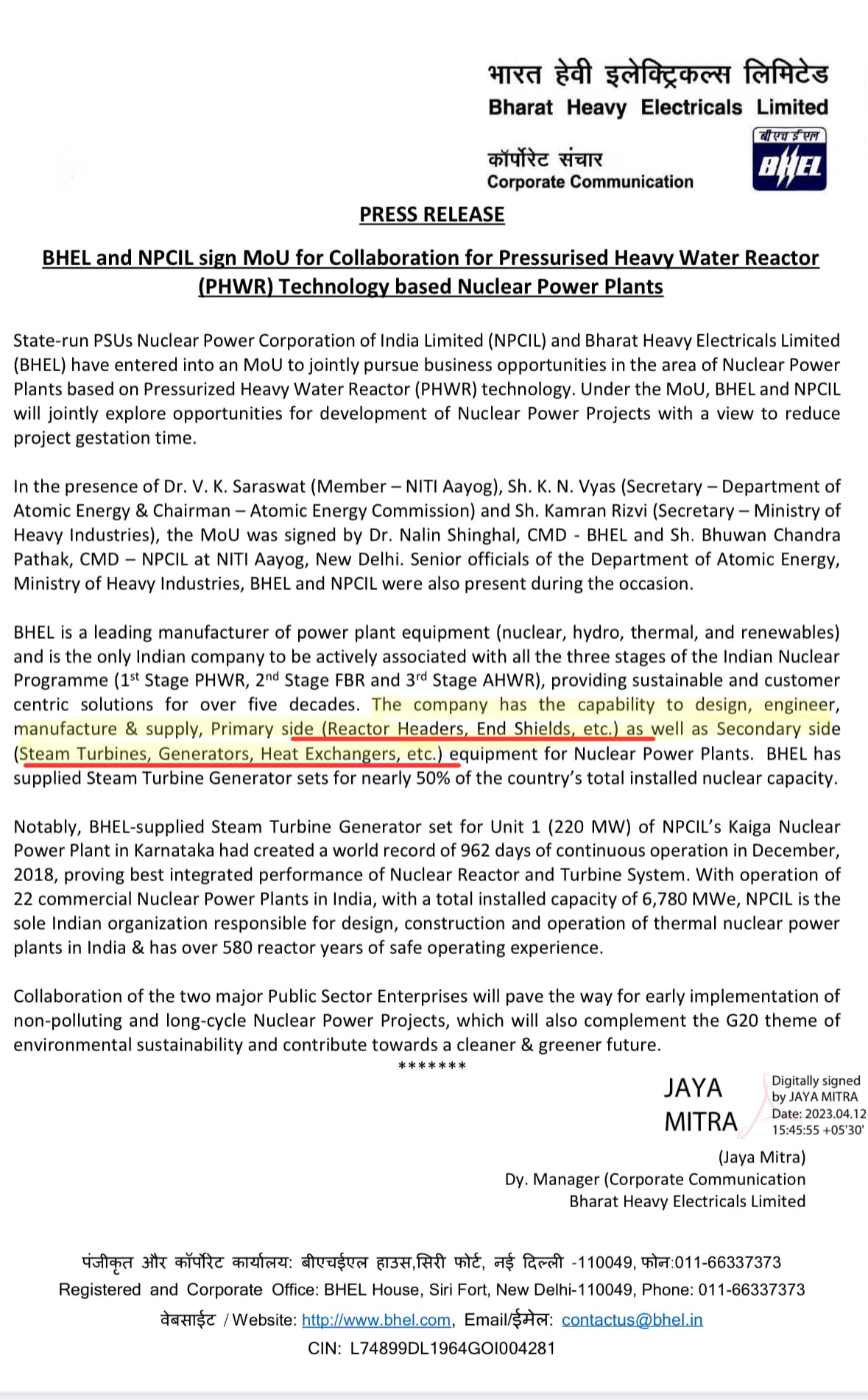

Wonder if Anup can extract some business opportunities in this space for their reactor, and heat exchanger offerings, especially now with their clean room Capex done as well.

3 Likes

Anyone having summary of concall?

• Kheda facility is ready and commercial production to start by Aug 2023. FY24 revenue expected from Kheda is around 60 cr. and to reach 150 cr. by FY25. Capex in FY23 is 75 cr and another 45 cr. in FY 24 for this facility. Phase 2 plan to be announced in next financial year.

• Orderbook by end of March 2023 is 530 cr. and they have got additional 150 cr. worth orders in FY24 so far.

• Expect 30% revenue growth at 22% margin. Upcoming Q1 & Q2 might have lower margins due to past high raw material cost, but Q3 & Q4 to be higher with yearly margin at 22+.

• Current export at 19%, & they are targeting 30% in FY24 and 40% in FY25.

• Targeting 1000cr revenue by FY27 & need to start on more complex & proprietary products, likes of duplex, stainless steel instead of carbon steel. They are already doing some of these and the new facility should help. There was also a mention of Titanium based product enquiries but they are yet to get an order on this.

• They are in the top 4 among competition, but they didn’t name names.

• Oil & Gas are predominant customers, with Pharma & Spec. chem picking up. Clean room availability should aid them moving forward with these industries.

Please correct me if there are any mistakes, thanks.

5 Likes

Some important pointers to note:

- Management did mention a few times, trying to increase revenue/sqm. Kheda facility(land) is ~ 3.5-4x the size of Odhav.

- Nickle prices is the RM to track for Anup.

- Green Ammonia and Green hydrogen can take over a share of the pie once oil and gas capex starts tapering.

- Need to figure if they have a role to place in nuclear energy space

- No mention yesterday of ISRO order for their clean room

2 Likes

1 Like

Strong order book of ₹658 crore as on May 31, 2023. It was ₹530 crore as on March 31,2023.

Highlights from june 2023 investor presentation

• Strong Order book (651 cr)and Enquiry pipeline.

• Targeting strong execution with focus on consistent performance and reducing the skewness of volume between the quarters.

• 1st dispatch from Kheda plant is expected in Q2 FY24

Disc…invested

4 Likes

Anup engineering update(from credit rating 2023 and concall and investor presentation)

ANUP ENG

1…Performance(2020-2023)

Revenue growth@18% cagr

Operating growth@6% cagr

Pat@14% cagr

2…Future growth

A…Kheda plant

=Phase 1

…Anup has developed and implemented the first Phase – I (comprises of 2 bay) of the projects, with an aggregate cost of around ₹120 crore

…1st dispatch from Kheda plant is expected in Q2 FY24.

=Phase 2 and phase 3

…The company plans to develop and implement Phase – II & III of the project comprises of another 6 bays with an investment outlay of around Rs.150 crore. As informed by the management, Phase-II and phase-III of the project is expected

to be commissioned by June 2024 and September 2025 respectivel

=Capacity constraint at its existing manufacturing facility (inability to handle equipment with weight more than 200 tons) ha d restricted its

scale of operations in the past. However, with commencement of new manufacturing facility at Kheda, near Ahmedabad, Anup expects to grow its scale of operation as it can now handle large size equipment and export orders more efficiently.

B…Order books

=Strong order book of ₹658 crore as on May 31, 2023, which is at all-time high for the company.

3…Quality

=The products of Anup are approved by all the major third-party inspection agencies and consultants like Engineers India Ltd. (EIL), Jacob H&G Ltd., ThyssenKrupp Industrial Solutions (India) Private Limited, Project Development India Ltd. etc.

=Further, Anup has also acquired “U”, “U2”, “S” & “R” stamp

authorization certifications issued by American Society of Mechanical Engineers (ASME) to penetrate export market (ASME product

certification mark complies with the laws and regulations of nearly 100 countries as a means of meeting their government safety

regulations).

4…Healthy profitability and return indicators:

= During FY23, Anup’s PBILDT margin declined by 415 bps on a y-o-y basis to 20.42% which has remained largely on the envisaged level. The decline in margin during FY23 was largely on account of elevated commodity prices which witnessed quick and sharp volatility during the year.

=However, with stabilization of commodity prices along with growth in scale of operation, the PBILDT margin is expected to improve to around 21-22% during FY24-FY26.

=Anup also has strict control over its overheads coupled with efficient management of order book and product mix. Moreover, Anup’s

technical expertise and specialized products like ‘Helixchanger’ and ‘Embaffle Heat Exchangers’ offer significant benefits over

conventional heat exchangers which is expected to support its profitability.

=Anup’s return on capital employed i.e., ROCE stood healthy at around 16.29% during FY23 (around 16.67% during FY22). ROCE is expected to remain healthy in the range of 17-

19% for FY24-FY26.

5…Anup receives interest free advances from its customers which keeps Anup’s external fund -based borrowing requirement low.

6…Market Focus:

=The company is focusing on consolidating its position in the market for centrifuge products.

=The company is exploring the possibility of entering the air cooled heat exchanger market.

7…Customer Acquisition:

=The company has gained three new customers: Graham, Indorama, and ITT.

8…Replacement market

Good replacement market as the average age of the company’s equipment is 15-25 years.

9…Future Growth:

=The company expects to maintain a growth rate of 25-30% for the next three years

Disc…invested

8 Likes

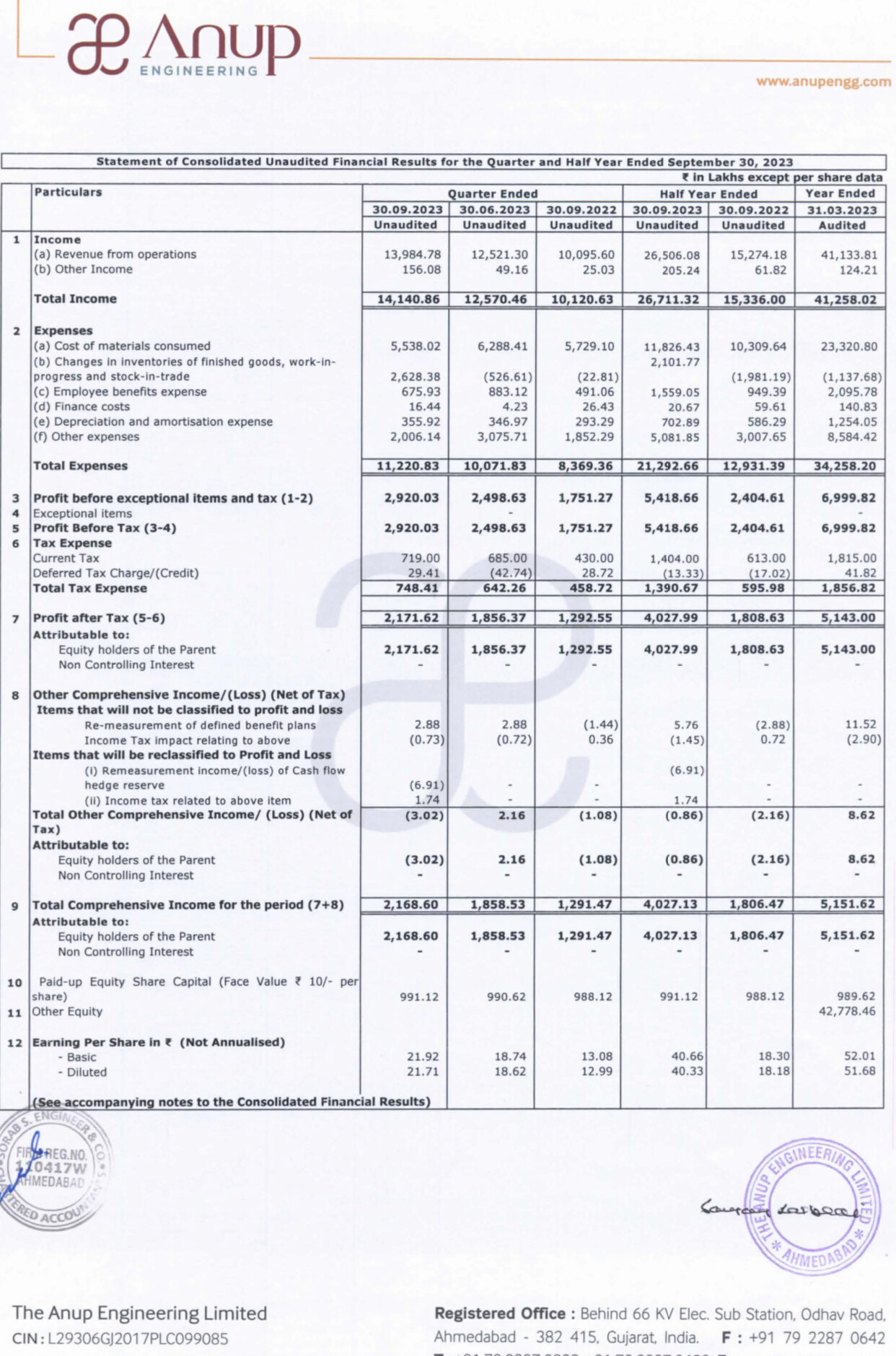

Had attended the Q2FY24 con call and would like to share the highlights:

On Q2FY24 Numbers:

- GP was lower due to the higher contribution of complex equipment and higher metallurgy products. As we move forward into more complex products. GP margins are going to fall but absolute EBITDA will be higher.

- Other expenses were lower due to a lower portion of royalty-based revenue. A broad range of other expenses achieved in Q2FY24 should be taken for the rest of the year.

Revenue & OB:

- Won over 365cr + 243cr (October) of new OB in this FY24 till date. So, as of today, the total OB is 873cr. It is the best we ever had. Out of this OB, 590cr. to be executed in FY25 and still counting. (Meaning H2FY24 potential revenue stands at 280+ cr.)

- Revenue growth of 25-30% with EBITDA 20%+ guidance remains for the next 2-3 years despite higher complex product contribution.

- We should touch export revenue of 30% in FY24 and are already at a 50:50 mix between export and domestic as guided for FY25.

Kheda & It’s CAPEX:

- Started first order in Q2 from Kheda. Happy to state that, already won >100Cr. of OB for the Kheda Plant and hence this facility will be well utilized.

- Looking at OB winning, planned to increase 0.5 bay capacity with an investment of 15cr. This will take us to a total of 2 operational bays by Q1FY25.

Conclusion:

Looking at the pace at which OB booking is happening, the early addition of 0.5 bay than expected, a higher proportion of less competitive export OB, increase in complex equipment - all this indicates a lot of improvement compared to what Anup was a couple of years ago. Mr. D’souza is very clear in communication about driving factors of Revenue, Expenses, and Margins as well. At this pace and very comfortable potential FY25 revenue based on the current OB in hand, gives a lot of comfort to keep holding this stock. Although I have no comment on valuation but I will continue to keep this stock till the time numbers speak.

Discl: Invested.

Regards,

Mukul Jain

12 Likes

If I look at the valuations -

Let’s assume they sustain with the same PAT -

June 23 - 19cr

Sep 23 - 22cr

Jan 24 - 22cr

March 24 - 22cr

Forward P/E FY 24 = 2532/85 = 29.7

EPS for June 23 = 18.74

EPS for Sep 23 = 21.91

EPS for Jan 24 = 21.91

EPS for March 24 = 21.91

FY 24 EPS = 84.47

SharePrice = 29.7X84.47 = 2508

Note: The calculation above is grounded in assumptions. The concept here leans towards probabilistic correctness rather than precision.

Is there any fundamental update that led to the recent 12% share price fall in 1 day? I went through the concall but did not notice any major issue

I perceive no alterations in the fundamentals. In my view, the reasons for the observed correction might be as follows:

-

The Q3-24 revenue witnessed a decline of around 8% compared to Q2-24. Nevertheless, the management explained that a client supplied raw materials for a project, resulting in a 12Cr reduction in raw material costs and subsequently impacting the top line.

-

There appears to be a general trend of selling or profit booking in mid & small-cap stocks.

I hope that helps.

Disclosure - Invested at lower levels

3 Likes

Acquisition , 0.7x sales

1 Like

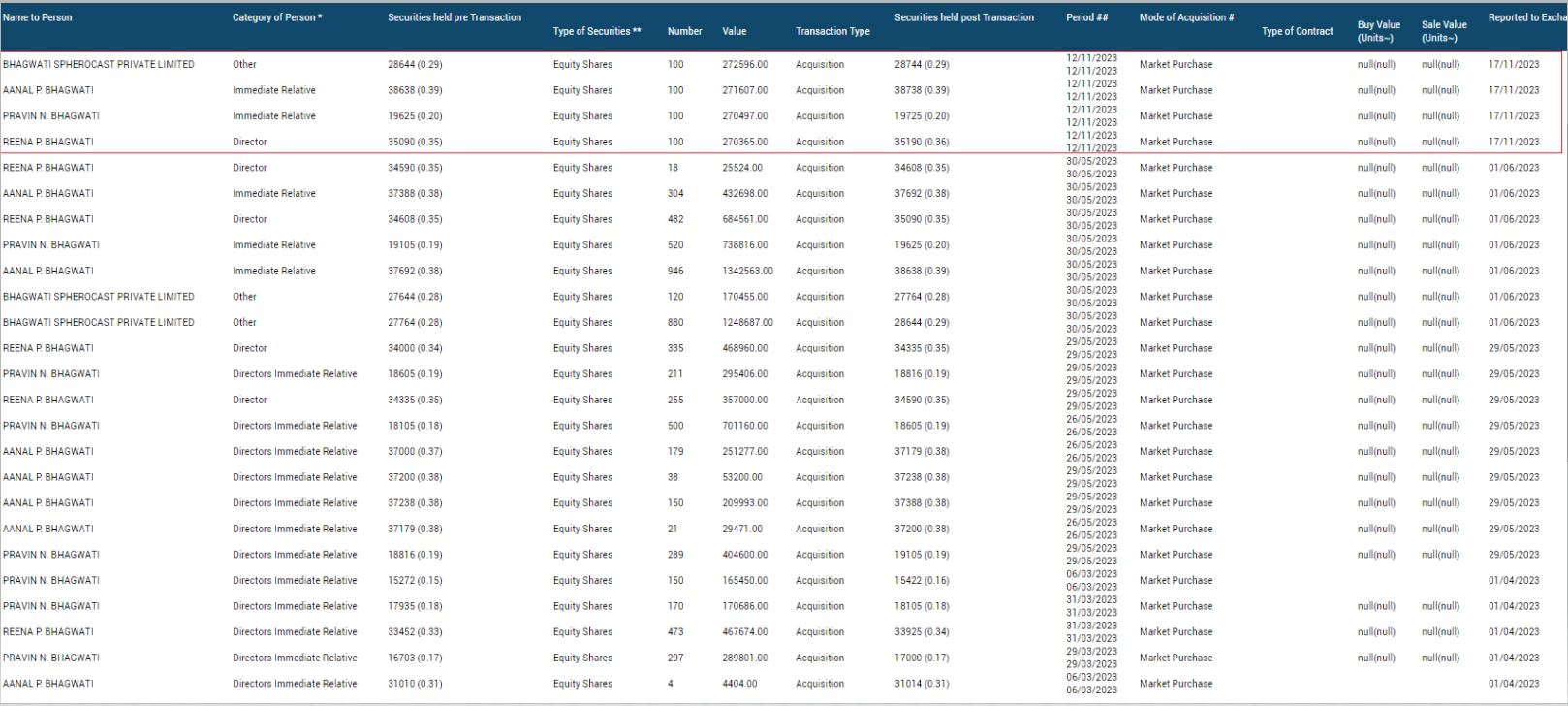

Bonus announcement

1 Like