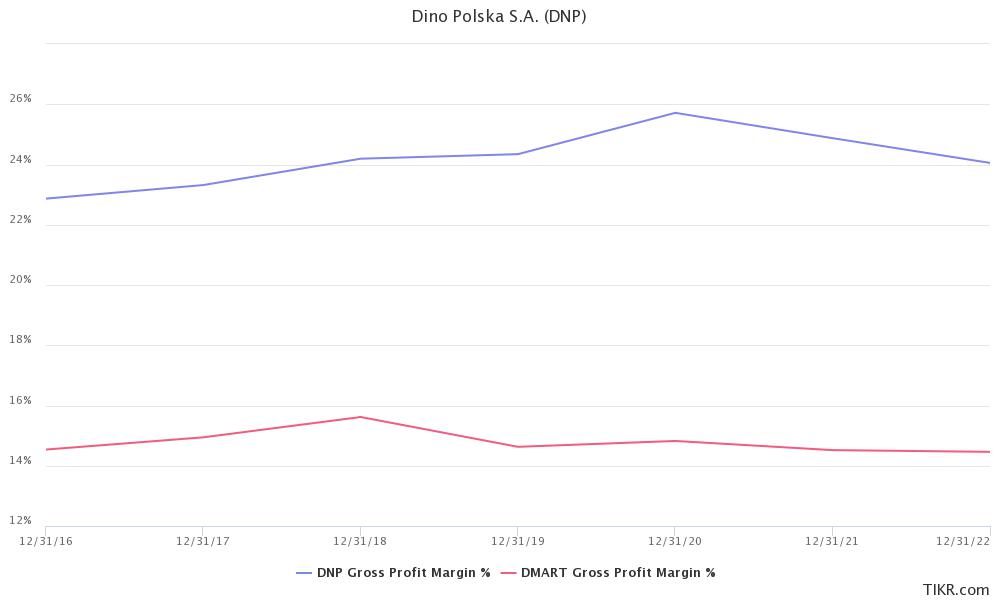

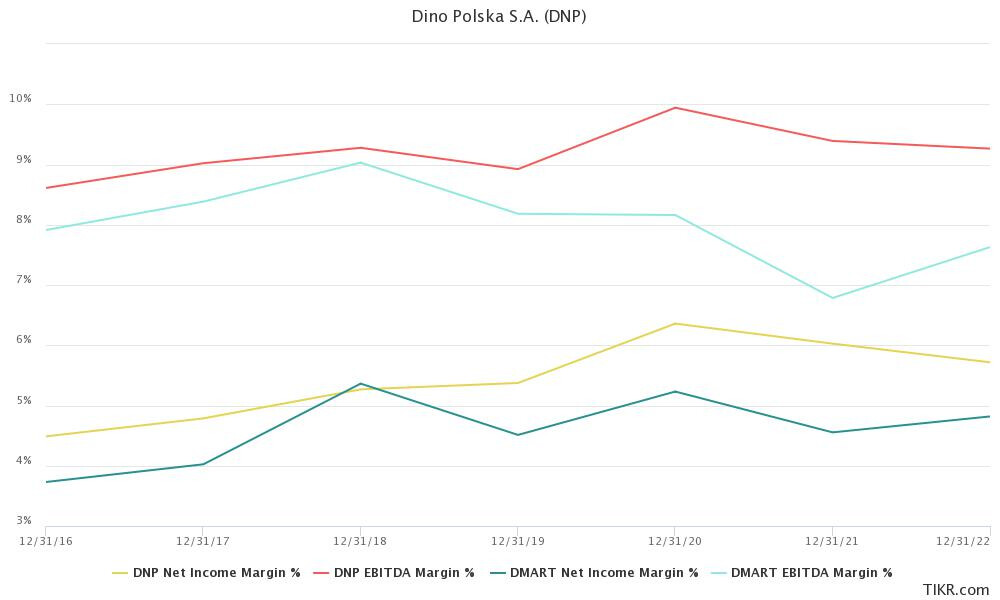

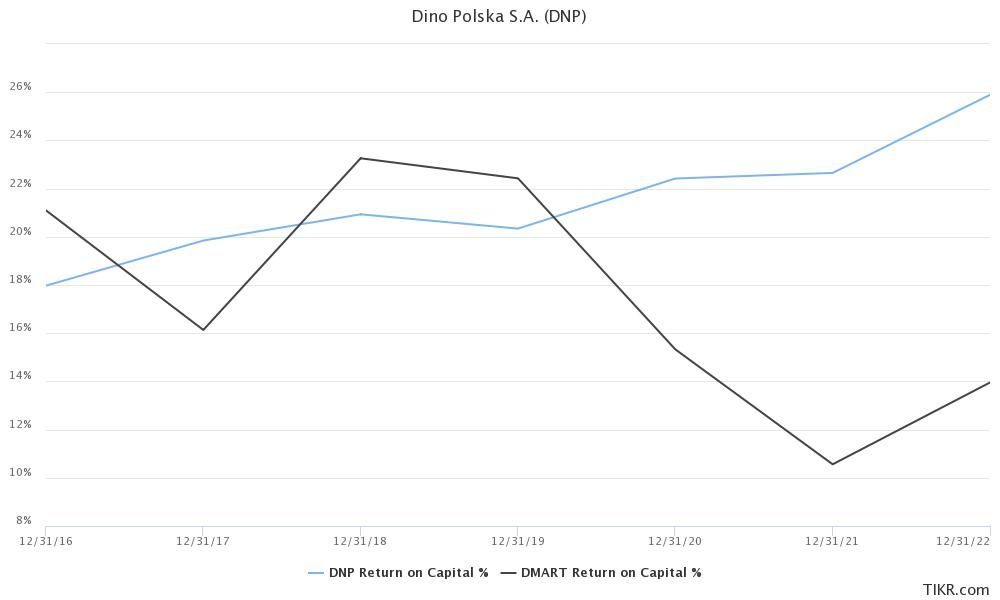

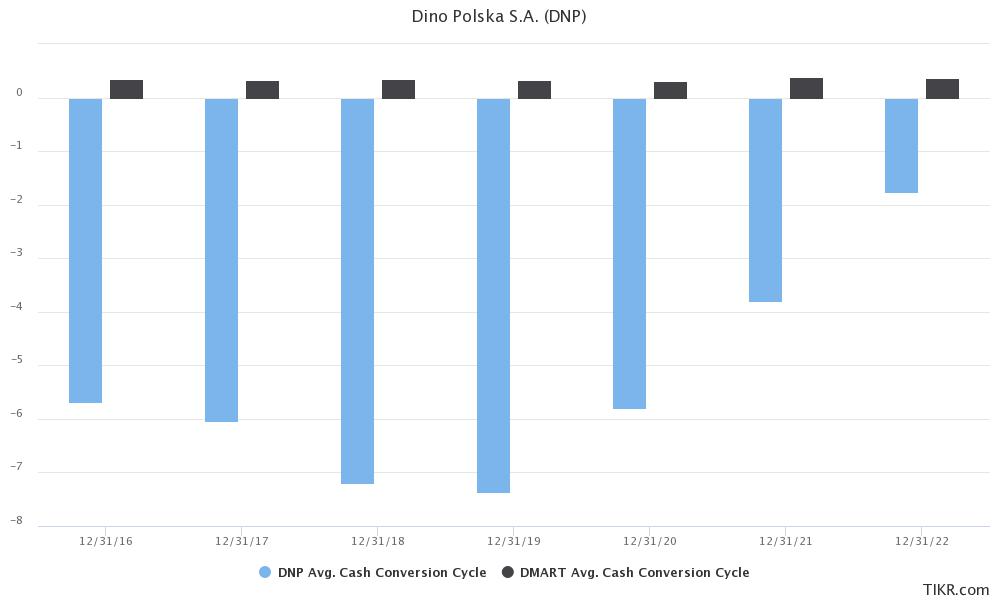

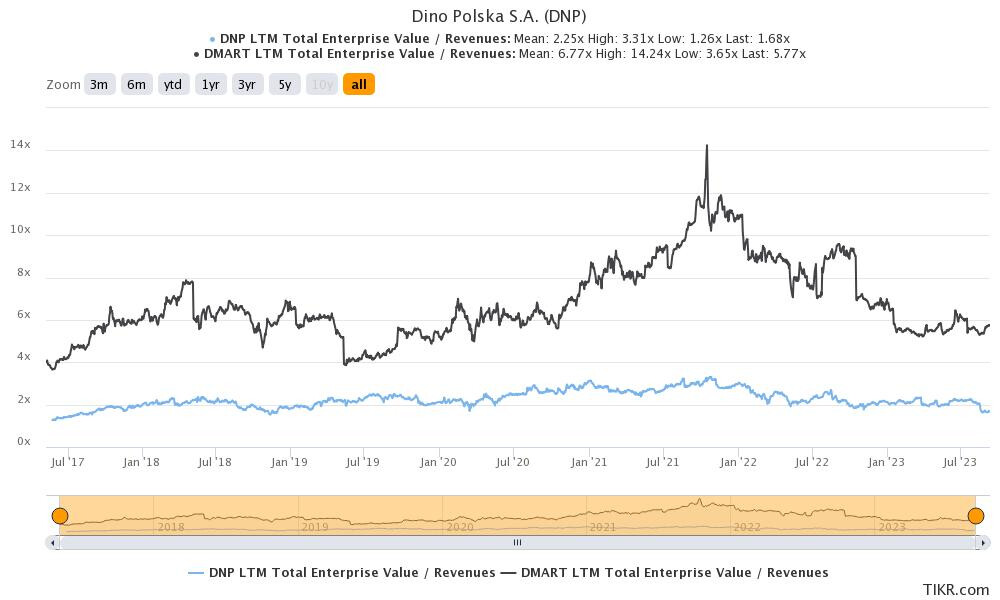

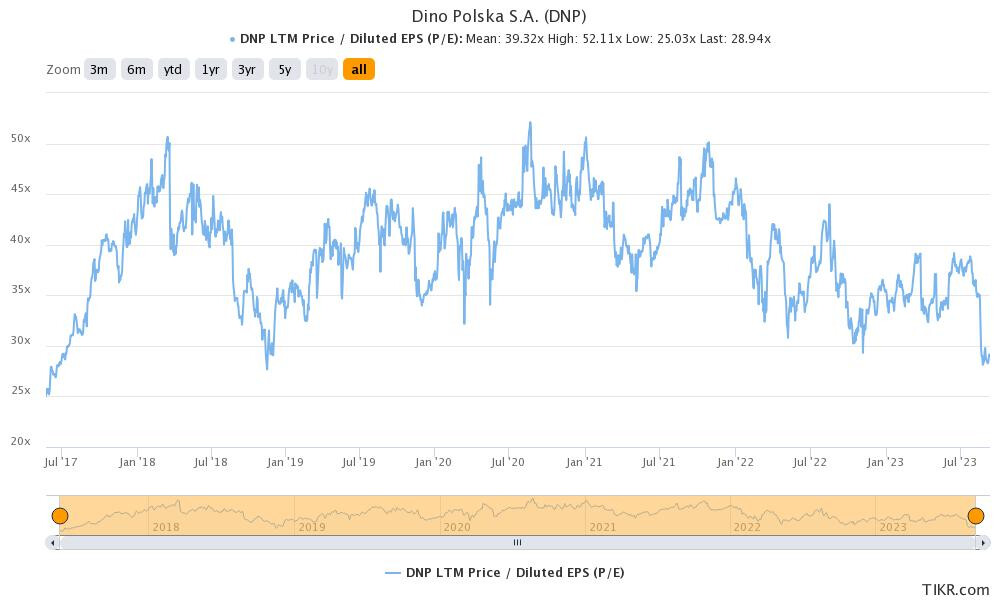

5**% position in Dino Polska SA:** The original idea came from our in-house Polish expert @rajanprabu . Dino is a retailer based out of Poland and has done amazingly in past few years. Just to give some context of their scale, I will compare their numbers with Dmart.

Sales growth (since 2016) for Dino has been 33% (vs 21% for Dmart).

If Dino was listed in India, I dont know what valuations people might have ascribed as they are superior on every metric vs a Dmart. Actual valuations are half of that of Dmart. So I am getting a superior business model growing faster at less than half the price (thank god for global investing!)

Dino has been consistently been bottoming out at ~25x PE and their current valuation is ~28x, so its towards the lower end of valuations. Lets see how this position works out.

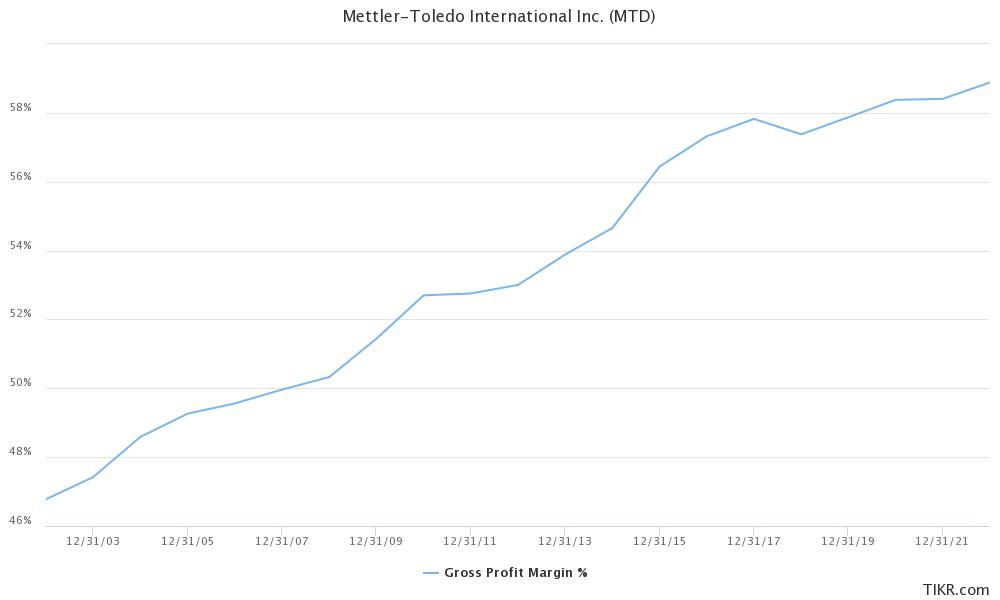

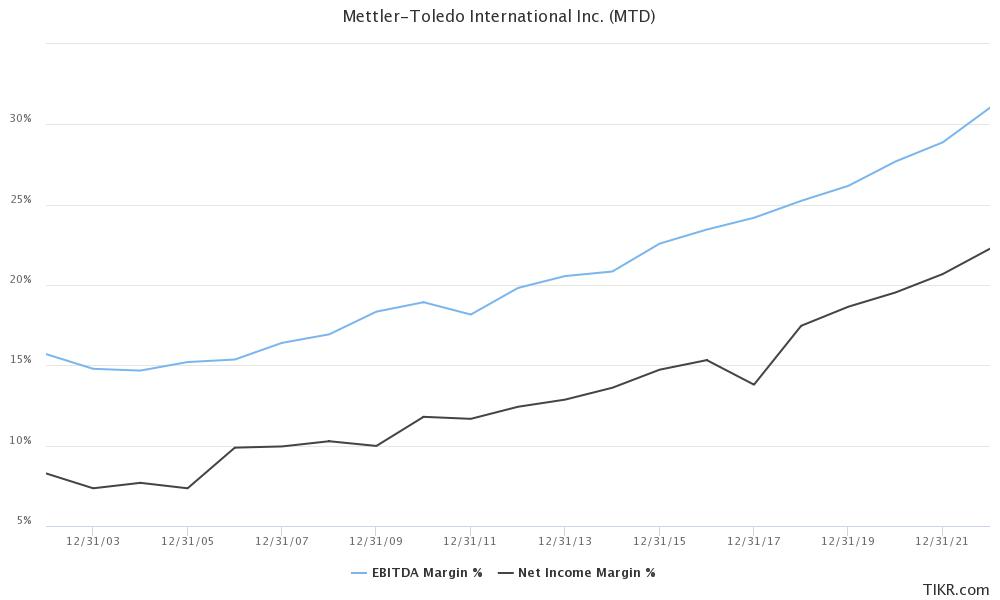

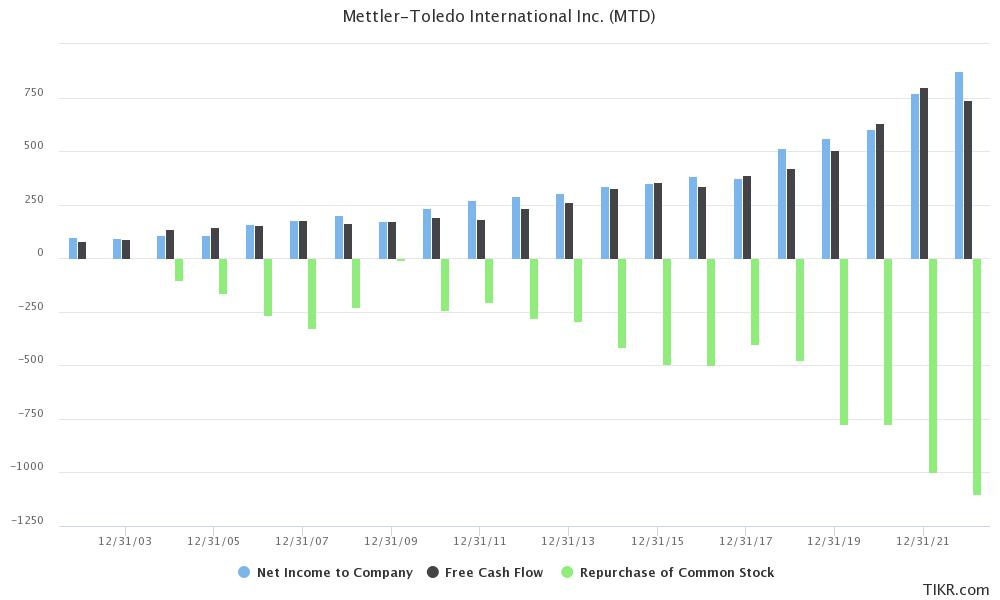

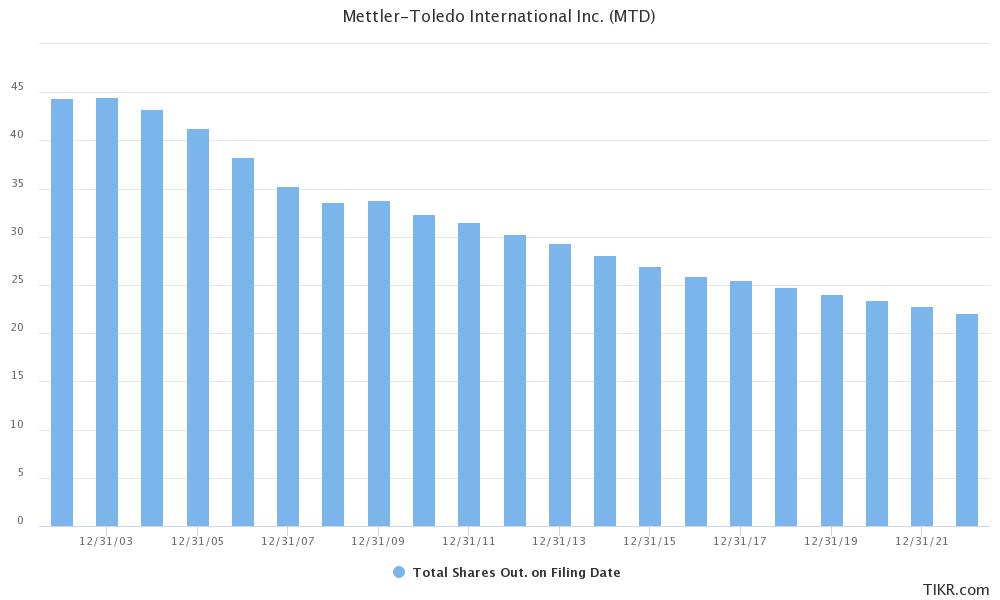

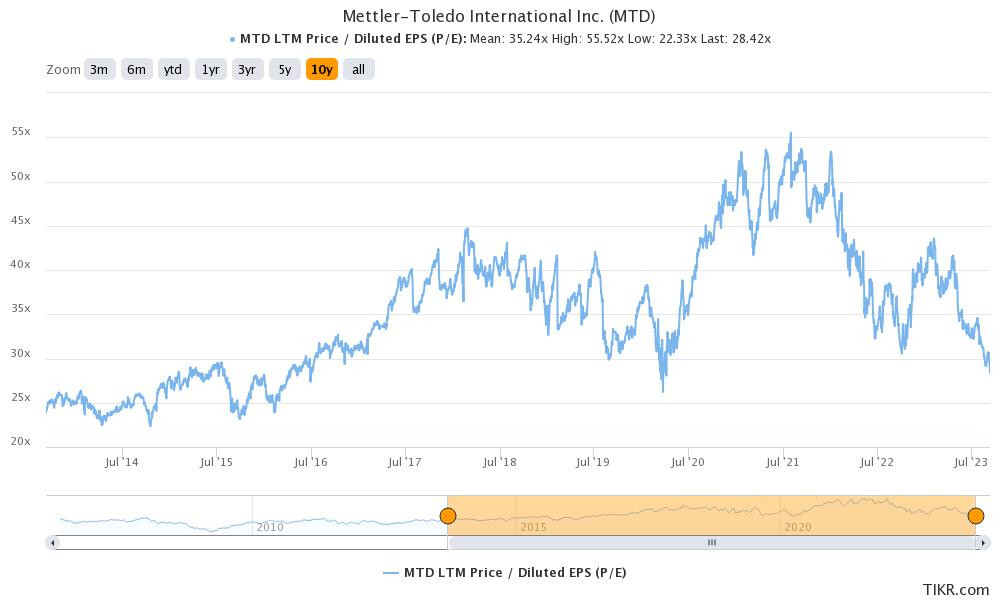

2% position in Mettler-Toledo. They manufacture lab instruments and have been industry benchmark for close to a century. I will share few numbers about this business:

Consistently increasing gross margins, leading to improvement in EBITDA and PAT margin over years.

They generate about $800-$1bn in profits and freecashflows, and they use all this to buyback their shares. As a result, their sharecount has kept decreasing over time.

Just to give some context, net profits have grown from $100mn in 2002 to $872mn in 2022 (11% CAGR). But their EPS has grown from 2.21 to 38.41 (15% CAGR) due to consistent buybacks. This is a very high quality and sticky business and they are trading at lower end of their valuation band. This is largely because they saw a large boom in business during COVID which has now normalized and market has derated them. Lets see how this works out.

I try to find mean reverting variables in terms of valuation, it makes the entire exercise very easy. For mature businesses with stable margins, EV/sales looks through business cycles and is a good metric.

I largely focus on free cashflow generation as a filter for accounting jugglery. By no means its perfect as companies can easily manipulate free cashflow. However, if a company returns a large part of its free cashflow to investors, its highly unlikely that they will be fudging accounts. But it can still happen.

Hi Harsh,

Any idea about the freefall in Inmode, it has declined from 45 level to 35 now despite delivering good results consistently. Few worries I see are-

i- High cash on book, Co. not using it for buyback or dividend

ii- other is they are talking about acquisition, the acquisition may not have same margins as theirs and consolidated margins may fall.

ii- Low spending on RnD - Market is still not able to understand how they make 85% gross margin despite low spending.

Do you think Disney is good buy at current level. As there are issues with their streaming and broadcasting businesses. However, Their theme park business will do very well going forward because of higher demands. If you can share your thoughts and holding thesis.

Hi Harsh, I would like to know if you considered Stellantis in your portfolio? And if you have, what were the reasons for you to not add it in your portfolio?

Share price fall: Its very common for share prices to fall a lot, I have seen Inmode falling from $100 to $20 without any deterioration in business quality. So this fall doesn’t seem too much.

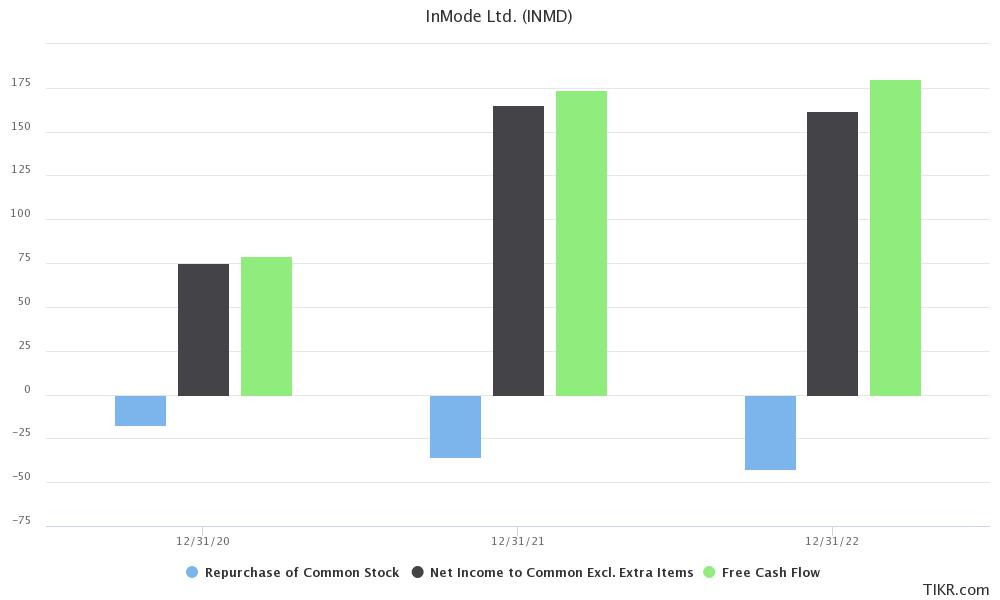

Dividends: I dont know why most of NASDAQ cos do not pay out dividends, despite generating high cashflows. That being said, InMode does regular buybacks and has bought back $95mn worth of shares in last 3 years, which is 22% of their freecashflows over these 3 years. This is in-line with most growing cos, I prefer them to reinvest most of their capital in their business.

R&D: They spend $10mn on R&D each year, they have kept the absolute spends constant in last 3-years, while growing sales from $200mn in 2020 to $500mn now. Thats why % spends look lower.

Acquisition: Its hard to make a generic comment on it, let them do something first before making a judgement on it.

I have been regularly buying Disney shares, I do feel its very undervalued. Over time, risk has reduced significantly in Disney as they have invested in building their streaming business and diversified beyond their linear TV business. Currently, market doesn’t like streaming cos, but just 2 years back market thought that streaming cos will rule the world. Over a longer period of time, its content which will make the difference. Whatever the distribution medium is, content will find a way to get monetized as long as customers want to see that. I feel Disney has one of the most precious contents, and they continue investing in that. Park is a decent business, and is currently doing very well.

I am finishing up my work on Stellantis. I will likely buy it soon, its crazy cheap!

I saw that you are using interactive brokers. Can you share it’s review with us once? I have done my research but wanted to get your opinion, if you’ve explored any alternatives as well.

Global markets have turned very jittery in the past month and I have been finally able to deploy some capital and reduce cash position.

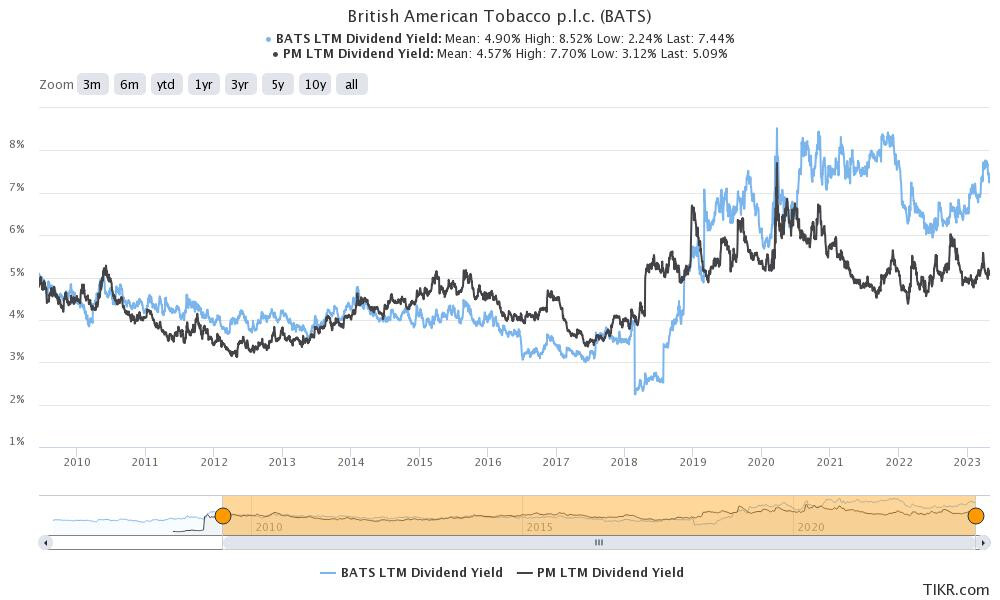

Increased position size in British American Tobacco to 5% (from 2% earlier). Its just ridiculous the kind of dividend yield this company is trading at. I find it very very hard to believe that there is any chance of capital erosion in this scrip.

Increased position size in InMode to 5% (from 2% earlier). Since 2019, there have been 4 instances when their valuations came below 4x EV/sales. I have been a buyer at last 2 occasions. Company continues to grow at healthy 20% CAGR and is trading at 14x PE and 18x price/freecashflow. I think its a good opportunity to increase position size here.

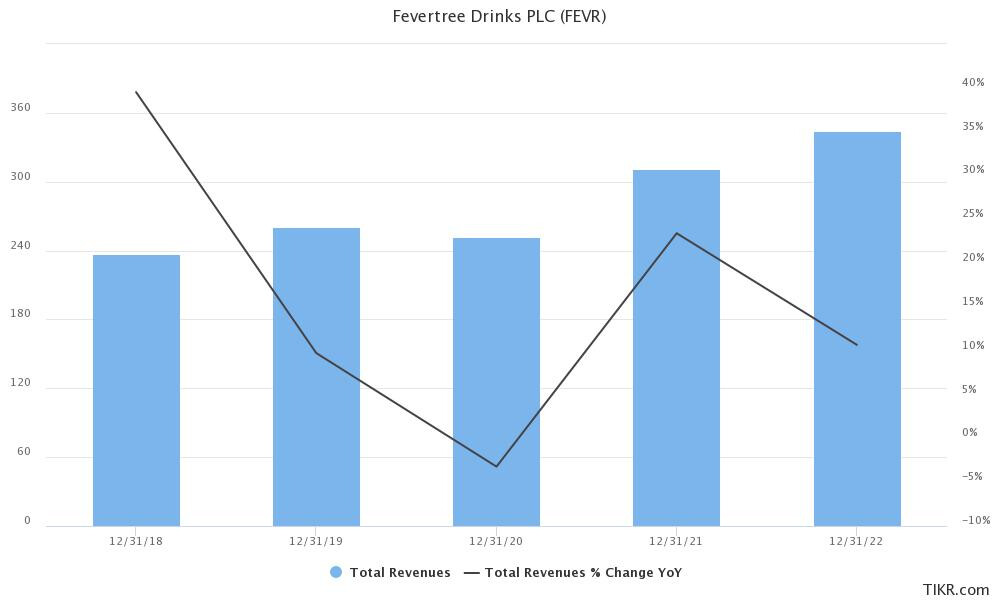

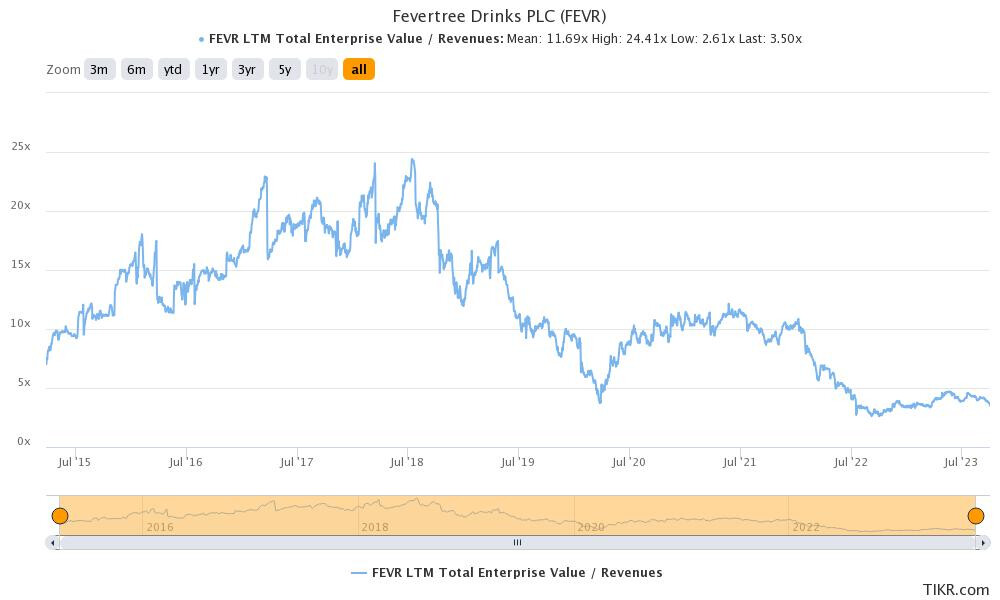

Added 2% position in Fever tree drinks PLC. Fever tree created the mixer drink market with 50% market share in UK. They have foreyed into US recently, where the opportunity size is much larger. In recent times, their margins got hit as glass prices increased a lot and they didn’t pass on price increase as their focus has been on increasing market share. I feel this margin wobble is a temporary issue and company should prioritize market share gains. In terms of valuations, they are trading towards the lower end. On a personal note, I love their mixer drinks!

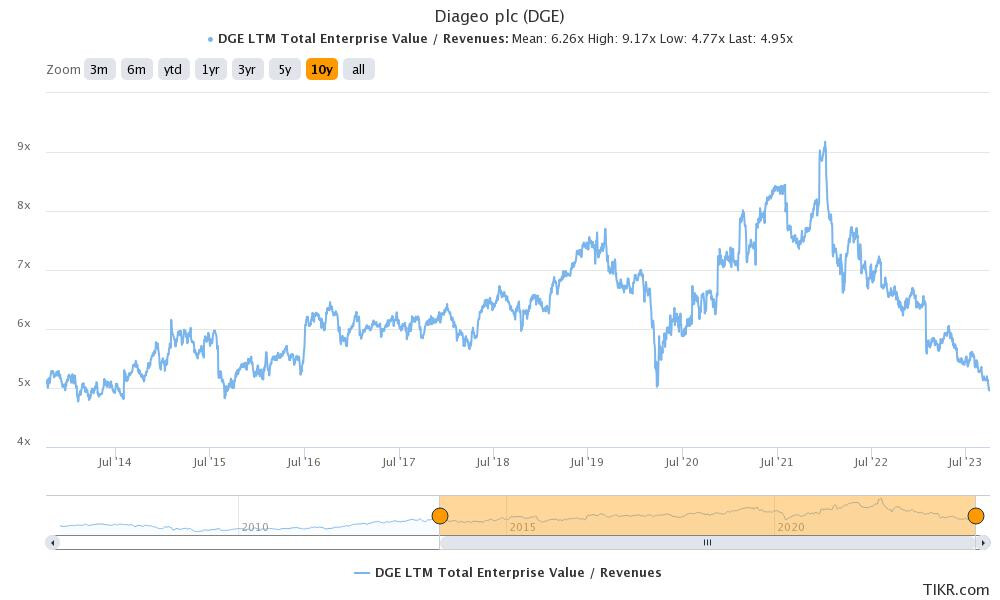

Added 2% position in Diageo. Diageo has been a market leader in whiskey and scotch for a very long time, currently they are trading at lower end of their valuations, which gives an opportunity to add shares.

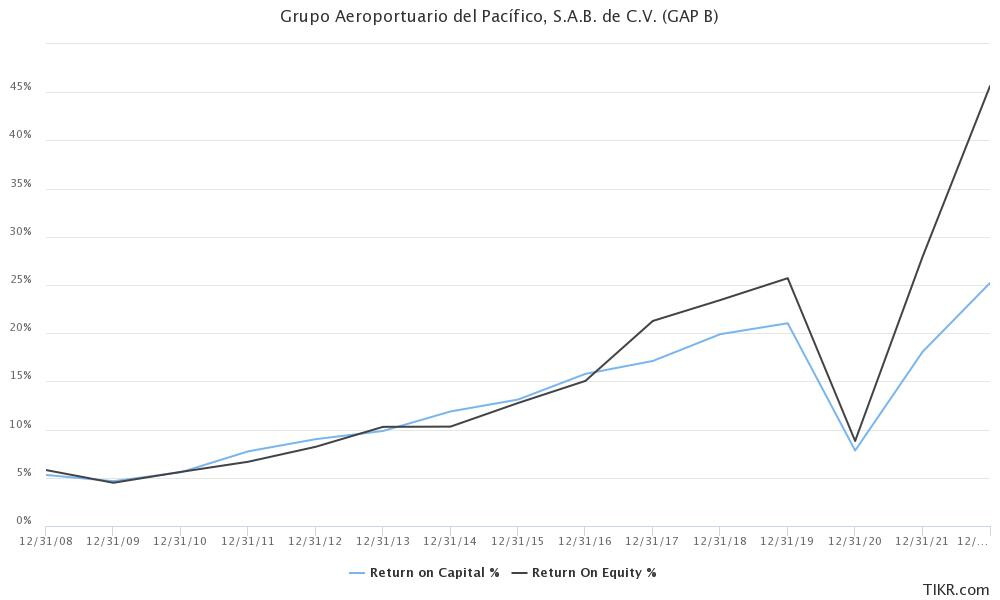

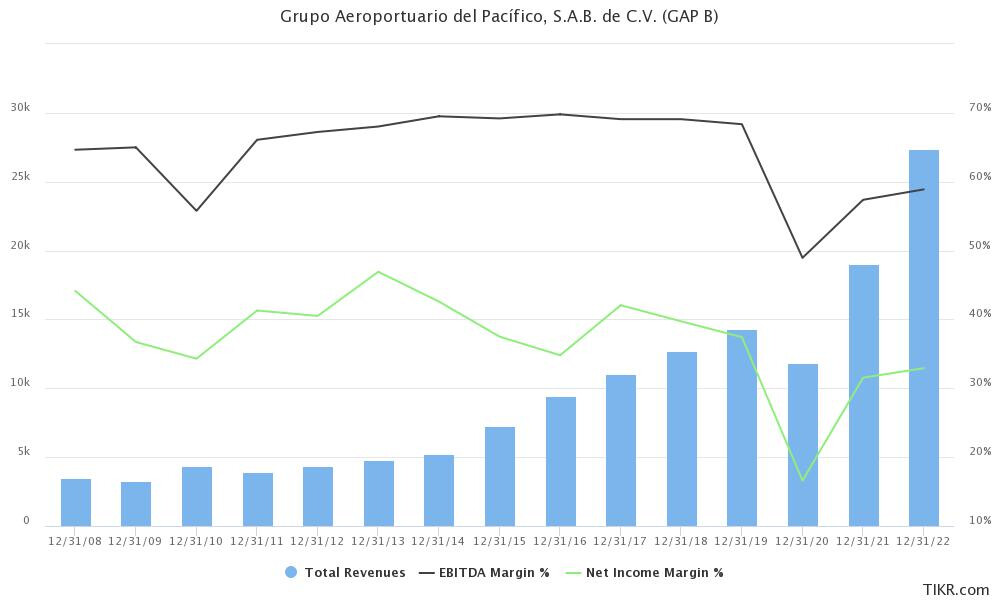

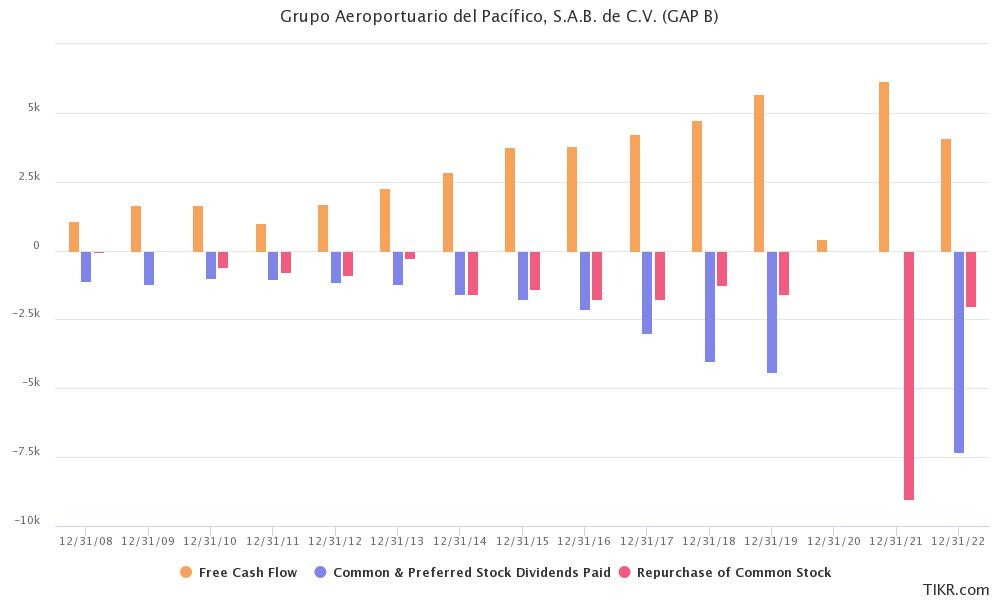

Added 2% position size in Grupo Aeroportr dl Pcfco SAB de CV. They operate multiple airports in Mexico and have grown tremendously in past few year. I will let the pictures summarize their growth story.

In terms of valuations, they are trading at lower end of their EV/EBITDA range, at 14x PE and 5%+ dividend yield, which I find quite reasonable for their growth profile. Its also a great way to play the Mexican growth story.

Reduced position size in Vanguard emerging market ETF (from 10% to 5%), Swiss market ETF (from 5% to 2%), and in VF Corp (from 2% to 1%). I am reducing position sizes in ETF as I feel buying shares in cos can give much higher returns. Drop in VF Corp position is due to drop in stock price, its been in a crazy fall since the last year!

Updated cash is around 8% and I am looking to deploy this soon.

Yes, I am happy they have stopped investing in loss making ventures like hotstar. It’s because of these kind of investments that their return metrics have been so low over years.

It’s quite cheap, they have an ongoing diesel pollution probe, but it’s very small considering their networth. A longer term worry is around integration issues, merging a US co with European co is very challenging as both have very different management styles. Maybe this is why co is trading so cheap.

Hi Harsh,

I have been a silent appraiser of your contribution to this forum and have been learning a lot from the conversations. I am currently a student in Germany and trying to invest after the learnings I gain. I wanted to know how you sit tight on your bets like Inmode, VFcorp, BAT since they have such uncertainty at the moment. I listened to one of the interviews with VFcorp CEO after their numbers and seems like it would take a long time to fix “the not-so-good things”. Is it good to exit such stocks for the time being and free the cash and look for opportunities elsewhere or sit back/average at such a valuation?