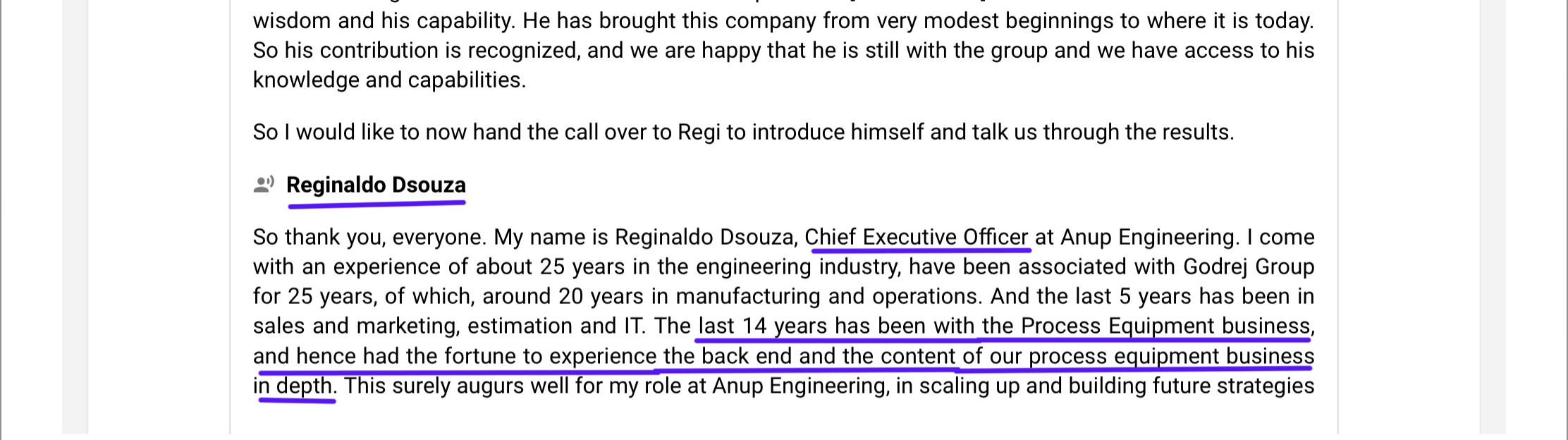

Anup engineering - concall -july 2021

1…Order book

=Since the 1st of April since the year opened, we have gone ahead and booked almost about 150 crores already. So, which is you can say one of the best run rate that we have had in terms of order booking.

=We are pretty much on track with the initial indications that we had given the expectations about booking orders to the tune of about 330cr

2…Clean room capex-Odhav

=We are certain that we will be able to complete the project in the month of September anywhere between 15th to 30th of September

= In the initial H2 we are likely to commission this by the end of H1 and H2 you will not see any impact there.

But yes, the following half that is the first half of next financial year, there’ll be an impact on revenue because we’ll be booking the orders at that time.

=In the second half maybe, we will be

utilizing the clean room as any other bay to begin with. So, we are not going to wait for the exotic metal orders but those orders will materialize in the second half of this financial year. So,

they will be executed in the first half of next year

3…kheda plant

=We intend to begin the first phase of construction in this quarter, in the current quarter in Q2.

= We are in the process of renewing our contracts and we plan to begin the construction at this time

without wasting any further days.

=Kheda, we are targeting Kheda to be the best fabrication facility as far as India is concerned.

=That’s how the aim that we have taken and it is definitely going to be equate with the best of equipment, best of planted machinery, best of way outs. To that extent I think definitely Kheda is going to be a benchmark in itself

=Ticket size of orders would also increase once the Kheda capacity is on scene

4…Sectors

A=Oil and gas(68%)

=The primarily the orderbook continues to be from our

conventional sectors which is refining downstream, oil and gas. But that’s maybe to the extent of about 68%.

B=Other sectors(32%)

=However, some very good progress we have been able to make, significant progress in other sectors, for example chemicals then we have been able to make good progress in power sector

=So the chemical sector contributes about 12% .Chemical sector is one of the sectors where we making inroads.

=Currently since we being more into heat exchanger right now is into more of refining but if you see, if we get

along our clean room from next quarter onwards, we will be more going sector having strigent corrosive application which consumes this exotic metallurgy.

=And also, we are looking at the product mix coming in from paper and pulp business which is also one big segment which we

are already present into, which we expand going forward.

=Also, then there are newer segments which will come up like Gas and everything which we are pursuing.

=The power sector is about 2%. Though it’s not really a very high proportion as of now but it’s a new

business stream, it’s a new revenue stream that has been opened up. We made some good breakthroughs with some of the global leaders in the sector.

=Of course, fertilizer will continue to

provide us with more opportunities, so happy to stay there that slowly we are making progress in other sectors other than the conventional refining sector.

=So almost about 32% is coming now

from non-refinery sectors. So that’s a great sign for us. And the momentum of the inquiries is I do not see any let-up in that. In fact, we are getting better choices because as we are going forward, we are improving our product mix.

=We are getting better approvals. We are getting our track record is becoming better than before and it is opening up doors for us on new product mix, new product categories, new customers. It’s pretty kind of expected market for us is going

to be quite positive in the future.

Q=Little disappointing that your orders are still just concentrated more than

two-thirds in Refining and Oil & Gas.

Ans=Absolutely agree with you. That’s something which has been driving us as well to venture out

into newer sectors and yes chemical sector does present a great opportunity to us and we are

gearing up to capture that opportunity. This clean room is going to be one of the factors we had more specifically

5…Ebita

=There could be a hit of a couple of percentage points instead of 25%-26% that we have been consistently showing on EBITDA, maybe it could

come down to what 23%-24% but that’s about it and we are confident of sustaining this.

=We are looking at the margins between 24% to 26% going forward

6…Replacement market

=The equipment which

are only installed there, they would need periodic replacements. So definitely shut down and

replacement is a major business segment for us.

=So our target customers would not just be the ones who are looking for a new expansion or new CAPEX but will also be existing plants where they need to enhance their efficiencies

7… Target of 1000 cr rev by 2025

=We had been talking about the key driver for this towards this target are going to be, the CAPEX that we are doing, the market expansion that we are doing, the technological

collaborations that we’re doing

=Kheda is one of the biggest building blocks for achieving

this number. That’s also one of the reasons why we would like to accelerate Kheda, especially

the first phase we want to really accelerate and get closer to our target as early as possible. We

are still expecting that in about FY25 is the target that we are taken for achieving our 1000 crores

number

=So, primarily what we have two units in our plan to achieve the 1000 crores revenue target.

A…Out of which 500 to 600 crores is going to be contributed by Odhav which is where we currently

operate from and which is currently actually the only functional facilities that we have. This contribution has come from Odhav

=Odhav should be delivering about the (+500) crores of revenue by FY24.

B…and the remaining is going to come from Kheda and that is

going to be divided into three phases.

=First phase as I mentioned is likely to begin by the end of this quarter and it should take about 6 to 7 months to be commissioned. That will add maybe

about 100-150 crores of revenue to the top line in the following period.

=Similarly, it is going to

be followed by two more phases of construction in Kheda.

=The completion of Kheda, the three

phases is going to happen one phase each year. The next phase is going to be planned in the next year and followed by the end of third year, the third phase.

8…Customer

Total number of customers maybe it will be close to about 70-75

=New customer addition has been muted in the last 12 to 16 months only because of COVID

9…Product mix

=Odhav facility we will continue to have similar kind of product mix between heat exchangers and other pressure vessels.

= But considering that our Kheda facility is going to be a

built heavy bay. We will be able to produce vessels, heavy vessels as well as long towers and reactors.

=So, per say with Kheda coming in on board, we will have this is this more balanced since Odhav is more suitable for us to produce more heat exchanger and that’s how we are chasing our order book

10…Technological upgradation

= As far as technological upgradation is concerned, we are continuing to have already two technical collaborations and we are continuing to pursue further to build up a more niche in our market offering

Disc…invested

My latest portfoloio