Blockbuster set of results from Anup

Order book - Rs 854 Crores

EBIDTA of Rs 37 Crores, growth of 24%

Margin at 23.7% vs 20.9%

Net Profit of Rs 43 Crore, growth of 121%

Blockbuster set of results from Anup

Order book - Rs 854 Crores

EBIDTA of Rs 37 Crores, growth of 24%

Margin at 23.7% vs 20.9%

Net Profit of Rs 43 Crore, growth of 121%

Order book is 875 cr against annual turnover of 550 odd Cr

New acquisition and Kheda completion should add to capacity

I think orders are not a problem, capacity constraints may be.

Had attended Q4FY24 con call, would like to share higlights along with my comments:

Revenue & OB:

CAPEX and Growth Initiatives:

Other Important KTA:

Note: Have highlighted only the points which I think are important. Might have missed some of the remarks made by management.

My Take:

I am pretty happy with way company guided on exports. There will be better WC efficiency as 30-40% will be advances. There is possibility to achive >20% EBITDA on exports. Hence, with Mable, it looks 35% revenue growth is within reach for FY25. And, on top the quality of earning is a big plus as the cash conversion is prestine.

Discl: Invested.

Regards,

Mukul Jain

This has been a good special situation aka demerger to be invested in.

I think Arvind group is preparing for another suc opportunity.

Another such opportunity?

Which one? Envisol?

Advanced Materials Division which is being separated into WOS…

Q1FY25 Concall Summary

Business Updates

Participants

Abakkus Asset Managers

Samasa Capital

Shubh Labh Research

QnA

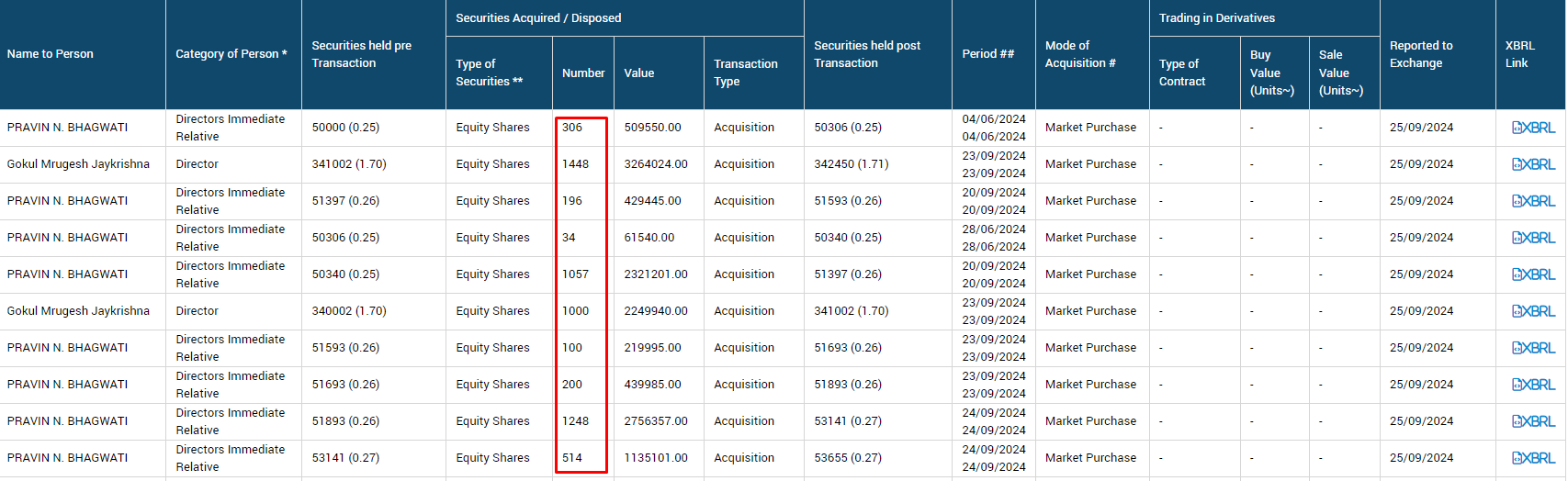

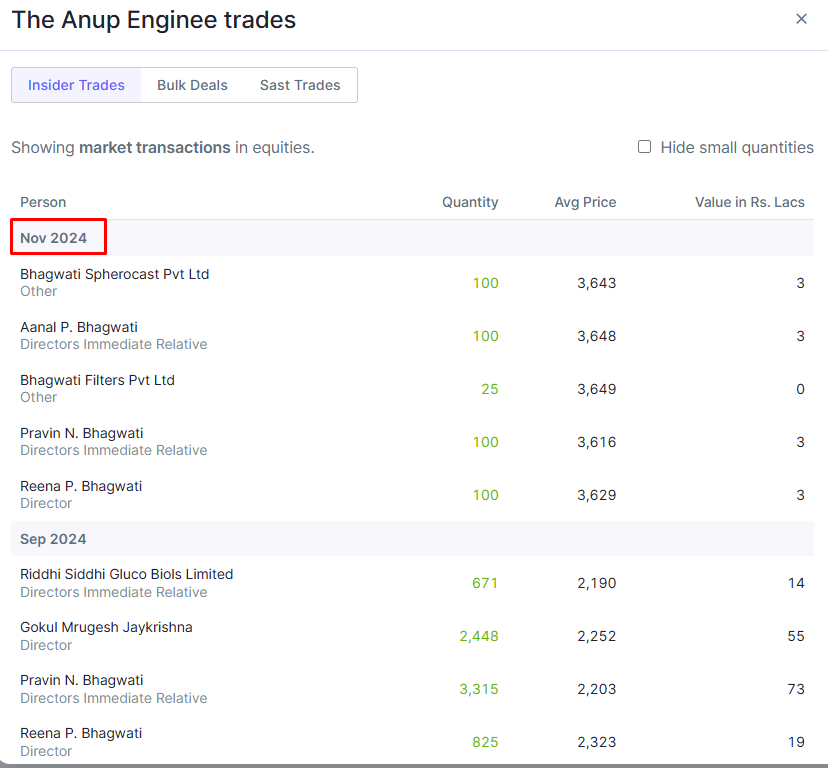

Just wondering will this not be called insider trading? like relatives buying just before the results?

Hi, Which platform can one see these transactions on ? Excuse me I am new to this and learning. Thank you.

Rupeevest, Morningstar, Trendlyne

Did anyone attend concall?

Q3FY25 Concall Summary:

Performance:

Sector-wise Q3 FY25:

Hydrogen Business Contribution

Product-wise Q3 FY25:

Geographical Revenue (9M FY25, revised):

Mabel Engineers Performance

Gross Margin Expansion Drivers

Capacity Expansion at Kheda:

Revenue Potential: Current Manufacturing Capabilities: Ahmedabad, Kheda, Tamil Nadu together can support ₹1,000 crore revenue

Post-expansion (including the ongoing construction), capacity will increase to ₹1,200 crore.

Kheda Plant Expansion & Revenue Potential

FY25 Outlook:

FY26 Growth Guidance:

Export Order Intake Run-Rate: Expected ₹110-115 crore export orders per quarter

Revenue growth of 25-30%

EBITDA margin over 20%

EBITDA margin guidance at 20%+ vs. 23%+ in FY25, with a conservative approach prioritizing growth.

Exports to remain 50-55% of total revenue.

Strong export inquiries, domestic market sluggish but improving.

Indian PLC (Petrochemical & Refining) projects yet to materialize; expected in 6–8 months

Global projects delayed due to geopolitics, policy uncertainties.

Hydrogen, gas, and energy transition projects remain key global opportunities.

Inquiry pipeline of ₹900 crore, with 70% from exports.

Strong demand from hydrogen (U.S., Canada, Europe) and gas projects (Middle East).

Domestic growth led by petrochemical projects (Reliance, Adani) and upcoming PSU refinery/petrochemical projects.

Miscellaneous:

Fixed-Term Contracts & Raw Material Price Volatility

Capacity Utilization: Current overall capacity utilization is approximately 70-75%.

Seasonality Impact on Quarterly Performance

Management is exploring more long-term manufacturing partnerships like Graham. Such tie-ups ensure stable order inflows rather than competing for each order.

Reason for low tax rate: lower tax rate due to some tax reversals of last year and ESOPs being exercised by a few members.

Net Debt-Free: The company remains net debt-free.

Hi there folks, just wanted to know if there is any impact or potential challenges of Trump tariff scenario on this company? Last 3-4 days the price action seem to be not that great which may indicate that there’s some fear. Thanks

ANUP’s export revenue was 46% in the last quarter and the company is targeting to achieve 50% by year-end. Of course, there is likely to be some impact due to the ongoing tariff issues, as they also supply to the United States. If an investor has a long-term perspective on this company, they should not worry about daily, weekly, or even monthly price movements. One should only buy if they believe the stock is at a cheaper valuation and closely track the business performance. Don’t worry about price movements as long as you feel that the growth story remains intact.

Disc - Invested at lower levels