U shud not hv been in a hurry to sell Suven pharma which has highest margins n ROCE among all pharma stocks n CDMO opp size is huge n one shud hold such stocks for long long time

Do u find the laurus allocation to be on a higher side or r u comfortable with such big allocation. your rationale to invest are sage. do add a few lines of them

@vikas_sinha. Have been following your portfolio. Amazed at the speed with which you churn. I have been looking at Pokarna recently. Seems interesting given the upcoming new line starts generating revenues from next year. In absence of presentation, transcript, I am unable to get operating details of the company. Was wondering since it forms 18% of your portfolio what data points (asset turnover, sales strategy for new capacity, margins, incremental roic, etc) you referred to build conviction.

Thanks

Disc. Recently took a tracking position. 1.5% of portfolio in Pokarna

The PF is very pharma heavy, Suven looked priced-to-perfection with some downside-risk, looks like CRAMS is attracting increasing competition. Main reason was trying to concentrate into 8-9 stocks, some had to be let go. Thanks to you made good gains in Suven but was bit late in ramping up position size, and I saw risk in growing it further. It was either grow or let go!

Missed out on Route. definitely a huge network but tech-cycle risk is there. Am slowly getting over the FOMO pressure, there are plenty of decent opportunities and ambition should be moderated.

Gland I did not consider, given the heavy pharma concentration in PF. Found the IPO reviews were not so glowing but the share has done decently well. China-related risk was off putting also.

Laurus is a very capable company, they deserve higher valuations since they seem to effortlessly grow such high-value pharma biz consistently. I love the confidence to grow with leverage. This is a good quality compounder, with decent moat and hence maybe worth the extra risk of concentration.

I have not made the effort to do bottom-up analysis to generate investment ideas but am still chasing the riskier class of stocks. Some catch the wandering eye and some later turn out to be not so well made decisions. One belief is the pharma uptick has just started and good business can happen here for the medium to long term (3 year+). So I am content with collecting some good quality compounders such as Laurus, Granules, Solara.

Pokarna is the market and tech leader for Quartz and the product is decent, may have a good domestic market, but current concentration is on US market. It has faced a really bad few quarters, and things can look up with added capacity coming online next quarters. I think EPS can be 7-8x easily from here and it is a stable business, since sourcing is mostly in-house stone and petro-chems based (which will be on constant decline, reason Reliance tried to sell main biz but could not and is now selling everything else). The demand scenario seems is healthy. Promoters are decent but have stopped sharing info, maybe they change and come back to the previous habits with the upturn. A 10+ long-term PE is a decent bet here.

Hi Vikas, was going through you thread…it is inspirational and nice to see your transformation… Regarding pokarna they are increasing capacity by 130% right?.. Will it increase eps drastically? …do you think opm will increase once new plant starts operating?

I am extrapolating the sales/PAT from the few good quarters they had in 2019, when everything was going good due to huge Chinese ADD, and adding the expansion on top. (considering quartz capacity contributes ~70% of their total product capacity). Maybe the margins are not the same or the sales fall short, the scenario I consider is quite optimistic.

Lifetime gain is 40%, over 3 years, matching the best MF returns in that period.

Smallest 3 holdings were sold-off and some others have been trimmed to make way for the top-weighted new entry. The VP thread on this is simply brilliant. I was advising this to a friend who was asking for some ideas, checked the stock price later the same day and it was 10% up! Re-read the excellent thread again and the numbers just jumped out and hit me on the head! Single trade, no averaging, LT holding for 2-3 years or more or till it hits the evaluated valuation!

Thanks to Edward Lobo for the discussion on the new entrant Vipul. And to Bhavvesh for Manorama.

The two smallest parts of the PF have been taken out. Ganesh Benzoplast looks cheap but the growth triggers can take a while here, low downside risk but can test patience. Same for Gujarat Themis, as I have also commented on its thread.

Also, changed my mind about Borosil Renewables, better to book out than depend on margins of a price-taker, when manufacturing giants of China have only seen 2x share price increase since august. Priority will perhaps be given to solar power projects over solar manufacturing, esp. for material like glass. After little more than 1-2 quarters, the ride may get bumpy with limited upside after the huge run-up!

Vipul has seen amazing promoter buying and now preferential issue, while the capex continues, hope is that this translates into bottom line.

Manorama pops up in the screener for huge Gross block increase, after all they have finally executed on their IPO plans. Some part is still ongoing, overall there is delay due to the pandemic. Could be that the migration to main-board gives it a bump soon.

Overall 50% increase in PF, almost 3x in the past year, which gives CAGR of approx 20% returns, hence target achieved! Thanks to VP forum!

Note: The folio is very lopsided, (commodity-like) micro-caps should not be in such high weightage. That is inviting trouble! There are plenty of small, mid, even large-caps, discussed well on this forum, which are very worthy of investing, to spread the risk.

One should normally think twice about having more than 10-12% in such micro-caps. I believe the focus should be on quality of business with growth, and longevity of returns (safe compounders). I may need to balance/restructure soon.

What I do is different than what I say is since my current phase in risk/reward judgment, is for higher returns currently and bit lower priority for safety. As the thread name suggests this is not a sanskari PF Above all, thanks to VP forum!

PS: pay-ins are just 5% of current folio value. PF lifetime returns are just 25% CAGR.

Reduction in Kanchi, attended first ever sort of con-call, they first collected all questions and gave an amalgamated statement as reply. To me it sounded just like a normal high growth share prospect, nothing exceptional, hence reducing given commodity shock is quite possible.

Also reduced a bit of Laurus and Kopran.

Added other possible high growth shares mainly export-oriented auto sector, GNA and RACL. Focused bit on Shakti pumps since agriculture + solar may benefit from govt scheme offtake. Dynemic looks cheap compared to peers, and export orientation, expansion etc. Added to Manorama.

Overall life-time returns are approaching 30% CAGR.

I have not looked at the EV theme much actually. Did not seem that there are domestic manufacturers for this. Basics required are batteries, drive, build etc. Have not tracked auto ancillary as a sector since 3 years or so, since the overall auto slowdown began.

The typical vehicular battery manufacturers are already diversifying into lithium. Tata chem seems to be planning this in medium term.

Tata motors has good tech for build, Mahindra may do well, cheap is going to be better seller in India. Traditional 2 wheeler producers are managing the switch with ease. Maybe more plastics are deployed to extend range.

Drive is going to need copper, and there is only one for India. Who can specialize in electric motors, no clue mostly, maybe kirloskar?

I do not think we are going to go electric that fast, at least with domestic inputs. It is expensive, and pollution can be controlled by switching the cheaper to fix, static etc. users of carbon fuels, first. There are other efficient ways for mobility solutions also, ranging from several decades old electric rail/metro to dirt cheap e-rickshaws. Policy support for EV does not seem very logical.

Bajaj health makes a come-back, it is trading at quite nice valuation now, with good guidance and feedback from management every quarter, rather than some fancy pictures on slides which mean very little. Capex rolling along nicely and the long steady growth trendline should be maintained.

Bajaj steel added since it seems to be a good candidate for a changing business with exports starting to dominate and should get lucky with cotton cycle peaking soon. Issues with Chinese cotton from Xinjiang province will help the company sell to the rest-of-the-world.

Both companies have really long background and valuations are not bad right now.

Trimmed everything else, some more some less, to create space for the new entrants.

Philosophy is something like Vivek Gautam has mentioned, diversify enough, to take advantage of market serendipity, since you cannot be sure what rises and how fast. Safety is also added naturally.

Overall, folio is at peak valuation, added 7% in past month or so.

PS: There was a mistake with stoploss on Kanchi, it should be 1-2% higher weight otherwise.

No changes, except increase in weight of Bajaj Steel and Bajaj Healthcare, invested equal amounts in total, pulling out little from here and there.

PF is up 5% in past 3 weeks to peak valuation.

Feb 2020 till date, overall increase is 265%. (while Nifty 50, has gone from 12450 to 14800, a 19% increase)

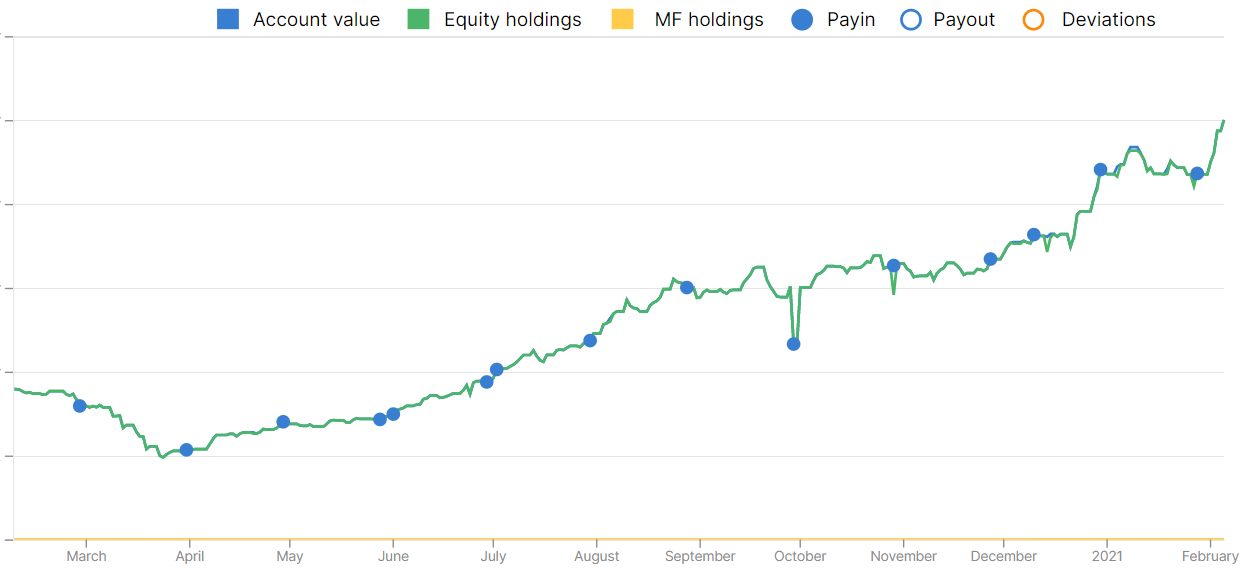

The pic below just shows the past exact one year.

PS: Bajaj healthcare saw huge volumes a few days after institutional meet about 2 weeks ago. First ever meet done by the company. 3.2% of listed shares got traded (delivery based), approx 20 Cr worth. Seems timing was to avoid disclosure as per new SEBI norms about such meetings and the deal was timed to avoid publication of shareholdings till next quarter. Only if seen with suspicious bent of thought, might be very innocently timed also. Overall seems not bad sign. Though several companies seem to show up in the public shareholdings and this triggers some suspicion. These have been constant sellers since almost 2 years and such concentrated holdings may explain the relatively stable prices seen in the overall trend.

Since some of companies I hold are not discussed on VP forum (viz. Vipul, Manorama, Bajaj Healthcare), some info on them might be useful for the community in general, so I will keep commenting here. The source is just a google search. Sorry, am too lazy to do a proper analysis for starting a thread on them.

Manorama Industries seems like a decent company with a long enough runway. The latest company presentation can be seen in screener.in, though I find the IPO presentation very useful to understand the company basics.

Yes, my style lacks depth and maybe it gains by reducing analysis-paralysis. The ones not discussed well, have a safe downside, being bought relatively cheap compared to the markets. At least no big red flags were seen superficially.