even for that you need heat exchanger.

agreed. And my point was that the economics in the long run work out compared to the initial technical complexity and capital intensive work.

Take a look at Renewables. It fails every metric in terms of efficiency and TCO, still people do it. Solar’s best efficency is 21% ± 4% under lab conditions, real field level is at 11-13%. Ditto ethanol blending. you dont have to know chemistry to know how badly inefficient is ethanol blending but still ESG stuff because it’s not oil/gas. Lets just handwave that the fertilizer and pesticide are not from oil and it’s not a good convertor of it to sugar and alcohol. Charlie Munger gave a good talk on this in 2010 I think.

So, you’re right on these things being complicated but some are worth doing in some cases.

1 Like

Anup eng concall Q2-2022/2023

1…vision

=Number one, we need to diversify in different geographies and product categories. Mainly, I talk about exotic metallurgy. So it will give a higher value for our equipment and product mix for us.

=Second is acquiring technology of proprietary products.

=Third, expanding the capacities and capabilities. So Kheda is a clear example of how we are going to increase our capacity and capability because of the sheer size of that facility. As you all know, it spreads under the hook 17 meters, which gives us a huge leverage in terms of getting more into a heavier, complex, and larger diameter equipments.

2…Growth

=With the addition of Kheda, along with our existing facility, which as we said should be commissioned by Q4, we expect that we should be able to grow at a CAGR of over 25% for the next 3 years.

3…Kheda

=the first phase will be getting commissioned by the end of the quarter 4 FY '23

=The complete first phase will be operational, which includes 1 full bay and half a bay. The full bay is used for the assembly, and the cutting and bending will happen in the half bay.

=Kheda, the sheer size of the plant, that is 17 meters under the hook and 25 meters wide, 200 meters long, that itself signifies the aspirations that we have when we set up this plant

=Next year, towards the end of the year is when Kheda will start delivering on its full capacity.

= we commission Kheda and concentrate more on exports

=The third phase, we are expecting to complete by FY '26.

=Kheda FSI is much higher than what all the 3 plants put together is.

=Total 5 bays in three phases upto 2026

=We can expand upto 7 bays

4…Diversification

=Going forward, with Kheda in place, that’s the change that we want to bring about. We want to keep heat exchangers to about 60%, and the balance is where we want to increase vessels ,reactors so that we do justice to the capabilities that we’ve built up at Kheda location.

5…Key strengths

=I think 3 strengths we’ve historically had as Anup. I think our competitiveness, our on-time delivery, and our quality.

=We’ve hardly had a quality complaint for the last 5 years.

= I don’t think we’ve ever missed a customer CDD. So I think preserving this is going to be key to looking to the future

6…Margin

=Margins are going to be back to the previous levels. This was due to a very extraordinary situation that the industry hasn’t seen, in at least my memory, where overnight, because of the war situation, prices of metals, sod, and especially in certain categories like nickel-based alloys, it went up by almost 200%

=I think we are going to aspire for that 24% kind of margin on a 25% annualized CAGR growth

=So there are 2 types of customers. One is tender business, where, unfortunately, the industry is structured in such a way that there is very little opportunity. Once you bid and you are L1, you only have a choice of accepting the order or rejecting it, right? Then there is very little actually price escalation built in. But that usually doesn’t matter because the window between becoming L1 and actually getting the PO is not inordinately long. So only a massive spike in a very short period of time can result in something like this. If you look at Anup’s history, we have not faced something like this in the past. And even the world hasn’t faced something like this in the past. That said, we tried our very best to go back to customers and request. But contractually, a lot of those provisions don’t exist. And when they don’t exist, your negotiating power is low. That said, we managed to get some marginal increases here and there

6…Capex loan

=The requirement for funding the working capital and CapEx would be close to around INR 20 crores to INR 25 crores. And we will be taking debt for it.

7…odhav

=Odhav facility is constrained from its location perspective also. It’s landlocked, and the space is very limited. So a lot of the export customers that require large equipment, et cetera, would not even consider this manufacturing location. So we have not gone to that set of customers also, which we know that if they come and see the facility, they will have the first question around logistics and that will be, before they even look at our systems, processes, and shop floor, it would become a constraint.

=So these are the issues of why we have sort of focused on this set of customers, which itself is giving us good bottom line. I think the right question to ask is what will happen after Kheda? And there, I can assure you that any export customer will love the infrastructure that we are putting in place. It’s going to be a best-in-class kind of infrastructure.

8…Export

Q=Is there a lead time there, sir, because what I understand, especially in your industry, with the export customers, you have a lead time to qualify for taking orders, and it pans out in 2 to 3 years, even then…

.

Answer=

Yes, but there is also existing – so we do have export customers already. We are qualified for a lot of export customers. And those customers can start utilizing the Kheda facility. So while new customers will send their people, they’ll do their inspections, they’ll get confident about our capability to deliver and then place orders, there are people that already trust us, where we have a 100% track record already. So those people will be quicker to place orders. And part of the INR 536 crores that we already have, there are some orders specifically taken for Kheda, which will start up in Q1. And we don’t want Kheda to ramp up beyond a certain pace, because we want to be able to digest the orders that we get and continue our promise of 100% on-time delivery.

9…Capacity utilization

=Capacity is a moving target because average equipment value is also changing all the time, right? So the same number of equipment can deliver a higher turnover if your average equipment value goes up, and it’s been constantly going up every year. So we are close to full right now, but we will continue to remain close to full with a higher turnover because our average equipment value is going up. Because equipments are all different, at different points in time, different equipment will take up different area under the crane. So it’s not as – when you think of an engineering bay, you’ve got to think of time under the crane, which is almost 100% right now. And it will be 100%, but deliver a much larger turnover going forward because of the quality of orders that we have already won.

So that’s how you should think about capacity.

=I think the additional stuff that will add to this is the clean room at Odhav.

=And if we are aiming to start with a INR 500 crore plus opening order balance next year, a big chunk of that will have to be done out of Odhav because there will be a ramp-up that we will see at Kheda. So only towards quarter 3, quarter 4, will we start seeing good levels of utilization, because we’ll have to get the qualifications, we’ll have to get the customers in, we’ll have to sort of get all the approvals in place for various different types of equipment. So that all will take some time. So next year, towards the end of the year is when Kheda will start delivering on its full capacity.

10…Revenue guidance

=Odhav would be to the tune of INR 500 crores. And beyond that is where Kheda will chip in. And in the first year, we are looking at INR 75 crores to INR 100 crores turnover from Kheda with the 1.5 bay commissioning that’s going to happen in Q4

=Both will contribute to revenue from 2024

Disc…invested

My latest portfolio

5 Likes

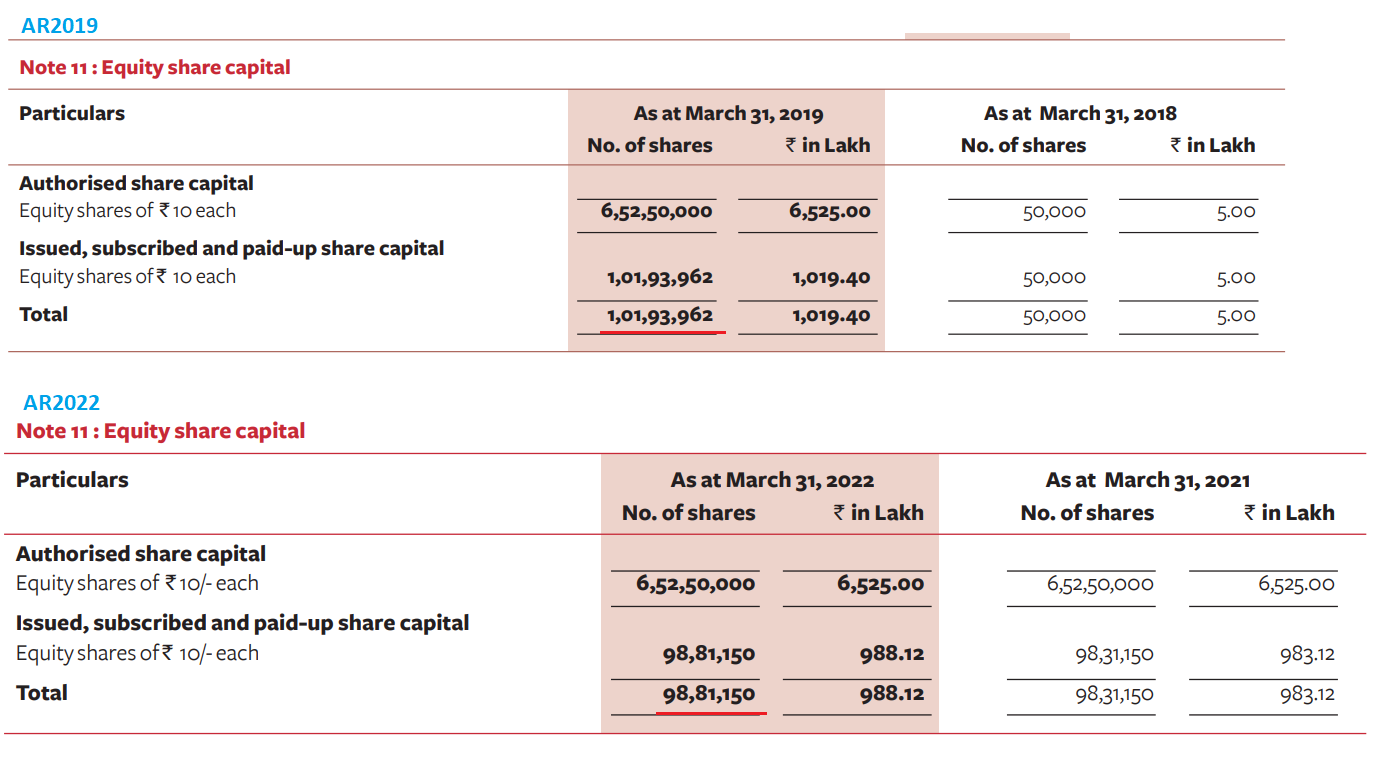

Sir can you explain what the red flag is exactly? On 26th Oct 2018 Arvind Ltd demerged its branded apparel (Arvind fashion) and engineering (Anup engineering) arms what this NCLT order is about. In 2019 Anup Eng allotted 10193962 shares to equity shareholders which now stand at 9881150 shares, thanks the to buyback + share option exercised during the period.

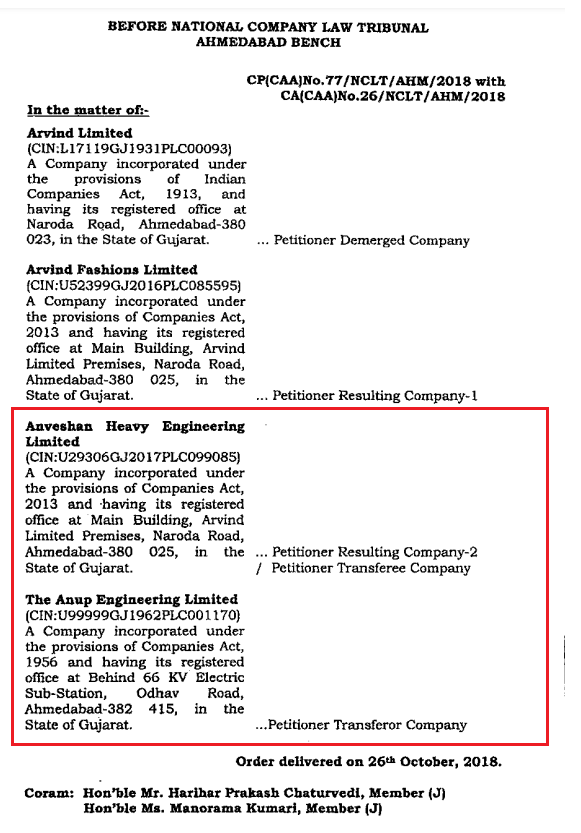

Regarding 1.92 cr expense adjusted against security premium, note that engineering arm was demerged into Anveshan, then Anup & Anveshan were merged and finally Anup was listed as a separate entity. Here is the proposed structure :

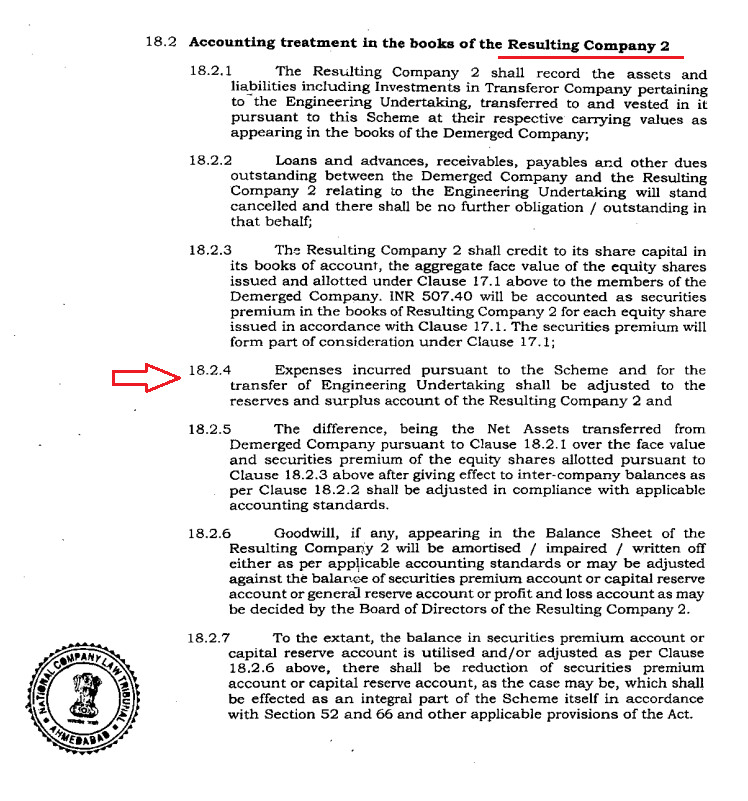

Here is the NCLT guideline for expenses incurred during the transfer of engineering undertaking:

If I am missing something, do let me know.

Regards

3 Likes

my intent is HOW this benefit retail investors . this is an accounting sharp practice which doesn’t add any value … If you think it help in retail investors could you please explain your point of view … we must not seek supporting evidence to reinforce our faith or rational of investment it is more of confirmation bias i may be wrong but this kind of sharp practice should not be taken as a positive

I am actually open to disconfirming evidence. Numbers you’ve highlighted in your post are : shares issued by the company and expenses adjusted against security premium. What’s the red flag here? If there is more to it, I am happy to hear it. Thanks

7 Likes

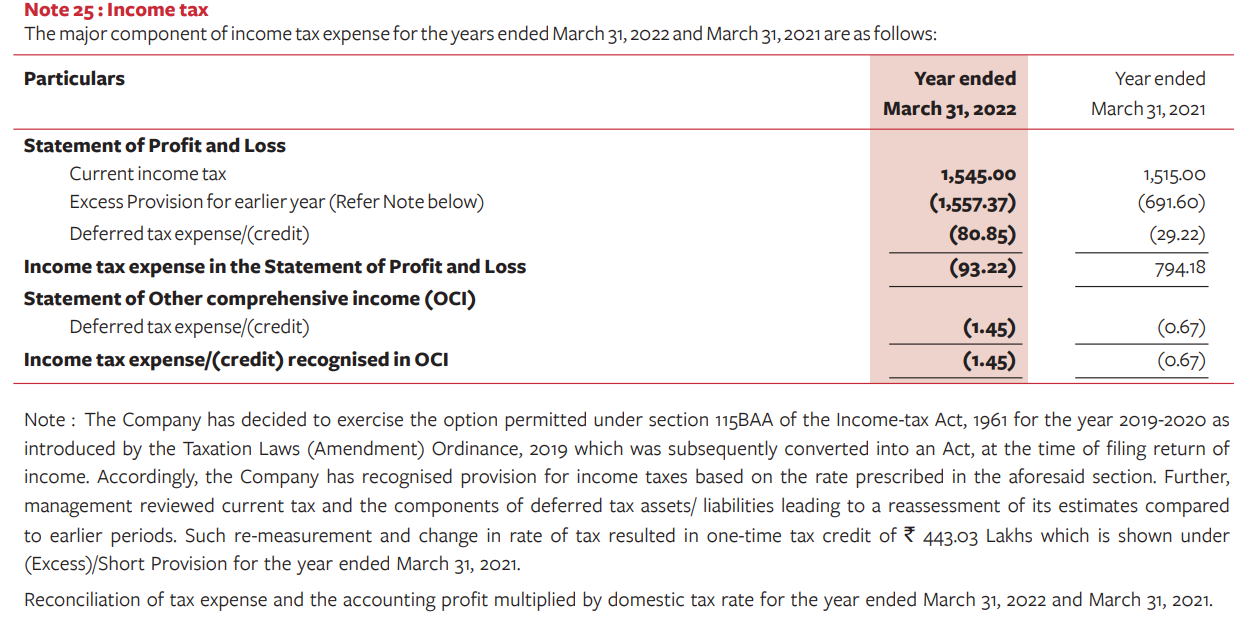

Hey Everyone - Recently started tracking this co. Every year once it is getting certain tax benefits.

Any idea on this ?

2nd query is around margins. EBITDA % is around 20-25%, what the that thing that is helping them sustain higher margins. It must be natural for customers to negotiate with them seeing 20-25% margins they are making

Thanks in advance

They have technology from Lummus Netherland to make high quality equipments

1 Like

Company opted for section 115BAA of IT act which is applicable from year 2019-20. This section allows domestic companies to pay income tax at 22% (+surcharge & cess). Excess provisions & deferred tax credit is adjusted here.

3 Likes

Any Idea, why no con-call post 3Q results?

They do con calls twice a year

2 Likes

Hello Experts,

I just need small help regarding Valuations. How to value a Capital Goods company? Is P/E ratio the right matrix or do we need to see some other multiple? Can someone please point out an article, video, or any reference to judge the ideal valuation a capital goods company should get?

With the increasing price of Anup, it is important for us to find the right valuation to help us decide whether to hold or exit.

Thanks in advance,

Disc: Holding Small %

1 Like

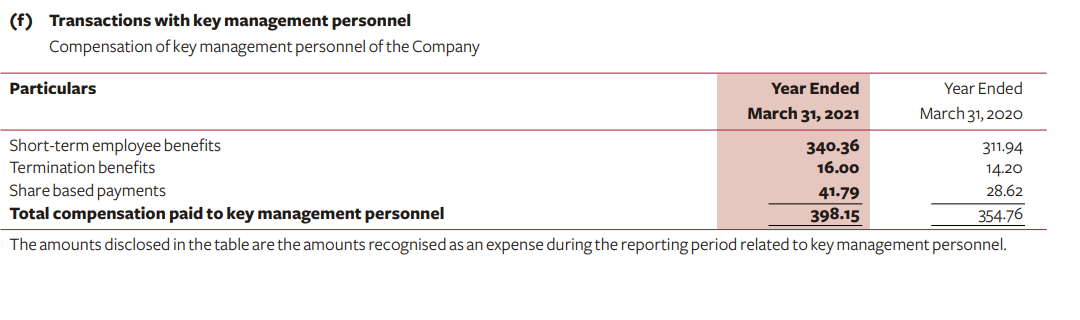

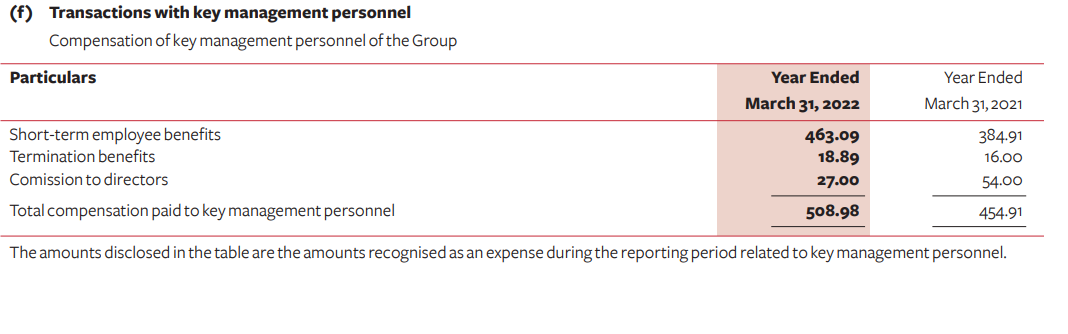

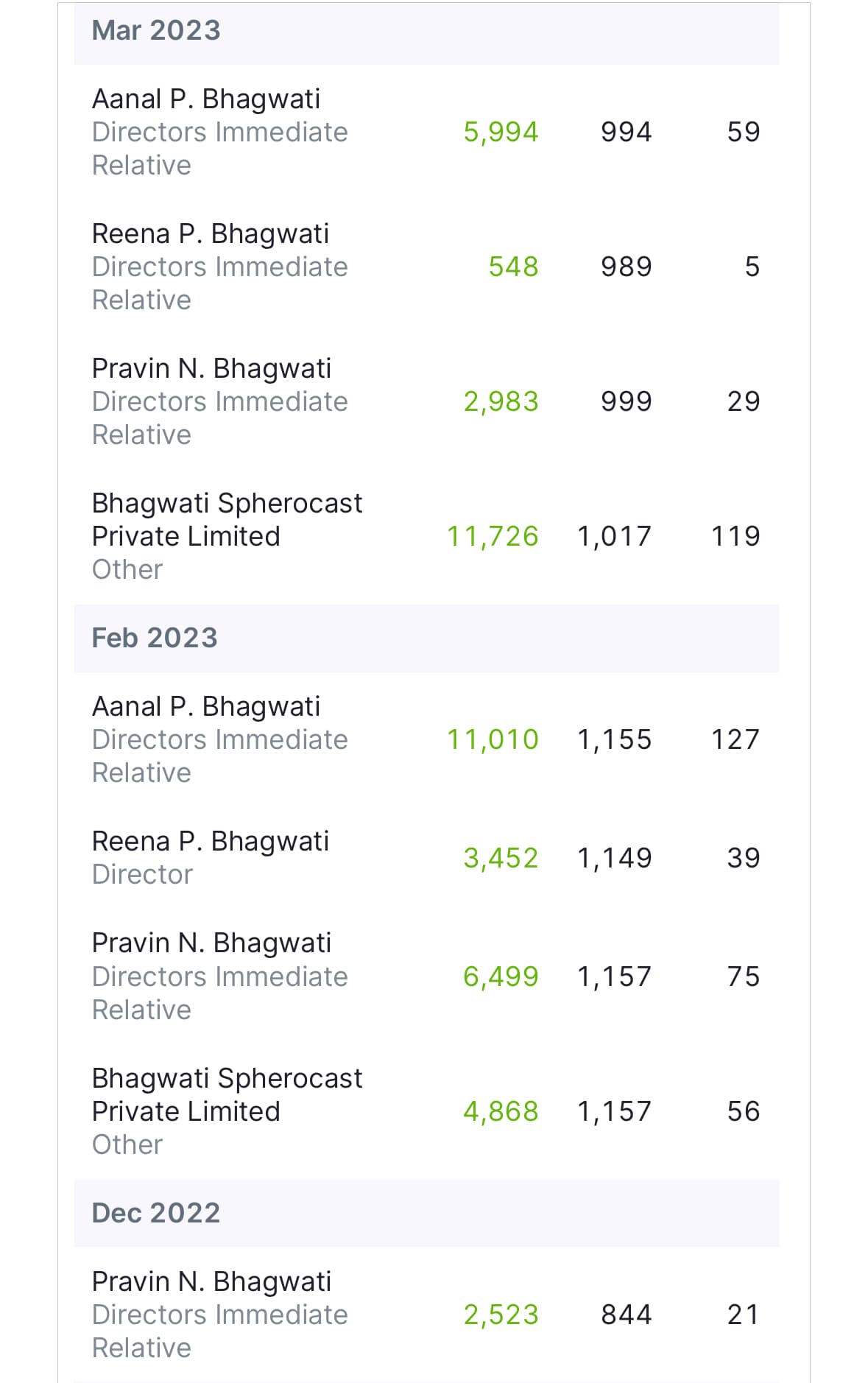

I took these screen shots from Annual Reports(both are consolidated) , compensation for 2021 is not match from 2021 annual report & 2022 annual report.

Is is Corporate Governance issue ?

1 Like

Wonder if Anup can extract some business opportunities in this space for their reactor, and heat exchanger offerings, especially now with their clean room Capex done as well.

3 Likes

Anyone having summary of concall?